|

市场调查报告书

商品编码

1685953

结构性黏着剂:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Structural Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

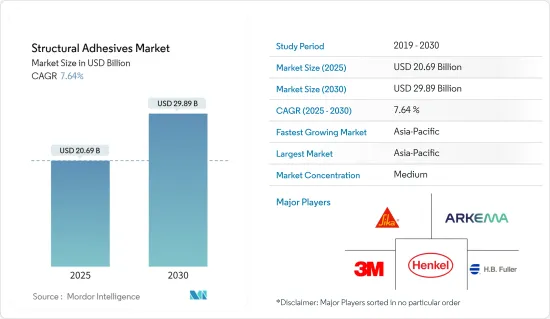

结构性黏着剂市场规模预计在 2025 年为 206.9 亿美元,预计到 2030 年将达到 298.9 亿美元,预测期内(2025-2030 年)的复合年增长率为 7.64%。

2020 年,市场受到了 COVID-19 的负面影响。然而,在建筑、汽车和风力发电等各个终端用户产业消费增加的推动下,2021年已显着復苏。

主要亮点

- 短期内,新兴经济体投资的增加以及全球建筑和汽车行业需求的不断增长可能会推动市场的发展。

- 然而,日益严重的环境和健康问题预计将阻碍市场成长。

- 加强对水下结构性黏着剂的研究可能会成为未来几年市场成长的机会。

- 亚太地区占市场主导地位,其中以中国消费最为突出。

结构性黏着剂市场趋势

建设产业需求增加

- 在建筑中,结构性黏着剂用于黏合能够承受负载和应力的材料。这些黏合剂具有优异的抗衝击性、断裂韧性和结构灵活性,并且不会影响黏合强度。

- 在建筑领域,结构性黏着剂可为混凝土、承重材料、铝和钢等金属、塑胶、工程木材等提供耐久性。结构性黏着剂不仅耐用,而且节能、美观。它还减少了维护需求。这些特性延长了建筑建筑幕墙和桥樑的生命週期。

- 建设产业使用的结构性黏着剂有丙烯酸结构性黏着剂、钢筋胶、锚固胶、注射胶、碳纤维加强胶、吊挂胶、硅胶结构性黏着剂等。

- 随着全球建设活动的活性化,预计预测期内对结构性黏着剂的需求将会增加。 2021 年全球建筑市场价值可能达到约 7.2 兆美元,2022 年成长率为 3.6%。

- 亚太地区建筑业是世界上最大的建筑业,由于人口增长、中产阶级的壮大和都市化,该行业正在健康地扩张。预计最高成长将来自亚太地区,主要受中国和印度住宅建筑市场扩张的推动。根据中国国家统计局的数据,2021 年全国建筑业产值为 25.92 兆元(约 4.3 兆美元),高于 2020 年的 23.27 兆元(约 3.62 兆美元)。

- 美国在北美建设产业中占有很大的份额。加拿大和墨西哥也对建筑业做出了巨大贡献。根据美国人口普查局的数据,2021年该国新建设将达到16,264.44亿美元,高于2020年的1,4,995.70亿美元。

- 因此,所有上述因素都可能对所研究市场的需求产生重大影响。

亚太地区占市场主导地位

- 2021年,亚太地区在全球结构性黏着剂市场占据主导地位。中国是世界上最大的结构性黏着剂消费国之一。

- 根据中国今年1月发布的五年规划,预计2022年中国建设产业的成长率将达到6%左右。中国计划增加装配式建筑的建设,以减少建筑工地的污染和废弃物。

- 此外,据国家发展和改革委员会称,中国政府已核准26 个基础设施计划,预计投资约 1,420 亿美元。这些计划目前正在进行中,预计将于2023年完工。

- 中国是世界上最大的汽车製造国。根据OICA预测,2021年该国汽车产量将达2,608万辆,较2020年的2,523万辆成长3%。预计汽车产量的成长将推动对结构性黏着剂,尤其是在高端汽车製造业。

- 此外,根据斯德哥尔摩国际和平研究所 (SIPRI) 的数据,中国是仅次于美国的世界第二大军费开支国,2021 年的军事开支预计将达到 2,930 亿美元。这比 2020 年增长了 4.7%。中国 2021 年的预算是「十四五」规划下的第一份预算,该规划将持续到 2025 年。

- 印度庞大的建筑业预计到2022年将成为世界第三大建筑市场。印度政府实施的包括智慧城市计划和2022年全民住宅在内的各项政策可望为低迷的建设产业带来提振。

- 汽车和航太部门是结构性黏着剂的其他重要使用者。根据 OICA 的数据,2021 年印度生产了约 4,399,112 辆汽车,比 2020 年的 3,381,819 辆成长 30%。

- 预计上述因素将在预测期内影响亚太地区对结构性黏着剂的需求。

结构性黏着剂产业概况

全球结构性黏着剂市场本质上是分散的,由各种国内和国际参与者组成。主要参与者包括汉高公司、西卡公司、3M、HB Fuller Company、阿科玛等(不分先后顺序)。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 调查前提条件

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 驱动程式

- 增加对亚太地区新兴经济体的投资

- 全球建筑和汽车产业的需求不断增长

- 限制因素

- 日益增长的环境和健康问题

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章 市场区隔

- 依树脂类型

- 环氧树脂

- 聚氨酯

- 丙烯酸纤维

- 氰基丙烯酸酯

- 甲基丙烯酸甲酯

- 其他树脂类型

- 按最终用户产业

- 建筑学

- 车

- 航太

- 风力发电

- 其他最终用户产业

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 义大利

- 法国

- 其他欧洲国家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争格局

- 合併、收购、合资、合作和协议

- 市场排名分析

- 主要企业策略

- 公司简介

- 3M

- Arkema

- Bondloc UK Ltd

- DuPont

- Engineered Bonding Solutions LLC

- Forgeway Ltd

- HB Fuller Company

- Henkel AG & Co. KGaA

- Huntsman International LLC

- Illinois Tool Works Inc.

- LG Chem

- Parker Hannifin Corp.

- Sika AG

- RS Industrial

第七章 市场机会与未来趋势

- 水下结构性黏着剂的发展

The Structural Adhesives Market size is estimated at USD 20.69 billion in 2025, and is expected to reach USD 29.89 billion by 2030, at a CAGR of 7.64% during the forecast period (2025-2030).

The market was negatively impacted by COVID-19 in 2020. However, it recovered significantly in 2021, owing to rising consumption from various end-user industries, such as construction, automotive, and wind energy.

Key Highlights

- Over the short term, the increasing investments in developing Asia-Pacific economies and increasing demand from the global construction and automotive sectors may drive the market studied.

- However, growing environmental and health concerns are expected to hinder the growth of the studied market.

- The growing research on underwater structural adhesives is likely to act as an opportunity for market growth in the future.

- Asia-Pacific dominated the market, with the most significant consumption recorded in China.

Structural Adhesives Market Trends

Increasing Demand from the Construction Industry

- In the construction sector, structural adhesives are used to bond materials to withstand loads or stresses. These adhesives offer good impact resistance, fracture toughness, and structural flexibility without affecting bond strength.

- In the construction sector, structural adhesives provide durability to concrete, load-bearing materials, metals such as aluminum and steel, plastics, engineered woods, etc. Apart from durability, structural adhesives are energy-efficient and aesthetically appealing. They also reduce the need for maintenance. These characteristics extend the life cycle of building facades and bridges.

- Some essential structural adhesives used in the construction industry include acrylic structural adhesives, steel glue, anchor glue, pouring glue, carbon fiber reinforcement glue, dry-hanging adhesives, and silicone structural adhesives.

- With growing construction activity worldwide, the demand for structural adhesives is projected to increase during the forecast period. The global construction market was valued at around USD 7.2 trillion in 2021 and is likely to witness a growth rate of 3.6% in 2022.

- The construction sector in the Asia-Pacific region is the largest in the world and is expanding at a healthy rate, owing to the rising population, increase in middle-class income, and urbanization. The highest growth for housing is also expected to be registered in the Asia-Pacific region, owing to the expanding housing construction markets in China and India. According to the National Bureau of Statistics of China, the output value of the construction works in the country in 2021 was CNY 25.92 trillion (~USD 4.03 trillion), increasing from CNY 23.27 trillion (~ USD 3.62 trillion) in 2020.

- The United States occupies a significant share of the North American construction industry. Canada and Mexico also contribute significantly to the construction sector. According to the US Census Bureau, the value of new construction put in place in the country accounted for USD 1,626,444 million in 2021, increasing from USD 1,499,570 million in 2020.

- Therefore, all the factors mentioned above are likely to impact the demand in the market studied significantly.

Asia-Pacific Region to Dominate the Market

- The Asia-Pacific region dominated the global structural adhesives market in 2021. China is one of the world's largest consumers of structural adhesives.

- According to China's Five-Year Plan, unveiled in January 2022, the country's construction industry is estimated to register a growth rate of approximately 6% in 2022. China plans to increase the construction of prefabricated buildings to reduce pollution and waste from construction sites.

- Moreover, as per the National Development and Reform Commission, the Chinese government approved 26 infrastructure projects with an estimated investment of around USD 142 billion. These projects are in progress and are estimated to be completed by 2023.

- China is the largest manufacturer of automobiles in the world. According to the OICA, the automotive production in the country reached 26.08 million in 2021, which increased by 3% compared to 25.23 million vehicles produced in 2020. The increase in automotive production is estimated to drive the demand for structural adhesives, especially in the high-end vehicle manufacturing sector.

- Furthermore, as per the Stockholm International Peace Research Institute (SIPRI), China, the world's second-largest spender on the military after the United States, allocated an estimated USD 293 billion to its military in 2021. This was an increase of 4.7% compared to 2020. The 2021 Chinese budget was the first under the 14th Five-Year Plan, which runs until 2025.

- India's massive construction sector is expected to become the world's third-largest construction market by 2022. Various policies implemented by the Indian government, such as the Smart Cities project and Housing for all by 2022, are expected to prove an impetus to the slowing construction industry.

- The automotive and aerospace sectors are the other significant users of structural adhesives. According to OICA, around 4,399,112 vehicles were produced in India in 2021, which increased by 30% compared to 3,381,819 units in 2020.

- The factors above are expected to affect the demand for structural adhesives in the Asia-Pacific region over the forecast period.

Structural Adhesives Industry Overview

The global structural adhesives market is partially fragmented in nature, with the presence of various international and domestic players. Some of the major players include Henkel AG & Co. KGaA, Sika AG, 3M, H.B. Fuller Company, and Arkema (not in any particular order).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increase in Investments in Developing Economies in Asia-Pacific

- 4.1.2 Increasing Demand from the Global Construction and Automotive Sectors

- 4.2 Restraints

- 4.2.1 Growing Environmental and Health Concerns

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 By Resin Type

- 5.1.1 Epoxy

- 5.1.2 Polyurethane

- 5.1.3 Acrylic

- 5.1.4 Cyanoacrylate

- 5.1.5 Methyl Methacrylate

- 5.1.6 Other Resin Types

- 5.2 By End-user Industry

- 5.2.1 Construction

- 5.2.2 Automotive

- 5.2.3 Aerospace

- 5.2.4 Wind Energy

- 5.2.5 Other End-user Industries

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers, Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 Bondloc UK Ltd

- 6.4.4 DuPont

- 6.4.5 Engineered Bonding Solutions LLC

- 6.4.6 Forgeway Ltd

- 6.4.7 H. B. Fuller Company

- 6.4.8 Henkel AG & Co. KGaA

- 6.4.9 Huntsman International LLC

- 6.4.10 Illinois Tool Works Inc.

- 6.4.11 LG Chem

- 6.4.12 Parker Hannifin Corp.

- 6.4.13 Sika AG

- 6.4.14 RS Industrial

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Research on Underwater Structural Adhesives

中性硅酮结构性黏着剂市场:按应用、通路和终端用户产业划分-2026-2032年全球预测

中性硅酮结构性黏着剂市场:按应用、通路和终端用户产业划分-2026-2032年全球预测 全球结构性黏着剂市场规模、份额、趋势和成长分析报告(2026-2034)

全球结构性黏着剂市场规模、份额、趋势和成长分析报告(2026-2034) 2026年全球结构性黏着剂市场报告按技术、应用、形式、安装方法和车辆类别分類的汽车车身结构黏合剂市场-全球预测,2026-2032年

2026年全球结构性黏着剂市场报告按技术、应用、形式、安装方法和车辆类别分類的汽车车身结构黏合剂市场-全球预测,2026-2032年 结构性黏着剂树脂、技术、基材、最终用户及地区划分)-2026-2033年产业预测

结构性黏着剂树脂、技术、基材、最终用户及地区划分)-2026-2033年产业预测 结构性黏着剂市场机会、成长要素、产业趋势分析及2026年至2035年预测

结构性黏着剂市场机会、成长要素、产业趋势分析及2026年至2035年预测 结构胶合剂市场-全球产业规模、份额、趋势、机会及预测(依树脂类型、基材、应用、地区及竞争细分,2020-2030 年)

结构胶合剂市场-全球产业规模、份额、趋势、机会及预测(依树脂类型、基材、应用、地区及竞争细分,2020-2030 年) 结构性黏着剂全球市场:需求与预测分析(2018-2034)2026-2032年结构性黏着剂市场(依基材、应用、技术及地区划分)

结构性黏着剂全球市场:需求与预测分析(2018-2034)2026-2032年结构性黏着剂市场(依基材、应用、技术及地区划分) 全球结构性黏着剂市场:按基材、树脂、技术、应用、地区划分 - 预测至 2029 年

全球结构性黏着剂市场:按基材、树脂、技术、应用、地区划分 - 预测至 2029 年