|

市场调查报告书

商品编码

1687171

杀软体动物剂:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Molluscicide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

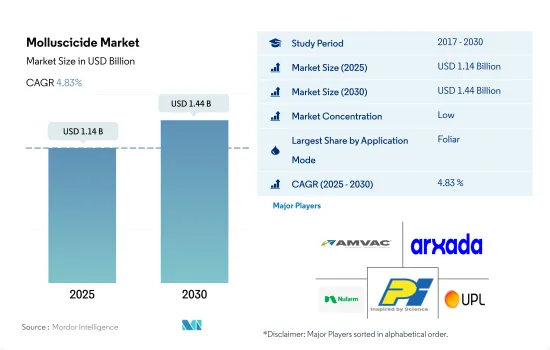

杀软体动物剂市场规模预计在 2025 年将达到 11.4 亿美元,预计到 2030 年将达到 14.4 亿美元,预测期内(2025-2030 年)的复合年增长率为 4.83%。

蜗牛数量的增加和农作物损失的增加推动了对杀软体动物剂的需求。

- 在全球范围内,杀软体动物剂的使用范围不断扩大,使用方式也多种多样。 2022年叶面喷布占整个杀软体动物剂市场的53.7%,占主要份额。该行业对杀软体动物剂的需求是由于蜗牛侵扰的增加而推动的,特别是在冬季和雨季,这需要提高产量并减少因蜗牛和蛞蝓造成的损失。

- 由于杀软体动物剂在土壤处理中的有效性,预计预测期内(2023-2029 年)土壤处理中对杀软体动物剂的需求将达到 4.8% 的复合年增长率。用于土壤处理的杀螺剂主要有四聚乙醛、磷酸亚铁、甲硫威、乙二胺四乙酸铁钠、氯硝柳胺等。

- 杀软体动物剂市场的化学灌溉部分预计在 2023 年至 2029 年期间的复合年增长率为 4.6%。此部分的增长可归因于透过滴灌系统增加灌溉面积,以及借助这些作物的水资源管理,使用化学药品对抗蜗牛和蛞蝓的趋势日益增长。

- 预测期内(2023-2029 年),熏蒸市场价值预计将成长 180 万美元。预计市场成长将受到农民和农业专业人士对软体动物侵扰造成的经济损失的认识不断提高以及熏蒸采用率不断上升的推动。

- 因此,蜗牛侵扰增加、灌溉面积增加和作物损失增加等因素正在推动对杀软体动物剂的需求。预测期内,即 2023-2029 年,全球杀软体动物剂市场预计将以 4.4% 的复合年增长率成长。

南美洲主导全球杀软体动物剂市场

- 蛞蝓和蜗牛造成的农作物损害会导致农作物产量严重损失,并对农民造成负面的经济影响。这导致对能够针对蜗牛并保护作物免受损害的有效杀软体动物剂的需求增加。

- 全球杀软体动物剂市场以南美洲为主,2022年的市场占有率为36.2%。影响南美国家农业的主要蜗牛包括非洲大蜗牛(Achatina fulica)和福寿螺(Pomacea canaliculata)。这些入侵物种以其旺盛的食慾和快速的繁殖而闻名,对多种作物构成了严重威胁。这些蜗牛造成的产量损失是巨大的,水稻、玉米和蔬菜等作物尤其容易受到影响。蜗牛以幼苗、叶子甚至成熟植物为食,降低作物的品质和数量。

- 2022 年,亚太地区以 26.0%的市场占有率位居第二。亚洲蜗牛养殖的失败是由于蜗牛破坏了正在生长的水稻作物,造成了严重的经济影响,因为水稻作物被认为是最重要的粮食和农业收入来源。福寿螺(Pomacea canaliculata)已引入几个亚洲国家,并意外地成为了水稻种植的害虫。大多数农民依靠化学控制,包括杀软体动物剂,也依赖综合蜗牛管理方法。

- 主要作物中蜗牛和蛞蝓侵扰的增加预计将推动全球杀软体动物剂市场的发展,预计在预测期内(2023-2029 年)的复合年增长率将达到 4.9%。

全球杀软体动物剂市场趋势

杀软体动物剂对作物生产的威胁越来越大,导致杀软体动物剂的使用增加

- 全球每公顷杀虫剂平均消费量从2017年的418.0克/公顷增加至2022年的425.5克/公顷。亚太地区每公顷杀虫剂消费量最高,2022年将达152.69公克/公顷。国际稻米研究所称,福寿螺对亚太国家水稻生产构成重大威胁,因为它会从基部折断稻秆,进而毁坏整株稻株,使产量减少高达50%,尤其是在灌溉稻田。

- 欧洲将成为单位面积杀软体动物肥料的第二消费量,2022年使用杀软体动物肥料的量为124.32公克/公顷。南美洲是单位面积杀软体动物剂的第三大消费国,2022年使用杀软体动物剂的量为110.41克/公顷。非洲大蜗牛(Achatina fulica)和福寿螺(Pomacea canaliculata)都是入侵物种,以其贪婪的食慾和快速的繁殖而闻名,对一系列作物构成了严重威胁。这些蜗牛造成的农作物损失庞大,水稻、玉米和蔬菜等作物尤其容易受到影响。

- 北美洲每公顷土地消耗的杀软体动物剂为37.2公克,明显低于其他地区。然而,Deroceras reticulatum 是美国最常见的入侵玉米和大豆的蛞蝓种类。蛞蝓吃掉玉米和大豆作物的叶子,会阻碍生长季节后期座舱罩的发育,从而降低产量。此类攻击需要有效的管理,包括使用杀软体动物剂。

四聚乙醛能够有效控制多种作物(包括田间作物和园艺作物)中的蜗牛和蛞蝓,这可能会提高四聚乙醛的价格。

- 杀软体动物剂在农业和园艺中至关重要,可以有效控制蜗牛和蛞蝓等软体动物,这些动物会对农作物和观赏植物造成巨大破坏。这些杀虫剂在保护植物健康、防止产量损失以及维持花园和景观的美丽方面发挥着重要作用。

- 甲醛是一种醛类化合物杀软体动物剂。它被广泛用于控制蜗牛和蛞蝓等农业和园艺作物的常见害虫。 2022 年的价格为每吨 52,500 美元。金属醛可有效控制多种类型的蜗牛和蛞蝓,包括常见的花园蜗牛、灰蛞蝓和黑蛞蝓。

- 这些软体动物会对多种作物造成广泛的破坏,包括蔬菜、水果、观赏植物和田间作物。甲醛作为杀软体动物剂的作用机制是诱发蜗牛和蛞蝓的过度活跃和协调性丧失。一旦摄入,甲醛就会扰乱神经系统,导致运动增加和无法正常进食。结果,害虫最终会脱水并受到甲醛的侵害。

- 磷酸铁是一种杀软体动物剂,用于农业和园艺中控制蜗牛和蛞蝓。它也被称为磷酸铁,是一种天然化合物。 2022 年的价格为每吨 52,000 美元。

- 磷酸铁可以有效控制多种类型的蜗牛和蛞蝓,包括普通花园蜗牛、灰蛞蝓和黑蛞蝓。这些软体动物是常见的害虫,会对农作物、蔬菜、水果、观赏植物和各种其他栽培植物造成破坏。

灭螺剂产业概况

杀软体动物剂市场较为分散,前五大公司占了23.27%的市场。市场的主要企业是:American Vanguard Corporation、Arxada、Nufarm Ltd、PI Industries 和 UPL Limited(按字母顺序排列)。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章执行摘要和主要发现

第二章 报告要约

第 3 章 简介

- 研究假设和市场定义

- 研究范围

- 调查方法

第四章 产业主要趋势

- 每公顷农药消费量

- 有效成分价格分析

- 法律规范

- 澳洲

- 中国

- 法国

- 德国

- 印度

- 印尼

- 义大利

- 日本

- 缅甸

- 荷兰

- 巴基斯坦

- 菲律宾

- 俄罗斯

- 西班牙

- 泰国

- 乌克兰

- 英国

- 越南

- 价值链与通路分析

第五章 市场区隔

- 使用模式

- 化学灌溉

- 叶面喷布

- 熏蒸

- 土壤处理

- 作物类型

- 经济作物

- 水果和蔬菜

- 粮食

- 豆类和油籽

- 草坪和观赏植物

- 地区

- 非洲

- 按国家

- 南非

- 非洲其他地区

- 亚太地区

- 按国家

- 澳洲

- 中国

- 印度

- 印尼

- 日本

- 缅甸

- 巴基斯坦

- 菲律宾

- 泰国

- 越南

- 其他亚太地区

- 欧洲

- 按国家

- 法国

- 德国

- 义大利

- 荷兰

- 俄罗斯

- 西班牙

- 乌克兰

- 英国

- 其他欧洲国家

- 北美洲

- 按国家

- 加拿大

- 墨西哥

- 美国

- 北美其他地区

- 南美洲

- 按国家

- 阿根廷

- 巴西

- 智利

- 其他南美国家

- 非洲

第六章 竞争格局

- 主要策略趋势

- 市场占有率分析

- 业务状况

- 公司简介

- American Vanguard Corporation

- Arxada

- Liphatech Inc.

- Mitsui & Co. Ltd(Certis Belchim)

- Nufarm Ltd

- PI Industries

- UPL Limited

- W. Neudorff GmbH KG

第七章:执行长的关键策略问题

第 8 章 附录

- 世界概况

- 概述

- 五力分析框架

- 全球价值链分析

- 市场动态(DRO)

- 资讯来源和进一步阅读

- 图片列表

- 关键见解

- 资料包

- 词彙表

简介目录

Product Code: 55939

The Molluscicide Market size is estimated at 1.14 billion USD in 2025, and is expected to reach 1.44 billion USD by 2030, growing at a CAGR of 4.83% during the forecast period (2025-2030).

The demand for molluscicide is driven by increasing snail infestation and rising crop losses

- Globally, the use of molluscicide is expanding in various application modes. Foliar holds the major share value, accounting for 53.7% of the total molluscicide market in 2022. Demand for molluscicides in this segment is driven by increased snail infestation, particularly during the winter and rainy periods, and a need to improve yields and reduce losses due to snails and slugs.

- The demand for molluscicide chemicals in soil treatment methods is expected to register a CAGR of 4.8% during the forecast period (2023-2029) due to the effectiveness of the soil treatment method for molluscicides. The main molluscicide products used for the treatment of soil are metaldehyde, iron phosphate, methiocarb, sodium ferric ethylenediaminetetraacetic acid (EDTA), and niclosamide.

- The chemigation segment in the molluscicide market is expected to grow at 4.6% CAGR from 2023 to 2029. The growth of this segment can be attributed to an increased area under drip irrigation systems, as well as a growing trend of the use of chemicals against snails or slugs using water management on these crops.

- The fumigation method's market value is expected to increase by USD 1.8 million during the forecast period (2023-2029). The market growth is expected to be stimulated by a growing awareness of the economic losses from mollusk damage in farmers and agricultural professionals, as well as the rising adoption of fumigation.

- Therefore, factors such as rising snail infestation, the growing area under irrigation, and increasing crop losses are driving the demand for molluscicide. The global molluscicide market is expected to grow at 4.4% CAGR during the forecast period from 2023 to 2029.

South America dominated the global molluscicide market

- Crop damage caused by slugs and snails can lead to a significant loss in crop yield as well as a negative economic impact on farmers. Consequently, the demand for effective molluscicides that are capable of targeting snails and protecting crops from damage is increasing.

- South America dominated the global molluscicide market, accounting for a market share of 36.2% in 2022. Some of the major snails that affect agriculture in South American countries include the giant African snail ( Achatina fulica) and the golden apple snail ( Pomacea canaliculata). These invasive species are known for their voracious appetite and ability to rapidly reproduce, posing a serious threat to various crops. The yield losses caused by these snails can be substantial, with crops like rice, corn, and vegetables being particularly vulnerable. The snails feed on young seedlings, foliage, and even mature plants, leading to reduced crop quality and quantity.

- Asia-Pacific accounted for the second-largest market share of 26.0% in 2022. Snail farming failed in Asia because snails were destroying the growing rice crops, which caused them severe economic consequences as rice farms were considered their most significant source of food and farm income. The golden apple snail, Pomacea canaliculata, had been introduced to several Asian countries, where it unexpectedly developed into a pest for rice crops. Most farmers have resorted to chemical control, which includes the use of molluscicides, and have also resorted to integrated snail management practices.

- The increasing snail and slug infestations in major crops will drive the molluscicides market globally, which is anticipated to register a CAGR of 4.9% during the forecast period (2023-2029).

Global Molluscicide Market Trends

Increasing threat to crop production due to molluscicides is increasing the usage

- The global average consumption of molluscicides per hectare increased from 418.0 grams per hectare in 2017 to 425.5 grams per hectare in 2022. Asia-Pacific recorded the highest per-hectare consumption of molluscicides, with 152.69 grams per hectare in 2022. Golden apple snails are the major threat to rice production in Asia-Pacific countries as they cut the rice stem at the base, destroying the whole plant and leading to annual yield losses of up to 50%, especially in irrigated rice fields, according to the International Rice Research Institute.

- Europe is the second-largest per-hectare consumer, with 124.32 grams per hectare of molluscicides in 2022. South America is the third-largest per-hectare consumer of molluscicides, with 110.41 grams per hectare of land in 2022. The giant African snail ( Achatina fulica) and the golden apple snail ( Pomacea canaliculata) are invasive species known for their voracious appetite and ability to reproduce rapidly, posing a serious threat to various crops. The yield losses caused by these snails can be substantial, with crops like rice, corn, and vegetables being particularly vulnerable.

- North America consumed 37.2 grams of molluscicides per hectare of land, which is significantly less compared to other regions. However, Deroceras reticulatum is one of the most invasive slug species of maize and soybean in the United States. At later growth stages, corn and soybean defoliation by slugs can lead to delayed canopy development and subsequent lower yields. Such attacks call for the need for effective management, which includes the use of molluscicides.

Effectiveness of the metaldehyde in controlling snails and slugs in various crops like field crops and horticultural crops may increase the price of it

- Molluscicides are essential in agriculture and horticulture for effectively controlling mollusks like snails and slugs, which can cause significant damage to crop and ornamental plants. These pesticides play a vital role in protecting plant health, preventing yield losses, and maintaining the aesthetic appeal of gardens and landscapes.

- Metaldehyde is a molluscicide belonging to the chemical class of aldehydes. It is widely used to control snails and slugs, which are common pests in agricultural and horticultural crops. It was priced at USD 52.5 thousand per metric ton in 2022. Metaldehyde effectively controls a variety of snail and slug species, including common garden snails, grey field slugs, and black field slugs.

- These mollusks can cause significant damage to a wide range of crops, including vegetables, fruits, ornamental plants, and field crops. The mode of action of metaldehyde as a molluscicide involves inducing hyperactivity and loss of coordination in snails and slugs. When ingested, metaldehyde disrupts their nervous systems, leading to increased movement and a loss of their ability to feed properly. This eventually results in the pests becoming dehydrated and succumbing to the effects of metaldehyde.

- Ferric phosphate is a molluscicide used to control snails and slugs in agricultural and horticultural settings. It is also known as iron phosphate and is a naturally occurring compound. It was priced at USD 52.0 thousand per metric ton in 2022.

- Ferric phosphate effectively controls a variety of snail and slug species, including common garden snails, grey field slugs, and black field slugs. These mollusks are common pests that can cause damage to crops, vegetables, fruits, ornamental plants, and various other cultivated plants.

Molluscicide Industry Overview

The Molluscicide Market is fragmented, with the top five companies occupying 23.27%. The major players in this market are American Vanguard Corporation, Arxada, Nufarm Ltd, PI Industries and UPL Limited (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 Australia

- 4.3.2 China

- 4.3.3 France

- 4.3.4 Germany

- 4.3.5 India

- 4.3.6 Indonesia

- 4.3.7 Italy

- 4.3.8 Japan

- 4.3.9 Myanmar

- 4.3.10 Netherlands

- 4.3.11 Pakistan

- 4.3.12 Philippines

- 4.3.13 Russia

- 4.3.14 Spain

- 4.3.15 Thailand

- 4.3.16 Ukraine

- 4.3.17 United Kingdom

- 4.3.18 Vietnam

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Application Mode

- 5.1.1 Chemigation

- 5.1.2 Foliar

- 5.1.3 Fumigation

- 5.1.4 Soil Treatment

- 5.2 Crop Type

- 5.2.1 Commercial Crops

- 5.2.2 Fruits & Vegetables

- 5.2.3 Grains & Cereals

- 5.2.4 Pulses & Oilseeds

- 5.2.5 Turf & Ornamental

- 5.3 Region

- 5.3.1 Africa

- 5.3.1.1 By Country

- 5.3.1.1.1 South Africa

- 5.3.1.1.2 Rest of Africa

- 5.3.2 Asia-Pacific

- 5.3.2.1 By Country

- 5.3.2.1.1 Australia

- 5.3.2.1.2 China

- 5.3.2.1.3 India

- 5.3.2.1.4 Indonesia

- 5.3.2.1.5 Japan

- 5.3.2.1.6 Myanmar

- 5.3.2.1.7 Pakistan

- 5.3.2.1.8 Philippines

- 5.3.2.1.9 Thailand

- 5.3.2.1.10 Vietnam

- 5.3.2.1.11 Rest of Asia-Pacific

- 5.3.3 Europe

- 5.3.3.1 By Country

- 5.3.3.1.1 France

- 5.3.3.1.2 Germany

- 5.3.3.1.3 Italy

- 5.3.3.1.4 Netherlands

- 5.3.3.1.5 Russia

- 5.3.3.1.6 Spain

- 5.3.3.1.7 Ukraine

- 5.3.3.1.8 United Kingdom

- 5.3.3.1.9 Rest of Europe

- 5.3.4 North America

- 5.3.4.1 By Country

- 5.3.4.1.1 Canada

- 5.3.4.1.2 Mexico

- 5.3.4.1.3 United States

- 5.3.4.1.4 Rest of North America

- 5.3.5 South America

- 5.3.5.1 By Country

- 5.3.5.1.1 Argentina

- 5.3.5.1.2 Brazil

- 5.3.5.1.3 Chile

- 5.3.5.1.4 Rest of South America

- 5.3.1 Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 American Vanguard Corporation

- 6.4.2 Arxada

- 6.4.3 Liphatech Inc.

- 6.4.4 Mitsui & Co. Ltd (Certis Belchim)

- 6.4.5 Nufarm Ltd

- 6.4.6 PI Industries

- 6.4.7 UPL Limited

- 6.4.8 W. Neudorff GmbH KG

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

软体动物控製剂市场:2026-2032年全球市场预测(依活性成分类型、製剂类型、作用机制、应用及通路划分)

软体动物控製剂市场:2026-2032年全球市场预测(依活性成分类型、製剂类型、作用机制、应用及通路划分) 南美洲杀软体动物剂:市场占有率分析、产业趋势与统计、成长预测(2026-2031 年)

南美洲杀软体动物剂:市场占有率分析、产业趋势与统计、成长预测(2026-2031 年) 2026年全球生物杀软体动物剂市场报告

2026年全球生物杀软体动物剂市场报告 生物软体动物杀虫剂市场-全球产业规模、份额、趋势、机会、预测:按类型、应用、地区和竞争格局划分,2021-2031年杀软体动物剂市场-全球产业规模、份额、趋势、机会和预测(按类型、形式、应用、地区和竞争细分,2020-2030 年)亚太杀软体动物剂市场:市场占有率分析、产业趋势与成长预测(2025-2030 年)欧洲杀软体动物剂市场:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)

生物软体动物杀虫剂市场-全球产业规模、份额、趋势、机会、预测:按类型、应用、地区和竞争格局划分,2021-2031年杀软体动物剂市场-全球产业规模、份额、趋势、机会和预测(按类型、形式、应用、地区和竞争细分,2020-2030 年)亚太杀软体动物剂市场:市场占有率分析、产业趋势与成长预测(2025-2030 年)欧洲杀软体动物剂市场:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年) 软体动物驱除剂市场:各类别,不同形态,各用途,各地区,机会,预测,2018年~2032年

软体动物驱除剂市场:各类别,不同形态,各用途,各地区,机会,预测,2018年~2032年