|

市场调查报告书

商品编码

1687327

抽水蓄能发电:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Pumped Hydro Storage - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

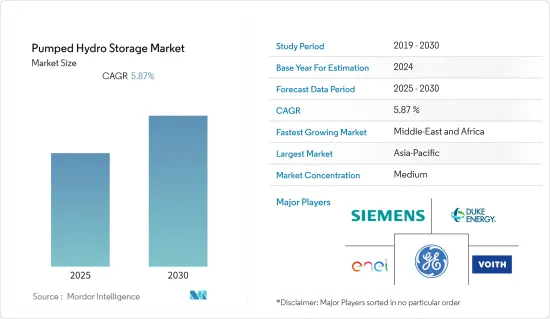

预计预测期内抽水蓄能发电市场将以 5.87% 的复合年增长率成长。

由于供应链中断,COVID-19 严重打击了抽水蓄能市场。然而,市场在 2022 年復苏。

主要亮点

- 在预测期内,PHS 市场预计将受到可变再生能源来源整合和维持电网稳定性需求的推动。此外,预计政府逐步淘汰石化燃料的目标将在预测期内推动市场成长。

- 然而,在预测期内,市场可能会受到 PHS计划的环境和社会影响以及其他能源储存技术日益激烈的竞争的影响。

- 目前正在研究几种新的 PSH 技术。预计这将加速PSH技术在能源储存的开发和利用,同时降低未来的成本和不利的环境影响,创造许多机会。此外,根据国际水力发电协会的数据,预计到 2030 年将有近 240 吉瓦的 PSH计划运作。

- 亚太地区是抽水蓄能发电的最大市场,2020 年年新增装置容量最高,预计在主要推动下将持续维持成长轨迹。

抽水蓄能发电市场趋势

闭合迴路部分预计将占据市场主导地位。

- 在闭合迴路系统中,建造一个抽水蓄能电站,并人工建造一个或两个水库。储存大量能量的唯一方法是将一大片水体放置在相对较靠近第二片水体的位置,并且尽可能高。在某些地方,这种情况是自然发生的。在某些地方,其中一个或两个水体都是人造的。抽水蓄能係统的能量密度相对较低,因此需要水库之间有较大的高程差或较大的流量。

- 闭合迴路抽水蓄能具有高度的灵活性、可靠性和功率输出。闭合迴路抽水蓄能係统对环境的影响比开放回路抽水蓄能係统小,因为它们不与现有的河流系统相连。此外,它们可以安装在需要电网支援的地方,而不需要位于现有河流或溪流附近。

- 闭合迴路系统预计在未来几年将出现显着增长,因为它们不会干扰现有的河流系统和水流,因此在获得营运许可证和许可方面更有把握。根据美国能源局(DOE)太平洋西北国家实验室(PNNL)的数据,近年来闭合迴路水力发电系统的许可证申请和预许可证数量大幅增加。

- 美国等国家越来越多地采用闭合迴路抽水发电工程,这为寻求进入市场的开发商提供了双赢的商业前景。

- 例如,苏门答腊抽水蓄能计画是一个500MW的水力发电发电工程。该计划计划在印尼西苏门答腊省实施,目前处于公告阶段。该开发计划分阶段进行。计划预计将于2024年开始建设,并于2027年开始商业运营。计划成本预计约为11.07亿美元。

- 由于所有这些因素,闭合迴路部分预计将在未来几年引领市场。

亚太地区可望主导市场

- 根据国际水力发电协会的数据,截至2021年,亚太地区水力发电储存容量约为685吉瓦,其中中国和日本占该地区大部分份额。 2021年水力发电装置容量约为2,385千万瓦。

- 随着亚太地区逐渐摆脱对石化燃料的依赖,可再生能源、水力和抽水储存建设正在成长,尤其是在中国、日本、东协地区、韩国和印度。

- 中国也宣布了到 2060 年实现碳中和、到 2025 年煤炭消费达到高峰的计画。中国于 2021 年 9 月发布的中长期抽水蓄能发展规划也设定了雄心勃勃的目标,即到 2025 年总设备容量至少达到 62 兆瓦,到 2030 年达到 120 吉瓦。这导致可再生能源领域的投资增加,2021 年将新增约 21 吉瓦的水力发电装置容量,其中包括鸡西计划最后四台机组的 1.2 吉瓦抽水蓄能。

- 以及装置容量为1.8兆瓦的鸡西抽水蓄能电站,这是中国最大的抽水发电工程,预计耗资16.1亿美元。它是由中国国家电网公司(SGCC)的子公司国网新源公司开发的。

- 此外,东南亚水力发电、抽水蓄能发电市场发展活跃。然而,由于新冠疫情造成的持续封锁,许多计划被推迟。不过,世界银行召开高峰会,鼓励南亚国家开放并投资永续水力发电。

- 例如,2021年9月,印尼宣布兴建首个抽水蓄能电站。由世界银行支持的计划Upper Cisokan PSH 将位于雅加达和万隆之间,预计发电容量为 1,040 兆瓦。它提供了为该地区供电所需的系统灵活性。

- 同样,韩国水电工业协会宣布在抱川、洪川和永同建设三个总合装置容量为 1.8 吉瓦的新计画,计划于 2034 年完工。

- 由于这些原因,预计未来几年亚太地区将引领抽水蓄能发电市场。

抽水蓄能发电产业概况

抽水蓄能市场相当分散。市场的主要企业包括通用电气公司、西门子股份公司、Enel SpA、杜克能源公司和福伊特有限公司。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究范围

- 市场定义

- 调查前提

第二章调查方法

第三章执行摘要

第四章 市场概述

- 介绍

- 抽水蓄能发电装置容量及至2028年预测(单位:GW)

- 2028年水力发电装置容量及预测(单位:吉瓦)

- 水力发电量(TWh,2013-2021)

- 近期趋势和发展

- 政府法规和政策

- 市场动态

- 驱动程式

- 限制因素

- 供应链分析

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 抽水能源储存系统。

第五章市场区隔

- 按类型

- 开放回路

- 闭合迴路

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 南美洲

- 中东和非洲

第六章竞争格局

- 併购、合资、合作与协议

- 主要企业策略

- 公司简介

- Operators

- Duke Energy Corporation

- EON SE

- Enel SpA

- Electricite de France SA(EDF)

- Iberdrola SA

- Technology Providers

- General Electric Company

- Siemens AG

- Andritz AG

- Mitsubishi Heavy Industries Ltd

- Voith GmbH & Co. KGaA

- Ansaldo Energia SpA

- Operators

第七章 市场机会与未来趋势

简介目录

Product Code: 61332

The Pumped Hydro Storage Market is expected to register a CAGR of 5.87% during the forecast period.

Due to supply chain disruptions, COVID-19 hurt the pumped hydro storage market. However, the market rebounded in 2022.

Key Highlights

- During the forecast period, the PHS market is expected to be driven by the integration of variable renewable energy sources and the need to keep the grid stable. Furthermore, increasing government targets to phase out fossil fuels will likely aid the market's growth during the forecast period.

- However, during the forecast period, the market studied is likely affected by the environmental and social effects of PHS projects and the growing competition from other energy storage technologies.

- Several new PSH technologies are being worked on right now. This is expected to speed up the development and use of PSH technology for energy storage while lowering costs and negative effects on the environment in the future, creating several opportunities. Further, as per the International Hydropower Association, nearly 240 GW of PSH projects will likely come online by 2030.

- Asia-Pacific turned out to be the largest market for pumped hydro storage, as it achieved the highest annual increase in capacity during 2020, continuing the growth trajectory primarily driven by China.

Pumped Hydro Storage Market Trends

Closed-loop Segment Expected to Dominate the Market

- In closed-loop systems, pumped hydro storage plants are created, in which one or both reservoirs are artificially built, and no natural inflows of water are involved with either reservoir. The only way to store a substantial amount of energy is by locating a large body of water relatively near the second body of water but as high above as possible. In some places, this happens naturally. In others, one or both bodies of water are man-made. The moderately low energy density of pumped storage systems entails either significant differences in height or large flows between reservoirs.

- Closed-loop pumped hydro storage offers high flexibility, reliability, and power output. Since closed-loop pumped-hydro systems are not connected to existing river systems, their impact on the environment is less compared to open-loop pumped-hydro storage systems. Moreover, they can be located where support for the grid is required and therefore do not need to be positioned near an existing river.

- Over the coming years, closed-loop systems are likely to witness significant growth because of the greater certainty in gaining an operating license or permit since they do not interfere with the existing river systems or any water streams. As per the Pacific Northwest National Laboratory (PNNL) under the US Department of Energy (DOE), the number of licensing applications and preliminary permits for closed-loop pumped hydro storage systems has significantly increased in recent years.

- The growing implementation of closed-loop pumped hydro storage projects in countries like the US can institute a favorable business scenario for developers looking to expand their market presence.

- For instance, Sumatera Pump Storage is a 500 MW hydropower project. It is planned in West Sumatra, Indonesia. The project is currently in its announced stage. It will be developed in a single phase. The project's construction is likely to commence in 2024 and is expected to enter commercial operation in 2027. The project cost is expected to be around USD 1.107 billion.

- Due to all of these factors, the close-loop segment is expected to lead the market over the next few years.

Asia-Pacific Expected to Dominate the Market

- According to the International Hydropower Association, as of 2021, Asia-Pacific had around 685 GW of installed hydro storage capacity, with China and Japan accounting for the majority share in the region. In 2021, the installed hydropower capacity was about 23.85 GW.

- As Asia and the Pacific continue to move away from fossil fuels, renewable energy, hydropower, and pumped hydro storage facilities are being built, especially in China, Japan, the ASEAN region, South Korea, and India.

- Furthermore, China announced its plan to become carbon neutral by 2060 and reach peak coal consumption by 2025. Besides China's mid- and long-term plans for pumped storage hydropower development, published in September 2021, it set out ambitious targets to reach a total installed capacity of at least 62 MW by 2025 and 120 GW by 2030. This led to increased investment in the renewable sector, and in 2021, around 21 GW of new hydropower was installed, including 1.2 GW of pumped storage from the last four units of the Jixi project.

- Also, the 1.8 GW Jixi Pumped Storage Power Station is the largest pumped hydro storage project, costing an estimated USD 1.61 billion. It was developed by the State Grid Xinyuan Company, a subsidiary company of the State Grid Corporation of China (SGCC).

- Furthermore, South-East Asia witnessed significant development in the hydropower and pumped hydro storage markets. However, many projects were delayed due to persistent lockdowns due to the COVID-19 pandemic. However, the World Bank held a summit to encourage South Asian nations to unlock and invest in sustainable hydropower.

- For instance, in September 2021, Indonesia announced its first pumped storage plant. The World Bank-supported project, Upper Cisokan PSH, is expected to be 1,040 MW and located between Jakarta and Bandung. It will provide necessary system flexibility to the electricity in the region.

- Similarly, the South Korean Hydropower Industry Association announced the construction of three new projects with a total capacity of 1.8 GW in Pocheon, Hongcheon, and Yeongdong, which are set to be completed by 2034.

- Due to the above reasons, it is expected that Asia-Pacific will lead the pumped hydro storage market over the next few years.

Pumped Hydro Storage Industry Overview

The pumped hydro storage market is moderately fragmented. Some of the key players in the market include (not in particular order) General Electric Company, Siemens AG, Enel SpA, Duke Energy Corporation, and Voith GmbH & Co. KGaA, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Pumped Hydro Installed Capacity and Forecast in GW, till 2028

- 4.3 Hydro Power Installed Capacity and Forecast in GW, till 2028

- 4.4 Hydroelectricity Generation in TWh, 2013-2021

- 4.5 Recent Trends and Developments

- 4.6 Government Policies and Regulations

- 4.7 Market Dynamics

- 4.7.1 Drivers

- 4.7.2 Restraints

- 4.8 Supply Chain Analysis

- 4.9 Porter's Five Forces Analysis

- 4.9.1 Bargaining Power of Suppliers

- 4.9.2 Bargaining Power of Consumers

- 4.9.3 Threat of New Entrants

- 4.9.4 Threat of Substitutes Products and Services

- 4.9.5 Intensity of Competitive Rivalry

- 4.10 Cost of Pumped Hydro Energy Storage System

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Open-loop

- 5.1.2 Closed-loop

- 5.2 Geography

- 5.2.1 North America

- 5.2.2 Europe

- 5.2.3 Asia-Pacific

- 5.2.4 South America

- 5.2.5 Middle-East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Operators

- 6.3.1.1 Duke Energy Corporation

- 6.3.1.2 EON SE

- 6.3.1.3 Enel SpA

- 6.3.1.4 Electricite de France SA (EDF)

- 6.3.1.5 Iberdrola SA

- 6.3.2 Technology Providers

- 6.3.2.1 General Electric Company

- 6.3.2.2 Siemens AG

- 6.3.2.3 Andritz AG

- 6.3.2.4 Mitsubishi Heavy Industries Ltd

- 6.3.2.5 Voith GmbH & Co. KGaA

- 6.3.2.6 Ansaldo Energia SpA

- 6.3.1 Operators

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

02-2729-4219

+886-2-2729-4219

抽水蓄能水力发电市场:2026-2032 年全球市场预测,计划开发阶段、容量范围、最终用户、技术类型和应用划分。

抽水蓄能水力发电市场:2026-2032 年全球市场预测,计划开发阶段、容量范围、最终用户、技术类型和应用划分。 2026年全球抽水蓄能市场报告

2026年全球抽水蓄能市场报告 抽水蓄能市场-全球产业规模、份额、趋势、机会及预测(依系统、应用、区域及竞争格局划分,2021-2031年)大型能源储存系统市场(按储能技术、容量范围、持续时间、所有权类型、配置、应用和最终用户划分)-2026年至2032年全球预测

抽水蓄能市场-全球产业规模、份额、趋势、机会及预测(依系统、应用、区域及竞争格局划分,2021-2031年)大型能源储存系统市场(按储能技术、容量范围、持续时间、所有权类型、配置、应用和最终用户划分)-2026年至2032年全球预测 抽水蓄能水电市场规模、份额及成长分析(按类型、储能容量、抽水蓄能机组容量、计划类型、最终用户及地区划分)-2026-2033年产业预测

抽水蓄能水电市场规模、份额及成长分析(按类型、储能容量、抽水蓄能机组容量、计划类型、最终用户及地区划分)-2026-2033年产业预测 抽水蓄能水力发电市场预测至2032年:按类型、容量、应用、最终用户和地区分類的全球分析

抽水蓄能水力发电市场预测至2032年:按类型、容量、应用、最终用户和地区分類的全球分析 抽水蓄能发电市场(按类型和地区划分)

抽水蓄能发电市场(按类型和地区划分) 亚太地区抽水蓄能:市场占有率分析、产业趋势与成长预测(2025-2030 年)北美抽水蓄能能源:市场占有率分析、产业趋势与成长预测(2025-2030)南美洲抽水蓄能储能:市场占有率分析、产业趋势与成长预测(2025-2030)

亚太地区抽水蓄能:市场占有率分析、产业趋势与成长预测(2025-2030 年)北美抽水蓄能能源:市场占有率分析、产业趋势与成长预测(2025-2030)南美洲抽水蓄能储能:市场占有率分析、产业趋势与成长预测(2025-2030)

▼