|

市场调查报告书

商品编码

1687942

印度预拌混凝土:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)India Ready Mix Concrete - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

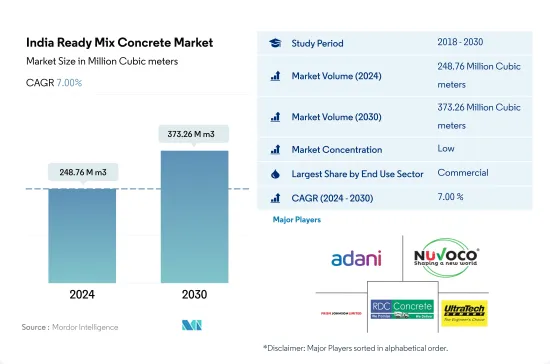

预计 2024 年印度预拌混凝土市场规模将达到 2.4876 亿立方米,到 2030 年预计将达到 3.7326 亿立方米,预测期内(2024-2030 年)的复合年增长率为 7.00%。

预计印度建筑业透过外国直接投资和政府计画进行的大量投资将推动对预拌混凝土的需求。

- 印度预拌混凝土市场适用于住宅、基础设施和商业建筑等多种计划,2022 年占亚太市场的 6.24%。预计 2023 年将增加 693 万立方米,在政府旨在加强国家建筑业的倡议的推动下,市场有望实现成长。

- 2022 年,基础建设占据了印度预拌混凝土市场的主导地位,需求达到 7,260 万立方公尺。这一增长归因于外国直接投资的增加,特别是在加强该国的交通网络,包括道路、高速公路和机场方面。预计 2023 年基础设施支出将增加 39 亿美元,进一步推动对预拌混凝土的需求。

- 根据预测,预测期内商业建筑领域的数量复合年增长率将达到 6.86%。这与预测相符,即到 2030 年,印度新的商业占地面积将增加 3.96 亿平方英尺,并从 2022 年开始大幅增加。商业建筑的增加必然会带动预拌混凝土的需求。

- 具体来说,预计预测期内工业建筑规模将以 7.13% 的复合年增长率位居第二。印度的目标是到2030年成为全球製造地,尤其是电子和汽车製造业。这个愿景得到了亚马逊和特斯拉等产业巨头的投资以及政府激励措施的支持。这些因素正在刺激製造设施的建设并增加预拌混凝土的需求。

印度预拌混凝土市场趋势

预计到 2030 年,印度甲级办公室市场规模将达到 12 亿平方英尺,这可能会推动商业建筑业的需求。

- 2022 年,印度新的商业占地面积比 2021 年增加了 6.2%。零售业需求强劲,尤其是在前七大城市(德里国家首都辖区、班加罗尔、海得拉巴、孟买、普纳、清奈和加尔各答),购物中心面积超过 260 万平方英尺,比 2021 年增长 27%。展望 2023 年,由于外国直接投资 (FDI) 的激增推动了对新办公、零售和其他设施的需求,该行业的新增占地面积预计将激增 3,800 万平方英尺。尤其是,预计2023年建筑业发展的外国直接投资流入将达到9,600万美元。

- 2020 年,印度新建商业占地面积较 2019 年下降 68.3%。下降的主要原因是政府在全国范围内实施封锁,导致正在进行的计划暂停、供应链紧张并影响了劳动力的可用性。然而,随着 2021 年限制措施的放鬆,出现了强劲復苏,新建占地面积激增约 5.26 亿平方英尺。此外,2021 年绿建筑倡议显着增加,约有 55% 的商业计划采用了永续性,进一步刺激了该领域的需求。

- 展望 2030 年,印度新的商业占地面积预计将达到 3.58 亿平方英尺,较 2023 年大幅成长。这一增长带来了对购物中心、办公空间和其他商业设施的需求。例如,印度前七大城市的甲级办公大楼市场到 2026 年将扩大到 10 亿平方英尺,到 2030 年将进一步扩大到 12 亿平方英尺。因此,预计该国新的商业占地面积在预测期内将实现 5.26% 的强劲成长率。

住宅需求增加和房地产行业的扩张将刺激住宅行业的需求

- 2022年,印度住宅占地面积成长9.4%,高于前一年。印度住宅需求激增,前七大城市(德里国家首都辖区、班加罗尔、海得拉巴、孟买、浦那、普纳清奈和加尔各答)总合建造约 402,000 套新房,比 2021 年增加 44%。 2023 年第一季,这些城市的住宅销售量达到 114,000 套,比上年大幅增加 99,500 多套。因此,预计 2023 年印度新建住宅占地面积将比 2022 年增加约 7,100 万平方英尺。

- 2020年,印度住宅产业遭遇挫折,新屋占地面积与前一年同期比较%。下降的原因是全国范围内的封锁、供应链中断、劳动力短缺、建筑生产率放缓以及外国投资下降。不过,印度住宅房地产市场在 2021 年有所復苏,排名前七位的城市新增住宅数量约为 163,000 套。这一激增导致 2021 年住宅领域的新建占地面积与 2020 年相比大幅增加,达到约 6.49 亿平方英尺。

- 展望未来,预计 2023 年至 2030 年间印度住宅产业的复合年增长率将达到 2.95%。这一增长得益于持续的住宅需求、不断增加的投资和有利的政府政策。特别是到2030年,预计印度40%以上的人口将居住在都市区,这将带来约2500万套额外经济适用住宅的需求。此外,到2030年,主要城市的住宅房地产市场预计将达到150万套,这将进一步推动该产业的需求。

印度预拌混凝土产业概况

印度预拌混凝土市场较为分散,前五大公司占的市占率为9.74%。该市场的主要企业是:Adani Group、Nuvoco Vistas Corp Ltd.、Prism Johnson Limited、RDC Concrete (India) Pvt Ltd 和 UltraTech Cement Ltd.(按字母顺序排列)。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章执行摘要和主要发现

第二章 报告要约

第 3 章 简介

- 研究假设和市场定义

- 研究范围

- 调查方法

第四章 产业主要趋势

- 最终用途趋势

- 商业

- 业/设施

- 基础设施

- 住宅

- 重大基础设施计划(目前和已宣布)

- 法律规范

- 价值链与通路分析

第五章 市场区隔

- 最终使用领域

- 商业

- 业/设施

- 基础设施

- 住宅

- 产品

- 中央混合

- 收缩混合

- 交通混合

第六章 竞争格局

- 主要策略趋势

- 市场占有率分析

- 业务状况

- 公司简介

- Adani Group

- India Cements Ltd.

- JK Lakshmi Cement Ltd.

- JSW Cement.

- Nuvoco Vistas Corp Ltd.

- Prism Johnson Limited

- Ramco Cements

- RDC Concrete(India)Pvt Ltd

- Skyway RMC Plants Private Limited

- UltraTech Cement Ltd.

第七章:执行长的关键策略问题

第 8 章 附录

- 世界概况

- 概述

- 五力分析框架(产业吸引力分析)

- 全球价值链分析

- 市场动态(DRO)

- 资讯来源和进一步阅读

- 图片列表

- 关键见解

- 资料包

- 词彙表

The India Ready Mix Concrete Market size is estimated at 248.76 million Cubic meters in 2024, and is expected to reach 373.26 million Cubic meters by 2030, growing at a CAGR of 7.00% during the forecast period (2024-2030).

High investments through FDIs and government schemes in India's construction sector are predicted to augment the demand for ready-mix concrete

- India's ready-mix concrete market, which caters to diverse projects like housing, infrastructure, and commercial buildings, held a 6.24% share of the market in Asia-Pacific in 2022. The market was poised for growth, with a projected increase of 6.93 million cubic meters in 2023, bolstered by government initiatives aimed at bolstering the nation's construction sector.

- In 2022, infrastructure construction was the dominant driver of India's ready-mix concrete market, accounting for a significant 72.6 million cubic meters. This surge can be attributed to heightened foreign direct investments, particularly in bolstering the nation's transportation networks, including roads, highways, and airports. Infrastructure spending was expected to rise by USD 3.9 billion in 2023, further fueling the demand for ready-mix concrete.

- Projections indicate that the commercial construction segment will witness a CAGR of 6.86% in volume during the forecast period. This is in line with estimates that India's new commercial floor space will expand by 396 million square feet by 2030, a significant jump from 2022. This uptick in commercial construction will inevitably drive up the demand for ready-mix concrete.

- Notably, industrial construction is anticipated to experience the second-highest CAGR of 7.13% in volume during the forecast period. India is positioning itself as a global manufacturing hub, particularly for electronics and automobiles, by 2030. This vision is bolstered by investments from industry giants such as Amazon and Tesla, alongside government incentives. These factors are propelling the construction of manufacturing units, thereby driving the demand for ready-mix concrete.

India Ready Mix Concrete Market Trends

India's Grade A office market is expected to reach 1.2 billion sq. ft by 2030 and is likely to drive the demand for the commercial construction sector

- In 2022, India's new commercial floor area saw a 6.2% volume growth compared to 2021. The retail sector, particularly in the top seven cities (Delhi NCR, Bangalore, Hyderabad, Mumbai, Pune, Chennai, and Kolkata), witnessed robust demand, adding over 2.6 million sq. ft of mall space, a 27% increase from 2021. Looking ahead to 2023, the sector's new floor area is expected to surge by 38 million sq. ft, driven by a surge in foreign direct investment (FDI) fueling the need for new offices, retail outlets, and other facilities. Notably, the FDI equity inflow for construction development in 2023 was projected to hit USD 96 million.

- In 2020, India's commercial new floor area plummeted by 68.3% in volume compared to 2019. This decline was primarily due to a nationwide lockdown imposed by the government, which disrupted ongoing projects, strained supply chains, and impacted labor availability. However, as restrictions eased in 2021, the country witnessed a significant rebound, with the new floor area surging by approximately 526 million sq. ft. Additionally, 2021 saw a notable uptick in green building initiatives, with around 55% of commercial projects embracing sustainability, further bolstering the demand for the sector.

- Looking ahead to 2030, India's commercial new floor area is projected to hit 358 million sq. ft, a significant jump from 2023. This surge drives a growing appetite for shopping malls, office spaces, and other commercial facilities. For instance, India's Grade A office market in the top seven cities is set to expand to 1 billion sq. ft by 2026 and further to 1.2 billion sq. ft by 2030. Consequently, the country's commercial new floor area is poised to witness a robust CAGR of 5.26% during the forecast period.

Rise in demand for housing units and increasing real estate sector to boost residential sector demand

- In 2022, India witnessed a 9.4% growth in residential floor area, outpacing the previous year. The demand for housing in the country surged, with the top seven cities (Delhi NCR, Bangalore, Hyderabad, Mumbai, Pune, Chennai, and Kolkata) collectively adding approximately 402,000 new units, marking a 44% increase from 2021. In Q1 2023, housing sales in these cities reached 1.14 lakh units, a staggering jump of over 99,500 units from the previous year. Consequently, it was projected that the residential new floor area in India would expand by approximately 71 million sq. ft in 2023 compared to 2022.

- In 2020, the residential sector in India faced a setback, witnessing a 6.25% decline in new floor area compared to the previous year. This decline was attributed to the nationwide lockdown, disruptions in the supply chain, labor shortages, reduced construction productivity, and a dip in foreign investments. However, in 2021, the Indian residential real estate market rebounded, adding around 163,000 new residential units across the top seven cities. This surge translated into a significant increase of about 649 million sq. ft in the residential sector's new floor area in 2021 compared to 2020.

- Looking ahead, the residential sector in India is poised to exhibit a CAGR of 2.95% in terms of volume from 2023 to 2030. This growth can be attributed to sustained housing demand, increased investments, and favorable government policies. Notably, by 2030, it is projected that over 40% of India's population will reside in urban areas, driving a demand for approximately 25 million additional affordable housing units. Furthermore, by 2030, the residential real estate market is expected to hit 1.5 million units in key cities, further fueling the demand in the sector.

India Ready Mix Concrete Industry Overview

The India Ready Mix Concrete Market is fragmented, with the top five companies occupying 9.74%. The major players in this market are Adani Group, Nuvoco Vistas Corp Ltd., Prism Johnson Limited, RDC Concrete (India) Pvt Ltd and UltraTech Cement Ltd. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End Use Sector Trends

- 4.1.1 Commercial

- 4.1.2 Industrial and Institutional

- 4.1.3 Infrastructure

- 4.1.4 Residential

- 4.2 Major Infrastructure Projects (current And Announced)

- 4.3 Regulatory Framework

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size, forecasts up to 2030 and analysis of growth prospects.)

- 5.1 End Use Sector

- 5.1.1 Commercial

- 5.1.2 Industrial and Institutional

- 5.1.3 Infrastructure

- 5.1.4 Residential

- 5.2 Product

- 5.2.1 Central Mixed

- 5.2.2 Shrink Mixed

- 5.2.3 Transit Mixed

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Adani Group

- 6.4.2 India Cements Ltd.

- 6.4.3 JK Lakshmi Cement Ltd.

- 6.4.4 JSW Cement.

- 6.4.5 Nuvoco Vistas Corp Ltd.

- 6.4.6 Prism Johnson Limited

- 6.4.7 Ramco Cements

- 6.4.8 RDC Concrete (India) Pvt Ltd

- 6.4.9 Skyway RMC Plants Private Limited

- 6.4.10 UltraTech Cement Ltd.

7 KEY STRATEGIC QUESTIONS FOR CONCRETE, MORTARS AND CONSTRUCTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

预拌混凝土:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

预拌混凝土:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 预拌混凝土市场规模、份额和成长分析(按产量、类型、搅拌机类型和地区划分)-2026-2033年产业预测

预拌混凝土市场规模、份额和成长分析(按产量、类型、搅拌机类型和地区划分)-2026-2033年产业预测 2025年全球混凝土搅拌站市场报告2025年全球混凝土搅拌站搅拌机市场报告

2025年全球混凝土搅拌站市场报告2025年全球混凝土搅拌站搅拌机市场报告 混凝土搅拌站市场分析与预测(至2034年):类型、产品、服务、技术、组件、应用、材料类型、流程、最终使用者、能力

混凝土搅拌站市场分析与预测(至2034年):类型、产品、服务、技术、组件、应用、材料类型、流程、最终使用者、能力 按纤维类型、交付方式、强度等级、最终用途和添加剂类型分類的预拌混凝土市场—2025-2032年全球预测

按纤维类型、交付方式、强度等级、最终用途和添加剂类型分類的预拌混凝土市场—2025-2032年全球预测 2025-2029年全球预拌混凝土市场

2025-2029年全球预拌混凝土市场 混凝土厂设备市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测混凝土搅拌站市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测预拌混凝土市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

混凝土厂设备市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测混凝土搅拌站市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测预拌混凝土市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测