|

市场调查报告书

商品编码

1773353

混凝土搅拌站市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Concrete Batch Plants Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

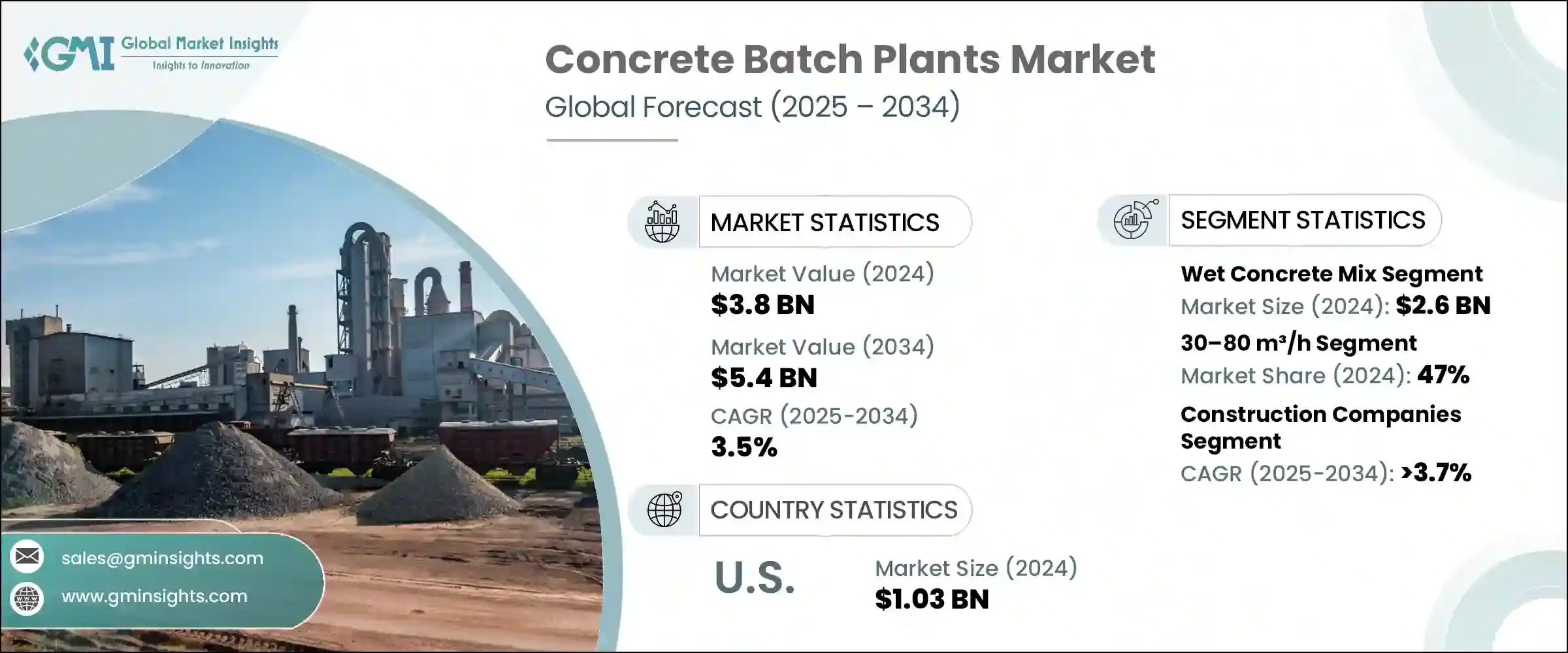

2024年,全球混凝土搅拌站市场规模达38亿美元,预计2034年将以3.5%的复合年增长率成长,达到54亿美元。这一成长趋势得益于基础设施建设的蓬勃发展、城市化进程的加速以及对高效能、高品质混凝土生产方法日益增长的需求。已开发经济体和发展中经济体的政府和私人实体都在持续投资建设完善的交通系统、商业枢纽、住宅开发项目以及能源相关基础设施。这些项目都高度依赖稳定、高性能的混凝土,这推动了对先进搅拌站的需求。

移动式混凝土搅拌站因其现场搅拌能力而备受青睐,这减少了对运输的依赖,并加快了专案进度。这种需求涵盖了公用事业、工业发展和道路建设等各个领域。不断变化的环境政策和对永续建筑的日益重视,促使承包商考虑采用电动移动式搅拌站而非柴油动力,尤其是在人口稠密的城市地区。紧凑型模组化搅拌站具有便携性,且易于迁移和灵活设置,因此越来越受到人们的青睐。此外,物联网整合、自动化和智慧控制面板等创新技术正在改变工厂运营,使即时监控和最大程度减少人工输入成为可能。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 38亿美元 |

| 预测值 | 54亿美元 |

| 复合年增长率 | 3.5% |

2024年,湿混凝土混合料市场规模达26亿美元,预计2025年至2034年的复合年增长率将达到3.7%。湿拌混凝土搅拌站正日益受到青睐,因为它们能够在混凝土装车运输前,将所有必需材料(包括水)在现场彻底搅拌。这使得混凝土混合更加均匀,品质更卓越,对追求一致性和可靠性的建筑专业人士极具吸引力。与需要预先称重材料并在运输途中搅拌的干拌混凝土搅拌站相比,湿拌系统具有更强的控制力和均匀性,尤其是在对强度规格要求更高的大型项目中。虽然干拌混凝土解决方案适用于快速移动的远端施工任务,但湿拌混凝土以其更佳的搅拌效果和生产精度,仍占据主导地位。

2024年,生产能力在30至80立方米/小时范围内的搅拌站占据了47%的市场份额,预计2025-2034年期间的复合年增长率将达到3.9%。这些搅拌站非常适合中型基础设施开发和城市项目,兼顾了产能和灵活性。其适中的吞吐量使承包商能够将其部署到各种应用中,例如商业开发、市政专案和道路铺设作业。它们在产出效率和移动性之间取得了良好的平衡,使用户能够快速适应不同的专案需求。

2024年,欧洲混凝土搅拌站市场规模达8亿美元,预计2025年至2034年期间的复合年增长率为3.1%。该地区的成长主要受到监管压力的影响,要求减少建筑排放,以及对永续建筑实践日益增长的需求。欧洲各地的承包商正在采用移动式混凝土搅拌站,以减少混凝土运输对环境的影响,并更好地融入以生态为重点的基础设施建设计画。西欧市场需求稳定,主要得益于翻新和维护活动;而东欧市场则因公共和私人对基础设施建设的投资增长以及新兴的建筑需求而迅速扩张。该地区各国正将永续性作为发展策略的核心,大力推广新一代混凝土搅拌系统。

引领市场的主要製造商包括三一、Elkon、Vince Hagan、普茨迈斯特、徐工、Cemco、Meka、JEL Concrete Plants、SCHWING Stetter、Semix、Stephens Mfg、Ammann、AIMIX Group、利勃海尔和 Astec。混凝土搅拌站市场的顶尖企业正在部署多项重点策略,以增强竞争优势并提高市场份额。各公司优先考虑产品创新,高度重视自动化和数位集成,以提供具有即时控制功能的智慧配料解决方案。他们正在引入节能模型,以顺应永续发展趋势并满足排放标准。透过合作伙伴关係和本地化製造进行的区域扩张正在帮助企业提高市场响应能力并降低物流成本。模组化和便携式工厂设计正在受到重视,以服务偏远项目和快节奏的施工现场。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 利润率

- 每个阶段的增值

- 影响价值链的因素

- 产业衝击力

- 成长动力

- 产业陷阱与挑战

- 机会

- 成长潜力分析

- 未来市场趋势

- 技术和创新格局

- 当前的技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 按类型

- 监管格局

- 标准和合规性要求

- 区域监理框架

- 认证标准

- 贸易统计(HS 编码 - 84743110)

- 主要进口国

- 主要出口国

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估计与预测:按类型,2021 - 2034 年

- 主要趋势

- 固定式配料厂

- 移动式配料厂

第六章:市场估计与预测:依产能,2021 - 2034 年

- 主要趋势

- 低于30立方米/小时

- 30-80 立方米/小时

- 高于80立方米/小时

第七章:市场估计与预测:依混合类型,2021 - 2034

- 主要趋势

- 湿混凝土混合物

- 干混凝土混合物

第八章:市场估计与预测:按应用,2021 - 2034 年

- 主要趋势

- 住宅建筑

- 商业建筑

- 办公大楼

- 零售空间

- 饭店和度假村

- 卫生保健

- 教育机构

- 其他的

- 基础设施项目

- 道路和高速公路

- 桥樑和隧道

- 机场和海港

- 铁路和地铁

- 水坝和水库

- 风力发电场和太阳能发电场

- 仓库

- 其他的

- 市政和智慧城市项目

- 工业建筑

第九章:市场估计与预测:依最终用途,2021 - 2034 年

- 主要趋势

- 建筑公司

- 政府机构

- 其他的

第 10 章:市场估计与预测:按配销通路,2021 年至 2034 年

- 主要趋势

- 直销

- 间接销售

第 11 章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 南非

- 沙乌地阿拉伯

- 阿联酋

第十二章:公司简介

- AIMIX Group

- Ammann

- Astec

- Cemco

- Elkon

- JEL Concrete Plants

- Liebherr

- Meka

- Putzmeister

- Sany

- SCHWING Stetter

- Semix

- Stephens Mfg

- Vince Hagan

- XCMG

The Global Concrete Batch Plants Market was valued at USD 3.8 billion in 2024 and is estimated to grow at a CAGR of 3.5% to reach USD 5.4 billion by 2034. This upward trend is supported by growing infrastructure development, rapid urban expansion, and the rising demand for efficient, high-quality concrete production methods. Governments and private entities across both developed and developing economies are continuing to invest in robust transportation systems, commercial hubs, housing developments, and energy-related infrastructure. These projects all rely heavily on consistent and high-performance concrete, which is fueling the need for advanced batch plants.

Mobile batching plants are gaining notable traction due to their on-site mixing capability, which reduces the reliance on transportation and speeds up project timelines. This demand spans across various sectors, including utilities, industrial development, and road construction. Evolving environmental policies and growing emphasis on sustainable construction are prompting contractors to consider electric-powered mobile plants over diesel-based alternatives, particularly in dense urban areas. Compact modular plants with portable features are increasingly being adopted for their ease of relocation and set-up flexibility. Furthermore, innovations like IoT integration, automation, and smart control panels are transforming plant operations, making real-time monitoring and minimal manual input possible.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.8 Billion |

| Forecast Value | $5.4 Billion |

| CAGR | 3.5% |

The wet concrete mix segment generated USD 2.6 billion in 2024 and is expected to grow at a CAGR of 3.7% from 2025 to 2034. Wet mix plants are gaining more preference as they allow all essential materials-including water-to be thoroughly mixed at the site before the concrete is loaded for delivery. This results in a more even mix and superior concrete quality, which appeals to construction professionals seeking consistency and reliability. Compared to dry batch plants that deliver pre-weighed materials for mixing in transit, wet mix systems offer greater control and uniformity, especially in larger projects requiring higher strength specifications. While dry mix solutions are useful for fast-moving, remote construction tasks, wet batching remains dominant for its better results and production precision.

Plants with a production capacity ranging from 30 to 80 m3/h segment accounted for 47% share in 2024 and are projected to register a CAGR of 3.9% during 2025-2034. These batch plants are ideally suited for medium-scale infrastructure developments and urban projects, balancing capacity with flexibility. Their moderate throughput enables contractors to deploy them for a wide range of applications such as commercial developments, municipal projects, and road paving operations. They strike a good balance between output efficiency and mobility, allowing users to adapt quickly to different project requirements.

Europe Concrete Batch Plants Market was valued at USD 800 million in 2024 and is anticipated to grow at a CAGR of 3.1% from 2025 to 2034. This regional growth is being shaped by regulatory pressure to cut construction emissions and the rising demand for sustainable building practices. Contractors throughout Europe are adopting mobile batch plants to reduce the environmental footprint of transporting concrete and to better align with eco-focused infrastructure initiatives. Western Europe sees steady demand supported by refurbishment and maintenance activities, while in Eastern Europe, the market is expanding rapidly due to public and private investment in infrastructure growth and emerging construction demands. Countries across the region are making sustainability central to development strategies, pushing the adoption of newer-generation concrete batching systems.

Key manufacturers leading the market include Sany, Elkon, Vince Hagan, Putzmeister, XCMG, Cemco, Meka, JEL Concrete Plants, SCHWING Stetter, Semix, Stephens Mfg, Ammann, AIMIX Group, Liebherr, and Astec. Top players in the concrete batch plants market are deploying several focused strategies to strengthen their competitive edge and enhance market share. Companies prioritize product innovation with a strong emphasis on automation and digital integration to deliver smart batching solutions with real-time control features. They are introducing energy-efficient models to align with sustainability trends and meet emission norms. Regional expansion through partnerships and localized manufacturing is helping firms improve market responsiveness and reduce logistics costs. Modular and portable plant designs are being emphasized to serve remote projects and fast-paced construction sites.

Table of Contents

Chapter 1 Methodology and scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 By type

- 2.2.3 By capacity

- 2.2.4 By mix type

- 2.2.5 By application

- 2.2.6 By end use

- 2.2.7 By distribution channel

- 2.3 CXO perspectives: strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.2.3 Opportunities

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Trade statistics (HS code - 84743110)

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Type, 2021 - 2034 ($Billion, Thousand Units)

- 5.1 Key trends

- 5.2 Stationary batch plant

- 5.3 Mobile batch plant

Chapter 6 Market Estimates & Forecast, By Capacity, 2021 - 2034 ($Billion, Thousand Units)

- 6.1 Key trends

- 6.2 Below 30 m³/h

- 6.3 30-80 m³/h

- 6.4 Above 80 m³/h

Chapter 7 Market Estimates & Forecast, By Mix Type, 2021 - 2034 ($Billion, Thousand Units)

- 7.1 Key trends

- 7.2 Wet concrete mix

- 7.3 Dry concrete mix

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Billion, Thousand Units)

- 8.1 Key trends

- 8.2 Residential construction

- 8.3 Commercial construction

- 8.3.1 Office buildings

- 8.3.2 Retail spaces

- 8.3.3 Hotels and resorts

- 8.3.4 Healthcare

- 8.3.5 Educational institutions

- 8.3.6 Others

- 8.4 Infrastructure projects

- 8.4.1 Roads and highways

- 8.4.2 Bridges and tunnels

- 8.4.3 Airports and seaports

- 8.4.4 Railways and Metros

- 8.4.5 Dam & reservoirs

- 8.4.6 Wind farms and solar farms

- 8.4.7 Warehouses

- 8.4.8 Others

- 8.5 Municipality & smart city projects

- 8.6 Industrial construction

Chapter 9 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Billion, Thousand Units)

- 9.1 Key trends

- 9.2 Construction companies

- 9.3 Government agencies

- 9.4 Others

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2021 - 2034 ($Billion, Thousand Units)

- 10.1 Key trends

- 10.2 Direct sales

- 10.3 Indirect sales

Chapter 11 Market Estimates & Forecast, By Region, 2021 - 2034 ($Billion, Thousand Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 Japan

- 11.4.3 India

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 AIMIX Group

- 12.2 Ammann

- 12.3 Astec

- 12.4 Cemco

- 12.5 Elkon

- 12.6 JEL Concrete Plants

- 12.7 Liebherr

- 12.8 Meka

- 12.9 Putzmeister

- 12.10 Sany

- 12.11 SCHWING Stetter

- 12.12 Semix

- 12.13 Stephens Mfg

- 12.14 Vince Hagan

- 12.15 XCMG

预拌混凝土市场:依混凝土类型、製造方法、强度等级、应用、最终用途及通路划分-2026-2032年全球预测

预拌混凝土市场:依混凝土类型、製造方法、强度等级、应用、最终用途及通路划分-2026-2032年全球预测 混凝土搅拌站市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、材料类型、製程、最终用户、功能划分预拌混凝土市场分析及预测(至2035年):类型、产品类型、应用、技术、组成成分、最终用户、製程、安装类型、设备、解决方案

混凝土搅拌站市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、材料类型、製程、最终用户、功能划分预拌混凝土市场分析及预测(至2035年):类型、产品类型、应用、技术、组成成分、最终用户、製程、安装类型、设备、解决方案 全球预拌混凝土市场规模、份额、趋势和成长分析报告(2026-2034)

全球预拌混凝土市场规模、份额、趋势和成长分析报告(2026-2034) 日本预拌混凝土市场规模、份额、趋势和预测:按产品、最终用途和地区划分,2026-2034年

日本预拌混凝土市场规模、份额、趋势和预测:按产品、最终用途和地区划分,2026-2034年 预拌混凝土:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

预拌混凝土:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 预拌混凝土市场规模、份额和成长分析(按产量、类型、搅拌机类型和地区划分)-2026-2033年产业预测

预拌混凝土市场规模、份额和成长分析(按产量、类型、搅拌机类型和地区划分)-2026-2033年产业预测 2025-2029年全球预拌混凝土市场

2025-2029年全球预拌混凝土市场 混凝土厂设备市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测预拌混凝土市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

混凝土厂设备市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测预拌混凝土市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测