|

市场调查报告书

商品编码

1693676

北美预拌混凝土:市场占有率分析、产业趋势与成长预测(2025-2030 年)North America Ready-Mix Concrete - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

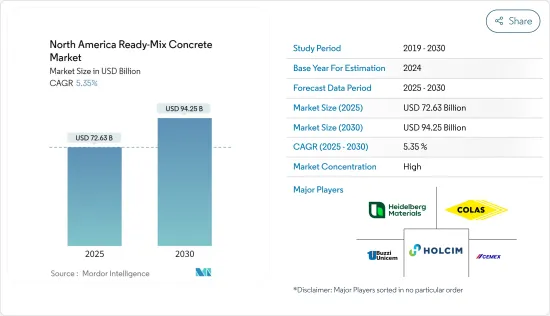

北美预拌混凝土市场规模预计在 2025 年为 726.3 亿美元,预计到 2030 年将达到 942.5 亿美元,预测期内(2025-2030 年)的复合年增长率为 5.35%。

新冠疫情为建筑业等密集型产业带来了沉重打击。然而,随着所有有关社交距离规范和隔离的限制被取消,该地区现在正走上復苏之路。

关键亮点

- 预计全部区域建筑需求的不断增长,以及人们对 RMC 的潜在优势及其优于普通混凝土的性能的认识不断提高,将推动该地区市场的成长。

- 另一方面,RMC 运输相关的挑战以及潜在替代品的易得性可能会阻碍市场成长。

- 然而,基础设施建设投资的增加导致全部区域的建设活动增加,为未来的预拌混凝土市场提供了潜在的机会。

- 在预测期内,美国预计将引领北美预拌混凝土市场。

北美预拌混凝土市场趋势

住宅领域展现出巨大的成长潜力

- 北美被视为住宅开发的有前景的地区,美国和加拿大等主要经济体已经宣布并正在进行各种计划。

- 住宅建筑中预拌混凝土的应用包括路缘石铺设和衬砌、钢筋和非钢筋地基、单层和双层扩建、钢筋和非钢筋住宅地板、筏板、车库、化粪池铺设、沟槽填充、花园棚屋和墙壁、排水工程、外部花园区、重型货车 (HGV) 停车场、车道、小路填充、楼梯、外部表面、排水工程、外部花园区、重型货车 (HGV) 停车场、小径、小路、楼梯、外部表面、温室、地板、建筑和停车场。

- 政府在房地产市场住宅方面的支出增加,以及对豪华住宅的需求不断增长,可能会有利于所研究市场的成长。公共和私营部门对经济适用住宅的日益关注推动了该地区住宅建筑业的成长。

- 在美国和加拿大的部分地区,儘管中产阶级住宅停滞不前(经济适用住宅持续减少),但低房屋抵押贷款利率仍在推动住宅建设增加。

- 在加拿大,经济适用房倡议(AHI)、新建筑加拿大计划(NBCP)和加拿大製造等各种政府计划极大地推动了住宅领域的扩张,并促进了建筑涂料在住宅领域的使用。

- 此外,根据哈佛大学住宅研究联合中心的数据,美国每年估计在住宅重建和维修上花费超过 4,000 亿美元,其中可能包括建筑涂料和涂层,这将对需求产生积极影响。

- 根据美国人口普查局的数据,预计2022年美国私部门新建住宅数量将达到约9,000亿美元,连续第三年强劲成长。这一趋势也反映在建筑许可上,德克萨斯州的达拉斯-沃斯堡-阿灵顿大都会区是全国住宅建筑率最高的地区之一。

- 此外,2023年3月,以季节性已调整的的以年度为基础,共获得141.3万套自住住宅的建筑许可。这比2023年2月修正后的155万套低8.8%,比2022年3月的187.9万套低24.8%。 3月独栋住宅许可证数量为81.8万套,比2月修正后的78.6万套增加4.1%。 2023 年 3 月,五套或五套以上单元建筑的核准数量为 543,000 套。

- 因此,由于上述因素,住宅产业对预拌混凝土的需求可能会在预测期内影响市场成长。

美国主导市场

- 美国建筑业前景广阔,住宅和基础设施建设吸引了大量关注和投资。

- 美国拥有庞大的建筑业,僱用了超过 760 万人。该国的建筑业在商业、工业、机构、住宅、基础设施、能源和公共工程建设中发挥关键作用,是该国经济的主要贡献者。根据经济分析局的数据,建筑业占美国GDP 的份额将从前一年的 4.1% 放缓至 2022 年的 4%。

- 根据美国人口普查局的数据,2023 年 2 月美国建筑支出经季节性已调整的后年化率估计为 1.8,441 兆美元,比 2023 年 1 月修订后的 1.8451 兆美元低 0.1%。

- 此外,根据美国人口普查局的数据,2022 年美国私人建筑支出的成长率几乎是公共建筑支出的四倍。纵观美国所有 50 个州的建筑支出,德克萨斯州和加利福尼亚州处于领先地位。预测显示,美国新建筑的价值将持续上涨。

- 同样,2023年2月美国私人建筑业经季节性调整后的年率估计为1.45万亿美元,而住宅建筑业经季节性调整后的年率估计为8521亿美元,比1月份修订后的估计值8570亿美元低0.6%。 2023 年 2 月住宅建筑经季节性调整后的年率为 6,010 亿美元,比 1 月修订后的 5,967 亿美元高出 0.7%。

- 美国除了新建住宅外,还正在进行大规模的重建。该国不断增长的移民人口带来了越来越大的翻修需求。人们对永续性和高效建筑的认识不断提高,也推动了修復趋势。多种政府贷款也为该国的住宅装修提供支援。

- 根据美国保险建筑业共识预测小组的数据,2022 年住宅建筑支出将增加 5.4%。此外,美国新的私人住宅建筑支出将在 2022 年达到峰值,略高于 5,390 亿美元。到 2023 年,预计所有主要商业、工业和机构类别都将实现至少相当健康的成长。

- 2022 年 5 月,Holcim 美国收购了大巴吞鲁日地区着名的预拌混凝土 。此次收购使 Holcim 获得了 51 辆搅拌机搅拌车和 8 家国家认证的配料厂,为巴吞鲁日及週边城市提供服务。

- 此外,2022 年 5 月,Martin Marietta Materials Inc. 签署最终协议,以 2.5 亿美元现金将其西海岸水泥预拌混凝土业务的一部分出售给 CalPortland Corp.。交易完成后,CalPortland 将获得加州雷丁水泥厂、相关水泥配送终端和 14 家预拌混凝土厂的使用权。

- 这些因素表明,未来几年住宅和基础设施发展可能会出现强劲增长,从而加强该地区的预拌混凝土市场。

北美预拌混凝土产业概况

北美预拌混凝土市场本质上是整合的。市场的主要企业包括 CEMEX SAB de CV、HOLCIM、Buzzi Unicem SpA、HeidelbergCement AG 和 Colas。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 调查前提条件

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 驱动程式

- 整个全部区域建筑需求不断成长

- 比普通混凝土具有更优异的性能和优势

- 限制因素

- 潜在替代方案的可用性

- 价值链分析

- 波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章市场区隔

- 按最终用户部门

- 住宅

- 商业的

- 工业/设施

- 基础设施

- 按地区

- 美国

- 加拿大

- 墨西哥

第六章竞争格局

- 併购、合资、合作与协议

- 市场占有率(%)**/排名分析

- 主要企业策略

- 公司简介

- BuzziUnicem SpA

- CEMEX SAB de CV

- Colas Group

- CRH

- 海湾合作委员会国家

- HeidelbergCement

- HOLCIM

- RW Sidley, Inc.

- Sika AG

- Thomas Concrete Group

- Titan Cement

- Vicat SA

- Vulcan Materials

第七章 市场机会与未来趋势

- 增加对该地区商业基础建设的投资

The North America Ready-Mix Concrete Market size is estimated at USD 72.63 billion in 2025, and is expected to reach USD 94.25 billion by 2030, at a CAGR of 5.35% during the forecast period (2025-2030).

The COVID-19 pandemic wreaked havoc on labor-intensive industries like the building and construction industry. However, with all restrictions on social distancing norms and lockdowns lifted, the region is now progressing on the path to recovery.

Key Highlights

- The growing demand for building construction across the region, along with the rising awareness about the potential advantages and superior properties of RMC over normal concrete, is expected to drive regional market growth.

- On the flip side, the easy availability of potential substitutes, along with the challenges associated with the transportation of RMC, may hamper the market growth.

- However, the rising investments in infrastructure development are resulting in increasing construction activities across the region, thereby providing potential opportunities to the ready-mix concrete market in the future.

- The United States is expected to the leader in the North American ready-mix concrete market during the forecast period.

North America Ready-Mix Concrete Market Trends

Residential Segment Showing Great Potential for Growth

- In the North American region, residential development looks promising, with various projects already announced and initiated across major economies like the United States and Canada.

- The applications of ready-mix concrete found in residential construction are curb bedding and backing, reinforced and unreinforced foundations, single and double-story extensions, reinforced and unreinforced house floors, raft, garage, and septic tank bedding, trench fill, garden shed and wall, drainage works, external yard areas, heavy goods vehicle (HGV) parking and driveways, paths, steps, and external paving, and hard standings and bases for greenhouses, patios, and conservatories.

- The increased government spending in the real estate market for residential construction, along with the growing demand for high-class residential homes, are likely to benefit the growth of the market studied. The increased focus on affordable housing by both the public and private sectors is driving the residential construction sector's growth in the region.

- Though the middle-class housing segment is suffering a slump in a few regions of the United States and Canada (as they keep losing ground on affordability), low interest rates for home mortgages have increased residential construction.

- In Canada, various government projects, including the Affordable Housing Initiative (AHI), the New Building Canada Plan (NBCP), and Made in Canada, are set to support the expansion of the sector hugely, thereby driving the use of architectural paints and coatings in the residential sector.

- Furthermore, as per the Harvard Joint Center for Housing Studies, it is estimated that Americans spend more than USD 400 billion a year on residential renovations and repairs, which might as well involve the use of architectural paints and coatings, which positively affects their demand.

- According to the US Census Bureau, the private sector's production of new house building in the United States reached approximately USD 900 billion in 2022, marking the third year of robust growth in a row. This trend is mirrored in the number of dwelling units authorized by building permits, with the Dallas-Fort Worth-Arlington metropolitan area in Texas having some of the largest residential construction production in the country.

- Additionally, in March 2023, 1,413,000 privately owned homes had building permits authorized on a seasonally adjusted annual basis. It was 8.8% lower than the revised February 2023 rate of 1,550,000 and 24.8% lower than the March 2022 rate of 1,879,000. Single-family authorizations were 818,000 in March, up by 4.1% from the revised February figure of 786,000. In March 2023, there were 543,000 authorizations for units in buildings with five or more units.

- Therefore, owing to the aforementioned factors, the demand for ready-mix concrete for the residential industry is likely to impact market growth during the forecast period.

United States to Dominate the Market

- The United States construction sector shows great promise, with residential and infrastructure construction drawing substantial attention and investment.

- The United States boasts a colossal construction sector that employs over 7.6 million people. It plays a prominent role in commercial, industrial, institutional, residential, infrastructure, energy, and utility construction; the construction sector in the country exhibits a significant contribution to the country's economy. As per the Bureau of Economic Analysis, in 2022, the share of the US construction sector in the country's GDP slumped to 4% from 4.1% in the past year.

- According to the US Census Bureau, during February 2023, construction spending in the country was estimated at a seasonally adjusted annual rate of USD 1,844.1 billion, 0.1% lower than the revised January 2023 estimate of USD 1,845.1 billion.

- Moreover, according to the US Census Bureau, in 2022, private construction spending in the United States grew at a rate roughly four times that of public construction spending. When looking at building spending throughout the 50 states, Texas and California came out on top. According to projections, the value of new buildings in the United States will continue to rise in the coming years.

- Similarly, in February 2023, private construction in the country was estimated at a seasonally adjusted annual rate of USD 1.45 trillion, with residential construction assessed at a seasonally adjusted annual rate of USD 852.1 billion, 0.6% lower than the revised January estimate of USD 857.0 billion. Nonresidential construction remained at a seasonally adjusted annual rate of USD 601.0 billion in February 2023, 0.7% higher than the revised January 2023 estimate of USD 596.7 billion.

- In addition to new home construction, the United States is doing massive home renovations. With the growing population of migrants in the country, the need for renovation has become increasingly important. Also, the growing awareness toward sustainability and high-efficiency structures has created a spur in the restoration trend. The availability of several loans by the government also supports home remodeling in the country.

- According to the AIA (American Institute of Architects) Construction Consensus Forecast Panel, non-residential building construction spending expanded to 5.4% in 2022. Further, US expenditure on new private non-residential buildings peaked at over USD 539 billion in 2022. By 2023, all the major commercial, industrial, and institutional categories are projected to witness at least reasonably healthy gains.

- In May 2022, Holcim US acquired a prominent ready-mix concrete company in the Greater Baton Rouge Area, Cajun Ready-Mix Concrete, to further expand its reach in Louisiana through enhanced capacity to serve its customers. The acquisition allowed Holcim to have access to 51 mixer trucks and eight state-certified batch plants that serve Baton Rouge and surrounding cities.

- Further, in May 2022, Martin Marietta Materials Inc. entered into a definitive agreement to divest certain West Coast cement and ready-mixed concrete operations and sell them to CalPortland Company for a transaction of USD 250 million in cash. On completion of the transaction, CalPortland Company will have access to the Redding cement plant, related cement distribution terminals, and 14 ready-mixed concrete plants located in California.

- These factors indicate that residential and infrastructure development may potentially gain strong traction in the coming years, thereby strengthening the market for ready-mix concrete in the region.

North America Ready-Mix Concrete Industry Overview

The North American ready-mix concrete market is consolidated in nature. Some of the key players in the market include CEMEX SAB de CV, HOLCIM, Buzzi Unicem SpA, HeidelbergCementAG, Colas, and others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Demand for Building Construction across The Region

- 4.1.2 Superior Properties and Advantages Over Normal Concrete

- 4.2 Restraints

- 4.2.1 Easy Availability of Potential Subsitutes

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 By End-user Sector

- 5.1.1 Residential

- 5.1.2 Commercial

- 5.1.3 Industrial/Institutional

- 5.1.4 Infrastructure

- 5.2 By Geography

- 5.2.1 United States

- 5.2.2 Canada

- 5.2.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) **/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 BuzziUnicem SpA

- 6.4.2 CEMEX SAB de CV

- 6.4.3 Colas Group

- 6.4.4 CRH

- 6.4.5 GCC

- 6.4.6 HeidelbergCement

- 6.4.7 HOLCIM

- 6.4.8 R.W. Sidley, Inc.

- 6.4.9 Sika AG

- 6.4.10 Thomas Concrete Group

- 6.4.11 Titan Cement

- 6.4.12 Vicat SA

- 6.4.13 Vulcan Materials

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Rising Investment in Commercial and Infrastructure Development in the Region

预拌混凝土市场:依混凝土类型、製造方法、强度等级、应用、最终用途及通路划分-2026-2032年全球预测

预拌混凝土市场:依混凝土类型、製造方法、强度等级、应用、最终用途及通路划分-2026-2032年全球预测 混凝土搅拌站市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、材料类型、製程、最终用户、功能划分预拌混凝土市场分析及预测(至2035年):类型、产品类型、应用、技术、组成成分、最终用户、製程、安装类型、设备、解决方案

混凝土搅拌站市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、材料类型、製程、最终用户、功能划分预拌混凝土市场分析及预测(至2035年):类型、产品类型、应用、技术、组成成分、最终用户、製程、安装类型、设备、解决方案 全球预拌混凝土市场规模、份额、趋势和成长分析报告(2026-2034)

全球预拌混凝土市场规模、份额、趋势和成长分析报告(2026-2034) 日本预拌混凝土市场规模、份额、趋势和预测:按产品、最终用途和地区划分,2026-2034年

日本预拌混凝土市场规模、份额、趋势和预测:按产品、最终用途和地区划分,2026-2034年 预拌混凝土:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

预拌混凝土:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 预拌混凝土市场规模、份额和成长分析(按产量、类型、搅拌机类型和地区划分)-2026-2033年产业预测

预拌混凝土市场规模、份额和成长分析(按产量、类型、搅拌机类型和地区划分)-2026-2033年产业预测 2025-2029年全球预拌混凝土市场

2025-2029年全球预拌混凝土市场 混凝土厂设备市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测混凝土搅拌站市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

混凝土厂设备市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测混凝土搅拌站市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测