|

市场调查报告书

商品编码

1687957

印尼预拌混凝土:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Indonesia Ready Mix Concrete - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

预计 2024 年印尼预拌混凝土市场规模将达到 1.0722 亿立方米,预计到 2030 年将达到 1.624 亿立方米,预测期内(2024-2030 年)的复合年增长率为 7.16%。

运输混合类型推动印尼商业领域预拌混凝土市场的成长

- 在所有行业中,由于现浇混凝土的使用增加,印尼 2022 年的预拌混凝土需求显着低于 2021 年。因此,2022 年该国预拌混凝土整体消费量与 2021 年相比下降了 15.7%。然而,由于预计包括住宅和商业在内的所有终端使用领域都将实现高成长,因此预计 2023 年整体消费量将比 2022 年成长 21.4%。

- 住宅领域是印尼预拌混凝土砂浆的最大消费量。例如,到2022年,住宅领域将占印尼预拌混凝土总消费量的约40%。该行业最受欢迎的预拌混凝土类型是运输混合料,占 2022 年消费量的 76%。

- 工业和机构部门是印尼预拌混凝土的消费量,因为其建筑面积仅次于住宅,为第二大建筑领域。例如,到2022年,工业和机构部门将占全国新增占地面积的31%。预计在预测期内(2023-2030 年),该领域对预拌混凝土的需求将达到最快的复合年增长率,达到 8.3%。

- 预测期内,印尼的整体预拌混凝土需求预计将成长,其中商业领域的复合年增长率最快,为 8.94%。这主要是由于使用了混合运输方式,预计在预测期内复合年增长率为 9.20%。 2022 年,运输混合混凝土将占全国预拌混凝土需求的 73%。

印尼预拌混凝土市场趋势

预计到 2028 年,印尼的商业房地产市场规模将达到 1.39 兆美元,这可能会刺激商业领域的需求

- 2022年,印尼新建商业占地面积预计将与前一年同期比较9.7%。这一下降是由于建筑活动在新冠疫情期间下降后恢復正常所致。疫情爆发前,印尼商业建筑的年能耗强度就已呈现下降趋势,年均下降率为2.64%。然而,2023年将出现復苏,新的商业占地面积将成长 5.7%,这得益于对新的办公室、仓库和零售空间的需求激增的外国直接投资 (FDI)。

- 在新冠疫情期间,印尼 2020 年和 2021 年新增商业占地面积大幅增加,达到约 960 万平方英尺。政府致力于振兴经济,已推出多项措施,例如放宽私人和公共计划建筑相关的检疫限制。这使得员工可以返回现场工作,企业可以继续运作。值得注意的是,印尼2020年完工建筑量预计将达到约1.32兆印尼盾,2021年将增加至1.42兆印尼盾。

- 预计到 2030 年,印尼的新商业占地面积将比 2023 年大幅成长约 58.72%。这一增长是由于对购物中心、办公室和其他商业空间的需求不断增加。零售房地产领域已成为该国特别有吸引力的行业。例如,商业房地产市场预计到2028年将达到1.39兆美元。印尼新的商业占地面积预计将保持稳定成长,预测期内复合年增长率为6.82%。

住宅需求的增加可能会推动住宅产业的成长

- 2022 年,印尼新建住宅占地面积较 2021 年成长了 7.10%。这一增长是由于人口增长、富裕程度提高和都市化加快。政府主导的住宅支持预计将在 2022 年达到 29 兆印度卢比,在住宅融资流动性工具计画下,到 2023 年将增加至 32 兆印度卢比。该倡议旨在建造至少 220,000 套住宅。住宅建筑业将经历显着的成长。预计到 2023 年,这一数字与前一年同期比较增加到约 5,600 万平方英尺。

- 2020年,印尼新建住宅占地面积较2019年成长7.06%。这是政府的策略性倡议,优先发展建筑业,以缓解景气衰退并支持收入减少的家庭。因此,包括检疫在内的建设活动限制已大大放宽。然而,2021年趋势出现逆转,住宅开工占地面积下降约12.54%。这主要是由于建筑业的外国直接投资(FDI)下降。 2021年建筑业外国直接投资与前一年同期比较减51%。

- 预测期内,印尼新建住宅占地面积预计将以 6.08% 的复合年增长率成长。这一增长归功于该国日益加快的都市化,这得益于政府倡议以及国内外投资。这些因素直接或间接地加剧了该国日益增长的住宅需求,并最终促进了住宅建设。据估计,到 2030 年,每年将需要建造 82 万至 100 万套住宅才能满足不断增长的需求。

印尼预拌混凝土产业概况

印尼预拌混凝土市场较为分散,前五大企业合计占有7%的市占率。市场的主要企业有:Heidelberg Materials、PT Cemindo Gemilang Tbk、PT Waskita Beton Precast Tbk、SCG 和 SIG(按字母顺序排列)。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章执行摘要和主要发现

第二章 报告要约

第 3 章 简介

- 研究假设和市场定义

- 研究范围

- 调查方法

第四章 产业主要趋势

- 最终用途趋势

- 商业

- 业/设施

- 基础设施

- 住宅

- 重大基础设施计划(目前和已宣布)

- 法律规范

- 价值链与通路分析

第五章 市场区隔

- 最终使用领域

- 商业

- 业/设施

- 基础设施

- 住宅

- 产品

- 中央混合

- 收缩混合

- 交通混合

第六章 竞争格局

- 主要策略趋势

- 市场占有率分析

- 业务状况

- 公司简介

- Heidelberg Materials

- Kalla Group.

- PT Cemindo Gemilang Tbk

- PT Waskita Beton Precast Tbk

- PT. Adhimix Precast Indonesia

- PT. Beton Indotama Surya

- PT. Fresh Beton Indonesia

- PT. Modernland Realty Tbk.

- SCG

- SIG

第七章:执行长的关键策略问题

第 8 章 附录

- 世界概况

- 概述

- 五力分析框架(产业吸引力分析)

- 全球价值链分析

- 市场动态(DRO)

- 资讯来源和进一步阅读

- 图片列表

- 关键见解

- 资料包

- 词彙表

简介目录

Product Code: 67082

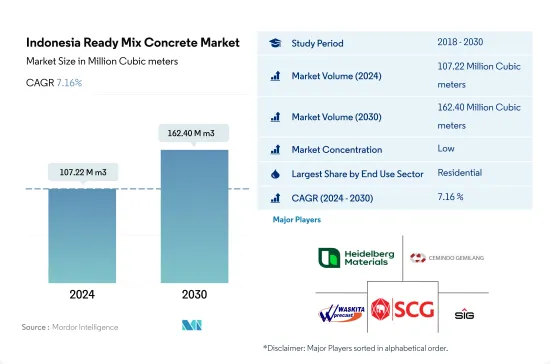

The Indonesia Ready Mix Concrete Market size is estimated at 107.22 million Cubic meters in 2024, and is expected to reach 162.40 million Cubic meters by 2030, growing at a CAGR of 7.16% during the forecast period (2024-2030).

Transit mixed type to drive the growth of the Indonesian ready mix concrete market in the commercial sector

- Across all sectors, the demand for ready mix concrete in Indonesia in 2022 was significantly lower than in 2021 due to more use of on-site mix concrete. This resulted in the country's overall consumption of ready mix concrete being 15.7% lower in 2022 compared to 2021. However, in 2023, as high growth was anticipated across all end-use sectors, such as residential and commercial, the overall consumption was estimated to grow by 21.4% compared to 2022.

- The residential sector accounts for the highest consumption volume of ready mix mortar in Indonesia. For instance, in 2022, the residential sector held a share of around 40% of the total ready mix concrete volume consumption across Indonesia. The most preferred type of ready mix concrete in the sector is transit mixed, which accounted for 76% of the consumption in 2022.

- After residential, the highest volume of ready mix concrete in Indonesia is consumed in the industrial & institutional sector as it has the largest construction area after residential. For instance, in 2022, the industrial & institutional sector accounted for 31% of the total new floor area of the country. The demand for shrink-mixed type ready mix concrete in the sector is expected to record the fastest CAGR of 8.3% during the forecast period (2023-2030).

- The overall demand for ready mix concrete in Indonesia is anticipated to grow, with the fastest CAGR of 8.94% in the commercial sector during the forecast period. This is mainly due to the usage of transit mix in the sector, which is expected to grow with a CAGR of 9.20% during the forecast period. Transit mix accounted for 73% of the country's ready mix concrete demand in 2022.

Indonesia Ready Mix Concrete Market Trends

Indonesian commercial real estate market volume is projected to reach USD 1.39 trillion by 2028 and is likely to augment the demand for commercial sector

- In 2022, Indonesia witnessed a 9.7% decline in the volume of new commercial floor area compared to the previous year. This drop was a result of a return to normalcy following a decline in building activities during the COVID-19 pandemic. Even before the pandemic, commercial buildings in Indonesia were already showing a downward trend in annual energy intensity, accounting for a rate of 2.64% per year. However, in 2023, the country saw a rebound, registering a 5.7% increase in the volume of new commercial floor area, driven by a surge in foreign direct investment (FDI) necessitating new offices, warehouses, and retail spaces.

- Amidst the COVID-19 pandemic, in 2020 and 2021, Indonesia witnessed a significant surge in the volume of new commercial floor area, accounting for approximately 9.6 million square feet. The government's focus on revitalizing the economy led to measures such as easing construction-related quarantines, both in private and public projects. This allowed employees to resume work on-site and companies to continue their operations. Notably, the value of completed constructions in Indonesia stood at around IDR 1.32 quadrillion in 2020 and rose to IDR 1.42 quadrillion in 2021.

- The volume of new commercial floor area in Indonesia is projected to witness a robust growth of around 58.72% by 2030 compared to 2023. This surge is driven by a rising demand for shopping malls, offices, and other commercial spaces. The retail real estate segment is emerging as a particularly captivating sector in the country. For instance, the volume of the commercial real estate market is anticipated to reach USD 1.39 trillion by 2028. The commercial new floor area in Indonesia is expected to maintain steady growth, registering a CAGR of 6.82% during the forecast period.

Increase in demand for housing units is likely to augment the residential sector's growth

- In 2022, Indonesia witnessed a 7.10% volume growth in residential new floor area compared to 2021. This surge can be attributed to increased population, wealth, and urbanization. The government-led housing aid reached IDR 29 trillion in 2022, which was projected to increase to IDR 32 trillion in 2023 under the Housing Financing Liquidity Facility scheme. This initiative aims to construct at least 220 thousand houses. The residential construction sector is poised to witness a significant growth rate. It was estimated to increase to approximately 56 million square feet in 2023 compared to the preceding year.

- In 2020, the volume of residential new floor areas in Indonesia grew by 7.06% compared to 2019. This was a strategic move by the government, prioritizing construction to mitigate the economic downturn and support households grappling with reduced incomes. Consequently, restrictions on construction activities, including quarantines, were significantly eased. However, in 2021, the trend reversed, with a decline of about 12.54% in residential new floor area, primarily attributed to a dip in foreign direct investment (FDI) in the construction sector. FDI for construction plummeted by 51% in 2021 compared to the previous year.

- The residential new floor area in Indonesia is projected to witness a CAGR of 6.08% in volume during the forecast period. This growth stems from the country's increasing urbanization, bolstered by government initiatives and foreign and domestic investments. These factors, directly and indirectly, underscore the mounting housing needs in the nation, ultimately driving residential building construction. Projections indicate that to meet the escalating demand, the country would require between 820,000 and 1 million housing units annually by 2030.

Indonesia Ready Mix Concrete Industry Overview

The Indonesia Ready Mix Concrete Market is fragmented, with the top five companies occupying 7%. The major players in this market are Heidelberg Materials, PT Cemindo Gemilang Tbk, PT Waskita Beton Precast Tbk, SCG and SIG (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End Use Sector Trends

- 4.1.1 Commercial

- 4.1.2 Industrial and Institutional

- 4.1.3 Infrastructure

- 4.1.4 Residential

- 4.2 Major Infrastructure Projects (current And Announced)

- 4.3 Regulatory Framework

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size, forecasts up to 2030 and analysis of growth prospects.)

- 5.1 End Use Sector

- 5.1.1 Commercial

- 5.1.2 Industrial and Institutional

- 5.1.3 Infrastructure

- 5.1.4 Residential

- 5.2 Product

- 5.2.1 Central Mixed

- 5.2.2 Shrink Mixed

- 5.2.3 Transit Mixed

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Heidelberg Materials

- 6.4.2 Kalla Group.

- 6.4.3 PT Cemindo Gemilang Tbk

- 6.4.4 PT Waskita Beton Precast Tbk

- 6.4.5 PT. Adhimix Precast Indonesia

- 6.4.6 PT. Beton Indotama Surya

- 6.4.7 PT. Fresh Beton Indonesia

- 6.4.8 PT. Modernland Realty Tbk.

- 6.4.9 SCG

- 6.4.10 SIG

7 KEY STRATEGIC QUESTIONS FOR CONCRETE, MORTARS AND CONSTRUCTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

预拌混凝土:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

预拌混凝土:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 预拌混凝土市场规模、份额和成长分析(按产量、类型、搅拌机类型和地区划分)-2026-2033年产业预测

预拌混凝土市场规模、份额和成长分析(按产量、类型、搅拌机类型和地区划分)-2026-2033年产业预测 2025年全球混凝土搅拌站市场报告2025年全球混凝土搅拌站搅拌机市场报告

2025年全球混凝土搅拌站市场报告2025年全球混凝土搅拌站搅拌机市场报告 混凝土搅拌站市场分析与预测(至2034年):类型、产品、服务、技术、组件、应用、材料类型、流程、最终使用者、能力

混凝土搅拌站市场分析与预测(至2034年):类型、产品、服务、技术、组件、应用、材料类型、流程、最终使用者、能力 按纤维类型、交付方式、强度等级、最终用途和添加剂类型分類的预拌混凝土市场—2025-2032年全球预测

按纤维类型、交付方式、强度等级、最终用途和添加剂类型分類的预拌混凝土市场—2025-2032年全球预测 2025-2029年全球预拌混凝土市场

2025-2029年全球预拌混凝土市场 混凝土厂设备市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测混凝土搅拌站市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测预拌混凝土市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

混凝土厂设备市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测混凝土搅拌站市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测预拌混凝土市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

▼