|

市场调查报告书

商品编码

1692442

纸和纸板包装:市场占有率分析、行业趋势和统计数据、成长预测(2025-2030 年)Paper and Paperboard Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

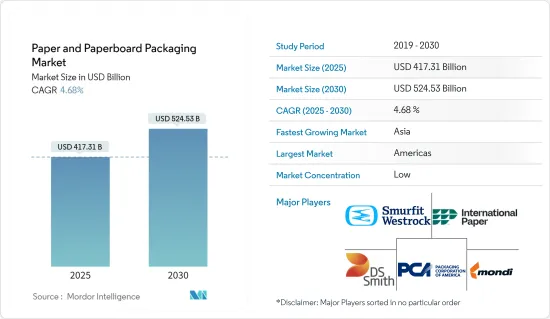

预计 2025 年纸和纸板包装市场规模将达到 4,173.1 亿美元,到 2030 年将达到 5,245.3 亿美元,预测期内(2025-2030 年)的复合年增长率为 4.68%。

主要亮点

- 纸板包装是包装食品市场的热门选择。它用于各种产品,包括汤、调味品和乳製品。它们通常涂有聚合物或塑胶以确保清洁并保持食品品质。此涂层可起到阻挡湿气和外部污染物的作用,延长包装食品的保质期。纸板的优点是比玻璃或金属包装更轻,同时仍能保持产品的新鲜度。这种轻质有助于降低运输成本并减少对环境的影响。它的气味和味道是中性的,不会干扰内容物的味道或香气,使其成为理想的食品包装材料。纸板可回收和生物分解,满足消费者对永续包装解决方案日益增长的需求。纸板的多功能性意味着它可以适应各种形状和尺寸,以满足一系列食品需求并增强零售环境中的货架吸引力。

- 电子商务销售额的成长和折迭纸盒包装需求的不断增长正在推动纸板包装市场的发展。然而,高性能替代品的出现可能会阻碍市场的成长。纸板包装由于其多功能性,仍然是受欢迎的环保选择。它们可以製造成各种尺寸且占地面积小,适合用于多个最终用户行业。这种适应性加上其环境效益,使得纸板包装成为许多行业的首选。

- 世界各地的消费者现在都意识到塑胶包装对环境的影响,并将他们的购买偏好转向更环保的选择。这种意识涵盖多个产品类型,从食品和饮料到个人保养用品到电子产品。製造商面临来自消费者、政府和媒体的压力,要求他们采用环保产品、包装和工艺。这种压力导致了纸板包装设计的创新,包括可回收和可堆肥材料的开发。

- 消费者愿意为环保包装支付额外费用,进一步推动了环保包装的趋势。这种价格接受度反映出人们对永续包装的长期环境成本的认识日益加深。如今,许多消费者认为环保包装对于产品的价值提案至关重要。

- 预计这些因素将推动纸板包装行业的显着成长。该公司正在投资研发,以创造更永续的纸板解决方案,例如由再生材料製成并来自负责任管理的森林的纸板解决方案。纸板技术的进步改善了其性能特征,使其成为许多应用中塑胶的可行替代品。因此,纸板包装产业有望向各行各业扩张,满足功能性和环境责任的双重需求。

- 美国超过 60% 的纸板包装被收集和回收。这种广泛的回收利用显示全国越来越重视包装的永续性。该公司也推出可回收纸板产品,以满足消费者对环保选择的需求。例如,Cascades 最近推出了由可回收纤维製成的纸板托盘,展示了永续包装解决方案的创新。同样,SIG 还开发了由消费后废弃物回收聚合物製成的纸盒,进一步表明了该行业致力于减少包装材料对环境的影响和促进循环经济原则。

- 这种纸张是由新种植的森林的树纤维和再生纸製成的。森林砍伐和森林劣化是全球性问题。然而,儘管纸质包装的需求不断增加,但不负责任的森林砍伐却造成原材料的损失,严重影响纸板包装产业。据忧思科学家联盟称,纸张等「木製品」约占森林砍伐总量的 10%,可能会限制市场。

- 纸包装主要由新种植的森林中的木纤维和再生纸製成。该行业严重依赖这些原材料来满足全球对纸质包装解决方案日益增长的需求。然而,这种不断增长的需求正在世界各地造成严重的环境问题,特别是森林砍伐和森林劣化。

- 不负责任的森林砍伐威胁着纸板包装产业的长期永续性,因此该产业面临重大挑战。如果目前的趋势持续下去,该行业可能很快就会面临严重的原材料短缺。这种潜在的短缺可能导致生产成本上升和供应有限,最终影响该行业满足市场需求的能力。

- 据忧思科学家联盟称,包括纸张在内的木製品造成了全球约 10% 的森林砍伐。这项统计数据凸显了造纸业对世界森林资源的影响。随着人们对环境问题的认识不断增强,消费者和监管机构越来越严格地审查纸质包装製造商的采购惯例。

- 为了应对这些挑战,造纸业正在探索永续的林业实践,投资重新造林工作并增加再生材料的使用。然而,在满足市场需求和确保环境永续性之间取得平衡仍然是一个复杂的问题,可能会限制未来几年的市场成长。该行业采用和创新更永续实践的能力将决定其未来发展轨迹和市场潜力。

纸和纸板包装市场的趋势

食品和饮料行业需求增加

- 电子商务销售额的成长以及食品和饮料行业对纸质包装的需求的增加正在推动市场的发展。根据国际货币基金组织的数据,预计 2022 年食品和饮料的消费者支出将达到 950 万美元,到 2026 年将成长到 1,221 万美元。食品和饮料行业的这些成长趋势预计将推动全球对纸和纸板包装的需求。

- 电子商务的快速扩张大大增加了对运输包装和产品保护包装的需求。同时,食品和饮料行业越来越青睐永续和可回收的包装解决方案,导致折迭式纸盒包装的采用率增加。製造商和零售商正在寻找高效、环保的包装选择,以满足消费者的期望并遵守监管要求;这些因素共同推动了市场成长。

- 食品和饮料製造商正在加强满足消费者对永续性、性能、可及性和更健康食品选择的需求。这种变化是由环保意识的增强和消费者偏好的变化所推动的。生物分解性塑胶和再生纸产品等永续包装材料在该行业越来越普遍。纸袋在饭店、餐厅、咖啡馆和其他餐饮场所越来越受欢迎。纸袋具有生物分解性、可回收、二氧化碳排放塑胶袋少等优点。

- *许多企业采用纸袋作为其企业社会责任的一部分,并遵守有关一次性塑胶的当地法规。外带和网路订餐的日益普及进一步推动了餐饮业对纸袋的需求。随着越来越多的消费者选择外带和外送服务,对耐用、环保的包装解决方案的需求显着增加。纸袋为运输食品提供了实用、环保的选择,符合消费者的期望和产业永续性目标。

- 消费者偏好正在推动饮料及其包装的流行趋势。消费者对永续性、客製化和电子商务的期望不断变化,刺激着包装设计和功能的创新。对永续性的关注导致了环保材料和可回收包装选择的发展。客製化的需求催生了允许个性化和独特产品体验的包装。电子商务的兴起要求包装解决方案能够确保产品在运送过程中的完整性并增强网路购物购物者的拆包体验。这些不断变化的偏好继续影响饮料包装产业,迫使製造商适应和创新以满足消费者的需求。

- 为了满足消费者的偏好,世界各地的主要食品和饮料公司都设定了使其包装完全可回收或生物分解的目标。例如,百加得宣布计划透过开发一种新型纸质饮料瓶,在 2030 年消除塑料,以响应全球减少一次性塑料的努力。对循环经济原则的承诺可能会促进造纸业的进一步创新。

- 包装提供安全密封和可追溯性功能,以提高产品可靠性。设计师使用手工元素和当地图像来传达其产品的起源。品牌经常与当地艺术家合作讲述引人入胜的故事。区域标识凸显了产品的产地。环保纸和纸板广泛用于包装各种食品,包括乳製品、食品和饮料、干货和快餐。

预计亚洲将占很大份额

- 中国是亚洲最大的折迭纸盒包装市场之一,由于食品和饮料行业的巨大成长潜力,预计其需求将会增加。这种成长受到多种因素的推动,包括都市化加快、消费者偏好变化以及零售连锁店的扩张。中国是加工纸和瓦楞纸板的主要生产国,对该行业具有重大影响力。

- 该国的生产能力对于满足国内和国际折迭纸盒包装材料的需求至关重要。 2023年9月,中国纸包装产量为1,287万吨,2024年1-2月产量上升至2,242万吨。产量的大幅成长反映了各行各业对纸包装的需求不断增长,尤其是食品和饮料行业。产量的激增也凸显了中国扩大生产以满足市场需求的能力,进一步巩固了其作为全球折迭纸盒包装行业关键参与者的地位。

- 印度、中国、日本和韩国是亚洲地区工业化快速发展的主要国家,为瓦楞纸製造商创造了巨大的机会。这些国家的各个产业都在经历成长,包括汽车、电子和消费品,对包装解决方案的需求也随之增加。瓦楞纸箱广泛应用于食品饮料、电子、电子商务等各行业。

- 瓦楞包装的多功能性和适应性使其适合保护和运输各种各样的产品。随着消费者环保意识的增强和对经济高效的包装选择的追求,该地区对此类包装解决方案的需求正在增长。纸板可回收和生物分解,符合该地区对永续性日益增长的关注。

- 印度纸张和纸板产业将当前的转型期视为机会和挑战。该行业旨在开发具有成本效益且价格合理的替代品来满足市场需求。全国各地的造纸厂正在进行试验,生产用于各种用途的纸张和纸板,包括搬运、保护、包裹、包装和容器。印度最近对各种上游纸产品的需求增加。

- 印度食品和饮料用纸和纸板包装需求大幅增加。这一增长是由于消费者需求的增加和新公司进入市场。扩张的主要驱动力是消费者生活方式的改变、都市化的加速以及国内有组织的零售业的成长。食品和饮料行业正在经历包装产品的激增,从已调理食品到食品和饮料,都需要高效且有吸引力的包装解决方案。 Zomato、Swiggy等外宅配服务的快速成长,大大促进了食品饮料包装材料消费的扩大。这些平台彻底改变了人们订购和消费食品的方式,创造了新的包装需求领域。外带容器、食品饮料杯、纸质食品袋的需求急剧增加,推动了纸和纸板包装市场的成长。

- 线上食品配送平台 Zomato 宣布“100% 塑胶中性配送”,并设定了未来三年内使用永续包装配送超过 1 亿份订单的目标。该公司计划与包括政府主导的倡议、社会企业和新兴企业在内的各相关人员合作,为食品服务业开发创新的包装解决方案。

- 新兴国家对纸张和纸浆的需求不断增长,尤其是中国,其人均纸张消费量增长最快。受零售业和电子商务行业扩张以及环保包装产品需求不断增长的推动,中国纸浆和纸包装行业正在经历成长。网路购物平台和线上消费者的增加、消费者对永续包装的偏好的改变以及政府的支持性政策总体上推动了该地区对纸和纸板包装产品的需求。

- 日本是各行各业纸製品的重要消费国,包括报纸、包装、印刷和通讯、卫生产品和其他用途。在包装方面,由于消费者对永续包装的意识不断增强、对森林砍伐的担忧以及原材料的可用性等因素,我们看到了向使用纸张的转变。

- 日本的纸和纸板包装市场也在稳定成长。对食品、饮料和包装食品的需求不断增长,推动了日本对瓦楞包装的需求。日本加工食品产业的扩张预计将成为纸板包装市场的主要动力。除了调查对象国家的亚太国家外,台湾、马来西亚、新加坡和越南等其他国家也显示出在该领域占据重要市场占有率的潜力。

纸和纸板包装市场概览

全球纸和纸板包装市场较为分散,国际纸业公司、DS Smith PLC 和美国包装公司等多家全球和区域性企业在竞争激烈的市场空间中争夺关注。该市场的特点是产品差异化程度低、产品渗透率高、竞争激烈。

- 2024 年 5 月—全球永续包装和造纸公司 Mondi 在义大利杜伊诺举行奠基仪式,启动对该工厂的 2 亿欧元(2.164 亿美元)投资。该计划将把工厂现有的造纸机改造成生产高品质再生箱板纸的机器。该投资旨在加强与当地相关人员的伙伴关係,并为该地区的经济发展做出贡献。

- 2024 年 4 月—国际纸业和 DS Smith 宣布,双方已就推荐的全股票组合达成一致,以打造永续包装解决方案的全球领导者。

- 2024 年 1 月—WestRock Corporation 宣布计划在威斯康辛州普莱森特草原建造一家新的瓦楞包装厂,以满足五大湖地区日益增长的客户需求。新工厂建成后,该公司计划关闭位于芝加哥北部的工厂。此次投资旨在增强 WestRock 的生产能力并改善其在五大湖地区的成本结构。预计建设成本约1.4亿美元。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概览

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争强度

- 产业生态系统分析

第五章市场动态

- 市场驱动因素

- 食品和饮料行业需求增加

- 对塑胶包装产品的限制将导致需求增加

- 电子商务的兴起推动了对纸和纸板包装的需求

- 市场挑战

- 原材料成本上涨和外包

- 森林砍伐对纸和纸板包装的影响

第六章市场区隔

- 北美洲

- 依产品类型

- 折迭式纸盒

- 瓦楞纸箱

- 其他产品类型

- 按最终用户产业

- 食物

- 饮料

- 卫生保健

- 个人护理

- 电器

- 其他行业

- 按国家

- 美国

- 加拿大

- 依产品类型

- 欧洲

- 依产品类型

- 折迭式纸盒

- 瓦楞纸箱

- 其他产品类型

- 按最终用户产业

- 食物

- 饮料

- 卫生保健

- 个人护理

- 电器

- 其他行业

- 按国家

- 英国

- 德国

- 法国

- 义大利

- 波兰

- 依产品类型

- 亚太地区

- 依产品类型

- 折迭式纸盒

- 瓦楞纸箱

- 其他产品类型

- 按最终用户产业

- 食物

- 饮料

- 卫生保健

- 个人护理

- 电器

- 其他行业

- 按国家

- 中国

- 印度

- 韩国

- 日本

- 印尼

- 泰国

- 澳洲和纽西兰

- 依产品类型

- 中东和非洲

- 依产品类型

- 折迭式纸盒

- 瓦楞纸箱

- 其他产品类型

- 按最终用户产业

- 食物

- 饮料

- 卫生保健

- 个人护理

- 电器

- 其他行业

- 按国家

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 埃及

- 以色列

- 卡达

- 依产品类型

- 拉丁美洲

- 依产品类型

- 折迭式纸盒

- 瓦楞纸箱

- 其他产品类型

- 按最终用户产业

- 食物

- 饮料

- 卫生保健

- 个人护理

- 电器

- 其他行业

- 按国家

- 巴西

- 墨西哥

- 阿根廷

- 哥伦比亚

- 依产品类型

第七章 交易情景

- 历史进出口分析

- 主要进口国名单

- 主要出口国家一览

- 主要收穫

第八章竞争格局

- 公司简介

- International Paper Company

- Eastern Pak Limited

- Mondi Group

- Smurfit Westrock

- DS Smith PLC

- Packaging Corporation of America

- Cascades Inc.

- Nippon Paper Industries Ltd

- Oji Holdings Corporation

- Stora Enso Oyj

- Billerud AB

- Sonoco Products Company

第九章投资分析

第十章:投资分析市场未来展望

The Paper and Paperboard Packaging Market size is estimated at USD 417.31 billion in 2025, and is expected to reach USD 524.53 billion by 2030, at a CAGR of 4.68% during the forecast period (2025-2030).

Key Highlights

- Paperboard packaging is a popular choice in the packaged food market. It is used for various products, including soups, seasonings, and dairy items. It is often coated with polymers or plastics to maintain cleanliness and preserve food quality. This coating acts as a barrier against moisture and external contaminants, extending the shelf life of packaged foods. Paperboard offers weight reduction advantages over glass and metal packaging while ensuring product freshness. This lightweight nature contributes to reduced transportation costs and environmental impact. Its neutral odor and taste properties make it an ideal packaging material for food products, as it does not interfere with the flavor or aroma of the contents. Paperboard is recyclable and biodegradable, aligning with the growing consumer demand for sustainable packaging solutions. The versatility of paperboard allows for various shapes and sizes, accommodating different food product requirements and enhancing shelf appeal in retail environments.

- The growth of e-commerce sales and increasing demand for folded carton packaging are driving the paperboard packaging market. However, the availability of high-performance alternatives may hinder market growth. Paperboard packaging remains a popular eco-friendly option due to its versatility. It can be produced in various sizes with a compact footprint, making it suitable for use across multiple end-user industries. This adaptability, combined with its environmental benefits, positions paperboard packaging as a preferred choice in many sectors.

- Consumers across the world are now aware of the environmental impact of plastic packaging, shifting their purchasing preferences toward eco-friendly options. This awareness extends across various product categories, from food and beverages to personal care items and electronics. Manufacturers face pressure from consumers, governments, and media to adopt environmentally responsible products, packaging, and processes. This pressure has led to innovations in paperboard packaging design, including the development of recyclable and compostable materials.

- * The trend toward eco-friendly packaging is further bolstered by consumers' willingness to pay premium prices for such options. This price tolerance reflects a growing understanding of the long-term environmental costs of non-sustainable packaging. Many consumers now view environmentally friendly packaging as integral to a product's value proposition.

- These factors are expected to drive substantial growth in the paperboard packaging industry. Companies are investing in research and development to create more sustainable paperboard solutions, including those made from recycled materials or sourced from responsibly managed forests. Advancements in paperboard technology are improving its performance characteristics, making it a viable alternative to plastic in many applications. As a result, the paperboard packaging sector is poised for expansion across various industries, meeting the dual demands of functionality and environmental responsibility.

- Over 60% of communities in the United States collect and recycle paperboard packaging. This widespread adoption of recycling practices demonstrates a growing commitment to sustainability in packaging nationwide. Companies are also introducing recyclable paperboard products to meet consumer demand for eco-friendly options. For example, Cascades recently launched a cardboard tray made from recyclable fibers, showcasing innovation in sustainable packaging solutions. Similarly, SIG has developed cartons using recycled polymers from post-consumer waste, further illustrating the industry's efforts to reduce environmental impact and promote circular economy principles in packaging materials.

- * Paper is made from tree fibers from newly planted forests or recycled paper. Deforestation and forest degradation are global issues. However, even though there is an increase in demand for paper packaging, irresponsible deforestation will severely impact the paperboard packaging industry by causing a loss of raw materials. According to the Union of Concerned Scientists, "wood products," such as paper, account for around 10% of total deforestation, which might limit the market.

- Paper packaging is primarily produced from tree fibers sourced from newly planted forests or recycled paper. The industry relies heavily on these raw materials to meet the growing global demand for paper-based packaging solutions. However, this increasing demand has raised significant environmental concerns worldwide, particularly regarding deforestation and forest degradation.

- The paperboard packaging industry faces a critical challenge as irresponsible deforestation threatens its long-term sustainability. If current trends continue, the sector may experience a severe shortage of raw materials shortly. This potential scarcity could lead to increased production costs and limited supply, ultimately affecting the industry's ability to meet market demands.

- According to the Union of Concerned Scientists, wood products, including paper, contribute to approximately 10% of worldwide deforestation. This statistic highlights the paper industry's s on global forest resources. As awareness of environmental issues grows, consumers and regulatory bodies are increasingly scrutinizing the sourcing practices of paper packaging manufacturers.

- To address these challenges, the industry is exploring sustainable forestry practices, investing in reforestation efforts, and increasing the use of recycled materials. However, the balance between meeting market demand and ensuring environmental sustainability remains a complex issue that may constrain market growth in the coming years. The industry's ability to innovate and adopt more sustainable practices will determine its future trajectory and market potential.

Paper and Paperboard Packaging Market Trends

Increase in Demand from the Food and Beverage Sector

- The growth of e-commerce sales and increasing demand for folded carton packaging in the food and beverage industry are driving the market. According to the International Monetary Fund, consumer spending on food and beverages reached USD 9.5 million in 2022 and is projected to grow to USD 12.21 million by 2026. This upward food and beverage sector trend will boost global demand for paper and paperboard packaging.

- The rapid expansion of e-commerce has significantly increased the demand for shipping and product protection packaging. Concurrently, the food and beverage industry has shown a growing preference for sustainable and recyclable packaging solutions, leading to increased adoption of folded-carton packaging. These factors collectively drive market growth as manufacturers and retailers seek efficient, environmentally friendly packaging options to meet consumer expectations and comply with regulatory requirements.

- Food and beverage manufacturers are intensifying efforts to meet consumer demands for sustainability, performance, accessibility, and healthier food options. This shift is driven by increasing environmental awareness and changing consumer preferences. Sustainable packaging materials, such as biodegradable plastics and recycled paper products, are becoming more prevalent in the industry. Paper bags are gaining popularity in hotels, restaurants, cafes, and other food establishments. These bags offer several advantages, including biodegradability, recyclability, and a lower carbon footprint than plastic alternatives.

- * Many businesses are adopting paper bags as part of their corporate social responsibility initiatives and to comply with local regulations on single-use plastics. The increasing trend of on-the-go meal delivery and online food ordering further drives the demand for paper bags in food services. As more consumers opt for takeout and delivery options, the need for sturdy, eco-friendly packaging solutions has grown significantly. Paper bags provide a practical and environmentally responsible choice for transporting food items, aligning with consumer expectations and industry sustainability goals.

- Consumer preferences drive trends in both beverages and their packaging. Changes in consumer expectations regarding sustainability, customization, and e-commerce have spurred innovation in packaging design and functionality. Sustainability concerns have led to the development of eco-friendly materials and recyclable packaging options. Customization demands have resulted in packaging that allows for personalization or unique product experiences. The rise of e-commerce has necessitated packaging solutions that ensure product integrity during shipping and enhance the unboxing experience for online shoppers. These evolving preferences continue to shape the beverage packaging industry, prompting manufacturers to adapt and innovate to meet consumer needs.

- Primary global food and beverage companies have established goals to make their packaging fully recyclable or biodegradable, responding to consumer preferences. For example, Bacardi announced plans to eliminate plastic by 2030 by developing new paper-based beverage bottles, aligning with the worldwide effort to reduce single-use plastics. This commitment to circular economy principles may lead to further innovations in the paper industry.

- Packaging enhances product authenticity through safety seals and traceability features. Designers use artisanal elements and local imagery to convey product origins. Brands often collaborate with local artists for compelling storytelling. Regional identifiers highlight product provenance. Paper and paperboard, being eco-friendly, are widely used for packaging various food products, including dairy, beverages, dry goods, and fast-food items.

Asia is Expected to Hold Significant Share

- China, one of Asia's largest folding carton packaging markets, is expected to see increased demand due to substantial growth potential in its food and beverage sector. This growth is driven by several factors, including rising urbanization, changing consumer preferences, and expanding retail chains. As a leading manufacturer of processed paper and cardboard, China significantly influences the industry.

- The country's production capacity is crucial in meeting domestic and international demand for folding carton packaging materials. In September 2023, China produced 12.87 million metric tons of these materials, which rose to 22.42 million in January-February 2024. This notable increase in production reflects the growing demand for folding carton packaging across various industries, particularly in the food and beverage sector. The surge in output also highlights China's ability to scale up manufacturing to meet market needs, further solidifying its position as a critical player in the global folding carton packaging industry.

- India, China, Japan, and South Korea are leading countries in the Asia region experiencing rapid industrialization, creating significant opportunities for corrugated packaging manufacturers. The growth of various industries in these countries, such as automotive, electronics, and consumer goods, has increased demand for packaging solutions. Corrugated boxes are widely used across multiple industries, including food and beverage, electronics, and e-commerce.

- Corrugated packaging's versatility and adaptability make it suitable for protecting and transporting a wide range of products. Demand for these packaging solutions is growing in the region as consumers become more environmentally conscious and seek cost-effective packaging options. Corrugated boxes are recyclable and biodegradable, aligning with the region's increasing focus on sustainability.

- The Indian paper and paperboard industry perceives the current transition phase as both an opportunity and a challenge. The sector aims to develop cost-effective and affordable alternatives to meet market demands. Paper mills nationwide are conducting trials to produce paper and paperboard for various applications, including carrying, protecting, wrapping, packaging, and container use. India has recently seen a growing demand for various upstream paper products.

- India has witnessed a substantial rise in paper and paperboard packaging for food and beverages. This increase is driven by growing consumer demand and the entry of new companies into the market. The expansion is primarily attributed to evolving consumer lifestyles, increasing urbanization, and the growth of organized retail in the country. The food and beverage industry has seen a surge in packaged products, ranging from ready-to-eat meals to beverages, all requiring efficient and attractive packaging solutions. The rapid growth of food delivery services, notably Zomato and Swiggy, has substantially contributed to the increased consumption of food and beverage packaging materials. These platforms have revolutionized the way people order and consume food, creating a new segment of packaging demand. The need for takeaway containers, beverage cups, and food-grade paper bags has risen dramatically, driving the growth of the paper and paperboard packaging market.

- Online food delivery platform Zomato announced '100% plastic-neutral deliveries' and set a target to deliver over 100 million orders in sustainable packaging within the next three years. The company plans to collaborate with various stakeholders, including government-led initiatives, social enterprises, and startups, to develop innovative packaging solutions for the restaurant industry.

- The demand for paper pulp is increasing in developing countries, particularly in China, which is the fastest-growing paper per capita consumer. China's paper packaging sector is experiencing growth, driven by the expanding retail and e-commerce industries and increased demand for environmentally friendly packaging products. The rise in online shopping platforms and online shoppers, shifting consumer preferences toward sustainable packaging, and supportive government policies have collectively boosted the demand for paper and paperboard packaging products in the region.

- Japan is a significant consumer of paper-based products across various industries, including newspapers, packaging, printing and communication, sanitary products, and other miscellaneous applications. The packaging sector has seen a shift toward paper usage due to increased consumer awareness about sustainable packaging, concerns over deforestation, and raw material availability, among other factors.

- The paper and paperboard packaging market in Japan is also experiencing steady growth. The increasing demand for beverages and packaged food has driven the need for corrugated packaging in the country. Japan's expanding processed food industry is expected to be a key driver for the paperboard packaging market. Beyond the countries included in the Asia-Pacific region study, other nations such as Taiwan, Malaysia, Singapore, and Vietnam also show significant potential for gaining substantial market share in this sector.

Paper and Paperboard Packaging Market Overview

The global paper and paperboard packaging market is fragmented, with several global and regional players, such as International Paper Company, DS Smith PLC, Packaging Corporation of America, and others, vying for attention in a contested market space. This market is characterized by low product differentiation, growing levels of product penetration, and high levels of competition.

- May 2024 - Mondi, a global player in sustainable packaging and paper, held a groundbreaking ceremony in Duino, Italy, marking the start of its EUR 200 million (USD 216.4 million) investment in the mill. The project involves converting the facility's existing paper machine into a high-quality recycled containerboard machine. This investment aims to strengthen partnerships with local stakeholders and contribute to the region's economic development.

- April 2024 - International Paper and DS Smith Plc announced an agreement on the terms of a recommended all-share combination, aiming to create a global leader in sustainable packaging solutions.

- January 2024 - WestRock Company unveiled plans to construct a new corrugated box facility in Pleasant Prairie, Wisconsin, to address increasing customer demand in the Great Lakes region. Upon completion of the new facility, the company intends to close its North Chicago plant. This investment aims to enhance WestRock's production capabilities and improve its cost structure in the Great Lakes area. The estimated construction cost is approximately USD 140 million.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definitions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHT

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Ecosystem Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Demand from the Food and Beverage Sector

- 5.1.2 Regulations on Plastic-based Packaging Products Contribute to Higher Demand

- 5.1.3 Increasing Growth of E-commerce Creates Demand for Various Paper and Paperboard Packaging Types

- 5.2 Market Challenges

- 5.2.1 Increasing Raw Material Costs and Outsourcing

- 5.2.2 Effects of Deforestation on Paper and Paperboard Packaging

6 MARKET SEGMENTATION

- 6.1 North America

- 6.1.1 By Product Type

- 6.1.1.1 Folding Cartons

- 6.1.1.2 Corrugated Boxes

- 6.1.1.3 Other Product Types

- 6.1.2 By End-user Vertical

- 6.1.2.1 Food

- 6.1.2.2 Beverage

- 6.1.2.3 Healthcare

- 6.1.2.4 Personal Care

- 6.1.2.5 Electrical

- 6.1.2.6 Other End-user Verticals

- 6.1.3 By Country

- 6.1.3.1 United States

- 6.1.3.2 Canada

- 6.1.1 By Product Type

- 6.2 Europe

- 6.2.1 By Product Type

- 6.2.1.1 Folding Cartons

- 6.2.1.2 Corrugated Boxes

- 6.2.1.3 Other Product Types

- 6.2.2 By End-user Vertical

- 6.2.2.1 Food

- 6.2.2.2 Beverage

- 6.2.2.3 Healthcare

- 6.2.2.4 Personal Care

- 6.2.2.5 Electrical

- 6.2.2.6 Other End-user Verticals

- 6.2.3 By Country***

- 6.2.3.1 United Kingdom

- 6.2.3.2 Germany

- 6.2.3.3 France

- 6.2.3.4 Italy

- 6.2.3.5 Poland

- 6.2.1 By Product Type

- 6.3 Asia-Pacific

- 6.3.1 By Product Type

- 6.3.1.1 Folding Cartons

- 6.3.1.2 Corrugated Boxes

- 6.3.1.3 Other Product Types

- 6.3.2 By End-user Vertical

- 6.3.2.1 Food

- 6.3.2.2 Beverage

- 6.3.2.3 Healthcare

- 6.3.2.4 Personal Care

- 6.3.2.5 Electrical

- 6.3.2.6 Other End-user Verticals

- 6.3.3 By Country***

- 6.3.3.1 China

- 6.3.3.2 India

- 6.3.3.3 South Korea

- 6.3.3.4 Japan

- 6.3.3.5 Indonesia

- 6.3.3.6 Thailand

- 6.3.3.7 Australia and New Zealand

- 6.3.1 By Product Type

- 6.4 Middle East and Africa

- 6.4.1 By Product Type

- 6.4.1.1 Folding Cartons

- 6.4.1.2 Corrugated Boxes

- 6.4.1.3 Other Product Types

- 6.4.2 By End-user Vertical

- 6.4.2.1 Food

- 6.4.2.2 Beverage

- 6.4.2.3 Healthcare

- 6.4.2.4 Personal Care

- 6.4.2.5 Electrical

- 6.4.2.6 Other End-user Verticals

- 6.4.3 By Country***

- 6.4.3.1 Saudi Arabia

- 6.4.3.2 United Arab Emirates

- 6.4.3.3 Egypt

- 6.4.3.4 Israel

- 6.4.3.5 Qatar

- 6.4.1 By Product Type

- 6.5 Latin America

- 6.5.1 By Product Type

- 6.5.1.1 Folding Cartons

- 6.5.1.2 Corrugated Boxes

- 6.5.1.3 Other Product Types

- 6.5.2 By End-user Vertical

- 6.5.2.1 Food

- 6.5.2.2 Beverage

- 6.5.2.3 Healthcare

- 6.5.2.4 Personal Care

- 6.5.2.5 Electrical

- 6.5.2.6 Other End-user Verticals

- 6.5.3 By Country***

- 6.5.3.1 Brazil

- 6.5.3.2 Mexico

- 6.5.3.3 Argentina

- 6.5.3.4 Colombia

- 6.5.1 By Product Type

7 TRADE SCENARIO

- 7.1 Historical Import-Export Analysis

- 7.2 List of Major Importing Countries

- 7.3 List of Major Exporting Countries

- 7.4 Key Takeaways

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 International Paper Company

- 8.1.2 Eastern Pak Limited

- 8.1.3 Mondi Group

- 8.1.4 Smurfit Westrock

- 8.1.5 DS Smith PLC

- 8.1.6 Packaging Corporation of America

- 8.1.7 Cascades Inc.

- 8.1.8 Nippon Paper Industries Ltd

- 8.1.9 Oji Holdings Corporation

- 8.1.10 Stora Enso Oyj

- 8.1.11 Billerud AB

- 8.1.12 Sonoco Products Company

9 INVESTMENT ANALYSIS

10 FUTURE OUTLOOK OF THE MARKET

全球纸板包装市场:预测(至2032年)-按产品类型、等级、包装形式、最终用户和地区分類的分析

全球纸板包装市场:预测(至2032年)-按产品类型、等级、包装形式、最终用户和地区分類的分析 PE涂布纸:全球市占率及排名、总收入及需求预测(2025-2031年)2032 年纸包装市场预测:按产品类型、等级、最终用户和地区进行的全球分析

PE涂布纸:全球市占率及排名、总收入及需求预测(2025-2031年)2032 年纸包装市场预测:按产品类型、等级、最终用户和地区进行的全球分析 卫生纸包装机市场按机器类型、最终用户、自动化程度、应用和包装材料划分-2025-2032 年全球预测挠性纸包装市场:依最终用途、材料类型、应用、结构、印刷技术和涂层类型划分-2025-2032年全球预测无菌纸包装市场(依最终用途、包装类型、材料、通路和包装尺寸)-2025-2032 年全球预测纸包装材料市场按产品类型、材料类型、印刷技术和应用划分-全球预测(2025-2032 年)蜂窝纸包装市场按包装类型、材料等级、应用、销售管道和最终用途行业划分-2025-2032年全球预测

卫生纸包装机市场按机器类型、最终用户、自动化程度、应用和包装材料划分-2025-2032 年全球预测挠性纸包装市场:依最终用途、材料类型、应用、结构、印刷技术和涂层类型划分-2025-2032年全球预测无菌纸包装市场(依最终用途、包装类型、材料、通路和包装尺寸)-2025-2032 年全球预测纸包装材料市场按产品类型、材料类型、印刷技术和应用划分-全球预测(2025-2032 年)蜂窝纸包装市场按包装类型、材料等级、应用、销售管道和最终用途行业划分-2025-2032年全球预测 纸质和塑胶包装的未来(2030-2040)

纸质和塑胶包装的未来(2030-2040) 2025年全球纸和纸板包装市场报告

2025年全球纸和纸板包装市场报告