|

市场调查报告书

商品编码

1693615

北美厢型车:市场占有率分析、产业趋势与统计数据、成长预测(2025-2030 年)North America Van - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

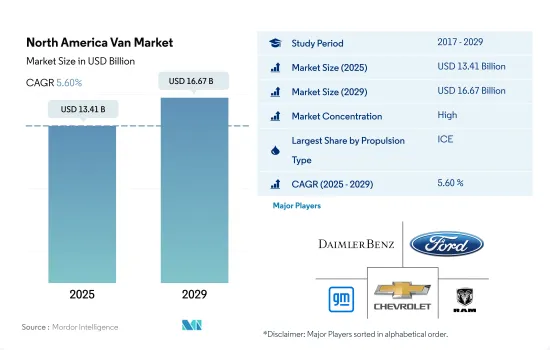

预计 2025 年北美货车市场规模将达到 134.1 亿美元,到 2029 年预计将达到 166.7 亿美元,预测期内(2025-2029 年)的复合年增长率为 5.60%。

受经济发展、新兴市场物流需求以及永续交通的推动,北美轻型商用车市场预计将稳定成长

- 2023年,北美轻型商用车市场所有动力类型的销售量都将略有成长,销售量将从2022年的4,046,122辆增至4,055,770辆。儘管增幅不大,但这标誌着市场趋于稳定,在不断变化的经济和环境条件下,轻型商用车市场将继续在支撑物流、零售和服务等各个行业方面发挥关键作用。预计2024年销量将达到4,058,449辆,显示北美对轻型商用车的需求稳定。稳定的市场表现反映了该地区经济的韧性和商业部门的多样化需求,凸显了轻型商用车在促进商业和贸易方面的重要作用。

- 北美轻型商用车市场的温和成长与更广泛的趋势一致,包括经济復苏、电子商务的激增以及对永续性的日益关注。虽然人们的注意力往往集中在电动和混合动力汽车上,但对轻型商用车的需求涵盖了多种推进类型,这标誌着向更清洁的交通方式的平衡转变。

- 从 2024 年到 2030 年,北美轻型商用车市场预计将逐步扩大,到 2030 年底销售量可能达到 4,473,267 辆。这一成长是由经济扩张、都市化和电子商务需求激增所推动的,因此需要强大的物流。此外,在环境问题和汽车效率进步的推动下,电动和混合动力轻型商用车市场将经历显着增长,并进一步塑造北美商业运输格局。

北美货车市场正在经历显着成长,全国趋势显示人们越来越偏好多功能、高效的运输解决方案。

- 由于石油供应减少和汽油价格上涨,汽车製造商正在积极探索汽车的替代燃料来源。 2022 年俄罗斯和乌克兰之间的衝突进一步加剧了油价上涨(过去几十年来油价已经翻了一番),促使全球推行电动车 (EV) 作为更经济的日常交通方式。税率也会影响全球燃料成本,美国的燃料税最低,为 19%,而印度的税率高达 69%。这些因素,加上过去二十年来不断上涨的燃料价格,使得电动车具有吸引力,因为它们的营业成本比传统内燃机 (ICE) 汽车低得多。

- 使其汽车产品电动化已成为汽车製造商的首要任务。沃尔沃的目标是到 2025 年,电动车将占其全球销量的 50%。斯巴鲁计划在 2035 年,旗下所有车型都配备混合动力汽车或电动车。福特计划到 2025 年在电动车领域投资 290 亿美元,而通用汽车计划投资 270 亿美元,实现到 2035 年所有小型车系列都实现电气化。其他製造商也有类似的雄心,虽然时间表和目标各不相同,但都致力于电气化。

- 2020年至2028年期间,北美计画推出12款新型电动厢型车。值得注意的是,大多数将是全新车型,包括ELMS UD-1、Rivian R1A和BrightDrop EV600。此外,Mercedes-Benz eSprinter 和福特 Transit 等现有的货车系列也准备在未来推出全电动货车。

北美厢型车市场趋势

由于政府的支持和对环境问题的日益关注,北美对电动车的需求正在增长。

- 近年来,俄罗斯共产党经历了显着的起伏。从 2017 年的 2.082 亿美元稳步上升至 2019 年的高峰。然而,由于新冠疫情带来的经济挑战,2020 年这一数字下降至 1.939 亿美元。值得注意的是,该市场预计将在 2022 年强劲復苏,达到 2.698 亿美元。復苏凸显了俄罗斯汽车产业的韧性以及奖励策略的潜在影响。

- 政府的激励和补贴对客户(尤其是物流和电子商务公司)采用电动商用车具有强大的吸引力。其中一个例子是加拿大和北美,政府宣布将于 2022 年 4 月为轻型和中型电动车提供 5,000 美元的联邦退税。预计这些努力将推动2024年至2030年间北美对电动商用车的需求大幅成长。

- 电动车部署计划、有吸引力的税收优惠和外国投资津贴等政府措施将推动北美国家的电动车市场发展。引人注目的是,2022 年 3 月,福斯承诺斥资 70 亿美元在北美建立电动车製造工厂。至2030年,福斯汽车计画为美国、墨西哥和加拿大的客户推出25款新型电动车型。因此,预计 2024 年至 2030 年间北美对电动车的需求将大幅成长。

北美厢型车产业概况

北美厢型车市场格局较为集中,前五大厂商占93.82%的市占率。该市场的主要企业有:戴姆勒股份公司(梅赛德斯-奔驰股份公司)、福特汽车公司、通用汽车公司、通用汽车公司(雪佛兰)和Ram Trucking, Inc.(按字母顺序排列)

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章执行摘要和主要发现

第二章 报告要约

第三章 引言

- 研究假设和市场定义

- 研究范围

- 调查方法

第四章 产业主要趋势

- 人口

- 人均GDP

- 消费者汽车支出(cvp)

- 通货膨胀率

- 汽车贷款利率

- 共乘

- 电气化的影响

- 电动车充电站

- 电池组价格

- 新款 Xev 车型发布

- 燃油价格

- OEM生产统计

- 法律规范

- 价值炼和通路分析

第五章市场区隔

- 推进类型

- 混合动力汽车和电动车

- 按燃料类别

- BEV

- PHEV

- ICE

- 按燃料类别

- 柴油引擎

- 汽油

- 混合动力汽车和电动车

- 国家

- 加拿大

- 墨西哥

- 美国

第六章竞争格局

- 关键策略趋势

- 市场占有率分析

- 商业状况

- 公司简介

- Daimler AG(Mercedes-Benz AG)

- Fiat Chrysler Automobiles NV

- Ford Motor Company

- General Motors Company

- GM Motor(Chevrolet)

- Nissan Motor Co. Ltd.

- Peugeot SA

- Ram Trucking, Inc.

- Toyota Motor Corporation

- Volkswagen AG

第七章:CEO面临的关键策略问题

第 8 章 附录

- 世界概况

- 概述

- 五力分析框架

- 全球价值链分析

- 市场动态(DRO)

- 资讯来源及延伸阅读

- 图片列表

- 关键见解

- 数据包

- 词彙表

简介目录

Product Code: 92999

The North America Van Market size is estimated at 13.41 billion USD in 2025, and is expected to reach 16.67 billion USD by 2029, growing at a CAGR of 5.60% during the forecast period (2025-2029).

Steady growth is anticipated in North America's LCV market, fueled by economic development, evolving logistics needs, and a focus on sustainable transportation

- In 2023, the North American market for LCVs across all propulsion types exhibited a slight increase, with sales volumes reaching 4,055,770 units from 4,046,122 units in 2022. This growth, albeit modest, indicates a stabilizing market that continues to play a crucial role in supporting various sectors, including logistics, retail, and services, amid evolving economic and environmental landscapes. In 2024, sales are expected to reach 4,058,449 units, indicating a steady demand for LCVs in North America. This steady market performance underscores the essential role of LCVs in facilitating commerce and trade, reflecting the region's economic resilience and the diverse needs of its commercial sectors.

- The North American LCV market's modest growth aligns with broader trends, including economic recovery, a surge in e-commerce, and a heightened focus on sustainability. While the spotlight often falls on electric and hybrid vehicles, the demand for LCVs spans a spectrum of propulsion types, signaling a balanced shift toward cleaner transportation.

- From 2024 to 2030, the North American LCV market is poised for gradual expansion, with projections pointing to sales potentially reaching 4,473,267 units by the end of 2030. This growth is propelled by economic expansion, urbanization, and the surging demands of e-commerce, necessitating robust logistics. Moreover, as environmental concerns and advancements in vehicle efficiency gain traction, the market for electric and hybrid LCVs is poised for a notable increase, further shaping the commercial transportation landscape in North America.

The North American van market is witnessing significant growth, with distinct trends in each country pointing toward a rising preference for versatile and efficient transportation solutions

- Automakers are proactively exploring alternative fuel sources for their vehicles, driven by the dwindling petroleum supplies and escalating gasoline costs. The 2022 Russia-Ukraine conflict further exacerbated the already doubled petroleum prices over the past few decades, prompting a global push towards electric vehicles (EVs) for more economical everyday transportation. Tax rates also play a role in global fuel costs, with the US having the lowest fuel tax at 19% and India imposing a hefty 69% tax. These factors, combined with the rising fuel prices over the last two decades, underscore the appeal of EVs, which boast significantly lower operating costs compared to traditional internal combustion engine (ICE) vehicles.

- Electrifying their vehicle portfolios has become a paramount objective for automakers. Volvo aims for EVs to constitute 50% of its global sales by 2025. Subaru plans to introduce hybrid or electric versions for all its models by 2035. Ford is planning to invest a substantial USD 29 billion in EVs by 2025, while GM is allocating USD 27 billion, with a vision to electrify its entire light-duty vehicle lineup by 2035. Other manufacturers have set similar ambitions, albeit with varying timelines and targets, all united by their commitment to electrification.

- North America is set to witness the launch of 12 new electric vans between 2020 and 2028. Notably, the majority will be entirely new models, including the ELMS UD-1, Rivian R1A, and BrightDrop EV600. Additionally, established van lines like the Mercedes-Benz eSprinter and Ford Transit are also gearing up to introduce all-electric variants in the future.

North America Van Market Trends

Growing demand for electric vehicles in North America driven by government support and growing environmental concerns

- The CVP in Russia has experienced significant fluctuations in recent years. It climbed steadily from USD 208.2 million in 2017, peaking in 2019. However, it dipped to USD 193.9 million in 2020, largely due to the economic challenges brought on by the COVID-19 pandemic. Notably, the market rebounded sharply in 2022, reaching USD 269.8 million. This resurgence highlights both the resilience of the Russian automotive sector and the potential impact of economic stimulus measures and heightened consumer demand.

- Government incentives and subsidies are proving to be a strong draw for customers, particularly logistics and e-commerce firms, in their adoption of electric commercial vehicles. A case in point is Canada and North America, where, in April 2022, the government unveiled federal rebates of USD 5000 for electric light- and medium-duty vehicles. These initiatives are expected to significantly bolster the demand for electric commercial vehicles in North America from 2024 to 2030.

- Government initiatives, including plans for EV deployment, attractive incentives, and foreign investment allowances, are set to propel the electric vehicle market across North American nations. In a notable move, in March 2022, Volkswagen committed a staggering USD 7 billion to establish an electric car manufacturing facility in North America. By 2030, the automaker plans to roll out 25 new EV models, catering to customers in the US, Mexico, and Canada. As a result, the demand for electric vehicles is projected to witness a notable surge across various North American countries from 2024 to 2030.

North America Van Industry Overview

The North America Van Market is fairly consolidated, with the top five companies occupying 93.82%. The major players in this market are Daimler AG (Mercedes-Benz AG), Ford Motor Company, General Motors Company, GM Motor (Chevrolet) and Ram Trucking, Inc. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Population

- 4.2 GDP Per Capita

- 4.3 Consumer Spending For Vehicle Purchase (cvp)

- 4.4 Inflation

- 4.5 Interest Rate For Auto Loans

- 4.6 Shared Rides

- 4.7 Impact Of Electrification

- 4.8 EV Charging Station

- 4.9 Battery Pack Price

- 4.10 New Xev Models Announced

- 4.11 Fuel Price

- 4.12 Oem-wise Production Statistics

- 4.13 Regulatory Framework

- 4.14 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 Propulsion Type

- 5.1.1 Hybrid and Electric Vehicles

- 5.1.1.1 By Fuel Category

- 5.1.1.1.1 BEV

- 5.1.1.1.2 PHEV

- 5.1.2 ICE

- 5.1.2.1 By Fuel Category

- 5.1.2.1.1 Diesel

- 5.1.2.1.2 Gasoline

- 5.1.1 Hybrid and Electric Vehicles

- 5.2 Country

- 5.2.1 Canada

- 5.2.2 Mexico

- 5.2.3 US

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Daimler AG (Mercedes-Benz AG)

- 6.4.2 Fiat Chrysler Automobiles N.V

- 6.4.3 Ford Motor Company

- 6.4.4 General Motors Company

- 6.4.5 GM Motor (Chevrolet)

- 6.4.6 Nissan Motor Co. Ltd.

- 6.4.7 Peugeot S.A.

- 6.4.8 Ram Trucking, Inc.

- 6.4.9 Toyota Motor Corporation

- 6.4.10 Volkswagen AG

7 KEY STRATEGIC QUESTIONS FOR VEHICLES CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

电动车底盘域控制单元市场按控制架构、车辆类型、底盘功能、自动驾驶等级和作业系统划分 - 全球预测(2026-2032 年)

电动车底盘域控制单元市场按控制架构、车辆类型、底盘功能、自动驾驶等级和作业系统划分 - 全球预测(2026-2032 年) 欧洲厢型车市场-份额分析、产业趋势与统计、成长预测(2026-2031)

欧洲厢型车市场-份额分析、产业趋势与统计、成长预测(2026-2031) 厢型车市场机会、成长驱动因素、产业趋势分析及预测(2026-2035年)电动货车改装套件市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)

厢型车市场机会、成长驱动因素、产业趋势分析及预测(2026-2035年)电动货车改装套件市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年) 厢型车市场-全球产业规模、份额、趋势、机会和预测(按吨位、推进类型、最终用途、地区和竞争细分,2020-2030 年预测)

厢型车市场-全球产业规模、份额、趋势、机会和预测(按吨位、推进类型、最终用途、地区和竞争细分,2020-2030 年预测) 2032 年厢型车改装市场预测:按车型、尺寸、改装、应用、最终用户和地区进行的全球分析美国货车:市场占有率分析、行业趋势和统计数据、成长预测(2025-2030 年)

2032 年厢型车改装市场预测:按车型、尺寸、改装、应用、最终用户和地区进行的全球分析美国货车:市场占有率分析、行业趋势和统计数据、成长预测(2025-2030 年) 货车市场规模、份额、趋势分析报告:按吨位、推进器、最终用途、地区、细分市场预测,2025-2030 年

货车市场规模、份额、趋势分析报告:按吨位、推进器、最终用途、地区、细分市场预测,2025-2030 年