|

市场调查报告书

商品编码

1693660

电动轻型商用车:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Electric Light Commercial Vehicles - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

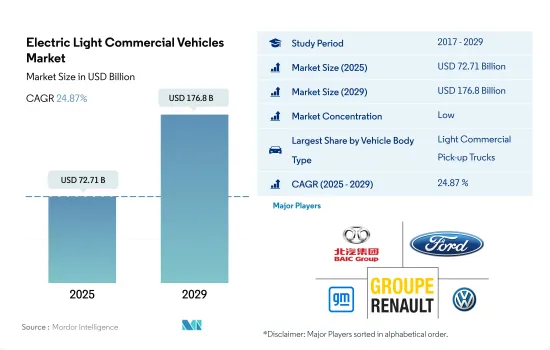

预计 2025 年电动轻型商用车市场规模将达到 727.1 亿美元,到 2029 年预计将达到 1,768 亿美元,预测期内(2025-2029 年)的复合年增长率为 24.87%。

随着网路和智慧型手机的普及,全球线上零售和电子商务蓬勃发展,带动全球轻型商用车购买量增加。

- 电子商务和物流行业是全球电动轻型商用车市场的主要驱动力。随着网路和智慧型手机的普及,网路零售和电子商务蓬勃发展,导致全球轻型商用车的购买量增加。 2021年全球轻型商用车产量达18,593,850辆,高于去年的17,217,990辆。

- 新冠疫情推动了网路销售的成长,导致全球电子商务市场的收益和用户数量都大幅增加。随着网上购物越来越受欢迎,预计这一趋势将会持续下去。 2020 年全球电子商务市场呈现快速扩张态势,预计未来一年仍将持续成长,2021 年收益将达到 26.7 兆美元。全球网路购物购物者的数量和比例一直在稳步增长,其中 2020 年出现了最大增长,这得益于疫情引发的向网路购物的转变。

- 欧洲、美国和中国等主要经济体的电子商务和物流产业正在强劲成长,推动对现代化物流网路的需求。戴姆勒、日产、福特、雷诺等知名轻型商用车製造商的电子商务销售额正在大幅成长,并正在加强其物流产业。传统上,皮卡车和货车一直是电子商务物流和消费者配送的首选车辆,进一步加强了全球轻型商用车市场。

汽车产业对清洁能源的需求不断增长以及鼓励采用电动车的政策是全球电动商用车发展的主要驱动力。

- 近年来,世界各国政府都在积极推行鼓励电动车发展的政策。特别是中国、印度、法国和英国已设定目标,2040年逐步淘汰汽油和柴油汽车。

- 汽车产业对清洁能源的需求不断增长是市场成长的主要动力。主要OEM正在重新调整其针对电动车的策略。例如,起亚汽车于2022年3月宣布进军电动皮卡领域,并计画在2027年推出两款车型。其中一款车型将直接与特斯拉Cybertruck、福特F-150 Lightning、Rivian R1T和GMC Hummer EV等现有竞争对手竞争。同样,福特在2022年3月宣布,计画在2024年推出四款商用电动车的新阵容。阵容包括将于2023年上市的新型1吨厢型车“Transit 自订”和多功能车“Tourneo 自订”,以及将于2024年上市的下一代“Transit Courier Van”和多功能车“Tourneo Courier”。

- 北美网路和智慧型手机普及率高,为电子商务公司进入零售电子商务市场提供了丰厚的机会。这种数位化环境不仅有利于电子商务公司的业务扩展,而且在推动全球电动轻型商用车市场和卡车领域发展方面发挥关键作用。因此,汽车製造商正在加大对卡车领域的研发投入,进一步推动电动卡车的发展。

全球电动轻型商用车市场趋势

全球需求成长和政府支持将推动电动车市场成长

- 电动车(EV)已成为汽车产业的重要组成部分,因为它具有提高能源效率、减少温室气体和污染排放的潜力。这种快速成长背后的主要因素是日益增长的环境问题和政府的支持。其中,电动车全球销售呈现强劲成长势头,2022年较2021年成长10.82%。据预测,2025年底,电动乘用车年销量将超过500万辆,约占汽车总销量的15%。

- 领先的製造商和组织(例如伦敦警察厅和消防队)正在积极推行电动车策略。例如,该公司设定了在 2025 年实现零排放汽车、在 2030 年实现 40% 货车电气化、到 2040 年实现全电动化的目标。预计全球也将出现类似的趋势,2024 年至 2030 年间电动车的需求和销售量将急剧成长。

- 在电池技术和汽车电气化进步的推动下,亚太地区和欧洲有望主导电动车生产。 2020年5月,起亚汽车欧洲公司公布“S计划”,宣布转向电动化策略。这项决定是在起亚电动车在欧洲创下销售纪录之际做出的。起亚雄心勃勃地计划在 2025 年之前在全球推出 11 款电动车,涵盖轿车、SUV 和 MPV 等各个领域。该公司的目标是到 2026 年实现全球电动车年销量达到 50 万辆。

电动轻型商用车产业概况

电动轻型商用车市场较为分散,前五大企业占22.60%的市场。市场的主要企业是:北京汽车股份有限公司、福特汽车公司、通用汽车公司、雷诺集团和大众汽车集团(按字母顺序排列)

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章执行摘要和主要发现

第二章 报告要约

第三章 引言

- 研究假设和市场定义

- 研究范围

- 调查方法

第四章 产业主要趋势

- 人口

- 非洲

- 亚太地区

- 欧洲

- 中东

- 北美洲

- 南美洲

- 人均GDP

- 非洲

- 亚太地区

- 欧洲

- 中东

- 北美洲

- 南美洲

- 消费者汽车购买支出(cvp)

- 非洲

- 亚太地区

- 欧洲

- 中东

- 北美洲

- 南美洲

- 通货膨胀率

- 非洲

- 亚太地区

- 欧洲

- 中东

- 北美洲

- 南美洲

- 汽车贷款利率

- 电气化的影响

- 电动车充电站

- 电池组价格

- 非洲

- 亚太地区

- 欧洲

- 中东

- 北美洲

- 南美洲

- 新款 Xev 车型发布

- 物流绩效指数

- 非洲

- 亚太地区

- 欧洲

- 中东

- 北美洲

- 南美洲

- 燃油价格

- 製造商生产统计

- 法律规范

- 价值炼和通路分析

第五章市场区隔

- 车辆配置

- 轻型商用车

- 燃料类别

- BEV

- FCEV

- HEV

- PHEV

- 地区

- 非洲

- 南非

- 非洲

- 亚太地区

- 澳洲

- 中国

- 印度

- 印尼

- 日本

- 马来西亚

- 韩国

- 泰国

- 亚太地区其他国家

- 欧洲

- 奥地利

- 比利时

- 捷克共和国

- 丹麦

- 爱沙尼亚

- 法国

- 德国

- 爱尔兰

- 义大利

- 拉脱维亚

- 立陶宛

- 挪威

- 波兰

- 俄罗斯

- 西班牙

- 瑞典

- 英国

- 其他欧洲国家

- 中东

- 沙乌地阿拉伯

- 其他中东地区

- 北美洲

- 加拿大

- 墨西哥

- 美国

- 北美其他地区

- 南美洲

- 阿根廷

- 巴西

- 南美洲其他地区

- 非洲

第六章 竞争格局

- 关键策略趋势

- 市场占有率分析

- 商业状况

- 公司简介

- BAIC Motor Corporation Ltd.

- BYD Auto Co. Ltd.

- Daimler AG(Mercedes-Benz AG)

- Dongfeng Motor Corporation

- Ford Motor Company

- General Motors Company

- Groupe Renault

- Nissan Motor Co. Ltd.

- Rivian Automotive Inc.

- Volkswagen AG

第七章:CEO面临的关键策略问题

第 8 章 附录

- 世界概况

- 概述

- 五力分析框架

- 全球价值链分析

- 市场动态(DRO)

- 资讯来源及延伸阅读

- 图片列表

- 关键见解

- 数据包

- 词彙表

简介目录

Product Code: 93053

The Electric Light Commercial Vehicles Market size is estimated at 72.71 billion USD in 2025, and is expected to reach 176.8 billion USD by 2029, growing at a CAGR of 24.87% during the forecast period (2025-2029).

The surge in online retail and e-commerce worldwide, fueled by increased internet and smartphone access, is leading to a rise in light commercial vehicle purchases globally

- The e-commerce and logistics industries are the primary drivers of the global electric light commercial vehicles market. The surge in online retail and e-commerce worldwide, fueled by increased internet and smartphone access, is leading to a rise in light commercial vehicle purchases globally. In 2021, global light commercial vehicle production reached 18,593.85 thousand units, up from 17,217.99 thousand units in the previous year.

- The COVID-19 pandemic propelled online sales, resulting in a significant boost in both revenue and user base for the global e-commerce market. This trend is expected to continue as internet shopping gains further traction. The global e-commerce market witnessed a rapid expansion in 2020, which continued over the next year, generating USD 26.7 trillion in revenue in 2021. The number and proportion of online shoppers have been steadily rising worldwide, with the largest surge seen in 2020, driven by the pandemic-induced shift to online shopping.

- The e-commerce and logistics industries are experiencing robust growth in major economies, including Europe, the United States, and China, driving the need for modernized distribution networks. Prominent light commercial vehicle manufacturers, such as Daimler, Nissan, Ford, and Renault, have witnessed a significant uptick in e-commerce sales, bolstering the logistics industry. Traditionally, pickup trucks and vans have been the go-to vehicles for e-commerce logistics and consumer deliveries, further bolstering the global light commercial vehicle market.

The rising demand for clean energy in the automotive industry and policies to promote the adoption of EVs are the key drivers for electric commercial vehicles globally

- Several governments worldwide have proactively implemented policies to promote the adoption of electric vehicles in recent years. Notably, China, India, France, and the United Kingdom have set targets to phase out the petrol and diesel vehicle industries by 2040.

- The rising demand for clean energy in the automotive industry is a key driver for the market's growth. Major OEMs are reshaping their strategies for electric vehicles. For example, in March 2022, Kia Motors unveiled plans to enter the electric pickup truck segment, with two models slated for release by 2027. One of these models will directly compete with established rivals like the Tesla Cybertruck, Ford F-150 Lightning, Rivian R1T, and GMC Hummer EV. Similarly, in March 2022, Ford announced its intention to introduce a new lineup of four commercial electric vehicles by 2024. This lineup included the all-new Transit Custom one-tonne van and Tourneo Custom multi-purpose vehicle launched in 2023, followed by the next-generation Transit Courier van and Tourneo Courier multi-purpose vehicle in 2024.

- North America, with its high internet and smartphone penetration, presents lucrative opportunities for e-commerce companies to tap into the retail e-commerce market. This digital landscape not only facilitates broader business expansion for e-commerce players but also plays a pivotal role in driving the global electric light commercial vehicles market as well as its truck segment. Consequently, automakers are ramping up their R&D investments in the truck segment, further fueling the growth of electric trucks.

Global Electric Light Commercial Vehicles Market Trends

The rising global demand and government support propel electric vehicle market growth

- Electric vehicles (EVs) have become indispensable in the automotive industry, driven by their potential to enhance energy efficiency and reduce greenhouse gas and pollution emissions. This surge is primarily attributed to growing environmental concerns and supportive government initiatives. Notably, global EV sales witnessed a robust 10.82% growth in 2022 compared to 2021. Projections indicate that annual sales of electric passenger cars will surpass 5 million by the end of 2025, accounting for approximately 15% of total vehicle sales.

- Leading manufacturers and organizations, like the London Metropolitan Police & Fire Service, have been actively pursuing their electric mobility strategies. For instance, they have set a target of a zero-emission fleet by 2025, with a goal of electrifying 40% of their vans by 2030 and achieving full electrification by 2040. Similar trends are expected globally, with the period from 2024 to 2030 witnessing a surge in demand and sales of electric vehicles.

- Asia-Pacific and Europe are poised to dominate electric vehicle production, driven by their advancements in battery technology and vehicle electrification. In May 2020, Kia Motors Europe unveiled its "Plan S," signaling a strategic shift toward electrification. This decision came on the heels of record-breaking sales of Kia's EVs in Europe. Kia has ambitious plans to introduce 11 EV models globally by 2025, spanning various segments like passenger vehicles, SUVs, and MPVs. The company aims to achieve annual global EV sales of 500,000 by 2026.

Electric Light Commercial Vehicles Industry Overview

The Electric Light Commercial Vehicles Market is fragmented, with the top five companies occupying 22.60%. The major players in this market are BAIC Motor Corporation Ltd., Ford Motor Company, General Motors Company, Groupe Renault and Volkswagen AG (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Population

- 4.1.1 Africa

- 4.1.2 Asia-Pacific

- 4.1.3 Europe

- 4.1.4 Middle East

- 4.1.5 North America

- 4.1.6 South America

- 4.2 GDP Per Capita

- 4.2.1 Africa

- 4.2.2 Asia-Pacific

- 4.2.3 Europe

- 4.2.4 Middle East

- 4.2.5 North America

- 4.2.6 South America

- 4.3 Consumer Spending For Vehicle Purchase (cvp)

- 4.3.1 Africa

- 4.3.2 Asia-Pacific

- 4.3.3 Europe

- 4.3.4 Middle East

- 4.3.5 North America

- 4.3.6 South America

- 4.4 Inflation

- 4.4.1 Africa

- 4.4.2 Asia-Pacific

- 4.4.3 Europe

- 4.4.4 Middle East

- 4.4.5 North America

- 4.4.6 South America

- 4.5 Interest Rate For Auto Loans

- 4.6 Impact Of Electrification

- 4.7 EV Charging Station

- 4.8 Battery Pack Price

- 4.8.1 Africa

- 4.8.2 Asia-Pacific

- 4.8.3 Europe

- 4.8.4 Middle East

- 4.8.5 North America

- 4.8.6 South America

- 4.9 New Xev Models Announced

- 4.10 Logistics Performance Index

- 4.10.1 Africa

- 4.10.2 Asia-Pacific

- 4.10.3 Europe

- 4.10.4 Middle East

- 4.10.5 North America

- 4.10.6 South America

- 4.11 Fuel Price

- 4.12 Oem-wise Production Statistics

- 4.13 Regulatory Framework

- 4.14 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 Vehicle Configuration

- 5.1.1 Light Commercial Vehicles

- 5.2 Fuel Category

- 5.2.1 BEV

- 5.2.2 FCEV

- 5.2.3 HEV

- 5.2.4 PHEV

- 5.3 Region

- 5.3.1 Africa

- 5.3.1.1 South Africa

- 5.3.1.2 Rest-of-Africa

- 5.3.2 Asia-Pacific

- 5.3.2.1 Australia

- 5.3.2.2 China

- 5.3.2.3 India

- 5.3.2.4 Indonesia

- 5.3.2.5 Japan

- 5.3.2.6 Malaysia

- 5.3.2.7 South Korea

- 5.3.2.8 Thailand

- 5.3.2.9 Rest-of-APAC

- 5.3.3 Europe

- 5.3.3.1 Austria

- 5.3.3.2 Belgium

- 5.3.3.3 Czech Republic

- 5.3.3.4 Denmark

- 5.3.3.5 Estonia

- 5.3.3.6 France

- 5.3.3.7 Germany

- 5.3.3.8 Ireland

- 5.3.3.9 Italy

- 5.3.3.10 Latvia

- 5.3.3.11 Lithuania

- 5.3.3.12 Norway

- 5.3.3.13 Poland

- 5.3.3.14 Russia

- 5.3.3.15 Spain

- 5.3.3.16 Sweden

- 5.3.3.17 UK

- 5.3.3.18 Rest-of-Europe

- 5.3.4 Middle East

- 5.3.4.1 Saudi Arabia

- 5.3.4.2 Rest-of-Middle East

- 5.3.5 North America

- 5.3.5.1 Canada

- 5.3.5.2 Mexico

- 5.3.5.3 US

- 5.3.5.4 Rest-of-North America

- 5.3.6 South America

- 5.3.6.1 Argentina

- 5.3.6.2 Brazil

- 5.3.6.3 Rest-of-South America

- 5.3.1 Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 BAIC Motor Corporation Ltd.

- 6.4.2 BYD Auto Co. Ltd.

- 6.4.3 Daimler AG (Mercedes-Benz AG)

- 6.4.4 Dongfeng Motor Corporation

- 6.4.5 Ford Motor Company

- 6.4.6 General Motors Company

- 6.4.7 Groupe Renault

- 6.4.8 Nissan Motor Co. Ltd.

- 6.4.9 Rivian Automotive Inc.

- 6.4.10 Volkswagen AG

7 KEY STRATEGIC QUESTIONS FOR VEHICLES CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

全球工业电动车市场规模、份额、趋势和成长分析报告(2026-2034年)全球电动商用车市场规模、份额、趋势和成长分析报告(2026-2034年)

全球工业电动车市场规模、份额、趋势和成长分析报告(2026-2034年)全球电动商用车市场规模、份额、趋势和成长分析报告(2026-2034年) 电动商用车市场-全球产业规模、份额、趋势、机会及预测(按车辆类型、动力系统、续航里程、地区及竞争格局划分,2021-2031年)电动商用车零件市场-全球产业规模、份额、趋势、机会及预测(依车辆类型、需求类别、零件类型、地区及竞争格局划分,2021-2031年)

电动商用车市场-全球产业规模、份额、趋势、机会及预测(按车辆类型、动力系统、续航里程、地区及竞争格局划分,2021-2031年)电动商用车零件市场-全球产业规模、份额、趋势、机会及预测(依车辆类型、需求类别、零件类型、地区及竞争格局划分,2021-2031年) 新能源商用车地板市场按动力类型、电池容量、充电方式、车辆类型和应用领域划分,全球预测(2026-2032)纯电动自装式垃圾车市场:按电池类型、有效载荷、功率输出、车速、应用和销售管道的全球预测(2026-2032)

新能源商用车地板市场按动力类型、电池容量、充电方式、车辆类型和应用领域划分,全球预测(2026-2032)纯电动自装式垃圾车市场:按电池类型、有效载荷、功率输出、车速、应用和销售管道的全球预测(2026-2032) 日本商用电动车市场规模、份额、趋势及预测(按车辆类型、驱动方式、应用领域、电池类型、电池容量和地区划分)(2026-2034 年)电动商用车市场规模、占有率、成长及全球产业分析:依类型、应用和地区划分的洞察,以及2024-2032年预测

日本商用电动车市场规模、份额、趋势及预测(按车辆类型、驱动方式、应用领域、电池类型、电池容量和地区划分)(2026-2034 年)电动商用车市场规模、占有率、成长及全球产业分析:依类型、应用和地区划分的洞察,以及2024-2032年预测 全球电动商用车市场:预测(至2032年)-按车辆类型、推进系统、零件、电池容量、续航里程、应用和地区进行分析电动商用车市场(按车辆类型、动力类型、应用、续航里程和充电基础设施划分)-全球预测,2025-2032年

全球电动商用车市场:预测(至2032年)-按车辆类型、推进系统、零件、电池容量、续航里程、应用和地区进行分析电动商用车市场(按车辆类型、动力类型、应用、续航里程和充电基础设施划分)-全球预测,2025-2032年

▼