|

市场调查报告书

商品编码

1693835

欧洲聚碳酸酯(PC):市场占有率分析、产业趋势和成长预测(2024-2029年)Europe Polycarbonate (PC) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

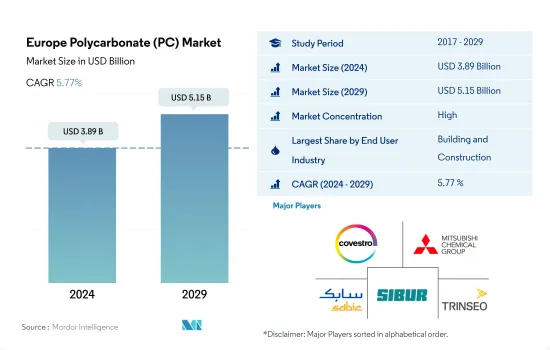

预计 2024 年欧洲聚碳酸酯 (PC) 市场规模为 38.9 亿美元,到 2029 年将达到 51.5 亿美元,预测期内(2024-2029 年)的复合年增长率为 5.77%。

即将启动的建设计划将推动聚碳酸酯需求

- 聚碳酸酯 (PC) 因其高抗衝击强度、重量轻、抗紫外线和光学透射性而被广泛应用于光碟、防弹玻璃、汽车头灯镜头、屋顶材料和嵌装玻璃等。 2022年,欧洲聚碳酸酯(PC)市场占全球聚碳酸酯(PC)市场以金额为准的19%。

- 2020年,受新冠疫情影响,PC市场以金额为准较2019年下降了10.41%。这是由于供应链中断、原材料短缺以及全部区域贸易交流停止所造成的。由于生产设施的恢復,2021年对PC树脂的需求以金额为准与2020年相比增加了19.22%。

- 汽车和建筑业是该地区 PC 树脂的最大消费者。预计到 2029 年,该地区的新建筑占地面积将达到 95 亿平方英尺,高于 2023 年的 78 亿平方英尺。预计该地区的汽车产量将从 2023 年的 1830 万辆增长到 2029 年的 2070 万辆。预计该地区建筑和汽车产量的成长将在未来几年推动对 PC 树脂的需求。

- 航太是该地区 PC 树脂成长最快的终端用户产业,预计预测期内以金额为准复合年增长率为 7.38%。航太工业对高强度、轻量材料的日益增长的趋势预计将推动该地区对 PC 树脂的需求。该地区的飞机零件製造收入预计将从 2023 年的 2,432 亿美元增至 2029 年的 3,488 亿美元。该地区航太零件产量的扩大预计将推动对 PC 树脂的需求。

汽车生产可能推动该地区聚碳酸酯的成长

- 2022年欧洲将占全球聚碳酸酯树脂消费量的19%(以体积为基础)。聚碳酸酯在法国和德国等欧洲国家用于汽车、航太、电气和电子等多个行业。德国、俄罗斯和义大利等国家是该地区聚碳酸酯树脂的主要消费国。

- 由于航太、汽车和电气电子工业的不断发展,德国是该地区最大的聚碳酸酯消费国。 2021 年,飞机零件和汽车生产将推动区域对聚碳酸酯树脂的需求,收入份额约为 16.9%,产量份额约为 20.19%。预计汽车和电气电子设备产量的成长将推动对聚碳酸酯树脂的需求。

- 由于汽车和电气电子行业产量的增加,义大利对聚碳酸酯树脂的需求正在大幅增长。义大利是欧盟第五大汽车生产国。 2022年产量预计为108万台,占该地区的6.13%(以单位计算)。该国的电气和电子产业也在不断扩张,预计到 2023 年将创造 171.5 亿美元的收益。预计这些因素将在预测期内推动欧洲对聚碳酸酯树脂的需求。

- 预计英国将成为聚碳酸酯树脂成长最快的消费国,预测期内(2023-2029 年)其收入复合年增长率为 6.19%。汽车产量的成长将带来该地区最高的 3.4%(以产量为基础)的复合年增长率,预计将推动该国对 PC 树脂的需求。

欧洲聚碳酸酯(PC)市场趋势

科技创新驱动家用电子电器市场

- 2017年至2021年,欧洲电气和电子设备产量的复合年增长率将超过3.8%。电子创新的快速步伐推动着对更新、更快的电气和电子产品的持续需求。因此,该地区对电气和电子设备生产的需求也在增加。

- 儘管远距工作和学习导致对电脑和笔记型电脑的需求增加,但欧洲消费性电子产品领域的每用户平均收入仍下降了 6.3%。 2020年销售额约2,521亿美元。因此,该地区2020年电气及电子设备产量较去年与前一年同期比较2.8%。

- 2021年,欧洲电气和电子设备出口额约2,283.7亿美元,比2020年成长12.4%。因此,该地区电气和电子设备产量有所增长,2021与前一年同期比较增长11.6%。

- 预计机器人、虚拟和扩增实境实境、物联网 (IoT) 和 5G 连线将在预测期内成长。由于技术进步,预计预测期内家用电子电器的需求将会上升。该地区消费电子领域的销售额预计将从 2023 年的 1,211 亿美元增至约 2027 年的 1,572 亿美元。到 2027 年,欧洲预计将成为全球第二大电气和电子设备生产国,占全球市场的 12.7% 左右。因此,预计未来几年家用电子电器的兴起将推动对电气和电子设备生产的需求。

欧洲聚碳酸酯(PC)产业概况

欧洲聚碳酸酯(PC)市场比较集中,前五大公司占100%的市占率。该市场的主要企业包括科思创股份公司、三菱化学株式会社、沙乌地基础工业公司、西布尔控股公司、盛禧奥等。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章执行摘要和主要发现

第二章 报告要约

第三章 引言

- 研究假设和市场定义

- 研究范围

- 调查方法

第四章 产业主要趋势

- 最终用户趋势

- 航太

- 车

- 建筑与施工

- 电气和电子

- 包装

- 进出口趋势

- 聚碳酸酯(PC)贸易

- 价格趋势

- 形态趋势

- 回收概述

- 聚碳酸酯(PC)回收趋势

- 法律规范

- EU

- 法国

- 德国

- 义大利

- 俄罗斯

- 英国

- 价值炼和通路分析

第五章市场区隔

- 最终用户产业

- 航太

- 车

- 建筑与施工

- 电气和电子

- 工业/机械

- 包装

- 其他的

- 国家

- 法国

- 德国

- 义大利

- 俄罗斯

- 英国

- 其他欧洲国家

第六章竞争格局

- 关键策略趋势

- 市场占有率分析

- 商业状况

- 公司简介

- CHIMEI

- Covestro AG

- Formosa Plastics Group

- LG Chem

- Lotte Chemical

- Mitsubishi Chemical Corporation

- SABIC

- SIBUR Holding PJSC

- Teijin Limited

- Trinseo

第七章 CEO 的关键策略问题

第 8 章 附录

- 世界概况

- 概述

- 五力分析框架(产业吸引力分析)

- 全球价值链分析

- 市场动态(DRO)

- 资讯来源及延伸阅读

- 图片列表

- 关键见解

- 数据包

- 词彙表

简介目录

Product Code: 5000173

The Europe Polycarbonate (PC) Market size is estimated at 3.89 billion USD in 2024, and is expected to reach 5.15 billion USD by 2029, growing at a CAGR of 5.77% during the forecast period (2024-2029).

Upcoming construction projects to boost polycarbonate demand

- Polycarbonate (PC) is used in various applications, such as compact discs, bullet-proof glasses, car headlamp lenses, roofing, and glazing, due to its high impact strength, lightweight property, UV resistance, and optical transmission. In 2022, the European polycarbonate (PC) market accounted for 19% of the global polycarbonate (PC) market in terms of value.

- In 2020, due to the COVID-19 pandemic, the PC market declined by 10.41% in terms of value compared to 2019, attributed to supply chain disruptions, raw material shortages, and the halting of trade exchanges throughout the region. With the resumption of production facilities, the demand for PC resin increased by 19.22% in terms of value in 2021 compared to 2020.

- Automotive and building and construction are the region's largest consumers of PC resin. The region's new construction floor area is expected to reach 9.5 billion sq. ft in 2029 from 7.8 billion sq. ft in 2023. Vehicle production in the region is projected to reach 20.7 million units in 2029 from 18.3 million units in 2023. The region's increasing construction and vehicle production is projected to drive the demand for PC resin over the coming years.

- Aerospace is the region's fastest-growing end-user industry for PC resin, with a projected CAGR of 7.38% in terms of value during the forecast period. The rising trend of high-strength and lightweight materials in the aerospace industry is expected to drive the demand for PC resin in the region. The region's aircraft component production revenue is projected to reach USD 348.8 billion in 2029 from USD 243.2 billion in 2023. The growing production of aerospace components in the region is projected to drive the demand for PC resin.

Automotive production may boost the growth of polycarbonate across the region

- Europe accounted for 19% (by volume) of the global consumption of polycarbonate resin in 2022. Polycarbonate is used in European countries, such as France and Germany, in various industries, including automotive, aerospace, and electrical and electronics. Countries such as Germany, Russia, and Italy are the leading consumers of polycarbonate resin in the region.

- Germany is the largest consumer of polycarbonate in the region due to its growing aerospace, automotive, and electrical and electronics industries. Aircraft components and vehicle production held a share of around 16.9% by revenue and 20.19% by volume in 2021 at the regional level, driving the demand for polycarbonate resin. The growing automotive and electrical and electronics production is expected to drive the demand for polycarbonate resin.

- The demand for polycarbonate resin in Italy is increasing significantly due to growing production in the automotive and electrical and electronics industries. Italy is the European Union's fifth-largest vehicle producer. In 2022, the country produced 1.08 million units, 6.13% (by volume) of the region. The country's electrical and electronics industry is also expanding, and the revenue is projected to amount to USD 17.15 billion in 2023. These factors are expected to drive the demand for polycarbonate resins in Europe during the forecast period.

- The United Kingdom is expected to be the fastest-growing consumer of polycarbonate resin, with a CAGR of 6.19% by revenue during the forecast period (2023-2029). The growth in vehicle production, with the highest CAGR of 3.4% (in volume) in the region, is expected to drive the demand for PC resin in the country.

Europe Polycarbonate (PC) Market Trends

Technological innovations to boost the consumer electronics market

- Europe's electrical and electronics production registered a CAGR of over 3.8% between 2017 and 2021. The rapid pace of electronic technological innovation is driving consistent demand for newer and faster electrical and electronic products. As a result, it has also increased the demand for electrical and electronics production in the region.

- Despite the increased demand for computers and laptops due to remote working and distance learning, the average revenue per user in the European consumer electronics segment dropped by 6.3%. It generated a revenue of around USD 252.1 billion in 2020. As a result, in 2020, the electrical and electronic production in the region decreased by 2.8% by revenue compared to the previous year.

- In 2021, Europe's electrical and electronic equipment exports were around USD 228.37 billion, 12.4% higher compared to 2020. As a result, electrical and electronic production in the region increased and registered 11.6% in 2021 compared to the previous year.

- Robotics, virtual reality and augmented reality, IoT (Internet of Things), and 5G connectivity are expected to grow during the forecast period. As a result of technological advancements, demand for consumer electronics is expected to rise during the forecast period. The consumer electronics segment in the region is projected to reach a revenue of around USD 157.2 billion in 2027 from USD 121.1 billion in 2023. By 2027, Europe is projected to be the second-largest electrical and electronics production accounting for around 12.7% of the global market. As a result, the rise in consumer electronics is projected to increase the demand for electrical and electronics production in the coming years.

Europe Polycarbonate (PC) Industry Overview

The Europe Polycarbonate (PC) Market is fairly consolidated, with the top five companies occupying 100%. The major players in this market are Covestro AG, Mitsubishi Chemical Corporation, SABIC, SIBUR Holding PJSC and Trinseo (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Aerospace

- 4.1.2 Automotive

- 4.1.3 Building and Construction

- 4.1.4 Electrical and Electronics

- 4.1.5 Packaging

- 4.2 Import And Export Trends

- 4.2.1 Polycarbonate (PC) Trade

- 4.3 Price Trends

- 4.4 Form Trends

- 4.5 Recycling Overview

- 4.5.1 Polycarbonate (PC) Recycling Trends

- 4.6 Regulatory Framework

- 4.6.1 EU

- 4.6.2 France

- 4.6.3 Germany

- 4.6.4 Italy

- 4.6.5 Russia

- 4.6.6 United Kingdom

- 4.7 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Electrical and Electronics

- 5.1.5 Industrial and Machinery

- 5.1.6 Packaging

- 5.1.7 Other End-user Industries

- 5.2 Country

- 5.2.1 France

- 5.2.2 Germany

- 5.2.3 Italy

- 5.2.4 Russia

- 5.2.5 United Kingdom

- 5.2.6 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 CHIMEI

- 6.4.2 Covestro AG

- 6.4.3 Formosa Plastics Group

- 6.4.4 LG Chem

- 6.4.5 Lotte Chemical

- 6.4.6 Mitsubishi Chemical Corporation

- 6.4.7 SABIC

- 6.4.8 SIBUR Holding PJSC

- 6.4.9 Teijin Limited

- 6.4.10 Trinseo

7 KEY STRATEGIC QUESTIONS FOR ENGINEERING PLASTICS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms