|

市场调查报告书

商品编码

1693836

亚太地区聚碳酸酯(PC)-市场占有率分析、产业趋势与成长预测(2024-2029年)Asia-Pacific Polycarbonate (PC) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

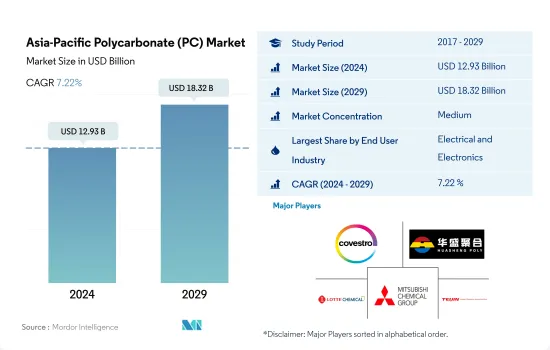

亚太聚碳酸酯 (PC) 市场规模预计在 2024 年为 129.3 亿美元,预计到 2029 年将达到 183.2 亿美元,预测期内(2024-2029 年)的复合年增长率为 7.22%。

电气电子产业保持优势

- 聚碳酸酯用途广泛且耐用,广泛应用于各行各业。应用包括冰箱、农业温室、工业和公共建筑、建筑幕墙、手术器械、药物输送系统、血液血液透析机膜、血液储存器、血液过滤器等。电气和电子产业是该地区聚碳酸酯的最大消费产业,2022 年将占据 45% 以上的市场占有率。

- 2017年至2019年,聚碳酸酯需求稳定成长,年成长率与前一年同期比较为5.14%和3.53%。这一成长主要得益于电子产业产量的增加。

- 2020年,新冠疫情限制了营运、旅行和贸易,导致聚碳酸酯需求与前一年同期比较减3.71%。受影响尤其严重的是汽车和工业机械产业,2019 年产量分别下降了 12.52% 和 16.65%。然而,随着限制的放宽,对聚碳酸酯的需求逐渐恢復,其中中国和印度在推动成长方面发挥了关键作用。

- 预计在预测期内,用聚碳酸酯替代传统丙烯酸和玻璃的趋势将日益增长,这将推动对这种材料的需求。在亚太地区所有终端用户产业中,印度电气和电子产业预计将经历最高成长,预测期内销量复合年增长率为 7.63%。总体而言,该地区对聚碳酸酯的需求预计在预测期内将达到 5.66% 的复合年增长率(数量)和 7.22% 的以金额为准。

中国保持数量和价值优势

- 亚太地区是全球最大的聚碳酸酯消费地区,到 2022 年将占据超过 63.07% 的市场。在亚太地区,聚碳酸酯在电气和电子、汽车、航太零件製造和医疗设备製造业有着广泛的应用。

- 2017年至2019年期间,聚碳酸酯的需求呈现稳定成长,主要得益于中国和印度等国家塑胶包装产业的蓬勃发展。 2020年,疫情期间的营运和贸易限制导致劳动力短缺、原材料短缺等各种限制因素严重影响了各个终端用户产业,从而对该地区对聚碳酸酯的需求产生了负面影响。尤其是澳洲的聚碳酸酯需求受到明显影响。 2020年全国需求年与前一年同期比较40.96%,与前一年同期比较地区较去年同期下降3.71%。

- 2021年,限制措施有所放鬆,聚碳酸酯需求恢復至疫情前的水准。这一增长的主要驱动力是印度等国家的工业活动的快速增长。预计这一成长趋势将在整个预测期内持续下去,其中印度对聚碳酸酯的需求增幅在所有国家中最高。总体而言,预测期内亚太地区对聚碳酸酯的需求预计将达到 5.60% 的复合年增长率(按数量计算)。

亚太地区聚碳酸酯(PC)市场趋势

东南亚国协快速成长推动电子产品生产

- 在亚太地区,电气和电子设备生产收入从 2020 年到 2021 年成长了 13.9%。电子产品部门占大多数亚洲国家出口总额的 20-50%。电视、收音机、电脑和行动电话等大多数的家用电子电器产品都是在东协地区生产。

- 东协是硬碟生产的领先者,超过 80% 的硬碟在该地区生产。整体而言,东协的电气和电子(E&E)产业比其他产业更依赖外国投入和技术,53%的电气和电子出口可归因于东协电气和电子出口中嵌入的外国增加价值(FVA)或外国投入。

- 泰国和马来西亚等国家是该地区电子产品生产的领导者。泰国拥有东南亚最大的电子组装基地之一,在硬碟、积体电路和半导体生产领域居领先地位。它是全球第二大空调製造商和全球第四大冰箱製造商。

- 电子产业极大地受益于东协的一体化生产网络,这有助于改善与中国和日本等亚洲经济强国的贸易。

- 2019-2020年,中国占全球电器出口的11.2%,数位产品出口成长5.8%。亚洲开发银行称,中国为该地区的电子产品提供了庞大的市场。泰国、日本、中国、马来西亚、印度和菲律宾等国家继续在该地区电子产品生产领域处于领先地位。

亚太地区聚碳酸酯(PC)产业概况

亚太地区聚碳酸酯(PC)市场适度整合,前五大公司占59.21%的市占率。市场的主要企业包括科思创股份公司、海南华盛新材料科技、乐天化学、三菱化学株式会社、帝人株式会社等。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章执行摘要和主要发现

第二章 报告要约

第三章 引言

- 研究假设和市场定义

- 研究范围

- 调查方法

第四章 产业主要趋势

- 最终用户趋势

- 航太

- 车

- 建筑与施工

- 电气和电子

- 包装

- 进出口趋势

- 聚碳酸酯(PC)贸易

- 价格趋势

- 形态趋势

- 回收概述

- 聚碳酸酯(PC)回收趋势

- 法律规范

- 澳洲

- 中国

- 印度

- 日本

- 马来西亚

- 韩国

- 价值炼和通路分析

第五章市场区隔

- 最终用户产业

- 航太

- 车

- 建筑与施工

- 电气和电子

- 工业/机械

- 包装

- 其他的

- 国家

- 澳洲

- 中国

- 印度

- 日本

- 马来西亚

- 韩国

- 其他亚太地区

第六章竞争格局

- 关键策略趋势

- 市场占有率分析

- 商业状况

- 公司简介

- CHIMEI

- Covestro AG

- Formosa Plastics Group

- Hainan Huasheng New Material Technology Co., Ltd.

- LG Chem

- Lotte Chemical

- Mitsubishi Chemical Corporation

- Sinochem

- Sinopec SABIC Tianjin Petrochemical Company(SSTPC)

- Teijin Limited

第七章:CEO面临的关键策略问题

第 8 章 附录

- 世界概况

- 概述

- 五力分析框架(产业吸引力分析)

- 全球价值链分析

- 市场动态(DRO)

- 资讯来源及延伸阅读

- 图片列表

- 关键见解

- 数据包

- 词彙表

简介目录

Product Code: 5000174

The Asia-Pacific Polycarbonate (PC) Market size is estimated at 12.93 billion USD in 2024, and is expected to reach 18.32 billion USD by 2029, growing at a CAGR of 7.22% during the forecast period (2024-2029).

Electrical and electronics industry to maintain its dominance

- Polycarbonates are widely utilized in various industries due to their versatile and durable nature. They find applications in refrigerators, agricultural houses, industrial and public buildings, facades, surgical instruments, drug delivery systems, hemodialysis membranes, blood reservoirs, and blood filters. The electrical and electronics industry has been the largest consumer of polycarbonate in the region, and it accounted for over 45% of the market share in 2022.

- Between 2017 and 2019, polycarbonate demand experienced steady growth, with Y-o-Y rates of 5.14% and 3.53%, respectively. The increasing production in the electronics industry primarily drove this growth.

- In 2020, the COVID-19 pandemic led to operational, travel, and trade restrictions, resulting in a decline in the demand for polycarbonates by 3.71% compared to the previous year. The automotive and industrial machinery industries were particularly affected, experiencing declines of 12.52% and 16.65% in their 2019 volumes, respectively. However, as the restrictions eased, the demand for polycarbonates gradually recovered, with China and India playing a significant role in driving the growth.

- The growing trend of substituting traditional acrylics and glass with polycarbonates is expected to drive the demand for the material in the forecast period. Among all end-user industries in the Asia-Pacific region, the electrical and electronics industry in India is projected to witness the highest growth, with a CAGR of 7.63% in terms of volume during the forecast period. Overall, the regional demand for polycarbonates is expected to record a CAGR of 5.66% in volume terms and 7.22% in value terms throughout the forecast period.

China to maintain its dominance both in terms of volume and value

- The Asia-Pacific region is the largest consumer of polycarbonates globally, occupying a share of over 63.07% in 2022. In the Asia-Pacific region, polycarbonates find various applications in the electrical and electronics, automotive, aerospace components manufacturing, and healthcare devices manufacturing industries.

- During 2017-2019, the demand for polycarbonates witnessed steady growth, mainly driven by the rapid growth in the plastic packaging industry in countries like China and India. In 2020, various restraining factors, like worker unavailability and raw material shortages caused by operational and trade restrictions during the pandemic, severely affected various end-user industries, thereby negatively affecting the polycarbonate demand in the region. Among all countries, the polycarbonate demand in Australia was affected severely. In 2020, the country's Y-o-Y demand volume declined by 40.96%, whereas the regional Y-o-Y decline was 3.71%.

- In 2021, as the restrictions eased, the polycarbonate demand rose back to its pre-pandemic level. This growth was majorly driven by the rapid growth in industrial activities in countries like India. This growth trend is expected to continue throughout the forecast period, with India witnessing the highest growth in polycarbonate demand among all countries. Overall, the polycarbonate demand in the Asia-Pacific region is expected to record a CAGR of 5.60% (in volume) during the forecast period.

Asia-Pacific Polycarbonate (PC) Market Trends

Rapid growth in ASEAN countries to foster electronics production

- The Asia-Pacific region saw an increase in electrical and electronics production revenue by 13.9% from 2020 to 2021. The electronics sector accounts for 20-50% of the total value of most Asian countries' exports. Consumer electronics such as televisions, radios, computers, and cellular phones are largely manufactured in the ASEAN region.

- ASEAN leads the production of hard drives, with over 80% of hard drives being manufactured in the region. Overall, the electrical and electronics (E&E) industry in ASEAN relies more on foreign inputs and technology than other industries, with 53% of E&E exports arising from foreign value added (FVA) or foreign inputs integrated into ASEAN's E&E exports.

- Countries like Thailand and Malaysia lead in the production of electronics in the region. Thailand, home to one of the largest electronics assembly bases in Southeast Asia, leads in the production of hard drives, integrated circuits, and semiconductors. It ranks second in manufacturing air conditioning units and fourth in the global refrigerators market.

- The electronics industry has greatly benefitted from ASEAN's integrated production networks, which foster improved trade with larger Asian economies like China and Japan.

- China held an 11.2% share of global exports in electrical products and registered a growth of 5.8% in the export of digital products from 2019 to 2020. According to the Asian Development Bank, China provides a large market for electronics in the region. Countries such as Thailand, Japan, China, Malaysia, India, and the Philippines continue to lead the region in the production of electronics.

Asia-Pacific Polycarbonate (PC) Industry Overview

The Asia-Pacific Polycarbonate (PC) Market is moderately consolidated, with the top five companies occupying 59.21%. The major players in this market are Covestro AG, Hainan Huasheng New Material Technology Co., Ltd., Lotte Chemical, Mitsubishi Chemical Corporation and Teijin Limited (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Aerospace

- 4.1.2 Automotive

- 4.1.3 Building and Construction

- 4.1.4 Electrical and Electronics

- 4.1.5 Packaging

- 4.2 Import And Export Trends

- 4.2.1 Polycarbonate (PC) Trade

- 4.3 Price Trends

- 4.4 Form Trends

- 4.5 Recycling Overview

- 4.5.1 Polycarbonate (PC) Recycling Trends

- 4.6 Regulatory Framework

- 4.6.1 Australia

- 4.6.2 China

- 4.6.3 India

- 4.6.4 Japan

- 4.6.5 Malaysia

- 4.6.6 South Korea

- 4.7 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Electrical and Electronics

- 5.1.5 Industrial and Machinery

- 5.1.6 Packaging

- 5.1.7 Other End-user Industries

- 5.2 Country

- 5.2.1 Australia

- 5.2.2 China

- 5.2.3 India

- 5.2.4 Japan

- 5.2.5 Malaysia

- 5.2.6 South Korea

- 5.2.7 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 CHIMEI

- 6.4.2 Covestro AG

- 6.4.3 Formosa Plastics Group

- 6.4.4 Hainan Huasheng New Material Technology Co., Ltd.

- 6.4.5 LG Chem

- 6.4.6 Lotte Chemical

- 6.4.7 Mitsubishi Chemical Corporation

- 6.4.8 Sinochem

- 6.4.9 Sinopec SABIC Tianjin Petrochemical Company (SSTPC)

- 6.4.10 Teijin Limited

7 KEY STRATEGIC QUESTIONS FOR ENGINEERING PLASTICS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms