|

市场调查报告书

商品编码

1836652

行动装置使用者身分验证服务:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)Mobile Devices User Authentication Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

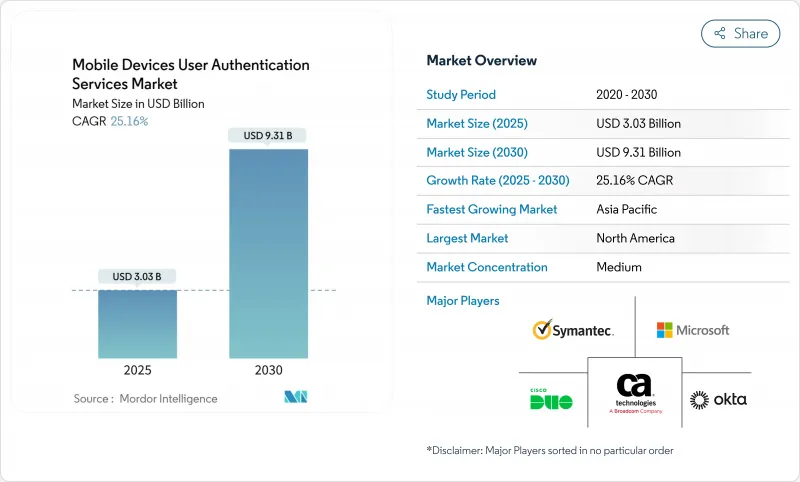

行动装置用户身份验证服务市场预计在 2025 年达到 30.3 亿美元,在 2030 年达到 93.1 亿美元,复合年增长率为 25.16%。

结构性需求正在从密码转向防网钓鱼身份验证,预计到 2024 年密钥采用率将激增 550%,而 2025 年至 2030 年期间无密码平台的复合年增长率将达到 26%。从欧洲的强客户身份验证 (SCA) 法规到美国国防部的零信任蓝图,监管审查力度不断加强,正在推动多因素采用以满足区域合规性需求,同时也提高了供应商的绩效标准。生态系统整合是竞争策略的核心。平台领导者正在推动广泛的身分结构,而专家则在硬体金钥、行为分析和营运商 API 中抓住成长点。在此背景下,企业意识到无密码身份验证的经济效益,JumpCloud 报告称,设备级生物辨识技术可降低凭证管理开销和违规成本。

全球行动装置用户身份验证服务市场趋势与洞察

行动优先企业采用无密码和 WebAuthn 标准

70% 的企业计划或已实施无密码身份验证,这反映了 WebAuthn 如何改变安全基准。 Microsoft Entra ID 等现有平台的原生支援将金钥功能直接嵌入装置硬件,简化了使用者流程,同时消除了共用机密的风险。随着银行、航空公司和旅游入口网站在 2025 年采用符合 FIDO 标准的流程,无密码身份验证的势头可能会进一步增强,这证实了无密码身份验证将成为高价值行动交易的常态。能够协调跨平台凭证移动性的供应商将在行动装置用户身份验证服务市场中占据相当大的份额。

金融科技和行动银行(SCA 合规性)的激增将推动 MFA 的部署

欧洲银行管理局 (EBSA) 的指导意见将设备解锁生物识别排除在独立的安全认证 (SCA) 之外,这加速了多因素身份验证的采用,迫使发卡机构建立结合生物识别、持有因素和动态风险检查的生物识别身份验证。预期的 PSD3提案将进一步禁止仅限行动装置的流程,迫使银行整合带频宽验证功能。电子商务、叫车和零工平台正在采用银行级控制措施,以满足消费者信任并维护监管公平性。这种需求的整合正在推动整个金融和准金融生态系统中行动装置用户身份验证服务市场实现两位数成长。

营运商分散地区的简讯 OTP 延迟和失败

全球简讯动态密码支出超过 16 亿美元,但在多营运商市场中,一次性密码的送达率低于企业门槛,导致购物车放弃和登入尝试失败。新加坡、印度和美国的监管机构已设定目标,到 2025 年逐步淘汰简讯一次性密码,这推动了对替代方案的需求。 NIST 目前不鼓励将简讯作为安全元素,而 Coinbase 等大型交易所已确认,95% 的帐户接管都利用了 SIM 卡交换攻击。虽然迁移成本可能会暂时阻碍中小企业,但推播通知和金钥成本的下降将随着时间的推移消除这一障碍。

报告中分析的其他驱动因素和限制因素

- 亚洲中阶智慧型手机生物辨识硬体采用情况

- 企业零信任安全架构加速行动身分验证功能的采用

- GDPR下的生物特征资料隐私问题

細項分析

到 2024 年,MFA 将占总收入的 56%,这反映了对凭证盗窃的早期保护。在平台级 FIDO 支援和金钥的广泛采用的推动下,无密码身份验证正以 26% 的复合年增长率加速成长。预计到 2030 年,无密码流程中行动装置用户身份验证服务的市场规模将达到 38 亿美元,几乎是 2025 年的两倍。虽然硬体安全金钥属于小众市场,但它满足了电讯和国防领域的高保证需求,随着单位经济效益的提高,正以两位数的成长率扩张。行为和被动身份验证增加了持续检验,减少了使用者提示并满足了零信任要求。将硬体金钥与隐形行为层结合的供应商完全有能力获得企业的提升销售预算。

虽然指纹辨识、脸部辨识和语音配对占据了生物辨识应用的大多数,但当以行为为中心的模型融入现有的行动 SDK 中时,其成长速度将会更快。号码匹配和设备信誉分析可以减少 MFA 疲劳,并关闭攻击者操纵的漏洞路径。这些趋势的结合,将行动装置使用者身分验证服务市场定位为无缝数位体验的推动者,而非查核点,从而增强了董事会层面投资的商业价值。

受快速 SaaS 部署和弹性扩展优势的推动,云端身分验证即服务 (CAS) 收入将在 2024 年成长 60%。随着受监管产业在保护资料驻留的同时利用云端身分创新,边缘和云端混合选项将以 23% 的复合年增长率成长。部署 Microsoft 混合 Kerberos 信任模型的组织在透过本机目录和云端点验证本机 Windows Hello 凭证时,展现出更低的延迟和更高的策略一致性。预计到 2030 年,本地架构的行动装置用户身份验证服务的市场份额将降至 15% 以下,但只要主权资料授权仍然严格,这一比例将保持不变。

混合云的采用遵循迁移浪潮:企业首先迁移简单的 Web 工作负载,然后再迁移到云端原生 FIDO仲介。这种渐进式迁移可以为整合商维持多年的业务收益,并延长平均合约期限。提供跨信任平面策略主导编配的供应商可以建立更牢固的关係,同时最大限度地降低客户淘汰和替换的风险。

区域分析

受美国网路安全和基础设施安全局(CSA)支持持续检验的零信任成熟度模型等监管催化剂的推动,北美将在2024年贡献该行业38%的收益。半数美国公司已经实施了某种形式的无密码身份验证,这为后进企业加速采用该技术奠定了参考基础。供应商实力雄厚,微软、Okta和Yubico制定了标准,利基市场参与者则在行为分析领域开拓创新。公共部门合同,例如国防部的2027财年指令,提供了长期的采购量可视性,并促进了邻近民用机构的溢出采购。因此,随着零信任计画的扩展,行动装置用户身份验证服务市场竞争激烈且可扩展。

亚洲是成长最快的地区,受智慧型手机普及和政府数位身分识别计画的推动,到2030年,复合年增长率将达到28.7%。中国原始设备製造商整合先进的生物识别感测器,加上印度与Aadhaar关联的支付生态系统,将产生巨大的身份验证吞吐量。儘管资料隐私立法尚不成熟,但东协五国市场正凭藉电子政府和数位银行的部署蓬勃发展。基于通讯业者的SIM卡身份验证API填补了频宽受限地区的基础设施空白,扩大了行动装置用户身份验证服务市场的潜在需求,同时将通讯业者集团更深层地整合到价值链中。

在欧洲,严格的GDPR合规性和SCA的快速应用并进。欧洲银行业监管机构对数位钱包的澄清将提高商业交易的多因素要求,为其他垂直行业树立榜样。预期的PSD3规则将禁止仅限行动装置的流程,从而有利于拥有能够动态提升因素的编配引擎的供应商。由于新兴的数位身分认证方案,北欧国家的采用率将最高,而随着开放银行和电子身分认证框架的成熟,英国、德国和法国将实现强劲成长。即将基于欧盟数位身分钱包的跨境协调将开发新的用例,使欧洲继续成为行动装置用户身份验证服务市场中利润丰厚但合规性至关重要的细分市场。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 调查结果

- 调查前提

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场状况

- 市场概况

- 市场驱动因素

- 行动优先企业采用无密码和 WebAuthn 标准

- 金融科技和行动银行(SCA 合规性)的激增推动了 MFA 的推出

- 亚洲中阶智慧型手机生物辨识硬体采用情况

- 新兴市场中运营商支援的基于 SIM 卡的身份验证 API

- 全球监管规定(PSD2、CCPA、HIPAA)推动身分验证支出

- 企业零信任安全架构加速行动验证器的采用

- 市场限制

- 营运商分散地区的简讯 OTP 延迟和失败

- GDPR下的生物特征资料隐私问题

- 传统 SMB 行动应用程式的整合成本高

- 专有行动身分验证 SDK 之间的互通性差距

- 价值/供应链分析

- 技术展望

- 投资分析

- 五力分析

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争强度

第五章市场规模及成长预测(金额)

- 按身份验证类型

- 密码和密码

- 双因素认证

- 多因素身份验证

- 生物特征认证

- 行为和被动身份验证

- 基于风险/情境的身份验证

- 软令牌和身份验证器应用程式

- 硬体安全金钥/FIDO 令牌

- 依部署方式

- 云端基础的即服务身份验证

- 本地部署

- 混合(边缘+云)

- 透过认证管道

- SMS OTP

- 推播通知

- 应用内生物辨识 API

- SIM/静默行动网路验证

- 电子邮件 OTP/魔术链接

- 按公司规模

- 中小型企业(员工人数少于1,000人)

- 大公司

- 按行业

- BFSI

- 消费性电子产品与电子商务

- 政府及公共机构

- IT和通讯服务

- 医疗保健和生命科学

- 製造业和工业物联网

- 教育和数位学习

- 旅游与饭店

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美

- 欧洲

- 北欧的

- 瑞典

- 挪威

- 芬兰

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 其他欧洲国家

- APAC

- 中国

- 印度

- 日本

- 韩国

- ASEAN-5

- 澳洲

- 纽西兰

- 亚太地区其他国家

- 中东

- GCC

- 沙乌地阿拉伯

- UAE

- 土耳其

- 以色列

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 肯亚

- 其他非洲国家

- 北美洲

第六章 竞争态势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Symantec Corporation

- Broadcom Inc.(CA Technologies)

- Cisco Systems Inc.(Duo Security)

- Microsoft Corporation

- Okta Inc.

- Thales Group(Gemalto)

- RSA Security LLC(Dell Technologies)

- OneSpan Inc.

- Entrust Corporation

- HID Global Corporation

- IDEMIA

- NEC Corporation

- Ping Identity Holding Corp.

- ForgeRock Inc.

- Authy(Twilio Inc.)

- Yubico AB

- Trustwave Holdings Inc.

- Micro Focus International plc

- Google LLC

- IBM Corporation

- Nexus Group

- SecurEnvoy Ltd.

- Aware Inc.

- Fujitsu Limited

第七章 市场机会与未来展望

The mobile devices user authentication services market size is valued at USD 3.03 billion in 2025 and is on track to reach USD 9.31 billion by 2030, and is forecast to expand at a 25.16% CAGR.

Structural demand is shifting from passwords toward phishing-resistant verification, reflected in the 550% jump in passkey roll-outs during 2024 and the 26% CAGR expected for passwordless platforms between 2025-2030. Heightened regulatory scrutiny-ranging from Europe's Strong Customer Authentication (SCA) rules to the U.S. Department of Defense Zero Trust Roadmap-is catalyzing multi-factor deployments that satisfy regional compliance needs while raising the performance bar for vendors. Competitive strategies now center on ecosystem integration: platform leaders push broad identity fabrics while specialists capture growth pockets in hardware keys, behavioral analytics, and carrier APIs. Against this backdrop, enterprises recognise the economic upside of passwordless authentication, with JumpCloud reporting that device-level biometrics reduce credential management overhead and breach costs in equal measure.

Global Mobile Devices User Authentication Services Market Trends and Insights

Adoption of Passwordless & WebAuthn Standards Across Mobile-First Enterprises

Seventy percent of organisations either plan to adopt or have already introduced passwordless authentication, illustrating how WebAuthn shifts the security baseline. Native support from platform incumbents such as Microsoft Entra ID embeds passkey functionality directly into device hardware, eradicating shared-secret risk while simplifying user journeys. Consumer familiarity with passkeys rose to 57% in 2025, up from 39% three years earlier, signalling readiness for large-scale transition.Momentum will intensify as banks, airlines and travel portals adopt FIDO-compliant flows in 2025, confirming passwordless as a mainstream control for high-value mobile transactions. Vendors able to orchestrate cross-platform credential mobility stand to win disproportionate share in the mobile devices user authentication services market.

Surge in FinTech and Mobile Banking (SCA Compliance) Driving MFA Roll-outs

European Banking Authority guidance ruling out device-unlock biometrics as a standalone SCA accelerates multi-factor adoption, forcing issuers to build layered verification that combines biometrics, possession factors, and dynamic risk checks. The expected PSD3 proposal will further prohibit mobile-only flows, prompting banks to embed out-of-band authenticators. Spillover into adjacent digital commerce is material; e-commerce, ride-hailing, and gig-work platforms adopt banking-grade controls to satisfy consumer trust and regulatory parity. These converging demands underpin double-digit growth in the mobile devices user authentication services market across financial and quasi-financial ecosystems.

SMS OTP Latency & Failure in Carrier-Fragmented Regions

Global spend on SMS OTP exceeds USD 1.6 billion even though delivery rates fall below enterprise thresholds in multi-operator markets, triggering cart abandonment and failed logins. Regulators in Singapore, India and the United States aim to retire SMS OTP by 2025, amplifying urgency for alternatives. NIST now discourages SMS as a secure factor, while leading exchanges such as Coinbase confirm that 95% of account takeovers leveraged SIM-swap attacks. Transition costs may temporarily restrain small businesses, but declining push notification and passkey expenses neutralise the barrier over time.

Other drivers and restraints analyzed in the detailed report include:

- Mid-Range Smartphone Biometric Hardware Penetration in Asia

- Enterprise Zero-Trust Security Architecture Accelerating Mobile Authenticator Adoption

- Biometric Data Privacy Concerns under GDPR

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

MFA dominated revenue with 56% in 2024, reflecting early defences against credential theft. Passwordless now sets the growth pace at 26% CAGR, powered by platform-level FIDO support and rising passkey familiarity. The mobile devices user authentication services market size for passwordless flows is projected to reach USD 3.8 billion by 2030, nearly doubling its 2025 base. Hardware security keys, while niche, address high-assurance needs in telecom and defence, expanding at double-digit rates as unit economics improve. Behavioural and passive authentication add continuous verification, reducing user prompts and aligning with zero-trust mandates. Vendors marrying hardware keys with invisible behavioural layers are well-positioned to capture enterprise up-sell budgets.

Fingerprints, facial recognition, and voice match account for the bulk of biometric adoption, yet behaviour-centric models grow faster by embedding in existing mobile SDKs. Number matching and device reputation analytics reduce MFA fatigue, closing an exploit path that attackers manipulate. The combination of these trends repositions the mobile devices user authentication services market as an enabler of seamless digital experience rather than a checkpoint, strengthening the business case for board-level investment

Cloud Authentication-as-a-Service delivered 60% revenue in 2024, driven by rapid SaaS roll-outs and elastic scaling advantages. The hybrid edge-plus-cloud option grows at 23% CAGR as regulated industries safeguard data residency while using cloud identity innovation. Organisations deploying Microsoft's hybrid Kerberos trust model demonstrate latency reductions and policy coherence when authenticating local Windows Hello credentials through both on-premises directory and cloud endpoint. The mobile devices user authentication services market share for on-premise architectures will slide below 15% by 2030, yet it persists wherever sovereign data mandates remain strict.

Hybrid adoption follows migration waves: firms lift simple web workloads first, then layer cloud-native FIDO brokers, leaving heritage mainframe authentications on-site until retirement. This staged transition sustains multi-year service revenue for integrators and lengthens average contract duration. Vendors offering policy-driven orchestration across trust planes achieve stickier relationships while minimising rip-and-replace risk for clients.

The Mobile Devices User Authentication Market is Segmented by Authentication Type (Passwords and PINs, Two-Factor Authentication, and More), Deployment Mode (Cloud-Based, On-Premise, and More), Authentication Channel (SMS OTP, Push Notification, and More), Enterprise Size (SMEs, Large Enterprises), End-User Vertical (BFSI, Consumer Electronics, and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 38% of 2024 sectoral revenue, anchored by regulatory catalysts like the Cybersecurity and Infrastructure Security Agency Zero Trust Maturity Model that champions continuous verification. Half of U.S. enterprises have already deployed some form of passwordless authentication, creating a reference base that accelerates late-mover adoption. Vendor presence is dense, with Microsoft, Okta, and Yubico shaping standards while niche players pioneer behaviour analytics. Public-sector contracts, notably the Department of Defense FY27 mandate, provide long-term volume visibility and drive spill-over purchases in adjacent civilian agencies. The mobile devices user authentication services market, therefore, remains highly competitive yet expandable as zero-trust programmes scale.

Asia is the fastest-growing theatre at 28.7% CAGR through 2030, propelled by smartphone ubiquity and government digital identity schemes. Chinese OEM integration of advanced biometric sensors combined with India's Aadhaar-linked payments ecosystem creates massive authentication throughput. ASEAN-5 markets add incremental momentum via e-government and digital banking roll-outs, even though data privacy legislation is still maturing, injecting both growth and complexity. Carrier-backed SIM authentication APIs fill infrastructure gaps in low-bandwidth geographies, enlarging the addressable demand for the mobile devices user authentication services market while embedding telecom groups deeper into the value chain.

Europe balances strict GDPR compliance with rapid SCA uptake. The European Banking Authority's clarification on digital wallets elevates multi-factor requirements across commerce and sets a playbook that other verticals can emulate. Anticipated PSD3 rules will forbid mobile-only flows, favouring vendors with orchestration engines capable of dynamic factor step-ups. Northern Europe demonstrates highest penetration due to early digital identity schemes, while the United Kingdom, Germany and France post robust growth as Open Banking and eID frameworks mature. Cross-border harmonisation under the forthcoming EU Digital Identity Wallet will unlock new use cases, maintaining Europe as a lucrative yet compliance-heavy segment of the mobile devices user authentication services market.

- Symantec Corporation

- Broadcom Inc. (CA Technologies)

- Cisco Systems Inc. (Duo Security)

- Microsoft Corporation

- Okta Inc.

- Thales Group (Gemalto)

- RSA Security LLC (Dell Technologies)

- OneSpan Inc.

- Entrust Corporation

- HID Global Corporation

- IDEMIA

- NEC Corporation

- Ping Identity Holding Corp.

- ForgeRock Inc.

- Authy (Twilio Inc.)

- Yubico AB

- Trustwave Holdings Inc.

- Micro Focus International plc

- Google LLC

- IBM Corporation

- Nexus Group

- SecurEnvoy Ltd.

- Aware Inc.

- Fujitsu Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Adoption of Passwordless and WebAuthn Standards Across Mobile-First Enterprises

- 4.2.2 Surge in FinTech and Mobile Banking (SCA Compliance) Driving MFA Roll-outs

- 4.2.3 Mid-Range Smartphone Biometric Hardware Penetration in Asia

- 4.2.4 Carrier-Backed SIM-Based Authentication APIs in Emerging Markets

- 4.2.5 Global Regulatory Mandates (PSD2, CCPA, HIPAA) Boosting Authentication Spend

- 4.2.6 Enterprise Zero-Trust Security Architecture Accelerating Mobile Authenticator Adoption

- 4.3 Market Restraints

- 4.3.1 SMS OTP Latency and Failure in Carrier-Fragmented Regions

- 4.3.2 Biometric Data Privacy Concerns under GDPR

- 4.3.3 High Integration Cost for Legacy SME Mobile Applications

- 4.3.4 Interoperability Gaps among Proprietary Mobile Auth SDKs

- 4.4 Value / Supply-Chain Analysis

- 4.5 Technological Outlook

- 4.6 Investment Analysis

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Authentication Type

- 5.1.1 Passwords and PINs

- 5.1.2 Two-Factor Authentication

- 5.1.3 Multi-Factor Authentication

- 5.1.4 Biometric Authentication

- 5.1.5 Behavioral and Passive Authentication

- 5.1.6 Risk-Based / Contextual Authentication

- 5.1.7 Soft Tokens and Authenticator Apps

- 5.1.8 Hardware Security Keys / FIDO Tokens

- 5.2 By Deployment Mode

- 5.2.1 Cloud-Based Authentication as-a-Service

- 5.2.2 On-Premise

- 5.2.3 Hybrid (Edge + Cloud)

- 5.3 By Authentication Channel

- 5.3.1 SMS OTP

- 5.3.2 Push Notification

- 5.3.3 In-App Biometric API

- 5.3.4 SIM / Silent Mobile Network Authentication

- 5.3.5 Email OTP / Magic Link

- 5.4 By Enterprise Size

- 5.4.1 SMEs (< 1,000 Employees)

- 5.4.2 Large Enterprises

- 5.5 By End-user Vertical

- 5.5.1 BFSI

- 5.5.2 Consumer Electronics and E-Commerce

- 5.5.3 Government and Public Sector

- 5.5.4 Telecommunications and IT Services

- 5.5.5 Healthcare and Life Sciences

- 5.5.6 Manufacturing and Industrial IoT

- 5.5.7 Education and eLearning

- 5.5.8 Travel and Hospitality

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Nordics

- 5.6.3.1.1 Sweden

- 5.6.3.1.2 Norway

- 5.6.3.1.3 Finland

- 5.6.3.2 Germany

- 5.6.3.3 United Kingdom

- 5.6.3.4 France

- 5.6.3.5 Italy

- 5.6.3.6 Spain

- 5.6.3.7 Rest of Europe

- 5.6.4 APAC

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 ASEAN-5

- 5.6.4.6 Australia

- 5.6.4.7 New Zealand

- 5.6.4.8 Rest of APAC

- 5.6.5 Middle East

- 5.6.5.1 GCC

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 UAE

- 5.6.5.2 Turkey

- 5.6.5.3 Israel

- 5.6.5.4 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Kenya

- 5.6.6.4 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, Recent Developments)}

- 6.4.1 Symantec Corporation

- 6.4.2 Broadcom Inc. (CA Technologies)

- 6.4.3 Cisco Systems Inc. (Duo Security)

- 6.4.4 Microsoft Corporation

- 6.4.5 Okta Inc.

- 6.4.6 Thales Group (Gemalto)

- 6.4.7 RSA Security LLC (Dell Technologies)

- 6.4.8 OneSpan Inc.

- 6.4.9 Entrust Corporation

- 6.4.10 HID Global Corporation

- 6.4.11 IDEMIA

- 6.4.12 NEC Corporation

- 6.4.13 Ping Identity Holding Corp.

- 6.4.14 ForgeRock Inc.

- 6.4.15 Authy (Twilio Inc.)

- 6.4.16 Yubico AB

- 6.4.17 Trustwave Holdings Inc.

- 6.4.18 Micro Focus International plc

- 6.4.19 Google LLC

- 6.4.20 IBM Corporation

- 6.4.21 Nexus Group

- 6.4.22 SecurEnvoy Ltd.

- 6.4.23 Aware Inc.

- 6.4.24 Fujitsu Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

行动用户身份验证市场:按身份验证技术、部署模式、最终用户和身份验证因素划分 - 全球预测(2025-2032 年)

行动用户身份验证市场:按身份验证技术、部署模式、最终用户和身份验证因素划分 - 全球预测(2025-2032 年) 2025年全球用户身份验证解决方案市场报告

2025年全球用户身份验证解决方案市场报告 全球行动用户身分验证市场研究报告-产业分析、规模、份额、成长、趋势及2025年至2033年预测2025年行动用户身份验证全球市场报告

全球行动用户身分验证市场研究报告-产业分析、规模、份额、成长、趋势及2025年至2033年预测2025年行动用户身份验证全球市场报告 行动用户身份验证市场规模、份额和成长分析(按用户类型、垂直行业和地区)- 行业预测,2025-2032 年

行动用户身份验证市场规模、份额和成长分析(按用户类型、垂直行业和地区)- 行业预测,2025-2032 年 行动用户身份验证市场 - 全球行业规模、份额、趋势、机会和预测,按身份验证方法、部署模式、组织规模、地区和竞争细分,2019-2029F

行动用户身份验证市场 - 全球行业规模、份额、趋势、机会和预测,按身份验证方法、部署模式、组织规模、地区和竞争细分,2019-2029F