|

市场调查报告书

商品编码

1844442

微电网:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030)Microgrid - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

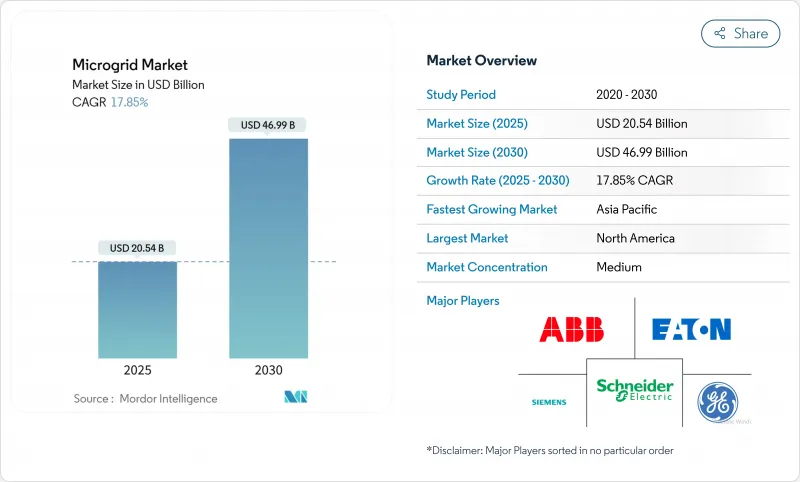

微电网市场规模预计在 2025 年为 205.4 亿美元,预计到 2030 年将达到 469.9 亿美元,预测期内(2025-2030 年)的复合年增长率为 17.85%。

成长将由IT/OT融合驱动,这种融合将边缘分析、数位双胞胎和网路安全层嵌入到先进的控制器中,从而实现跨硬体丛集的即时优化。由世界银行「300计画」主导的大规模农村电气化计画旨在2030年覆盖3亿非洲人口,这正在推动离网需求。在商业和工业领域,对不间断电源的需求以及国防资助的净零排放项目正在加速混合微电网的配置。同时,太阳能和电池成本的下降正在创造新的价值流,但锂离子电池价格的波动和互联线路的碎片化正在短期内缩短计划进度。

全球微电网市场趋势与洞察

加速非洲和南亚农村电气化

优惠资金筹措、硬体价格下降以及简化的采购流程将推动农村微电网普及率在 2024 年达到历史新高。刚果民主共和国于 2024 年 10 月核准了非洲最大的太阳能微电网计画。该计划耗资 5,030 万美元,由多边投资担保机构支持,将服务 28,000 户家庭和中小企业。根据《2024 年全球微电网市场状况》报告,撒哈拉以南非洲地区目前有 5,000 多个微电网运作,是 2020 年的三倍,其中太阳能光电占已装机发电量的 59%。在孟加拉国,2024 年为一个偏远村庄设计的太阳能-风能-电池微电网案例研究显示,其平准化成本为 0.0688 美元/千瓦时,低于区域电网扩展基准,证明了纯可再生能源设计的经济可行性。一些政府已经采用了基于绩效的融资窗口,在客户接入后提供补贴,从而降低了私人开发商的前期损失风险,并加速了预计将于 2025 年实现的部署流程。这些发展正在扩大近期需求池,并支持微电网市场预期的复合年增长率不断提高。

IT/OT融合推动北美先进微电网控制器的发展

先进的控制器如今整合了SCADA数据、云端分析和AI主导的网路安全,使资产能够在不断变化的市场讯号下进行自我优化。西门子和微软于2025年3月扩大了合作伙伴关係,将PLC数据与基于Azure的模型融合,以减少微电网营运商的计画外停机时间。数位双胞胎能够即时模拟运作状况,加速故障侦测和发电/输电决策。白宫能源现代化网路安全计画预测,分散式能源资源将从2024年的90吉瓦成长到2025年的380吉瓦,这将推动对安全OT通讯协定的需求。 AI异常侦测框架的准确率达到了96.5%,显着缩短了对网路威胁的回应时间。这些能力将增强公用事业和军事用户的信任,并增强微电网市场的成长前景。

互联互通代码分散阻碍市场成长

美国独立系统运营商的计划排队时间超过五年。旧金山的瓦伦西亚花园电池储能计划因意外的互联成本而被放弃,凸显了监管风险。美国能源部正在敦促公共产业开发自下而上的负载模型,以缓解瓶颈问题。欧洲开发商也指出,各成员国的标准有差异,增加了工程成本。缺乏协调会打击投资者的积极性,减缓公用事业采购週期,并在中期内限制微电网市场的扩张。

細項分析

到2024年,併网计划将占微电网市场份额的62%,全球微电网市场规模将达到107亿美元。微电网因其电价套利机会和停电期间的孤岛效应而极具吸引力。预计到2030年,微电网的复合年增长率将达到19%。双模架构现已整合同步器数据,使系统能够在200毫秒内切换,即使在野火和暴风雨期间也能保持电能品质标准。离网微电网虽然规模较小,但正在支持非洲和南亚的农村电气化。世界银行支持的计画已证明,混合太阳能储能係统能够以具有竞争力的电价满足全天候需求,从而扩大了离网EPC合约的可用性,并增强了微电网市场的深度。

离网部署吸引了来自气候变迁基金的优惠融资,从而允许更长的投资回报期和补贴费率方案。开发商可以利用标准化的货柜设计来最大限度地减少现场施工天数并提高融资可行性。社区所有模式还能提高收益并促进当地经济发展。随着通讯塔和采矿作业寻求绿能,自给自足的微电网将拓宽微电网产业的应用范围,使其超越纯电气化。在预测期内,连接选择将取决于收费系统、停电统计数据和政策奖励,但预计混合投资组合将主导投资者的投资方向。

到2024年,硬体市场将达到109亿美元,占微电网市场规模的63%。控制器、逆变器和电池架构成了硬体的实体核心。即使在北欧试点计画中可再生能源渗透率超过90%的情况下,电网整形逆变器也能维持系统稳定。随着供应商测试混合电池组并整合超级电容以加快启动速度,储存创新正在加速。虽然软体传统上仅占预算的15%,但在数位双胞胎和市场进入演算法的推动下,其复合年增长率高达22%。这些平台可以延长资产寿命、减少调度错误、释放配套服务收益,并增加微电网市场总收益。

服务提供者涵盖场地评估、授权、EPC 和营运。复杂性的增加,尤其是在多供应商环境中,推动了对专业整合商的需求,以确保系统级网路安全和服务级协定。咨询服务正在扩展到效能保证,利用机器学习模型来预测劣化率。随着客户优先考虑基于结果的合同,微电网即服务将硬体、软体和营运捆绑到单一订阅费用中,降低了小型商业客户的进入门槛。

微电网市场报告按连接性(併网和离网)、产品(硬体、软体、服务)、电源(太阳能光伏、热电联产、燃料电池、其他)、类型(交流微电网、直流微电网、其他)、额定功率(小于 1 MW、1-5 MW、其他)、最终用户(公共产业、商业/工业、住宅细分)和其他地区(北美地区进行细分)。

区域分析

北美占2024年销售额的38%,得益于美国能源部电网弹性和创新伙伴关係计画提供的105亿美元资金支持。美国国防部拨款5.48亿美元用于增强基础能源供给能力,重点在于采购混合微电网。网路安全仍然是该地区的重点,其基于人工智慧的多层框架在威胁侦测中实现了96.5%的准确率,增强了在关键设施部署微电网的信心。这些项目共同巩固了北美在微电网市场的领导地位。

预计到2030年,亚太地区的复合年增长率将达到24%,这得益于农村电气化和城市交通拥堵缓解。印度的PM-KUSUM计画为与社区微电网相连的农业太阳能水泵提供补贴,但补贴取消构成了短期风险。孟加拉的一个试点计画结合了太阳能光电、风能和电池,结果显示能源成本低于0.07美元/千瓦时,即使不扩建电网也具有经济可行性。中国正在扩大整合氢能储存的工业微电网规模,日本正在升级社区规模系统以提高抗震能力。这些多元化的倡议正推动该地区微电网市场以比其他任何地区都更快的速度扩张。

欧洲正专注于可再生能源渗透和电网整形技术。由芬兰Fluence公司提供的35兆瓦电池系统正在一个岛屿试验中支援100%可再生能源运作。欧洲审核院估计,到2050年,净零电力需要1.9兆至2.3兆欧元的电网投资,其中一部分将用于资助微电网建设,以缓解拥塞并平衡供电。南美、中东和非洲地区的微电网活动目前正在增加,儘管规模较小,其中最大的微电网部署在刚果,服务于28,000个连接。这些计划凸显了全球范围内在以前依赖柴油发电的地区采用微电网的趋势,并丰富了整体微电网市场前景。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场状况

- 市场概况

- 市场驱动因素

- 加速非洲和南亚农村电气化

- 北美IT/OT融合推动微电网控制器发展

- 用于加勒比海岛屿灾难復原的模组化「盒式」微电网

- 美国和澳洲公用事业主导的社区復原力计划

- 併网逆变器使北欧市场可再生能源利用率达到90%以上

- 美国国防部净零基地(北约和印度太平洋司令部)推广混合微电网

- 市场限制

- 程式码碎片化导緻美国各州互联互通核准延迟

- 印度PM-KUSUM计画的补贴追回风险

- 锂离子价格波动扰乱2024-25年资本支出计划

- 多供应商计划中的网路安全标准有限

- 供应链分析

- 监理前景(目标、政策)

- 技术展望

- 五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争强度

第五章市场规模及成长预测

- 连结性别

- 并联型微电网

- 离网/岛屿微电网

- 按产品

- 硬体(发电机、储存系统、电源转换器和逆变器、控制器)

- 软体(能源管理平台、微电网控制器)

- 服务(工程、采购和施工(EPC)、营运和维护(O&M)、咨询和顾问)

- 按电力源

- 光伏(PV)

- 热电联产(天然气)

- 柴油发电机

- 风力

- 燃料电池

- 其他(生质能、水力发电)

- 按类型

- 交流微电网

- 直流微电网

- 交直流混合微电网

- 按额定功率

- 小于1MW

- 1~5 MW

- 5~10 MW

- 超过10MW

- 按最终用户

- 公共产业

- 商业和工业

- 住房

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 英国

- 德国

- 法国

- 西班牙

- 北欧国家

- 俄罗斯

- 其他欧洲国家

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 东南亚国协

- 其他亚太地区

- 南美洲

- 巴西

- 阿根廷

- 哥伦比亚

- 南美洲其他地区

- 中东和非洲

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 南非

- 埃及

- 其他中东和非洲地区

- 北美洲

第六章 竞争态势

- 市场集中度

- 策略性倡议(併购、伙伴关係、购电协议)

- 市场占有率分析(主要企业的市场排名/份额)

- 公司简介

- ABB Ltd

- Siemens AG

- Schneider Electric SE

- General Electric Company

- Hitachi Energy Ltd

- Eaton Corporation PLC

- Honeywell International Inc.

- Toshiba Corporation

- S&C Electric Company

- ENGIE EPS SA

- Standard Microgrid Inc.

- PowerSecure Inc.

- Bloom Energy Corporation

- Caterpillar Inc.

- Wartsila Corporation

- Rolls-Royce Power Systems AG(MTU)

- Ameresco Inc.

- Tesla Inc.

- Enphase Energy Inc.

- Heila Technologies

- Spirae LLC

- Xendee Corporation

- HOMER Energy LLC

- AutoGrid Systems

第七章 市场机会与未来展望

The Microgrid Market size is estimated at USD 20.54 billion in 2025, and is expected to reach USD 46.99 billion by 2030, at a CAGR of 17.85% during the forecast period (2025-2030).

Growth is catalyzed by IT/OT convergence that embeds edge analytics, digital twins, and cybersecurity layers into advanced controllers, enabling real-time optimization across hardware fleets. Large-scale rural electrification, notably the World Bank's Mission 300 targeting 300 million Africans by 2030, is expanding off-grid demand. The commercial and industrial segment's need for uninterrupted power and defense-funded net-zero base programs accelerates hybrid microgrid configurations. Meanwhile, declining solar PV and battery costs open new value streams, although lithium-ion price volatility and fragmented interconnection codes temper near-term project timelines.

Global Microgrid Market Trends and Insights

Accelerated Rural Electrification in Africa & South Asia

Rural microgrid rollouts hit a new high in 2024 as concessional finance, falling hardware prices, and streamlined procurement converged. The Democratic Republic of Congo approved Africa's largest solar mini-grid in October 2024: a USD 50.3 million project backed by the Multilateral Investment Guarantee Agency to serve 28,000 households and small businesses. The "State of the Global Mini-Grids Market 2024" report shows that sub-Saharan Africa now hosts more than 5,000 operational mini-grids, triple the fleet counted in 2020, with solar providing 59% of installed generation capacity. In Bangladesh, a 2024 case study on a solar-wind-battery microgrid designed for an isolated village demonstrated a levelized cost of USD 0.0688/kWh-less than regional grid extension benchmarks-illustrating the economic viability of renewables-only designs. Multiple governments have adopted results-based financing windows that disburse subsidies upon verified customer connections, cutting first-loss risk for private developers and accelerating deployment pipelines scheduled for 2025. These developments collectively enlarge the near-term demand pool and underpin the forecast CAGR uplift for the microgrid market.

IT/OT Convergence Spurs Advanced Microgrid Controllers in North America

Advanced controllers now integrate SCADA data, cloud analytics, and AI-driven cybersecurity, allowing assets to self-optimize under changing market signals. Siemens and Microsoft extended their partnership in March 2025, blending PLC data with Azure-based models to shrink unplanned downtime for microgrid operators. Digital twins enable real-time simulation of operating states, accelerating fault detection and dispatch decisions. The White House Energy Modernization Cybersecurity plan anticipates distributed energy resources climbing from 90 GW in 2024 to 380 GW by 2025, heightening the need for secure OT protocols. An AI anomaly-detection framework has reached 96.5% accuracy, sharply reducing response time to cyber threats. These capabilities elevate confidence among utilities and military users, reinforcing the microgrid market growth outlook.

Fragmented Interconnection Codes Impede Market Growth

Project queues in several U.S. Independent System Operators have exceeded five years. The Valencia Gardens storage project in San Francisco was abandoned after unforeseen interconnection costs, illustrating regulatory risk. The Department of Energy urges distribution utilities to build bottom-up load models to ease bottlenecks. European developers also cite divergent standards between member states, increasing engineering overheads. Lack of harmonization discourages investors and slows utility procurement cycles, constraining the microgrid market expansion over the medium term.

Other drivers and restraints analyzed in the detailed report include:

- Modular "Box" Microgrids for Disaster-Recovery in Caribbean Islands

- Utility-Led Programs Redefine Community Energy Resilience

- Lithium-Ion Volatility Forces Storage Diversification Strategies

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Grid-connected projects held 62% of the microgrid market share in 2024, equating to USD 10.7 billion of the global microgrid market size. Their appeal stems from tariff arbitrage opportunities and the ability to island during outages. Utility resilience mandates and community programs support a projected 19% CAGR through 2030. Dual-mode architectures now integrate synchrophasor data so systems switch in sub-200 ms, maintaining power-quality standards during wildfires or storms. Though smaller in aggregate value, off-grid microgrids underpin the rural electrification push across Africa and South Asia. World Bank-backed schemes prove that solar-storage hybrids can meet 24/7 demand at competitive rates, expanding the funnel for off-grid EPC contracts and adding depth to the microgrid market.

Off-grid deployments attract concessionary finance from climate funds, allowing longer paybacks and subsidized tariffs. Developers leverage standardized container designs to minimize on-site construction days and improve bankability. Community ownership models also enhance revenue recovery and boost local economic development. As telecom towers and mining operations seek cleaner power, self-sufficient microgrids broaden the microgrid industry footprint beyond pure electrification plays. Over the forecast horizon, connectivity choice will depend on tariff structures, outage statistics, and policy incentives, but mixed portfolios are expected to dominate investor pipelines.

In 2024, hardware generated USD 10.9 billion, representing 63% of the microgrid market size. Controllers, inverters, and battery racks form the physical core. Grid-forming inverters keep systems stable even when renewable penetration exceeds 90% in Nordic pilots. Storage innovation is accelerating as vendors test hybrid battery packs and integrate supercapacitors for fast ramping. Software, although accounting for just 15% of traditional budgets, is growing at 22% CAGR, driven by digital twins and market-participation algorithms. These platforms extend asset life, cut dispatch errors, and unlock ancillary-service revenues, amplifying total microgrid market returns.

Service providers cover site assessment, permitting, EPC, and operations. Growing complexity, particularly in multi-vendor environments, raises demand for specialized integrators who guarantee system-level cybersecurity and service-level agreements. Consultancy practices are expanding into performance assurance, leveraging machine-learning models that predict degradation rates. As customers prioritize outcome-based contracts, microgrid-as-a-service offerings bundle hardware, software, and operations into a single subscription fee, lowering the entry barriers for small commercial clients.

The Microgrid Market Report is Segmented by Connectivity (Grid-Connected and Off-Grid), Offering (Hardware, Software, and Services), Power Sources (Solar Photovoltaic, Combined Heat and Power, Fuel Cell, and More), Type (AC Microgrids, DC Microgrids, and Others), Power Rating (Below 1 MW, 1 To 5 MW, and Others), End-User (Utilities, Commercial and Industrial, and Residential) and Geography (North America, Asia-Pacific, and Others).

Geography Analysis

North America generated 38% of 2024 revenue, supported by USD 10.5 billion in Department of Energy Grid Resilience and Innovation Partnerships funding that targets extreme-weather mitigation.The Department of Defense allocated USD 548 million for energy-resilience upgrades at bases, channeling procurement toward hybrid microgrids. Cybersecurity remains a regional focus; a layered AI-based framework recorded 96.5% threat-detection accuracy, reinforcing trust in critical-facility deployments. Collectively, these programs solidify North America's leadership in the microgrid market.

Asia-Pacific is forecast to expand at a 24% CAGR to 2030, propelled by rural electrification and urban congestion relief. India's PM-KUSUM scheme underwrites agricultural solar pumps that interface with community microgrids, although subsidy claw-backs pose short-term risk. A Bangladeshi pilot combining PV, wind, and batteries achieved an energy cost below USD 0.07/kWh, demonstrating economic viability even without grid extension. China is scaling industrial park microgrids that integrate hydrogen storage, while Japan refines neighborhood-scale systems for seismic resilience. These diverse initiatives enlarge the regional microgrid market faster than any other geography.

Europe concentrates on high-renewables penetration and grid-forming technology. A Finnish 35 MW battery system supplied by Fluence supports 100% renewable operation during islanding trials. The European Court of Auditors states that reaching net-zero will demand EUR 1.9-2.3 trillion in grid investments by 2050, part of which will fund microgrids to relieve congestion and balance supply. South America and the Middle East & Africa are smaller today but show escalating activity, highlighted by the Congo's largest mini-grid rollout that will serve 28,000 connections. These projects underscore the global diffusion of microgrids into regions previously reliant on diesel generation, enriching the overall microgrid market landscape.

- ABB Ltd

- Siemens AG

- Schneider Electric SE

- General Electric Company

- Hitachi Energy Ltd

- Eaton Corporation PLC

- Honeywell International Inc.

- Toshiba Corporation

- S&C Electric Company

- ENGIE EPS SA

- Standard Microgrid Inc.

- PowerSecure Inc.

- Bloom Energy Corporation

- Caterpillar Inc.

- Wartsila Corporation

- Rolls-Royce Power Systems AG (MTU)

- Ameresco Inc.

- Tesla Inc.

- Enphase Energy Inc.

- Heila Technologies

- Spirae LLC

- Xendee Corporation

- HOMER Energy LLC

- AutoGrid Systems

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated Rural Electrification in Africa & South Asia

- 4.2.2 IT/OT Convergence Spurs Advanced Microgrid Controllers in North America

- 4.2.3 Modular "Box" Microgrids for Disaster-Recovery in Caribbean Islands

- 4.2.4 Utility-led Community Resilience Programs in U.S. & Australia

- 4.2.5 Grid-Forming Inverters Enabling 90%+ Renewables in Nordic Markets

- 4.2.6 Defense-Funded Net-Zero Bases Driving Hybrid Microgrids (NATO & INDOPACOM)

- 4.3 Market Restraints

- 4.3.1 Fragmented Codes Stalling Inter-connection Approvals in U.S. States

- 4.3.2 Subsidy Claw-Back Risk in India's PM-KUSUM Programme

- 4.3.3 Lithium-ion Price Volatility Disrupting CAPEX Planning 2024-25

- 4.3.4 Limited Cyber-security Standards for Multi-Vendor Projects

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Outlook (Targets, Policies)

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Connectivity

- 5.1.1 Grid-Connected Microgrids

- 5.1.2 Off-Grid/Islanded Microgrids

- 5.2 By Offering

- 5.2.1 Hardware (Power Generators, Energy-Storage Systems, Power Converters & Inverters, and Controllers)

- 5.2.2 Software (Energy Management Platforms, and Microgrid Controllers)

- 5.2.3 Services (Engineering, Procurement & Construction (EPC), Operations & Maintenance (O&M), and Consulting & Advisory)

- 5.3 By Power Source

- 5.3.1 Solar Photovoltaic (PV)

- 5.3.2 Combined Heat and Power (Natural Gas)

- 5.3.3 Diesel Generators

- 5.3.4 Wind

- 5.3.5 Fuel Cells

- 5.3.6 Others (Biomass, Hydro)

- 5.4 By Type

- 5.4.1 AC Microgrids

- 5.4.2 DC Microgrids

- 5.4.3 Hybrid AC/DC Microgrids

- 5.5 By Power Rating

- 5.5.1 Below 1 MW

- 5.5.2 1 to 5 MW

- 5.5.3 5 to 10 MW

- 5.5.4 Above 10 MW

- 5.6 By End-User

- 5.6.1 Utilities

- 5.6.2 Commercial and Industrial

- 5.6.3 Residential

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 Europe

- 5.7.2.1 United Kingdom

- 5.7.2.2 Germany

- 5.7.2.3 France

- 5.7.2.4 Spain

- 5.7.2.5 Nordic Countries

- 5.7.2.6 Russia

- 5.7.2.7 Rest of Europe

- 5.7.3 Asia-Pacific

- 5.7.3.1 China

- 5.7.3.2 India

- 5.7.3.3 Japan

- 5.7.3.4 South Korea

- 5.7.3.5 ASEAN Countries

- 5.7.3.6 Rest of Asia-Pacific

- 5.7.4 South America

- 5.7.4.1 Brazil

- 5.7.4.2 Argentina

- 5.7.4.3 Colombia

- 5.7.4.4 Rest of South America

- 5.7.5 Middle East and Africa

- 5.7.5.1 United Arab Emirates

- 5.7.5.2 Saudi Arabia

- 5.7.5.3 South Africa

- 5.7.5.4 Egypt

- 5.7.5.5 Rest of Middle East and Africa

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 ABB Ltd

- 6.4.2 Siemens AG

- 6.4.3 Schneider Electric SE

- 6.4.4 General Electric Company

- 6.4.5 Hitachi Energy Ltd

- 6.4.6 Eaton Corporation PLC

- 6.4.7 Honeywell International Inc.

- 6.4.8 Toshiba Corporation

- 6.4.9 S&C Electric Company

- 6.4.10 ENGIE EPS SA

- 6.4.11 Standard Microgrid Inc.

- 6.4.12 PowerSecure Inc.

- 6.4.13 Bloom Energy Corporation

- 6.4.14 Caterpillar Inc.

- 6.4.15 Wartsila Corporation

- 6.4.16 Rolls-Royce Power Systems AG (MTU)

- 6.4.17 Ameresco Inc.

- 6.4.18 Tesla Inc.

- 6.4.19 Enphase Energy Inc.

- 6.4.20 Heila Technologies

- 6.4.21 Spirae LLC

- 6.4.22 Xendee Corporation

- 6.4.23 HOMER Energy LLC

- 6.4.24 AutoGrid Systems

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

2026年全球并联型安装市场报告2026年全球微电网控制器软体市场报告

2026年全球并联型安装市场报告2026年全球微电网控制器软体市场报告 微电网市场(至 2035 年):依组件、电源、容量范围、连接方式、技术、终端用户产业和地区划分:产业趋势和全球预测

微电网市场(至 2035 年):依组件、电源、容量范围、连接方式、技术、终端用户产业和地区划分:产业趋势和全球预测 2026-2030年全球微电网市场

2026-2030年全球微电网市场 混合微电网市场机会、成长要素、产业趋势分析及2026-2035年预测

混合微电网市场机会、成长要素、产业趋势分析及2026-2035年预测 即插即用型太阳能发电机市场:依容量范围、电池类型、应用、最终用户和分销管道划分,全球预测(2026-2032年)微电网软体市场:按软体类型、部署模式、最终用户和应用划分,全球预测(2026-2032年)

即插即用型太阳能发电机市场:依容量范围、电池类型、应用、最终用户和分销管道划分,全球预测(2026-2032年)微电网软体市场:按软体类型、部署模式、最终用户和应用划分,全球预测(2026-2032年) 2026-2034年全球交流微电网市场规模、份额、趋势和成长分析报告全球微电网市场规模、份额、趋势和成长分析报告(2026-2034年)2026年全球微电网市场报告

2026-2034年全球交流微电网市场规模、份额、趋势和成长分析报告全球微电网市场规模、份额、趋势和成长分析报告(2026-2034年)2026年全球微电网市场报告