|

市场调查报告书

商品编码

1939701

缝纫机:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Sewing Machines - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

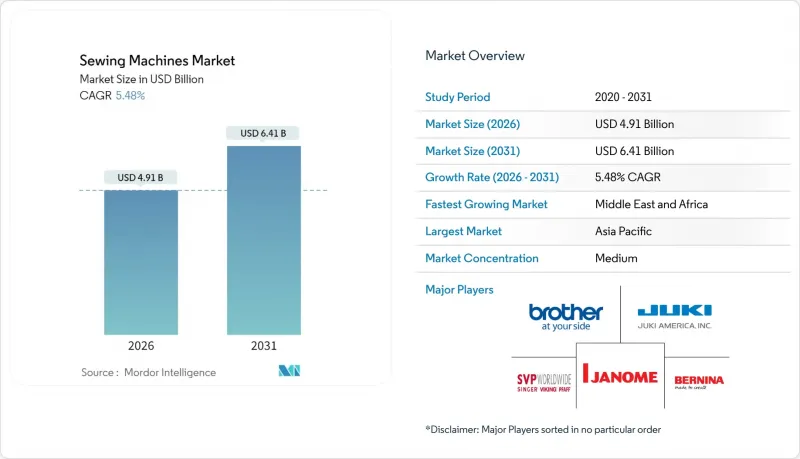

预计到 2026 年,缝纫机市场规模将达到 49.1 亿美元,高于 2025 年的 46.5 亿美元。

预计到 2031 年将达到 64.1 亿美元,2026 年至 2031 年的复合年增长率为 5.48%。

工业自动化需求的不断增长、创客运动的兴起以及工厂和家庭中为提高生产效率和减少废弃物而进行的快速能力升级,共同推动了成长。製造商受惠于双重因素:一方面是亚洲庞大的纺织品出口量,另一方面是北美和欧洲「优先维修」的文化。 Wi-Fi 连接、可下载的针迹库和可程式逻辑控制器 (PLC) 等技术升级延长了产品更换週期,同时提高了平均售价,即使销量趋于平稳,也能保证收入成长。服饰生产向美国和西欧的近岸外包进一步扩大了工业系统在灵活的小批量生产方面的潜在市场,该系统无需更换大量模具即可实现款式变更。

全球缝纫机市场趋势与洞察

亚太地区服装製造业的快速扩张

在政府激励措施和出口导向策略的支持下,亚洲服饰生产持续领先其他地区。光是印度就计画在2030年实现3,500亿美元的纺织品出口额,促使其大量采购高生产力的缝纫生产线。与技术纺织品生产挂钩的激励措施正在缩短自动化机器的投资回收期,这些机器无需人工操作,并能处理各种重量的布料。传统低成本地区的薪资上涨迫使製造商转向使用配备伺服马达和可程式设计缝纫图案的机器,以抵消人事费用。越南和孟加拉的工厂集群简化了售后物流,并鼓励供应商建立区域服务中心。随着订单从基本款T恤转向高价值的休閒和正装,对能够进行复杂缝纫结构和数位压板调节的机器的需求日益增长。

成熟经济体中DIY与手工艺文化的復兴

对于Z世代消费者而言,家用缝纫机代表着一种个人化时尚和减少纺织品废弃物的方式,而社群媒体上的教学正在将这种兴趣转化为实际的硬体销售。零售商推出了入门套装,将入门级缝纫机与可下载的纸样搭配,以降低学习门槛。缝纫在疫情期间成为一项热门爱好,并在解封后成为人们主要的减压方式,即使其他家居装修类别恢復正常,缝纫机的零售依然居高不下。紧凑的设计适合小户型空间,而类似智慧型手机的触控萤幕则引起了数位原生代的共鸣,迫使製造商优先考虑直观的用户体验而非机械的复杂性。 Etsy等手工製品转售平台的兴起促进了爱好变现,并鼓励用户在基本功能不再适用时升级设备。

工业机械的初始投资金额很高

虽然供应商提供融资方案,但这些方案仅涵盖硬件,不包括培训或维护。银行通常要求提供抵押品,而小规模工坊往往缺乏抵押品,导致现代化改造週期延迟后,生产车间仍在使用十年前的锁式缝纫机。随着品牌对缝纫强度和数位化可追溯性的要求日益提高,延迟投资会损害企业的竞争力。 JUKI 于 2024 年推出的租赁计划在越南率先采用,但在其他地区仍属新鲜事物,部分原因是营运商担心长期被专有软体生态系统锁定。

细分市场分析

到2025年,电动缝纫机将占总销量的64.35%,这印证了其在工厂和家庭中的广泛应用。许多工业用户透过加装伺服驱动器和半自动剪线器来延长机器的构成比,将这一细分市场定位为迈向全面自动化的过渡阶段。同时,随着工厂寻求稳定的缝纫品质和减少返工,预计到2031年,自动化缝纫机的年复合成长率将达到6.62%。自动化缝纫机的市场规模正在不断扩大,反映出运动服装和产业用纺织品工厂的需求日益增长。手动缝纫机在电力供应不稳定的地区仍然具有重要意义,并且在重视手感操作的工匠群体中也占有一席之地。

由于备件供应充足且操作人员普遍熟练,电动缝纫机仍然占据主导地位,从而缩短了培训时间。胜家(Singer)的M3330缝纫机配备了Wi-Fi功能,就是一个很好的例子,它在传统缝纫机类别中融入了智慧功能,而无需像数控机床那样复杂。液压驱动的绗缝机属于「其他」类别,在床垫製造领域取得了成功,并已拓展到土耳其和波兰等地区。电动缝纫机和入门级自动化系统之间的价格差异已缩小至18%,这是财务主管开始核准升级的阈值。

到2025年,服饰业仍将保持57.85%的营收主导地位,这主要得益于快时尚巨头和製服供应商的大量订单。在运动服装领域,对适用于拉伸布料的差动送布包缝机的需求不断增长,促使原始设备製造商(OEM)将专用压脚捆绑销售。家用纺织品(包括窗帘和靠垫套)是成长最快的细分市场,复合年增长率(CAGR)达6.69%,主要得益于住宅对个人化家居装饰的投入。预计2024年至2025年,家用纺织品缝纫机的市占率将成长120个基点,预示着家庭客製化趋势的持续发展。汽车内装、医疗抛弃式产品和工业过滤器构成了非服装业,这些产业都需要重型缝纫针和加固型工作台。

消费者对永续室内装潢日益增长的偏好推动了对优质纱线的需求,使供应环保染色纱线的子公司American & Efird受益匪浅。汽车座椅製造商要求每秒40针的加固缝纫能力,这为能够整合高扭矩伺服马达的供应商创造了机会。超音波缝纫技术正在医疗防护装备领域竞争,但监管审核仍然建议关键罩衣采用缝合接缝。印度都市区可支配收入的成长扩大了专用刺绣机的市场,使家庭作坊式的获利模式成为可能。这种多角化经营有助于缓解服饰製造业的经济波动,并在服装业低迷时期支撑OEM厂商的收入。

区域分析

亚太地区预计到2025年将占据全球50.60%的收入份额,这反映了其在从纺织品到时尚产业链中无可比拟的规模以及不断增长的中产阶级消费能力。印度正在实施的生产关联补贴计划,为资本投资提供高达15%的回馈,正在推动工厂快速现代化。中国原始设备製造商(OEM)正在扩大其伺服组件和人机介面的供应,以帮助全球品牌缩短功能升级的前置作业时间。越南服饰的成长促使供应商在胡志明市建立服务仓库,以减少零件更换造成的停机时间。该地区消费者对手工製作的热情也在不断高涨,雅加达和曼谷的零售连锁店报告称,入门级家用手工套装的销售额实现了两位数的增长。

预计中东和非洲将以6.89%的复合年增长率实现最快增长,这得益于结合工业园区和税收优惠的基础设施走廊,例如埃及的苏伊士运河经济区。埃塞俄比亚的哈瓦萨工业园区目前已拥有25家服装製造商,海关数据显示,到2024年,他们将进口总合5,000台可程式设计锁式缝纫机。波湾合作理事会(GCC)成员国正在其「2030愿景」计画下鼓励对纺织业的投资,沙乌地阿拉伯已拨款5亿美元用于建造综合工厂。非洲消费市场也在日趋成熟,中阶可携式缝纫机在尼日利亚的电商平台上节日期间销量良好。培训仍然是一项挑战。原始设备製造商(OEM)正与内罗毕和阿克拉的职业培训机构合作,为操作人员提供基础维护认证。

北美本土製造业正在復苏,主要得益于消费者对本地製造服饰的青睐,以及品牌面临的跨太平洋运输不确定性。耐吉等品牌正在奥勒冈州试行自动化生产线,采用能缝製多种材料的数控缝纫机头。在北卡罗来纳州和南卡罗来纳州,州政府津贴补贴传统工厂升级为智慧工厂的设备购买。加拿大服装业的中小型企业正在部署线上配置器,允许终端用户设计定製图案,这间接提升了对能够处理数位输入檔案的机器的需求。随着美国买家增加本地采购以适应快速反应的零售模式,墨西哥也从中受益。

欧洲成熟的工业基础和先进的永续性政策正在重新定义设备规格。将于2027年生效的生态设计指令要求对每台机器进行精确的能耗测量,迫使原始设备製造商(OEM)转向更高效的伺服马达。德国在汽车和航太应用的技术纺织品领域保持主导地位,推动了对耐用可编程对接缝纫机的需求。义大利奢侈时尚品牌正在利用手工刺绣工匠和自动化设备来维护其「义大利製造」标籤的真实性。由于物流中断,来自亚洲的订单转移到了罗马尼亚和保加利亚等东欧工厂,这些工厂正在迅速扩大生产规模。

在南美洲,巴西圣卡塔琳娜州的服饰丛集正在进行现代化改造,并展现出稳步发展势头,其中包括在电费上涨的情况下引入伺服电机维修以节约能源。乌拉圭和巴拉圭正吸引中国投资者建立从棉花到服饰的一体化生产基地,预计这将促进设备需求的在地化。同时,在智利,电子商务的兴起使得小型家用缝纫机作为一种爱好越来越受欢迎。汇率波动仍然是一个主要不利因素,许多人推迟了进口机械的购买决定,直到外汇稳定下来。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 亚太地区服装製造业的快速扩张

- 成熟经济体中DIY与手工艺文化的復兴

- 物联网和数控缝纫机的技术进步

- 推广工业自动化以提高生产力

- 近岸外包推动了对小批量工业单位的需求

- 「维修与再利用」消费运动强调永续性

- 市场限制

- 工业机械的初始投资金额很高

- 推广低成本再生产品

- 电子元件供应链(微控制器、伺服马达)中的瓶颈

- 缺乏能够操作先进型号的熟练操作员

- 产业价值链分析

- 波特五力分析

- 新进入者的威胁

- 供应商的议价能力

- 买方的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

- 洞察市场最新趋势与创新

- 深入了解市场近期发展动态(新产品发表、策略性倡议、投资、合作、合资、扩张、併购等)

第五章 市场规模与成长预测

- 按模型

- 手动的

- 电

- 自动化

- 其他机器类型

- 透过使用

- 服装与时尚

- 非服饰纺织品(用于汽车和家具)

- 鞋类/皮革製品

- 家用纺织品和工艺品

- 其他用途

- 最终用户

- 住宅

- 产业

- 透过分销管道

- B2C/零售

- 多品牌商店

- 独家品牌店

- 在线的

- 其他分销管道

- 製造商的B2B/直接销售

- B2C/零售

- 按地区

- 北美洲

- 加拿大

- 我们

- 墨西哥

- 南美洲

- 巴西

- 秘鲁

- 智利

- 阿根廷

- 南美洲其他地区

- 欧洲

- 英国

- 德国

- 法国

- 西班牙

- 义大利

- 比荷卢经济联盟(比利时、荷兰、卢森堡)

- 北欧国家(丹麦、芬兰、冰岛、挪威、瑞典)

- 其他欧洲地区

- 亚太地区

- 印度

- 中国

- 日本

- 澳洲

- 韩国

- 东南亚(新加坡、马来西亚、泰国、印尼、越南、菲律宾)

- 亚太其他地区

- 中东和非洲

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 南非

- 奈及利亚

- 其他中东和非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Brother Industries, Ltd.

- JUKI Corporation

- SVP Worldwide(Singer(R), Husqvarna Viking(R), Pfaff(R))

- Janome Sewing Machine Co., Ltd.

- Bernina International AG

- Mitsubishi Electric Corp.(Industrial Sewing Machinery)

- Jack Sewing Machine Co., Ltd.

- Pegasus Sewing Machine Mfg. Co., Ltd.

- Toyota Industries Corp.(TACHINO)

- Baby Lock/Tacony Corporation

- Zoje Sewing Machine Co., Ltd.

- Feiyue Group Co., Ltd.

- Union Special LLC

- Rimoldi & CF

- SunStar Co., Ltd.

- Yamato Sewing Machine Mfg. Co., Ltd.

- Typical Sewing Machine Co., Ltd.

- Seiko Sewing Machine Co., Ltd.

- Merrow Sewing Machine Company

第七章 市场机会与未来展望

Sewing machine market size in 2026 is estimated at USD 4.91 billion, growing from 2025 value of USD 4.65 billion with 2031 projections showing USD 6.41 billion, growing at 5.48% CAGR over 2026-2031.

Industrial automation requirements power growth, the widening maker movement, and rapid feature upgrades that allow both factories and households to boost productivity while reducing waste. Manufacturers benefit from dual exposure: large-volume textile exports in Asia and the repair-over-replace culture in North America and Europe. Technology upgrades toward Wi-Fi connectivity, downloadable stitch libraries, and programmable logic controllers lengthen replacement cycles yet raise average selling prices, supporting revenue even when unit volumes plateau. Near-shoring of garment production back to the United States and Western Europe further expands the addressable base for flexible, small-batch industrial systems that can switch styles without lengthy retooling.

Global Sewing Machines Market Trends and Insights

Rapid Apparel-Manufacturing Expansion in Asia-Pacific

Asia continues to outpace every other region in apparel output, fueled by public incentives and export-oriented strategies. India alone targets USD 350 billion in textile exports by 2030, stimulating bulk procurement of high-throughput sewing lines . Production-linked schemes covering technical textiles lower the payback period on automated machines that handle multiple fabric weights without manual intervention. Growing wages in legacy low-cost centers push manufacturers toward units with servo motors and programmable stitch patterns that offset labor costs. Factory clustering in Vietnam and Bangladesh simplifies after-sales logistics, encouraging suppliers to embed regional service hubs. As orders shift from basic tees to higher-value athleisure and formalwear, demand tilts toward machines capable of complex seam constructions and digital platen adjustments.

DIY & Craft Culture Revival in Mature Economies

Gen Z consumers view home sewing as a route to personalized fashion and lower textile waste, and social media tutorials convert that interest into measurable hardware sales. Retailers now curate starter bundles that pair entry-level machines with downloadable patterns, easing the learning curve. Pandemic-era hobby adoption has persisted post-lockdown as a stress-relief habit, keeping retail sell-through high even as other home-improvement categories normalize. Compact form factors that fit small apartments and smartphone-like touchscreens resonate with digital natives, forcing brands to prioritize intuitive UX over mechanical complexity. The rising tide of reseller platforms for handmade items, such as Etsy, further monetizes the hobby, reinforcing equipment upgrades once users outgrow basic functions.

High Capital Outlay for Industrial Machines

Vendor financing options exist yet cover only the hardware, leaving training and maintenance outside loan packages. Banks often require collateral that small workshops lack, delaying modernization cycles and leaving production stuck with 10-year-old lockstitch units. Deferred investment saps competitiveness when brands demand tight tolerances on seam strength and digital traceability. Leasing programs introduced by JUKI in 2024 showed early adoption in Vietnam but remain a novelty elsewhere, partly because operators fear long-term commitment to proprietary software ecosystems.

Other drivers and restraints analyzed in the detailed report include:

- Advancements in IoT-Enabled and CNC Sewing Machines

- Industrial Automation Push for Productivity

- Shortage of Skilled Operators

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Electric models accounted for 64.35% of revenue in 2025, underscoring their versatility for factories and households alike. Many industrial buyers regard the segment as an interim step toward full automation, adding servo drives and semi-automatic thread cutters to stretch machine life cycles. Automated units, meanwhile, are slated to expand at 6.62% CAGR through 2031 as factories chase consistent stitch quality and lower rework. The sewing machine market size for automated systems is growing, reflecting rising demand from sportswear and technical-textile plants. Manual machines linger in regions with unstable electricity grids, carving out a defensible niche among artisans who prize tactile control.

Continued dominance of the electric segment derives from abundant spare parts and universal familiarity among operators, decreasing training periods. Singer's Wi-Fi-ready M3330 illustrates how traditional categories absorb smart features without jumping to full CNC complexity. Hydraulically actuated quilting machines populate the "other" category and find success in mattress manufacturing, expanding geographic penetration into Turkey and Poland. Price gaps between electric and entry-level automated systems have narrowed to 18%, a threshold at which CFOs start green-lighting upgrades.

Apparel retained a commanding 57.85% slice of 2025 revenue due to vast order volumes from fast-fashion giants and uniform suppliers. Sportswear gains traction as stretch fabrics require differential-feed overlockers, prompting OEMs to bundle specialized presser feet. Home textiles, including curtains and cushion covers, represent the fastest-growing niche with a 6.69% CAGR as homeowners invest in personalized decor. The sewing machine market share for home-textile applications rose 120 basis points between 2024 and 2025, signaling a durable shift toward at-home customization. Automotive upholstery, medical disposables, and industrial filters round out the non-apparel group, each demanding heavy-duty needles and reinforced work tables.

Consumer preference for sustainable interiors boosts premium thread demand, benefiting subsidiaries like American & Efird that supply eco-dyed yarns. Car seat makers specify bar-tacking capabilities at 40 stitches per second, creating opportunities for providers that can integrate high-torque servo motors. In medical PPE, ultrasonic sewing alternatives compete, yet regulatory audits still favor stitched seams for critical gowns. Rising disposable income in urban India grows the market for embroidery-only machines that let users monetize home businesses. This diversification smooths cyclical dips in garment manufacturing, cushioning OEM revenue during apparel slowdowns.

The Sewing Machines Market Report is Segmented by Machine Type (Manual, Electric, and More), by Application (Apparel, Non-Apparel Textiles, and More), by End-User (Residential and Industrial), by Distribution Channel (B2C/Retail and B2B/Directly From the Manufacturers), and by Geography (North America, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific's 50.60% revenue leadership in 2025 reflects its unmatched scale in fiber-to-fashion value chains and ascending middle-class consumption. India continues to roll out Production Linked Incentives that reimburse up to 15% of capital investment, prompting mills to modernize quickly . Chinese OEMs increasingly supply servo components and human-machine interfaces to global brands, shortening lead times for feature updates. Vietnam's apparel export growth encourages suppliers to build service warehouses in Ho Chi Minh City, reducing downtime for spare-part replacements. The region also witnesses swelling consumer enthusiasm for craft hobbies, as retail chains in Jakarta and Bangkok report double-digit sales lift for entry-level home units.

The Middle East and Africa grows the fastest, projected at 6.89% CAGR, supported by infrastructure corridors like Egypt's Suez Canal Economic Zone that bundle industrial parks with duty exemptions. Ethiopia's Hawassa Industrial Park already houses 25 apparel manufacturers that collectively imported more than 5,000 programmable lockstitch machines in 2024 according to customs data. Gulf Cooperation Council states encourage textile investments under Vision-2030 plans, with Saudi Arabia earmarking USD 500 million loans for integrated mills. African consumer markets also mature; Nigeria's e-commerce platforms now list mid-range portable models that sell out during festival seasons. The challenge lies in training; OEMs partner with vocational institutes in Nairobi and Accra to certify operators on basic maintenance.

North America experiences a revival in domestic making, powered by consumers who value locally produced garments and by brands facing unpredictable trans-Pacific freight. Brands such as Nike pilot automated lines in Oregon that rely on CNC sewing heads capable of multi-material stitching. State-level grants in North Carolina and South Carolina subsidize equipment purchases for legacy mills upgrading to smart factories. Canada's apparel SMEs embrace online configurators that allow end-users to design custom patterns, indirectly boosting demand for machines that accept digital input files. Mexico secures spill-over benefits as US buyers near-source to comply with quick-response retail models.

Europe blends mature industrial bases with avant-garde sustainability policies that redefine equipment specifications. Eco-design directives coming into force by 2027 will require precise energy-consumption metrics at the machine level, nudging OEMs toward high-efficiency servo motors. Germany continues to lead in technical textiles for automotive and aerospace, prompting demand for heavy-duty programmable bartackers. Italy's luxury fashion houses employ specialized hand-guided embroiderers alongside automated equipment to uphold "Made in Italy" authenticity. Eastern European factories in Romania and Bulgaria win orders redirected from Asia due to logistics volatility, necessitating rapid scale-up in machine fleets.

South America exhibits steady momentum as Brazil's garment cluster in Santa Catarina modernizes, deploying servo-motor retrofits to capture energy savings under rising electricity tariffs. Uruguay and Paraguay court Chinese investors for integrated cotton-to-apparel complexes that could localize equipment demand. Meanwhile, Chile's e-commerce penetration fosters hobbyist uptake of compact home machines designed for small apartments. Currency fluctuations remain the principal headwind, often delaying purchase decisions for imported machines until exchange rates stabilize.

- Brother Industries, Ltd.

- JUKI Corporation

- SVP Worldwide (Singer(R), Husqvarna Viking(R), Pfaff(R))

- Janome Sewing Machine Co., Ltd.

- Bernina International AG

- Mitsubishi Electric Corp. (Industrial Sewing Machinery)

- Jack Sewing Machine Co., Ltd.

- Pegasus Sewing Machine Mfg. Co., Ltd.

- Toyota Industries Corp. (TACHINO)

- Baby Lock / Tacony Corporation

- Zoje Sewing Machine Co., Ltd.

- Feiyue Group Co., Ltd.

- Union Special LLC

- Rimoldi & CF

- SunStar Co., Ltd.

- Yamato Sewing Machine Mfg. Co., Ltd.

- Typical Sewing Machine Co., Ltd.

- Seiko Sewing Machine Co., Ltd.

- Merrow Sewing Machine Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid apparel-manufacturing expansion in APAC

- 4.2.2 DIY & craft culture revival in mature economies

- 4.2.3 Advancements in IoT-enabled and CNC sewing machines

- 4.2.4 Industrial automation push for productivity

- 4.2.5 Near-shoring boosts demand for small-batch industrial units

- 4.2.6 Sustainability-driven "repair & reuse" consumer movement

- 4.3 Market Restraints

- 4.3.1 High capital outlay for industrial machines

- 4.3.2 Proliferation of low-cost refurbished units

- 4.3.3 Electronics supply-chain bottlenecks (MCUs, servos)

- 4.3.4 Shortage of skilled operators for advanced models

- 4.4 Industry Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Insights into the Latest Trends and Innovations in the Market

- 4.7 Insights on Recent Developments (New Product Launches, Strategic Initiatives, Investments, Partnerships, JVs, Expansion, M&As, etc.) in the Market

5 Market Size & Growth Forecasts

- 5.1 By Machine Type

- 5.1.1 Manual

- 5.1.2 Electric

- 5.1.3 Automated

- 5.1.4 Other Machine Types

- 5.2 By Application

- 5.2.1 Apparel & Fashion

- 5.2.2 Non-apparel Textiles (Automotive, Upholstery)

- 5.2.3 Footwear & Leather Goods

- 5.2.4 Home Textiles & Crafts

- 5.2.5 Other Applications

- 5.3 By End User

- 5.3.1 Residential

- 5.3.2 Industrial

- 5.4 By Distribution Channel

- 5.4.1 B2C/Retail

- 5.4.1.1 Multi-brand Stores

- 5.4.1.2 Exclusive Brand Outlets

- 5.4.1.3 Online

- 5.4.1.4 Other Distribution Channels

- 5.4.2 B2B/Directly from the Manufacturers

- 5.4.1 B2C/Retail

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 Canada

- 5.5.1.2 United States

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Peru

- 5.5.2.3 Chile

- 5.5.2.4 Argentina

- 5.5.2.5 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Spain

- 5.5.3.5 Italy

- 5.5.3.6 BENELUX (Belgium, Netherlands, Luxembourg)

- 5.5.3.7 NORDICS (Denmark, Finland, Iceland, Norway, Sweden)

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 India

- 5.5.4.2 China

- 5.5.4.3 Japan

- 5.5.4.4 Australia

- 5.5.4.5 South Korea

- 5.5.4.6 South-East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines)

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Nigeria

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Brother Industries, Ltd.

- 6.4.2 JUKI Corporation

- 6.4.3 SVP Worldwide (Singer(R), Husqvarna Viking(R), Pfaff(R))

- 6.4.4 Janome Sewing Machine Co., Ltd.

- 6.4.5 Bernina International AG

- 6.4.6 Mitsubishi Electric Corp. (Industrial Sewing Machinery)

- 6.4.7 Jack Sewing Machine Co., Ltd.

- 6.4.8 Pegasus Sewing Machine Mfg. Co., Ltd.

- 6.4.9 Toyota Industries Corp. (TACHINO)

- 6.4.10 Baby Lock / Tacony Corporation

- 6.4.11 Zoje Sewing Machine Co., Ltd.

- 6.4.12 Feiyue Group Co., Ltd.

- 6.4.13 Union Special LLC

- 6.4.14 Rimoldi & CF

- 6.4.15 SunStar Co., Ltd.

- 6.4.16 Yamato Sewing Machine Mfg. Co., Ltd.

- 6.4.17 Typical Sewing Machine Co., Ltd.

- 6.4.18 Seiko Sewing Machine Co., Ltd.

- 6.4.19 Merrow Sewing Machine Company

7 Market Opportunities & Future Outlook

- 7.1 Growing demand for compact and portable sewing machines

- 7.2 Increasing prevalence of smart (integration of IoT and AI) and computerized sewing machines

家用缝纫机市场:按机器类型、价格范围、分销管道和应用划分,全球预测(2026-2032年)

家用缝纫机市场:按机器类型、价格范围、分销管道和应用划分,全球预测(2026-2032年) 2026年全球缝纫机市场报告

2026年全球缝纫机市场报告 全球多针刺绣机市场报告、绩效及预测(2020-2031年)电脑缝纫刺绣机市场:产品类型、机器配置、平台、应用领域、销售管道和应用划分,全球预测,2026-2032年

全球多针刺绣机市场报告、绩效及预测(2020-2031年)电脑缝纫刺绣机市场:产品类型、机器配置、平台、应用领域、销售管道和应用划分,全球预测,2026-2032年 缝纫机市场-全球产业规模、份额、趋势、机会和预测,按类型、用途、应用、配销通路、地区和竞争格局划分,2021-2031年预测

缝纫机市场-全球产业规模、份额、趋势、机会和预测,按类型、用途、应用、配销通路、地区和竞争格局划分,2021-2031年预测 刺绣市场规模、份额和成长分析(按产品类型、最终用途产业、材料类型、工艺、通路和地区划分)-2026-2033年产业预测

刺绣市场规模、份额和成长分析(按产品类型、最终用途产业、材料类型、工艺、通路和地区划分)-2026-2033年产业预测 缝纫机市场规模、份额和成长分析(按类型、用途、应用和地区划分)—2026-2033年产业预测

缝纫机市场规模、份额和成长分析(按类型、用途、应用和地区划分)—2026-2033年产业预测 缝纫机:全球市场份额和排名、总收入和需求预测(2025-2031 年)

缝纫机:全球市场份额和排名、总收入和需求预测(2025-2031 年) 2025 年至 2033 年缝纫机市场报告,按产品类型(机械、电子、刺绣)、应用(家用、工业)、配销通路(线上、线下)和地区划分

2025 年至 2033 年缝纫机市场报告,按产品类型(机械、电子、刺绣)、应用(家用、工业)、配销通路(线上、线下)和地区划分 全球刺绣机市场

全球刺绣机市场