|

市场调查报告书

商品编码

1939707

中国施工机械:市场占有率分析、产业趋势与统计、成长预测(2026-2031)China Construction Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

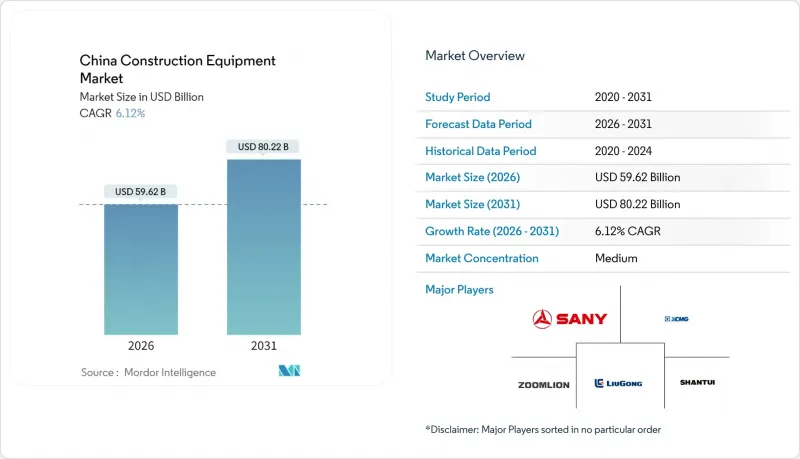

预计到 2026 年,中国施工机械市场规模将达到 596.2 亿美元,高于 2025 年的 561.8 亿美元。

预计到 2031 年,市场规模将达到 802.2 亿美元,2026 年至 2031 年的复合年增长率为 6.12%。

公共部门持续增加对铁路、公路和城市交通网络的投入,加上大力推动电动和智慧机械发展的政策,即使在住宅房地产市场活动放缓的情况下,也支撑着市场需求。诸如计划在2025年投入5,900亿元建设的18万公里全国铁路网等大型计划,带动了强劲的订单累积订单,并带动了对大容量土木工程机械、施工机械和起重设备的需求。同时,在与柴油成本差距缩小以及补贴抵销资本支出影响的推动下,电气化正从试点阶段走向全面部署。出口动能也提供了额外的缓衝。海外出货量超过国内出货量,显示中国整机製造商可以利用海外基础建设週期来抵销国内市场放缓的影响。

中国施工机械市场趋势与展望

政府基础建设投资和「一带一路」倡议

中国快速的基础设施投资是成长要素,仅Delta地区在2024年就投入创纪录的1400亿元人民币用于铁路建设,超过了前一年的1253亿元人民币。国家发展和改革委员会的《2025年装备更新政策》扩大了对工业、能源、交通和农业领域的支持,并透过加大利率补贴降低融资成本,重点扶持高端、智慧和绿色技术。由于基础设施计划的装备生命週期通常为三到五年,且更新模式可预测,此政策框架创造了超越传统建设週期的可持续需求。 「一带一路」倡议的国际化拓展也为国内製造商带来了更多出口机会,2022年中国挖掘机出口的70%销往「一带一路」沿线国家。这形成了一个良性循环:国内规模化生产使其产品具备了国际竞争力。隧道掘进、桥樑建设和轨道铺设等专用施工机械对于铁路网到2030年扩建至18万公里(包括6万公里高速铁路)至关重要。在这些领域,中国製造商凭藉国内计划经验已建立起技术优势。

现代化和电气化政策

政府的装备现代化政策正催生独立于新建设工程的更新换代需求,先进施工机械已被列入工信部《2024年重点技术装备指导目录》的优先发展领域。由于直接补贴和营运成本优势,电动施工机械的普及速度正在加快,中国製造商在某些应用领域已实现了电动和柴油机型的成本持平,从根本上改变了总拥有成本(TCO)的计算方式。 《绿色技术推广目录(2024版)》列出了七大领域的112项先进技术,其中施工机械在节能环保领域占据了显着地位。随着营运商寻求在确保获得最新技术的同时最大限度地减少资本支出,设备即服务(EaaS)模式正变得越来越受欢迎。一体化的安装和拆卸服务有助于符合安全标准并提高营运效率。这项政策正在形成一个两极化的市场:高端电动和智慧设备保持着较高的利润率,而传统的柴油设备则面临价格压力,这使得拥有强大研发能力和技术组合的製造商受益。

房地产业去槓桿化和建筑业放缓

房地产行业的去槓桿化导致需求暂时中断,开发商缩减了新计画开工和设备采购,尤其是在小型机械和住宅建筑设备领域。然而,政府的都市更新倡议和保障性住宅计画提供了替代需求来源,各大城市优先发展基础设施和公共建设,而非投机性开发。国有企业营运稳定,而私人开发商面临资金限制,两者之间出现了市场缺口,这为设备租赁和灵活的资金筹措模式创造了机会,从而降低了建设公司的资本需求。

细分市场分析

预计到2025年,挖土机和其他土木机械将占中国施工机械市场份额的54.68%,巩固其在土方工程、采矿和地铁隧道建设中的地位。基础设施投资的成长和出口需求的增加将维持高出交付,而随着补贴和电池成本下降削弱柴油引擎的生命週期成本优势,预计到2031年,电动挖土机的复合年增长率将达到11.72%。受电子商务履约驱动的仓储自动化影响,堆高机、伸缩臂堆高机和高空作业平台的需求正在稳步增长。道路施工机械受益于中国不断扩大的17.7万公里国家高速公路网的维护週期,其中自动压路机和摊舖机越来越多地被用作高规格高速公路改造项目中的关键设备。

技术融合将定义未来的竞争格局。挖土机将标配远端资讯处理系统、半自动挖掘演算法以及工厂预先安装的快速连接器,从而缩短附件更换时间。混凝土搅拌机和泵浦将整合物联网感测器,以优化坍落度和运输物流,确保在人口密集的城市中心准时浇筑。预计到2031年,光是中国施工机械挖土机市场规模就将接近439亿美元,这将为投资于专有电池组和控制软体的原始设备製造商(OEM)带来规模经济效益。随着互通性标准的日益成熟,提供开放式架构控制器的零件製造商将获得更大的议价能力,并将价值链重塑为以软体为中心的生态系统。

2025年,内燃机(柴油)仍将占据91.84%的销售份额,这主要得益于完善的燃料供应基础设施、较长的运作週期以及较低的初始价格。然而,到2031年,纯电动车型的年复合成长率将达到36.33%,标誌着一个决定性的转折点。由于北京、上海和深圳等城市实施了零排放法规(限制市政建设新增柴油采购),预计到2031年,中国施工机械市场中纯电动车型的市场规模将超过106亿美元。混合动力系统作为过渡方案,可在频繁怠速的运作週期中降低20-25%的油耗。

成本组成将取决于电池能量密度、充电基础设施和二手价值。製造商的金融部门目前正将充电站和太阳能微电网纳入设备租赁方案,为承包商在计划整个生命週期中提供每千瓦时的固定价格。同时,国家电网营运商正在试行车网互动(V2G)方案,以在运作时段将閒置的机械电池货币化,从而创造额外的收入来源。柴油在极端高温矿山以及「一带一路」沿线偏远、电网覆盖不足的地区仍将发挥重要作用。然而,在噪音和排放法规最严格的大城市土木工程项目中,柴油的份额将下降得最快。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 政府的「2025-30年新基础设施」计划

- 碳中和政策推动电子机械的需求

- 促进OEM出口将有助于在国内实现规模经济。

- 与「一带一路」倡议相关的零件供应商订单

- 当地碳信用市场青睐混合动力汽车

- 数位设备租赁平台刺激了中小企业的需求。

- 市场限制

- 房地产市场长期低迷

- 国内产能过剩引发的价格竞争

- 收紧对中小型承包商的贷款

- 电子设备逆变器和电池管理系统晶片供不应求

- 价值/供应链分析

- 监管环境

- 技术展望

- 波特五力模型

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 按机器类型

- 土木工程施工机械

- 挖土机

- 装载机

- 推土机

- 物料输送机械

- 起重机

- 堆高机

- 伸缩臂堆高机

- 道路施工机械

- 平土机机

- 压路机/压实机

- 摊舖机

- 混凝土设备

- 混凝土搅拌机

- 混凝土泵

- 土木工程施工机械

- 按驱动类型

- 内燃机(柴油引擎)

- 杂交种

- 纯电动

- 按销售管道

- OEM直销

- 由授权经销商出售

- 透过使用

- 建筑施工

- 基础设施建设

- 能源和自然资源

- 其他的

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Sany Group

- Xuzhou Construction Machinery Group Co., Ltd.(XCMG)

- Caterpillar Inc.

- Zoomlion Heavy Industry

- LiuGong Machinery

- Komatsu Ltd.

- Hitachi Construction Machinery

- AB Volvo(Volvo CE)

- Liebherr Group

- Shantui Construction Machinery

- Tadano Ltd.

- JC Bamford Excavators Limited

- Doosan Bobcat Ltd.

- Hyundai Construction Equipment Ltd.

- Yanmar Holdings Co. Ltd.

- Terex Corporation

- China Railway Construction Heavy Industry Co., Ltd.

第七章 市场机会与未来展望

China construction equipment market size in 2026 is estimated at USD 59.62 billion, growing from 2025 value of USD 56.18 billion with 2031 projections showing USD 80.22 billion, growing at 6.12% CAGR over 2026-2031.

Sustained public-sector spending on railway, highway, and urban transit links, paired with a strong policy push for electric and smart machinery, underpins demand even as residential real-estate activity cools. Large-scale projects such as the 180,000 km national railway build-out, for which CNY 590 billion was earmarked in 2025, keep order books healthy and favor high-capacity earth-moving and lifting equipment. At the same time, electrification is moving from pilot projects to scaled deployment as cost parity with diesel narrows and subsidies offset capital outlays. Export momentum offers an additional cushion: overseas shipments have overtaken domestic deliveries, signaling that Chinese original-equipment manufacturers (OEMs) can lean on foreign infrastructure cycles to balance local slowdowns.

China Construction Equipment Market Trends and Insights

Government Infrastructure Investment and Belt Road Initiative

China's infrastructure investment surge represents the primary growth catalyst, with the Yangtze River Delta region alone allocating CNY 140 billion for railway construction in 2024, marking a record high that surpasses the previous year's CNY 125.3 billion. The National Development and Reform Commission's 2025 equipment update policy expands support across industrial, energy, transportation, and agricultural sectors, emphasizing high-end, intelligent, and green technologies with enhanced loan interest subsidies to reduce financing costs. This policy framework creates sustained demand beyond traditional construction cycles, as infrastructure projects typically require 3-5 year equipment lifecycles with predictable replacement patterns. The Belt and Road Initiative's international dimension amplifies domestic manufacturers' export opportunities, with 70% of Chinese excavator exports directed to BRI countries in 2022, creating a virtuous cycle where domestic production scale enables competitive international pricing. Railway network expansion to 180,000 km by 2030, including 60,000 km of high-speed rail, necessitates specialized construction equipment for tunneling, bridge construction, and track laying, segments where Chinese manufacturers have developed technological advantages through domestic project experience.

Equipment Modernization and Electrification Policies

The government's equipment modernization mandate creates replacement demand independent of new construction activity, with the Ministry of Industry and Information Technology's 2024 Major Technological Equipment Guidance Catalog prioritizing advanced construction machinery. Electric construction equipment adoption accelerates through direct subsidies and operational cost advantages, with Chinese manufacturers achieving cost parity between electric and diesel versions in certain applications, fundamentally altering total cost of ownership calculations. The Green Technology Promotion Directory (2024 Edition) includes 112 advanced technologies across seven sectors, with construction equipment featuring prominently in energy-efficient and environmental protection categories. Equipment-as-a-service models gain traction as operators seek to minimize capital expenditure while accessing latest technology, with integrated installation-dismantling services improving safety compliance and operational efficiency. The policy creates a two-tier market where premium electric and smart equipment commands higher margins while conventional diesel equipment faces pricing pressure, benefiting manufacturers with strong R&D capabilities and technology portfolios.

Real Estate Sector Deleveraging and Construction Slowdown

The real estate sector's deleveraging process creates temporary demand disruption as developers reduce new project starts and equipment purchases, particularly affecting compact machinery and residential construction equipment segments. However, government urban renewal initiatives and affordable housing programs provide alternative demand sources, with major cities prioritizing infrastructure upgrades and public facility construction over speculative development. Market differentiation emerges between state-owned enterprises maintaining stable operations and private developers facing financial constraints, creating opportunities for equipment leasing and flexible financing models that reduce capital requirements for construction firms.

Other drivers and restraints analyzed in the detailed report include:

- Export Market Expansion and International Competitiveness

- Digitalization and Smart Construction Technology Adoption

- Trade Tensions and Tariff Barriers in International Markets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Earth-moving machinery such as excavators controlled 54.68% of China construction equipment market share in 2025, cementing their role across earthwork, mining and metro tunnelling projects. Rising infrastructure outlays and export demand keep delivery volumes elevated, while electric excavators record a 11.72% CAGR to 2031 as subsidies and falling battery costs erode diesel's lifetime cost advantage. Forklifts, telescopic handlers and aerial platforms gain steady traction from warehouse automation linked to e-commerce fulfilment. Road-building machines benefit from maintenance cycles for an expanding 177,000 km national highway grid, with autonomous rollers and pavers proving headline features on high-profile expressway upgrades.

Technology convergence defines future competition. Excavators now ship with standard telematics, semi-autonomous dig algorithms, and factory-installed quick couplers that cut attachment changeover time. Concrete mixers and pumps integrate IoT sensors to optimize slump quality and dispatch logistics, ensuring on-time pours in dense urban cores. China construction equipment market size for excavators alone is projected to approach USD 43.9 billion by 2031, providing scale economies for OEMs investing in proprietary battery packs and control software. As interoperability standards mature, component suppliers with open-architecture controllers will gain bargaining power, reshaping the value chain toward software-centric ecosystems.

Internal Combustion Engine (Diesel) still powered 91.84% of units sold in 2025, supported by established fueling infrastructure, long duty cycles, and lower upfront pricing. However, full-electric options post a 36.33% CAGR through 2031, signaling a decisive phase-change. The China construction equipment market size for battery-electric models is set to cross USD 10.6 billion by 2031, thanks to zero-emission mandates in Beijing, Shanghai, and Shenzhen that restrict new diesel purchases for municipal works. Hybrid drivetrains offer a bridge solution, trimming fuel burn by 20-25% on duty cycles involving frequent idling.

Cost parity hinges on battery density, charging logistics, and resale values. OEM finance arms now bundle charging depots and solar-powered micro-grids into equipment leases, giving contractors guaranteed kilowatt-hour pricing over project lifetimes. Meanwhile, state grid operators trial vehicle-to-grid schemes that monetize idle machinery batteries during off-shift hours, adding an ancillary revenue stream. Diesel's role will remain pronounced in extreme-temperature mines and remote Belt and Road corridors without grid access. Still, its share will erode fastest in metropolitan civil works segments where noise and emissions rules bite hardest.

The China Construction Equipment Market Report is Segmented by Machinery Type (Earth-Moving Machinery, Material-Handling Machinery, and More), Drive Type (Internal-Combustion, Hybrid, and More), Sales Channel (OEM Direct Sales, and Authorized Dealer Sales), and Application (Building Construction, Infrastructure Construction, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Sany Group

- Xuzhou Construction Machinery Group Co., Ltd. (XCMG)

- Caterpillar Inc.

- Zoomlion Heavy Industry

- LiuGong Machinery

- Komatsu Ltd.

- Hitachi Construction Machinery

- AB Volvo (Volvo CE)

- Liebherr Group

- Shantui Construction Machinery

- Tadano Ltd.

- J.C. Bamford Excavators Limited

- Doosan Bobcat Ltd.

- Hyundai Construction Equipment Ltd.

- Yanmar Holdings Co. Ltd.

- Terex Corporation

- China Railway Construction Heavy Industry Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Govt. 'New Infrastructure 2025-30' pipeline

- 4.2.2 Carbon-neutral mandate spurring electric machinery

- 4.2.3 OEM export push enables domestic economies of scale

- 4.2.4 Belt and Road back-orders for component suppliers

- 4.2.5 Provincial carbon-credit markets favouring hybrids

- 4.2.6 Digital equipment-rental platforms unlocking SME demand

- 4.3 Market Restraints

- 4.3.1 Prolonged real-estate downturn

- 4.3.2 Domestic price wars from over-capacity

- 4.3.3 Tight credit to SME contractors

- 4.3.4 Inverter and BMS chip shortages for e-equipment

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value (USD))

- 5.1 By Machinery Type

- 5.1.1 Earth-moving Machinery

- 5.1.1.1 Excavators

- 5.1.1.2 Loaders

- 5.1.1.3 Dozers

- 5.1.2 Material-Handling Machinery

- 5.1.2.1 Cranes

- 5.1.2.2 Fork-lifts

- 5.1.2.3 Telescopic Handlers

- 5.1.3 Road-Construction Machinery

- 5.1.3.1 Motor Graders

- 5.1.3.2 Rollers/Compactors

- 5.1.3.3 Pavers

- 5.1.4 Concrete Equipment

- 5.1.4.1 Concrete Mixers

- 5.1.4.2 Concrete Pumps

- 5.1.1 Earth-moving Machinery

- 5.2 By Drive Type

- 5.2.1 Internal-Combustion (Diesel)

- 5.2.2 Hybrid

- 5.2.3 Full-Electric

- 5.3 By Sales Channel

- 5.3.1 OEM Direct Sales

- 5.3.2 Authorized Dealer Sales

- 5.4 By Application

- 5.4.1 Building Construction

- 5.4.2 Infrastructure Construction

- 5.4.3 Energy and Natural Resources

- 5.4.4 Others

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Sany Group

- 6.4.2 Xuzhou Construction Machinery Group Co., Ltd. (XCMG)

- 6.4.3 Caterpillar Inc.

- 6.4.4 Zoomlion Heavy Industry

- 6.4.5 LiuGong Machinery

- 6.4.6 Komatsu Ltd.

- 6.4.7 Hitachi Construction Machinery

- 6.4.8 AB Volvo (Volvo CE)

- 6.4.9 Liebherr Group

- 6.4.10 Shantui Construction Machinery

- 6.4.11 Tadano Ltd.

- 6.4.12 J.C. Bamford Excavators Limited

- 6.4.13 Doosan Bobcat Ltd.

- 6.4.14 Hyundai Construction Equipment Ltd.

- 6.4.15 Yanmar Holdings Co. Ltd.

- 6.4.16 Terex Corporation

- 6.4.17 China Railway Construction Heavy Industry Co., Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

橡胶压机市场:依橡胶类型、压机类型、操作模式、产能、应用及通路划分-全球预测,2026-2032年电动施工机械市场:依设备类型、推进系统和应用划分-全球预测,2026-2032年自动液压机市场:按压机类型、控制类型、操作模式和终端用户产业划分,全球预测,2026-2032年

橡胶压机市场:依橡胶类型、压机类型、操作模式、产能、应用及通路划分-全球预测,2026-2032年电动施工机械市场:依设备类型、推进系统和应用划分-全球预测,2026-2032年自动液压机市场:按压机类型、控制类型、操作模式和终端用户产业划分,全球预测,2026-2032年 2026 年至 2035 年施工机械轮胎市场的商业机会、成长要素、产业趋势分析与预测。

2026 年至 2035 年施工机械轮胎市场的商业机会、成长要素、产业趋势分析与预测。 东协施工机械:市场占有率分析、产业趋势与统计、成长预测(2026-2031)施工机械:市场占有率分析、产业趋势与统计、成长预测(2026-2031)泰国施工机械市场占有率分析、产业趋势及统计、成长预测(2026-2031)

东协施工机械:市场占有率分析、产业趋势与统计、成长预测(2026-2031)施工机械:市场占有率分析、产业趋势与统计、成长预测(2026-2031)泰国施工机械市场占有率分析、产业趋势及统计、成长预测(2026-2031) 2026年全球建筑及道路施工机械市场报告2026年全球施工机械市场报告2026年全球液压搭乘用电梯市场报告

2026年全球建筑及道路施工机械市场报告2026年全球施工机械市场报告2026年全球液压搭乘用电梯市场报告