|

市场调查报告书

商品编码

1849987

欧洲下一代储存:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)Europe Next Generation Storage - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

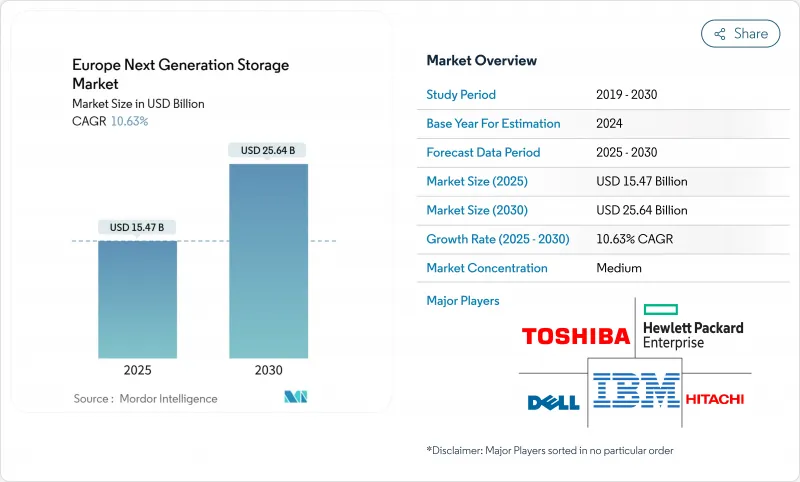

预计欧洲下一代储存市场规模将在2025年达到154.7亿美元,到2030年将扩大至256.4亿美元,复合年增长率为10.6%。

欧盟资料立法支援持续成长,该立法将于2025年9月生效,要求提供者促进云端迁移。同时,人工智慧训练和推理工作负载正在推动储存流量的成长,而能源效率法规也日益严格,倾向于每瓦延迟更低的快闪记忆体架构。法兰克福、伦敦、阿姆斯特丹、巴黎和都柏林的容量限制正推动营运商进行边缘部署,而对Gaia-X和virt8ra等主权云端计划的持续投资,正在刺激对可互通、与供应商无关的平台的需求,这些平台涵盖核心、云端和边缘场景。随着传统阵列供应商重新调整其产品组合,以应对超大规模云端创新、纯快闪记忆体专家以及欧洲主权云端供应商的挑战,竞争压力日益加剧。

欧洲下一代储存市场趋势与洞察

数位资料的爆炸性成长

预计2023年至2028年间,全球资料量将成长两倍,而GDPR规定的本地储存要求大部分成长资料必须储存在欧盟境内。因此,计划部署Petabyte级容量的企业正在部署混合拓扑结构,将本地阵列与自主云端扩展相结合,以确保合规性并降低延迟。支出模式明显倾向于可扩展的软体定义平台,这些平台可以容纳各种文件和物件工作负载,而无需锁定供应商。因此,随着越来越多的企业寻求在单一架构中兼顾合规性和效能,欧洲下一代储存市场的成长速度将高于全球平均水准。

快速过渡到 SSD 和 NVMe 架构

企业采用 PCIe Gen5 NVMe 正在缩小曾经存在于本地阵列和公共云端之间的效能差距。拥抱工业 4.0 的德国製造工厂的延迟预算已低于 100µs。能源效率如今已成为一项板级指标,SSD 每Terabyte 的消费量远低于 HDD,这有助于达到《德国能源效率法》规定的资料中心到 2027 年 50%可再生能源的基准值。这些动态将快闪记忆体媒体定位为欧洲下一代储存产业的策略性而非战术性投资。

全快闪和 NVMe 阵列的资本成本高昂

企业级 SSD 的单价仍高企,是 HDD 容量的 9.9 倍。对于中小企业而言,即使考虑到快闪记忆体的节能效果,这种差异也使得投资报酬率 (ROI) 的计算变得复杂。虽然超大规模资料中心的采用正在推动短期内价格下降,但许多欧洲中小企业仍将继续在混合使用 QLC 快闪记忆体和高容量磁碟的混合层中部署工作负载,直到快闪记忆体突破每位元成本阈值。

細項分析

预计到 2024 年,直接连接储存将占欧洲下一代储存市场规模的 45.6%,这突显了企业对关键任务工作负载可预测延迟的偏好,而融合式基础架构基础设施预计将实现 11.6% 的复合年增长率,这反映了对将运算、储存和网路结合到单一策略域中的横向节点的需求。

德国的国家数位化津贴正在推动超融合的发展动能。製造商需要在不违反主权法规的情况下进行现场处理以分析感测器资料。戴尔科技和 CoreWeave 的机架级 AI 平台证明,融合资源能够透过Petabyte级快闪记忆体提供 1.4 百亿亿次浮点运算,从而在单片阵列和纯公共云层之间创造出一个极具吸引力的中间地带。

檔案和物件式的储存为非结构化资料集(从分析日誌到 8K 媒体檔案)提供 RESTful、可扩展的储存库,到 2024 年将占据欧洲下一代储存市场 65.7% 的份额。软体定义储存正以 12.1% 的复合年增长率迅速扩张,因为它将服务与硬体分离并实现了资料可携性的承诺。

欧洲的银行和保险公司正在试用资料移动编排器,这些编排器可以在主权云端合作伙伴之间即时迁移Petabyte级资料集,且不会中断交易延迟。 Hitachi Vantara和Hammerspace等伙伴关係提供自动分类和迁移功能,可维护元资料的完整性,最大限度地减少重构遗留应用程式的麻烦。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场状况

- 市场概况

- 市场驱动因素

- 数位资料的爆炸性成长

- 快速过渡到 SSD 和 NVMe 架构

- 需要超低延迟的 AI/ML 工作负载

- 欧盟企业采用混合多重云端

- 边缘运算和5G微资料中心的兴起

- 欧盟Gaia-X和资料法支援主权云端存储

- 市场限制

- 全快闪和 NVMe 阵列的资本成本高昂

- 欧盟资料主权合规性分散

- 遗留工作负载迁移和供应商锁定的风险

- NAND/SSD稀土元素和关键金属的供应限制

- 价值链分析

- 监管格局

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 评估宏观经济趋势对市场的影响

第五章市场规模及成长预测

- 按储存系统

- 直接附加储存(DAS)

- 网路附加储存 (NAS)

- 储存区域网路(SAN)

- 融合式基础架构(HCI)

- 其他的

- 依储存架构

- 物件式的存储

- 区块储存

- 软体定义储存 (SDS)

- 按记忆体和媒体类型

- 硬碟机 (HDD)

- NAND快闪记忆体

- NVMe

- 3D XPoint/Optan

- 新兴NVM

- 按最终用户产业

- BFSI

- 零售与电子商务

- 资讯科技和通讯

- 医疗保健和生命科学

- 媒体和娱乐

- 政府和国防

- 其他最终用户产业

- 按国家

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 其他欧洲地区

第六章 竞争态势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Dell Technologies

- Hewlett Packard Enterprise(HPE)

- NetApp

- Hitachi Vantara

- IBM

- Toshiba

- Pure Storage

- DataDirect Networks(DDN)

- Scality

- Fujitsu

- Netgear

- Huawei Technologies

- Samsung Electronics

- Western Digital

- Seagate Technology

- Micron Technology

- Lenovo

- Cisco Systems

- Oracle

- VAST Data

第七章 市场机会与未来展望

The Europe next generation storage market size reached USD 15.47 billion in 2025 and is forecast to advance at a 10.6% CAGR to USD 25.64 billion by 2030.

Sustained growth is anchored in the EU Data Act, which comes into force in September 2025 and compels providers to enable effortless cloud switching; enterprises are therefore prioritizing portable, software-defined storage that safeguards data sovereignty. At the same time, AI training and inference workloads are multiplying storage traffic while energy-efficiency rules tighten, giving an edge to flash-based architectures that deliver low latency per watt. Capacity constraints in Frankfurt, London, Amsterdam, Paris and Dublin are pushing operators toward edge deployments, and continued investment in sovereign-cloud projects such as Gaia-X and virt8ra is stimulating demand for interoperable, vendor-agnostic platforms able to span core, cloud and edge footprints. Competitive pressure is intensifying as traditional array vendors recalibrate their portfolios to confront hyperscale cloud innovation, flash-only specialists, and European sovereign-cloud providers.

Europe Next Generation Storage Market Trends and Insights

Exploding Volume of Digital Data

Global data creation is set to triple between 2023 and 2028, and local retention obligations under GDPR mean most of that growth must be stored inside EU borders. Enterprises planning for petabyte-scale capacity are therefore deploying hybrid topologies that couple on-premises arrays with sovereign-cloud extensions, ensuring compliance while keeping latency in check. Spending patterns show a marked tilt toward scalable, software-defined platforms that can ingest diverse file and object workloads without vendor lock-in. The result is a Europe next generation storage market whose expansion rate outpaces global averages as organizations attempt to blend compliance and performance within a single architecture.

Rapid Shift to SSD and NVMe Architectures

Enterprise adoption of PCIe Gen5 NVMe is eliminating the performance gap that once separated on-premises arrays from public-cloud tiers. German manufacturing plants embracing Industry 4.0 have pushed latency budgets below 100 µs, a threshold unattainable for spinning disks. Energy efficiency is now a board-level metric; SSDs consume markedly fewer kilowatt-hours per terabyte than HDDs, helping operators meet the German Energy Efficiency Act's 50% renewable-energy threshold for data centres set for 2027. These dynamics position flash media as a strategic rather than tactical investment across the Europe next generation storage industry.

High Capital Cost of All-Flash and NVMe Arrays

Enterprise SSDs still carry a unit-cost premium as high as 9.9X over HDD capacity. For small and midsize firms, this delta complicates ROI calculations even when flash energy savings are factored in. Hyperscaler uptake is driving near-term price easing, but many European SMEs will continue staging workloads on hybrid tiers that mix QLC flash with high-capacity disk until flash crosses the cost-per-bit threshold.

Other drivers and restraints analyzed in the detailed report include:

- AI / ML Workloads Demanding Ultra-Low Latency

- Hybrid Multi-Cloud Adoption Across EU Enterprises

- Data-Sovereignty Compliance Fragmentation Across EU

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Direct-Attached Storage contributed 45.6% share to Europe next generation storage market size in 2024, underscoring enterprises' preference for predictable latency in mission-critical workloads. Hyper-Converged Infrastructure, however, is forecast to log an 11.6% CAGR, reflecting appetite for scale-out nodes that blend compute, storage and networking into a single policy domain.

Momentum toward hyperconvergence is reinforced by national digitalisation grants in Germany, where manufacturers need on-site processing to analyse sensor data without violating sovereignty rules. Dell Technologies and CoreWeave's rack-level AI platform demonstrates how converged resources can supply 1.4 exaFLOPS alongside petabyte-scale flash, making them an attractive middle ground between monolithic arrays and purely public-cloud tiers.

File and Object-Based Storage captured 65.7% of Europe next generation storage market share in 2024 by delivering RESTful, scale-out repositories for unstructured datasets, from analytics logs to 8K media files. Software-Defined Storage is scaling faster at 12.1% CAGR because it uncouples services from hardware, thereby fulfilling the Data Act's portability ethos.

European banks and insurers are piloting data-mobility orchestrators capable of live-migrating petabyte datasets between sovereign-cloud partners without disrupting transaction latency. Partnerships such as Hitachi Vantara and Hammerspace provide automated classification and movement that preserve metadata integrity, minimizing refactoring pain for legacy apps.

The Europe Next Generation Storage Market Report is Segmented by Storage System (Direct-Attached Storage (DAS), Network-Attached Storage (NAS), and More), Storage Architecture (File and Object-Based Storage, Block Storage, and More), Memory and Media Type (Hard Disk Drive (HDD), NAND Flash, and More), End-User Industry (BFSI, Retail and E-Commerce, and More), and Country. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Dell Technologies

- Hewlett Packard Enterprise (HPE)

- NetApp

- Hitachi Vantara

- IBM

- Toshiba

- Pure Storage

- DataDirect Networks (DDN)

- Scality

- Fujitsu

- Netgear

- Huawei Technologies

- Samsung Electronics

- Western Digital

- Seagate Technology

- Micron Technology

- Lenovo

- Cisco Systems

- Oracle

- VAST Data

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Exploding volume of digital data

- 4.2.2 Rapid shift to SSD and NVMe architectures

- 4.2.3 AI / ML workloads demanding ultra-low latency

- 4.2.4 Hybrid multi-cloud adoption across EU enterprises

- 4.2.5 Edge-computing and 5G micro-data-centre proliferation

- 4.2.6 EU Gaia-X and Data Act enabling sovereign-cloud storage

- 4.3 Market Restraints

- 4.3.1 High capital cost of all-flash and NVMe arrays

- 4.3.2 Data-sovereignty compliance fragmentation across EU

- 4.3.3 Legacy workload migration and vendor lock-in risks

- 4.3.4 Rare-earth and critical-metal supply constraints for NAND/SSD

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assessment of the Impact of Macroeconomic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Storage System

- 5.1.1 Direct-Attached Storage (DAS)

- 5.1.2 Network-Attached Storage (NAS)

- 5.1.3 Storage Area Network (SAN)

- 5.1.4 Hyper-Converged Infrastructure (HCI)

- 5.1.5 Others

- 5.2 By Storage Architecture

- 5.2.1 File and Object-Based Storage

- 5.2.2 Block Storage

- 5.2.3 Software-Defined Storage (SDS)

- 5.3 By Memory and Media Type

- 5.3.1 Hard Disk Drive (HDD)

- 5.3.2 NAND Flash

- 5.3.3 NVMe

- 5.3.4 3D XPoint / Optane

- 5.3.5 Emerging NVM

- 5.4 By End-User Industry

- 5.4.1 BFSI

- 5.4.2 Retail and e-Commerce

- 5.4.3 IT and Telecom

- 5.4.4 Healthcare and Life Sciences

- 5.4.5 Media and Entertainment

- 5.4.6 Government and Defence

- 5.4.7 Other End-User Industries

- 5.5 By Country

- 5.5.1 Germany

- 5.5.2 United Kingdom

- 5.5.3 France

- 5.5.4 Italy

- 5.5.5 Spain

- 5.5.6 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Dell Technologies

- 6.4.2 Hewlett Packard Enterprise (HPE)

- 6.4.3 NetApp

- 6.4.4 Hitachi Vantara

- 6.4.5 IBM

- 6.4.6 Toshiba

- 6.4.7 Pure Storage

- 6.4.8 DataDirect Networks (DDN)

- 6.4.9 Scality

- 6.4.10 Fujitsu

- 6.4.11 Netgear

- 6.4.12 Huawei Technologies

- 6.4.13 Samsung Electronics

- 6.4.14 Western Digital

- 6.4.15 Seagate Technology

- 6.4.16 Micron Technology

- 6.4.17 Lenovo

- 6.4.18 Cisco Systems

- 6.4.19 Oracle

- 6.4.20 VAST Data

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

新一代资料储存市场(按储存媒体、部署模型、储存架构、应用、最终用户产业和服务类型)-2025-2032 年全球预测

新一代资料储存市场(按储存媒体、部署模型、储存架构、应用、最终用户产业和服务类型)-2025-2032 年全球预测 2025年太空资料储存全球市场报告

2025年太空资料储存全球市场报告 下一代资料储存市场:2025 年至 2030 年的未来预测

下一代资料储存市场:2025 年至 2030 年的未来预测 2025-2029年全球AI优化储存市场2025年下一代资料储存全球市场报告

2025-2029年全球AI优化储存市场2025年下一代资料储存全球市场报告 下一代储存:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)亚太地区下一代储存:市场占有率分析、产业趋势和成长预测(2025-2030 年)北美下一代储存:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)

下一代储存:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)亚太地区下一代储存:市场占有率分析、产业趋势和成长预测(2025-2030 年)北美下一代储存:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年) 下一代资料储存市场规模、份额、成长分析(按储存系统、储存媒体、地区)- 产业预测,2024-2031 年

下一代资料储存市场规模、份额、成长分析(按储存系统、储存媒体、地区)- 产业预测,2024-2031 年 新一代资料储存技术市场 - 按类型、解决方案、记忆体、地区和竞争细分的全球产业规模、份额、趋势、机会和预测,2019-2029 年

新一代资料储存技术市场 - 按类型、解决方案、记忆体、地区和竞争细分的全球产业规模、份额、趋势、机会和预测,2019-2029 年