|

市场调查报告书

商品编码

1850115

南美作物保护:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)South America Agrochemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

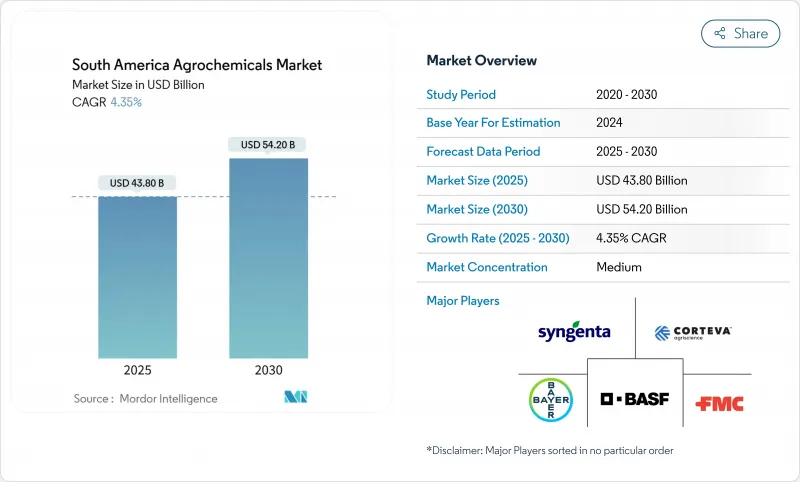

预计到 2025 年,南美洲作物保护市场价值将达到 438 亿美元,到 2030 年将达到 542 亿美元,在市场估算和预测期内的复合年增长率为 4.35%。

该地区的扩张主要得益于其在大豆、玉米和特色园艺领域的领先地位,以及生物技术作物、精准施药工具的日益普及和向生物解决方案的快速转型。巴西保持着国内市场的领先地位,而南美其他地区则正经历着最快的成长,这得益于其向高价值作物和现代投入体系的多元化发展。化学肥料占据主导地位,反映了土壤养分匮乏的现状,而助剂则因精准施药和生物化学整合而迅速增长。市场竞争异常激烈,前四大供应商占据了大部分市场份额,但大量生物技术新兴企业和数位平台的涌现正在重塑市场格局。儘管长期种植面积的扩大和对碳排放相关投入品的需求推动了南美农化市场的发展机会,但外汇波动、更严格的农药残留法规和物流缺口仍然抑制着短期内的增长势头。

南美洲作物保育市场趋势与洞察

基因改造作物增加了对农药的需求

阿根廷在2024年核准了五种生物技术作物,将核准简化为六个月週期,巩固了其作为全球第三大生物技术作物种植国的地位,种植面积达2500万公顷。巴西的Intacta2 Xtend性状已覆盖该国30%的大豆种植面积,刺激了对Glyphosate、麦草畏和草铵膦组合除草剂的需求。阿根廷HB4耐旱小麦的商业化正在推动针对新型除草剂耐受性组合的配套作物保护配方的发展。生物技术在全部区域的发展迫使农业化学品供应商设计轮作方案,以最大限度地提高产量并降低抗药性。因此,产品组合增强了投入品的特许权使用费,提高了每公顷的终身价值,并巩固了南美洲农业化学品市场的高端地位。

用于优化药物利用的精准农业平台

巴西拥有875家提供农业解决方案的深度科技公司,涵盖人工智慧机器人、微生物学和遥感探测领域。 Solinftec公司的太阳能机器人SOLIX能够自主巡田,识别杂草并建议精准喷洒,在保持产量的同时减少除草剂的使用。先正达的CROPWISE人工智慧平台已绘製了7000万公顷的地图,并将养分、病虫害和天气资料集中起来,用于指导性田间规划。高光谱遥测感测器现在可以即时预测氮钾含量,从而实现变数施肥和稳定剂的施用,减少径流。儘管实施成本仍然很高,但劳动力短缺和投入品价格上涨正促使农民寻求技术驱动的效率提升方案。这些工具加强了作物健康状况与投入需求之间的回馈循环,从而维持了农业化学品市场对优质添加剂、微量元素和生物刺激剂的需求。

重新登记及加强残留物法规

智利第47/2024号法令将于2025年5月生效,该法令加强了残留限量,提高了配方商和出口商的合规成本。巴西修订后的农药法加快了审批速度,同时加强了环境监管,给小型註册商带来了挑战。秘鲁继续批准在欧洲被禁用的农药,破坏了安第斯贸易路线沿线的监管一致性。巴西大豆病害菌株中杀菌剂抗性的蔓延也迫使当局重新评估作用机制轮换要求。这些措施加在一起,增加了数据生产成本,延长了市场准入时间,并可能延迟新进入者的活动,对处于转型期的南美农药市场造成了压力。

细分市场分析

2024年,化肥占据了南美农业化学品市场42%的份额,这主要得益于热带土壤养分贫瘠以及提高油籽产量的战略倡议,尤其是在巴西,种植者每公顷在化肥上的投入高达335美元。作物保护产品仍是第二大类别,其主要驱动因素是湿润气候下持续存在的杂草和病虫害问题,以及基因改造作物对除草剂产生抗药性。

助剂市场发展迅猛,预计到2030年复合年增长率将达到6.0%,这得益于可优化液滴大小并减少漂移的数位化喷雾图。如今,产品创新主要围绕着整合包装。 ICL在收购Nitro1000和Orion双线FA1500施用器后推出固氮接种剂,显示化学和生物製剂可以同时使用,呈现融合趋势。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 市场概览

- 市场驱动因素

- 基因改造作物增加了对农药的需求

- 扩大大豆和玉米的种植面积

- 为农业投入品提供农村信贷补贴

- 与碳信用挂钩的高效肥料的兴起

- 生物作物保护混合物的使用

- 精密农业平台,优化化学品施用

- 市场限制

- 重新登记并加强残留标准

- 商品价格波动会抑制支出

- 进口流量中的内陆物流瓶颈

- 除草剂抗药性增加,转换成本上升

- 技术展望

- 监管环境

- 波特五力分析

- 供应商的议价能力

- 买方/消费者的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场区隔

- 依产品类型

- 肥料

- 氮

- 磷酸

- 钾

- 特殊肥料

- 杀虫剂

- 除草剂

- 杀虫剂

- 消毒剂

- 生物农药

- 佐剂

- 植物生长调节剂

- 肥料

- 透过使用

- 农作物

- 粮食

- 豆类和油籽

- 水果和蔬菜

- 非农作物类

- 草坪和观赏草

- 其他非农作物类

- 农作物

- 按地区

- 巴西

- 阿根廷

- 其他南美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Syngenta

- Bayer Crop Science

- BASF SE

- Corteva Agriscience

- Nutrien Ltd

- FMC Corporation

- Yara International ASA

- UPL Limited

- Sumitomo Chemical Co., Ltd.

- ICL Group Ltd.

第七章 市场机会与未来展望

The South America Agrochemicals Market size is estimated at USD 43.80 billion in 2025, and is anticipated to reach USD 54.20 billion by 2030, at a CAGR of 4.35% during the forecast period.

Expansion rests on the region's leadership in soybean, corn, and specialty horticulture, reinforced by rising genetically modified crop adoption, precision-application tools, and a rapid shift toward biological solutions. Brazil retains the largest national position and the rest of South America is delivering the fastest growth as they diversify into high-value crops and modern input systems. Fertilizers dominate, reflecting nutrient-depleted soils, while adjuvants post the quickest gains on the back of precision spraying and biological-chemical integration. Competitive intensity is high because the top four suppliers hold the majority share, though a wave of biological start-ups and digital platforms is recalibrating power balances across the South America agrochemicals market. Currency swings, tighter residue rules, and logistics gaps still temper near-term momentum even as long-run acreage expansion and carbon-linked input demand lift the opportunity curve of the South America agrochemicals market.

South America Agrochemicals Market Trends and Insights

GM-crop driven pesticide demand surge

Argentina cleared five new genetically engineered crops in 2024, streamlining approvals to six-month cycles and reinforcing its status as the world's third-largest GM grower with 25 million hectares . Brazil's Intacta2 Xtend trait already spans 30% of national soybean acreage and stimulates demand for herbicide stacks that combine glyphosate, dicamba, and glufosinate. HB4 drought-tolerant wheat commercialized in Argentina is boosting complementary crop-protection formulations tailored for novel herbicide-tolerance packages. Region-wide, biotech expansion pushes agrochemical suppliers to design rotation programs, mitigating resistance while maximizing yield gains. The resulting product bundles strengthen input loyalty, enlarge lifetime value per hectare, and reinforce the premium tier of the South America agrochemicals market.

Precision-ag platforms optimizing chemical rates

Brazil hosts 875 deep-tech firms with agricultural solutions, including AI robotics, microbiology, and remote sensing. Solinftec's solar-powered SOLIX robot autonomously scouts fields to identify weeds and recommends surgical spraying, cutting herbicide volumes while preserving yields. Syngenta's CROPWISE AI platform already maps 70 million ha, centralizing nutrient, pest, and weather data for prescriptive field plans. Hyperspectral sensors now predict nitrogen and potassium levels in real-time, allowing variable-rate fertilizer and stabilizer placement that curbs runoff. Adoption cost hurdles persist, yet mounting labor shortages and input price spikes push growers toward tech-enabled efficiency. These tools tighten the feedback loop between crop status and input need, sustaining the consumption of premium-grade adjuvants, micronutrients, and bio-stimulants within the South America agrochemicals market.

Tighter re-registration and residue limits

Chile imposed stricter maximum residue limits through Decree 47/2024, effective May 2025, raising compliance costs for formulators and exporters. Brazil's updated pesticide law accelerates approvals yet heightens environmental oversight, challenging small registrants. Peru continues to authorize chemistries banned in Europe, fracturing regulatory alignment across Andean trade routes. Wider fungicide resistance in Brazilian soybean pathotypes also presses authorities to revise mode-of-action rotation mandates. Together, these measures lift data-generation expenses, extend market-entry timelines, and may delay newer activities, weighing on the South America agrochemicals market during the transition period.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of soybean and corn acreage

- Biological crop-protection blends adoption

- Commodity-price volatility curbing spend

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fertilizers secured a 42% share of the South America agrochemicals market in 2024, underpinned by nutrient-poor tropical soils and a strategic push to lift oilseed yields, especially in Brazil, where growers spend USD 335/hectare on fertilizer inputs. Pesticides remain the second-largest category, driven by persistent weed and pest pressure in humid climates and by widening herbicide-tolerance stacks in GM crops.

Adjuvants exhibit the fastest trajectory at a 6.0% CAGR through 2030, benefiting from digital spray maps that reward droplet-size optimization and drift reduction. Product innovation now revolves around integrated packages. ICL's launch of nitrogen-fixing inoculants after acquiring Nitro 1000 and Orion's dual-line FA 1500 applicator, able to deliver chemical and biological inputs concurrently, illustrates the convergence trend.

The South America Agrochemicals Market Report is Segmented by Product Type (Fertilizers, Pesticides, and More), by Application (Crop-Based and Non-Crop-Based), and Geography (Brazil, Argentina, and Rest of South America). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Syngenta

- Bayer Crop Science

- BASF SE

- Corteva Agriscience

- Nutrien Ltd

- FMC Corporation

- Yara International ASA

- UPL Limited

- Sumitomo Chemical Co., Ltd.

- ICL Group Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 GM-crop driven pesticide demand surge

- 4.2.2 Expansion of soybean and corn acreage

- 4.2.3 Subsidized rural credit for agri-inputs

- 4.2.4 Rise of carbon-credit-linked efficiency fertilizers

- 4.2.5 Biological crop-protection blends adoption

- 4.2.6 Precision-ag platforms optimizing chemical rates

- 4.3 Market Restraints

- 4.3.1 Tighter re-registration and residue limits

- 4.3.2 Commodity-price volatility curbing spend

- 4.3.3 Inland logistics bottlenecks on import flows

- 4.3.4 Herbicide resistance escalating switch costs

- 4.4 Technological Outlook

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Force Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Product Type

- 5.1.1 Fertilizers

- 5.1.1.1 Nitrogenous

- 5.1.1.2 Phosphatic

- 5.1.1.3 Potassic

- 5.1.1.4 Specialty Fertilizers

- 5.1.2 Pesticides

- 5.1.2.1 Herbicides

- 5.1.2.2 Insecticides

- 5.1.2.3 Fungicides

- 5.1.2.4 Bio-pesticides

- 5.1.3 Adjuvants

- 5.1.4 Plant Growth Regulators

- 5.1.1 Fertilizers

- 5.2 Application

- 5.2.1 Crop Based

- 5.2.1.1 Grains and Cereals

- 5.2.1.2 Pulses and Oilseeds

- 5.2.1.3 Fruits and Vegetables

- 5.2.2 Non-Crop Based

- 5.2.2.1 Turf and Ornamental Grass

- 5.2.2.2 Other Non-crop Based

- 5.2.1 Crop Based

- 5.3 Geography

- 5.3.1 Brazil

- 5.3.2 Argentina

- 5.3.3 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Syngenta

- 6.4.2 Bayer Crop Science

- 6.4.3 BASF SE

- 6.4.4 Corteva Agriscience

- 6.4.5 Nutrien Ltd

- 6.4.6 FMC Corporation

- 6.4.7 Yara International ASA

- 6.4.8 UPL Limited

- 6.4.9 Sumitomo Chemical Co., Ltd.

- 6.4.10 ICL Group Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

农药市场:全球市场按产品类型、性质、作物类型、配方和应用进行预测 - 2026-2032年农药储槽市场:2026-2032年全球市场预测(依储槽类型、材质、容量、运作模式、压力类型、移动性、应用、最终用户和通路划分)

农药市场:全球市场按产品类型、性质、作物类型、配方和应用进行预测 - 2026-2032年农药储槽市场:2026-2032年全球市场预测(依储槽类型、材质、容量、运作模式、压力类型、移动性、应用、最终用户和通路划分) 2026年全球农药市场报告氟嘧啶市场:2026-2032年全球市场预测(按剂型、作物类型、施用方法、分销管道和最终用户划分)

2026年全球农药市场报告氟嘧啶市场:2026-2032年全球市场预测(按剂型、作物类型、施用方法、分销管道和最终用户划分) 铜肥市场规模、份额和成长分析:按产品类型、配方类型、应用类型、最终用户和地区划分 - 2026-2033 年产业预测

铜肥市场规模、份额和成长分析:按产品类型、配方类型、应用类型、最终用户和地区划分 - 2026-2033 年产业预测 作物保护市场分析及预测(至2035年):依类型、产品类型、应用、技术、形式、最终用户、服务、实施类型、功能及解决方案划分

作物保护市场分析及预测(至2035年):依类型、产品类型、应用、技术、形式、最终用户、服务、实施类型、功能及解决方案划分 全球农业化学品市场规模、份额、趋势和成长分析报告(2026-2034年)

全球农业化学品市场规模、份额、趋势和成长分析报告(2026-2034年) 特种作物保护解决方案市场,全球预测至2034年:依产品类型、作物类型、配方、应用和地区划分2026年全球滷代农药市场报告农药储槽市场-2026-2031年预测

特种作物保护解决方案市场,全球预测至2034年:依产品类型、作物类型、配方、应用和地区划分2026年全球滷代农药市场报告农药储槽市场-2026-2031年预测