|

市场调查报告书

商品编码

1850209

作物保护:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)Agrochemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

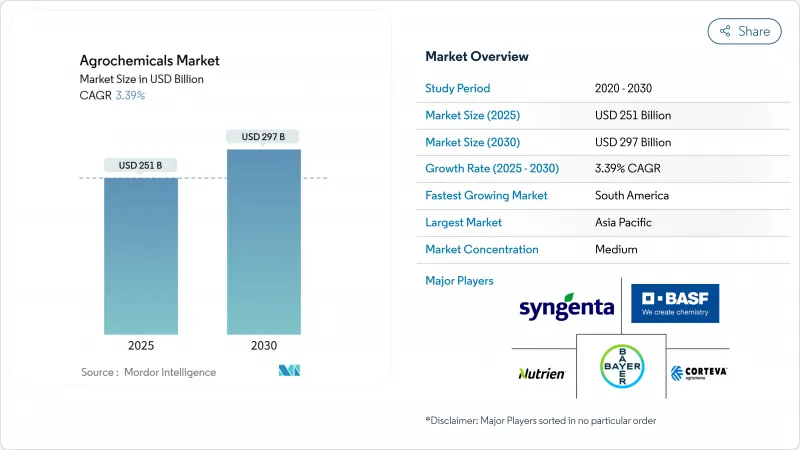

预计到 2025 年,农业化学品市场规模将达到 2,510 亿美元,到 2030 年将成长至 2,970 亿美元,复合年增长率高达 3.39%。

成长的驱动力来自粮食大国持续的化肥需求、生物农作物保护产品的快速普及以及提高投入利用效率的精密农业工具的广泛应用。同时,欧盟的「从农场到餐桌」指令要求到2030年将化学农药的使用量减半,中国定期限制化肥出口,以及主要进口市场日益严格的残留物监管,都迫使种植者加快产品组合的转型,转向毒性更低的化学品和数位化咨询服务。生物製药正迅速扩大规模,这得益于目前30个国家实施的农药税收制度以及巴西和印度简化的註册流程;而具有全新作用机制的高端除草剂则有助于应对高成本抗性杂草的出现。随着学名药蚕食成熟药物的利润空间,以及新的「投入即服务」模式鼓励基于效果而非数量的定价,竞争日益激烈,这预示着未来十年农化市场将以技术整合和永续性为特征。

全球作物保护市场趋势与洞察

抗除草剂杂草的增加刺激了对优质除草剂的需求

目前,全球超过2.7亿英亩的土地受到抗除草剂杂草的侵袭,促使种植者寻求具有全新作用机制的优质除草剂。 FMC公司的Dodirex Active是30年来首个采用全新作用机制的除草剂,首次在秘鲁註册,专门用于防治水稻田中的抗性禾本科杂草,预计将于2025年8月上市。美国环保署(EPA)的2024年抗性管理架构强化了杂草综合管理通讯协定,并为创新配方提供了监管支援。住友化学公司在阿根廷註册的Rapidisil,协助犁地系统的发展,并争取实现每年1000亿日圆(约6.5亿美元)的保护性犁地除草剂销售额。由于抗性杂草每年在全球整体造成超过150亿美元的产量损失,种植者仍愿意为此支付高价。

整合人工智慧驱动的输入即服务经营模式

数位农业平台正在取代传统的仅销售产品的分销模式,将农艺咨询、变数配方和基于效果的保证捆绑在一起。拜耳的 CROPWISE 平台目前整合了田间感测器、气象资料和卫星影像,以优化喷洒和施肥计画。BASF和 Agmatix 正在应用机器学习诊断技术,在大豆胞囊线虫出现明显症状之前检测出其胁迫,从而保护产量并减少化学物质用量。先正达和 Taranis 的合作计画为零售商提供人工智慧驱动的田间巡查服务,指导他们进行精准的投入,并将一次性销售转化为持续收入。这些服务可以将每英亩化学品用量减少高达 20%,使农化市场在盈利和永续性目标之间取得平衡。

加速欧盟、巴西和中国淘汰剧毒农药的步伐

监管机构正在缩短被认定为有毒活性成分的宽限期,迫使製造商减记库存并加快产品改进进程。欧盟最新提案将禁止在敏感栖息地使用某些有机磷酸盐,而巴西将核准标准与欧盟接轨,并计划在2026年前淘汰约200种遗留分子。BASF于2024年关闭了其草铵膦工厂,并累计了与监管收紧预期相关的减损损失。中国的政策优先发展低毒杀菌剂和生物农药,预计2025年,商业化产量将达到9万吨。

细分市场分析

到2024年,化肥将占作物保护市场收入的46.0%,这反映了其在为谷物和油籽提供大量营养元素方面发挥的关键作用。然而,天然气价格的波动推高了氨的成本,挤压了氮肥生产商的利润空间,这预示着市场将转向高效技术,例如尿素酶抑製剂和控制释放被覆剂可在不影响产量的情况下将施用量降低15-25%。由于新兴经济体的施用量趋于稳定,化肥作物保护市场规模的复合年增长率将低于整体市场,仅2.3%。因此,种植者优先考虑那些除了产量之外还能带来额外价值的产品,例如优质聚合物包衣产品和与碳信用额度挂钩的产品。

生物製剂领域(包括微生物製剂、植物製剂、费洛蒙製剂和生化产品)预计在2024年将成长14.7%,到2030年达到250亿美元。在该领域中,生物杀虫剂市场预计将以15.2%的复合年增长率成长,这主要得益于欧洲更严格的残留物法规和巴西的快速审批程序。因此,综合虫害管理方案越来越多地采用化学和生物防治方法轮换,这使得供应商能够交叉销售其专有菌株和添加剂。先正达生物製品公司和富美实公司等领导企业正积极聚焦这一领域,并加速併购以填补其产品组合的空白。除草剂、杀菌剂、添加剂和植物生长调节剂仍然很重要,但随着生物製药蚕食部分销售量并占据更高的利润率,它们在农药市场中的总份额预计将略有下降。

区域分析

亚太地区将在2024年维持最高的收入,占农业化学品市场的48.5%。中国生产全球50%的活性成分,但国内环境法规目前优先考虑低毒性产品线,刺激了对生物农药产能的投资。印度的合约开发和受託製造公司已获得多年期合约,填补了西方产品线的空白,推动了两位数的销售成长。日本将加快采用控制释放肥料以实现排放目标,而澳洲将平衡肥料需求与应对气候变迁导致的干旱。数位土壤检测和政府补贴计画将促进均衡营养,从而强化基本的消费模式。

南美洲是成长最快的地区,预计到2030年将以4.4%的复合年增长率成长。巴西的生物技术市场预计到2024年将达到50亿雷亚尔(10亿美元),主要集中在大豆和棉花领域。物流瓶颈依然存在,巴西62%的农用道路品质欠佳,推高了成本,促使製剂厂更加区域化。阿根廷的犁地面积超过90%,支撑了对Rapidicil等残留型除草剂的需求。气候变化,特别是干旱,正在推动微量元素和节水产品的销售,为农业化学品市场的适应性技术创造了稳健的商业前景。

儘管北美和欧洲农业发展日趋成熟,但它们仍然是创新中心。美国正在反对对加拿大钾肥提案关税,该关税可能使农场成本每吨增加100美元,促使人们对生物氮替代和钾溶解微生物产生了兴趣。加拿大正在推广4R营养管理认证,将贷款机构的奖励与最佳肥料使用实践挂钩。欧洲的「从农场到餐桌」策略要求到2030年将农药使用量减少50%,并推动加速生物认证和数位化可追溯性系统的建置。中东和非洲在较小的基数上分别成长了3.4%和4.1%,这主要得益于主权粮食安全投资、水耕技术的普及以及再生沙漠农业实践。总而言之,这些动态表明,农业化学品市场正保持着适度的销售成长轨迹,并辅以高价值产品的替代品。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 抗除草剂杂草的增加推动了对优质除草剂的需求

- 整合人工智慧驱动的输入即服务经营模式

- 由于农药税收制度,生技药品迅速成长。

- 氮高效利用产品的碳信用货币化

- 缓释肥料正逐渐成为主流

- 垂直和室内农场的作物多样化

- 市场限制

- 加速欧盟、巴西和中国淘汰高毒性活性物质的进程

- Glyphosate价格波动挤压生产商利润

- 监管资料包成本不断上涨

- 北美地区长期有激进诉讼风险

- 监管环境

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 依产品类型

- 肥料

- 氮

- 磷酸

- 钾

- 杀虫剂

- 除草剂

- 杀虫剂

- 消毒剂

- 生物农药

- 佐剂

- 植物生长调节剂

- 肥料

- 透过使用

- 农作物

- 粮食

- 豆类和油籽

- 水果和蔬菜

- 非农作物类

- 草坪和观赏草

- 其他非农作物类

- 农作物

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 北美其他地区

- 欧洲

- 德国

- 法国

- 英国

- 义大利

- 西班牙

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 亚太其他地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 其他中东地区

- 非洲

- 南非

- 埃及

- 其他非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Syngenta Group

- Bayer Crop Science AG

- BASF Agricultural Solutions

- Corteva Agriscience

- Nutrien Ltd

- Yara International ASA

- Mosaic Company

- CF Industries Holdings

- UPL Ltd

- FMC Corporation

- Sumitomo Chemical AgroSolutions

- Nufarm Ltd

- K+S AG

- ICL Group

- OCP Group

- Albaugh LLC

- OCI Global

- RovensaNext

- Bharat Rasayan Ltd

- Helm AG

第七章 市场机会与未来展望

The agrochemicals market reached USD 251 billion in 2025 and is forecast to rise to USD 297 billion by 2030, translating into a steady 3.39% CAGR.

Growth is supported by sustained fertilizer demand in large grain economies, rapid penetration of biological crop-protection products, and wider deployment of precision-agriculture tools that lift input-use efficiency. At the same time, the European Union's Farm to Fork mandate to halve chemical pesticide use by 2030, China's periodic fertilizer export curbs, and increasingly stringent residue limits in major import markets are forcing producers to accelerate portfolio shifts toward low-toxicity chemistries and digital advisory services. Biologicals are scaling quickly on the back of pesticide-tax regimes now active in 30 countries and streamlined Brazilian and Indian registration pathways, while premium herbicides with novel modes of action address the costly rise of resistant weeds. Competitive intensity is growing as generics erode margins on mature molecules and new "input-as-a-service" models reward outcome-based pricing over product volume, setting the stage for a decade defined by technology integration and sustainability credentials within the agrochemicals market.

Global Agrochemicals Market Trends and Insights

Escalating Herbicide-Resistant Weeds Spur Premium Herbicide Demand

Herbicide-resistant weeds now infest more than 270 million acres worldwide, pushing growers toward premium actives that deliver novel modes of action. FMC's Dodhylex active, the first new herbicide mode in three decades, secured its inaugural registration in Peru and targets resistant grass weeds in rice, with a commercial launch slated for August 2025. The United States Environmental Protection Agency's 2024 resistance-management framework reinforces integrated weed-management protocols, giving regulatory support to innovative formulations. Sumitomo Chemical's Rapidicil registration in Argentina underpins the competitive race to serve no-till systems, aiming for JPY 100 billion (USD 0.65 billion) in annual sales from conservation-tillage herbicides. Growers' willingness to pay remains strong because resistant weeds impose yearly global yield losses above USD 15 billion.

Convergence of AI-Enabled Input-as-a-Service Business Models

Digital farming platforms are displacing traditional product-only distribution by bundling agronomic advice, variable-rate prescriptions, and outcome-based guarantees. Bayer's CROPWISE platform now integrates field sensors, weather data, and satellite imagery to fine-tune spraying and fertilizing schedules. BASF and Agmatix apply machine-learning diagnostics to detect soybean cyst nematode stress before visual symptoms appear, protecting yields while cutting chemical load. Syngenta's tie-up with Taranis equips retailers with AI-powered scouting to drive precise input placement, converting one-time sales into subscription revenue. These services reduce chemical intensity per acre by up to 20%, aligning profitability with sustainability imperatives in the agrochemicals market.

Accelerating Phase-Outs of High-Toxicity Actives in EU, Brazil, and China

Regulators are shortening grace periods for active ingredients flagged for toxicity, forcing manufacturers to write off inventory and accelerate reformulation pipelines. The European Union's latest proposal eliminates certain organophosphates from sensitive habitats, while Brazil aligns approval criteria with the EU, removing nearly 200 legacy molecules by 2026. BASF shuttered its glufosinate plant in 2024, booking impairment charges linked to the tighter regulatory outlook. Chinese policies prioritize low-toxicity fungicides and biopesticides, expecting commercial volumes of 90,000 metric tons by 2025.

Other drivers and restraints analyzed in the detailed report include:

- Surge in Biologicals Pushed by Pesticide-Tax Regimes

- Carbon-Credit Monetization of Nitrogen-Efficiency Products

- Volatile Glyphosate Pricing Squeezes Formulator Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fertilizers accounted for 46.0% of 2024 revenue inside the agrochemicals market, reflecting their indispensable role in macronutrient delivery to grains and oilseeds. Yet volatile natural gas prices inflated ammonia costs, squeezing margins for nitrogen producers and signaling a pivot toward efficiency technologies such as urease inhibitors and controlled-release coatings that reduce application rates by 15-25% without yield loss. The agrochemicals market size for fertilizers is forecast to expand at just 2.3% CAGR, slower than the overall market because of plateauing application rates in developed economies. Producers, therefore, emphasize premium polymer-coated lines and carbon-credit-linked offerings that capture value beyond volume.

The biological segment, encompassing microbials, botanicals, pheromones, and biochemicals, grew 14.7% in 2024 and is projected to reach USD 25 billion by 2030. Within that total, the agrochemicals market size for bio-insecticides is on track to advance at 15.2% CAGR, buoyed by European residue-limit tightening and Brazilian fast-track registrations. As a result, integrated pest-management programs now mix chemical and biological tools in single-season rotations, enabling suppliers to cross-sell proprietary strains and adjuvants. Major players such as Syngenta Biologicals and FMC pivot aggressively toward this space, accelerating mergers and acquisitions to fill portfolio gaps. Herbicides, fungicides, adjuvants, and plant growth regulators remain critical; and their combined share of the agrochemicals market is projected to decline slightly as biologicals cannibalize volume while fetching higher margins.

The Agrochemicals Market Report is Segmented by Product Type (Fertilizers, Pesticides, Adjuvants, and Plant Growth Regulators), by Application (Crop-Based and Non-Crop-Based), and by Geography (North America, Europe, Asia-Pacific, South America, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific retained the highest regional revenue in 2024, accounting for 48.5% within the agrochemicals market, supported by intensive cultivation across China and India. China manufactures 50% of the worldwide active-ingredient output, yet domestic environmental rules now favor low-toxicity lines, stimulating investment in biopesticide capacity. India's contract development and manufacturing organizations secure multiyear deals that fill Western pipeline gaps, driving double-digit revenue growth. Japan accelerates the adoption of controlled-release fertilizers to meet emission targets, the Australia balances fertilizer demand with climate-induced drought adjustments. Government subsidy programs promoting digital soil testing and balanced nutrition enhance baseline consumption patterns.

South America is the fastest-growing territory, expanding by 4.4% CAGR through 2030. Brazil's biological market hit BRL 5 billion (USD 1 billion) in 2024, with uptake concentrated in soybean and cotton. Logistics bottlenecks persist; 62% of Brazilian agricultural roads are below optimal quality, raising costs and encouraging localized formulation plants. Argentina's no-till acreage exceeds 90%, underpinning demand for residue-compatible herbicides such as Rapidicil. Climate volatility, especially drought, boosts micronutrient and water-efficiency product sales, shaping a resilient business case for adaptive technologies within the agrochemicals market.

North America and Europe, though mature, remain innovation hubs. The United States contends with tariff proposals on Canadian potash that could raise farmer costs by USD 100 per ton, prompting interest in biological nitrogen replacement and potassium-solubilizing microbes. Canada promotes 4R nutrient-stewardship certification, linking lender incentives to fertilizer best practices. Europe's Farm to Fork strategy mandates 50% pesticide cuts by 2030, triggering accelerated biological approvals and digital traceability systems. The Middle East and Africa grew 3.4% and 4.1%, respectively, propelled by sovereign food-security investments, hydroponic adoption, and reclaimed desert farming, albeit from smaller bases. Collectively, these dynamics keep the agrochemicals market on a path of gradual volume growth complemented by higher-value product substitution.

- Syngenta Group

- Bayer Crop Science AG

- BASF Agricultural Solutions

- Corteva Agriscience

- Nutrien Ltd

- Yara International ASA

- Mosaic Company

- CF Industries Holdings

- UPL Ltd

- FMC Corporation

- Sumitomo Chemical AgroSolutions

- Nufarm Ltd

- K+S AG

- ICL Group

- OCP Group

- Albaugh LLC

- OCI Global

- RovensaNext

- Bharat Rasayan Ltd

- Helm AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Escalating herbicide-resistant weeds spur premium herbicide demand

- 4.2.2 Convergence of AI-enabled Input-as-a-service business models

- 4.2.3 Surge in biologicals pushed by pesticide-tax regimes

- 4.2.4 Carbon-credit monetization of nitrogen-efficiency products

- 4.2.5 Mainstream expansion of controlled-release fertilizers

- 4.2.6 Crop diversification in vertical and indoor farms

- 4.3 Market Restraints

- 4.3.1 Accelerating phase-outs of high-toxicity actives in EU, Brazil and China

- 4.3.2 Volatile glyphosate pricing squeezes formulator margins

- 4.3.3 Rising Regulatory data-package costs

- 4.3.4 Chronic activist litigation risk in North America

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Fertilizers

- 5.1.1.1 Nitrogenous

- 5.1.1.2 Phosphatic

- 5.1.1.3 Potassic

- 5.1.2 Pesticides

- 5.1.2.1 Herbicides

- 5.1.2.2 Insecticides

- 5.1.2.3 Fungicides

- 5.1.2.4 Bio-pesticides

- 5.1.3 Adjuvants

- 5.1.4 Plant Growth Regulators

- 5.1.1 Fertilizers

- 5.2 By Application

- 5.2.1 Crop-based

- 5.2.1.1 Grains and Cereals

- 5.2.1.2 Pulses and Oilseeds

- 5.2.1.3 Fruits and Vegetables

- 5.2.2 Non-crop-based

- 5.2.2.1 Turf and Ornamental Grass

- 5.2.2.2 Other Non-crop-based

- 5.2.1 Crop-based

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 France

- 5.3.2.3 United Kingdom

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Russia

- 5.3.2.7 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 Australia

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Rest of Middle East

- 5.3.6 Africa

- 5.3.6.1 South Africa

- 5.3.6.2 Egypt

- 5.3.6.3 Rest of Africa

- 5.3.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Syngenta Group

- 6.4.2 Bayer Crop Science AG

- 6.4.3 BASF Agricultural Solutions

- 6.4.4 Corteva Agriscience

- 6.4.5 Nutrien Ltd

- 6.4.6 Yara International ASA

- 6.4.7 Mosaic Company

- 6.4.8 CF Industries Holdings

- 6.4.9 UPL Ltd

- 6.4.10 FMC Corporation

- 6.4.11 Sumitomo Chemical AgroSolutions

- 6.4.12 Nufarm Ltd

- 6.4.13 K+S AG

- 6.4.14 ICL Group

- 6.4.15 OCP Group

- 6.4.16 Albaugh LLC

- 6.4.17 OCI Global

- 6.4.18 RovensaNext

- 6.4.19 Bharat Rasayan Ltd

- 6.4.20 Helm AG

7 Market Opportunities and Future Outlook

铜肥市场规模、份额和成长分析:按产品类型、配方类型、应用类型、最终用户和地区划分 - 2026-2033 年产业预测

铜肥市场规模、份额和成长分析:按产品类型、配方类型、应用类型、最终用户和地区划分 - 2026-2033 年产业预测 作物保护市场分析及预测(至2035年):依类型、产品类型、应用、技术、形式、最终用户、服务、实施类型、功能及解决方案划分

作物保护市场分析及预测(至2035年):依类型、产品类型、应用、技术、形式、最终用户、服务、实施类型、功能及解决方案划分 全球农业化学品市场规模、份额、趋势和成长分析报告(2026-2034年)

全球农业化学品市场规模、份额、趋势和成长分析报告(2026-2034年) 特种作物保护解决方案市场,全球预测至2034年:依产品类型、作物类型、配方、应用和地区划分

特种作物保护解决方案市场,全球预测至2034年:依产品类型、作物类型、配方、应用和地区划分 2026年全球滷代农药市场报告农药储槽市场-2026-2031年预测

2026年全球滷代农药市场报告农药储槽市场-2026-2031年预测 依运输方式、服务类型、产品类型、货柜类型、温控类型和物流所有权分類的农业化学品分销市场-2026-2032年全球预测农业烷氧基化物市场按产品类型、功能、形态、应用和分销管道划分,全球预测(2026-2032年)按剂型、作物类型、通路和应用方法分類的啶虫脒原料药市场-全球预测,2026-2032年作物保护供应商市场预测至2032年:按产品类型、作物类型、供应商类型、分销管道和地区分類的全球分析

依运输方式、服务类型、产品类型、货柜类型、温控类型和物流所有权分類的农业化学品分销市场-2026-2032年全球预测农业烷氧基化物市场按产品类型、功能、形态、应用和分销管道划分,全球预测(2026-2032年)按剂型、作物类型、通路和应用方法分類的啶虫脒原料药市场-全球预测,2026-2032年作物保护供应商市场预测至2032年:按产品类型、作物类型、供应商类型、分销管道和地区分類的全球分析