|

市场调查报告书

商品编码

1850127

软性饮料包装:市场占有率分析、产业趋势与统计、成长预测(2025-2030)Soft Drinks Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

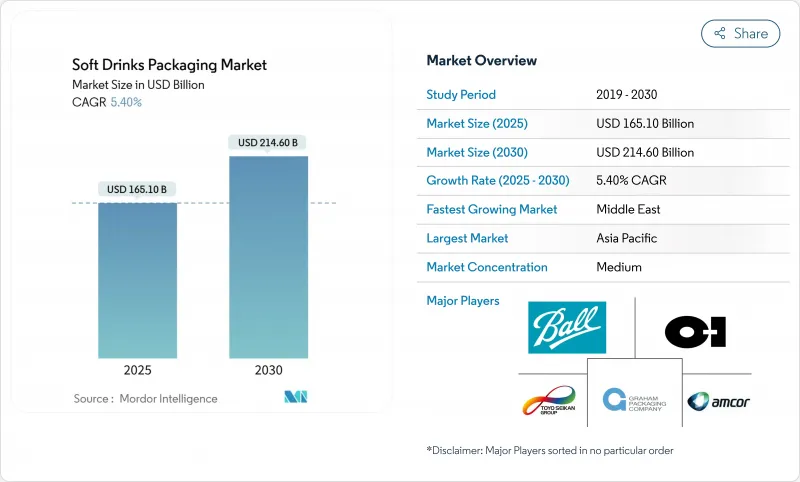

预计到 2025 年,软性饮料包装市场规模将达到 1,651 亿美元,到 2030 年将达到 2,146 亿美元,年复合成长率为 5.4%。

这一成长反映了监管机构对可回收性的日益严格要求、品牌加速投资高端和智慧包装,以及化学回收资产的快速扩张。日益严格的法规,例如欧盟强制要求到2030年宝特瓶含有30%的再生材料,正在推动rPET产能的扩张,同时也迫使各种包装形式进行重新设计。品牌也转向使用更轻的瓶子和生物基聚合物以减少碳排放,而Z世代对分量控制、视觉独特的包装的偏好也强化了这一转变。同时,像Amkor收购Very Global这样价值84亿美元的併购案凸显了该产业为实现规模经济和创新发展而展开的竞争。从区域来看,亚太地区都市化中产阶级的需求推动了这一增长,而中东地区由于各国政府鼓励本地饮料生产,增长速度最快。

全球软性饮料包装市场趋势与洞察

更轻的宝特瓶和rPET整合量的激增

监管目标和成本压力迫使加工商减少树脂用量,日本宝特瓶的重量已不足20克,仅为传统瓶子重量的一半。印度的Ganesha Ecopet公司正在扩大rPET的生产规模,目标是到2026年将产量提升至4.2万吨,以回收当地25%的瓶子废弃物。轻量化可降低15-20%的材料成本并减少运输排放,但需要良好的氧气和二氧化碳阻隔性,以确保产品在保质期后仍能保持风味。

寻求高端包装的“功能性苏打水”SKU数量增长

预计到2026年,全球机能饮料销售额将达到1,981亿美元,要求包装能展现产品的健康特性并讲述成分故事。 Z世代已推动该品类38%的成长,他们重视透明度,促使百事公司在包装上融入故事叙述,以证明其20-30%的包装成本是合理的。金属罐因其遮光性和优异的气体阻隔性能而日益受到青睐,无需添加防腐剂即可保护活性成分,保持货架稳定性,并营造高端形象。

生产者延伸责任制(EPR)费用挤压利润空间

美国已有五个州颁布了生产者责任延伸制度(EPR),要求生产商在2031年承担90%的路边回收成本。与可回收性设计挂钩的环境调整费用可能会使包装成本增加2-3%,从而挤压饮料行业的利润空间。同时,在多个州为生产者责任延伸机构(PRO)提供服务会增加行政负担,并提高违规规处罚的风险。

细分市场分析

到2024年, 宝特瓶和rPET瓶将占总销售额的71%,这反映了数十年来成本、透明度和生产线适配性方面的调整。预计到2025年,PET软性饮料包装市场规模将达到1,172亿美元,随着食品级rPET供应的改善,市场将维持稳定的中位数个位数成长。 Avantium的PEF和Danimer的PHA产品线将推动生质塑胶达到17.4%的复合年增长率。

品牌目标的变化、净零排放承诺以及再生材料含量配额的实施,正在加速rPET(再生聚对苯二甲酸乙二醇酯)的普及,即使在价格敏感的市场也是如此。例如,印度已强制规定到2025年,消费后回收材料(PCR)含量必须达到30%。铝罐的优点在于其无限循环利用,在欧洲的回收率高达76.1%,但价格波动较大,正在挤压加工商的利润空间。玻璃在工艺品领域享有盛誉,但在物流存在劣势。纸板产业正争相在禁令生效前替换PFAS涂层。

2024年,瓶装饮料将占总销售额的59%,这主要得益于成熟的吹塑成型线、丰富的产品规格以及环绕式标籤的普及。到2030年,瓶装软性饮料包装市场预计将超过1,220亿美元,部分原因是阻隔技术创新带来的轻量化瓶坯的普及。然而,纤细的铝罐正以8.9%的复合年增长率快速增长,因为Z世代更注重便携性和适合拍照的外形,而非容量。

零售商正积极采用这种包装形式,以提高货架陈列效率,品牌商在相同包装容量下可获得高达 20% 的价格上涨。随着利乐公司转向使用植物来源高密度聚乙烯(HDPE)瓶盖,纸盒包装在冷藏果汁货架上的份额正在不断增长。儘管面临环境税的挑战,小袋包装在新兴市场仍然占据重要地位,因为它提供了一个超低成本的切入点。

区域分析

亚太地区43%的销售份额源自中阶购买力的快速成长、密集的都市区零售业以及健全的消费后PET回收体系,这些都促进了低成本rPET循环利用。日本的PET回收率高达90%,为国内加工商提供原料;中国则透过补贴化学品回收中心来实现其雄心勃勃的回收率目标。印度的生产者责任延伸(EPR)蓝图正在提振对瓶级rPET的需求,使该地区成为扩大循环经济规模的先驱。

2030年,中东地区将以7.1%的复合年增长率领跑,沙乌地阿拉伯和阿联酋正加快建造本地铝罐轧延线和食品饮料工厂,以应对食品安全挑战。儘管全球铝价波动,但年轻消费者越来越青睐高端罐装能量饮料,从而提振了金属需求。政府对永续产业丛集的激励措施将进一步推动波湾合作理事会)罐装采用rPET瓶坯。

北美正面临EPR成本上涨和铝供需紧张的双重挑战,但人工智慧主导的设计软体的领先商业试验缩短了新产品开发週期,使北美市场受益匪浅。 PPWR回收强制令推动了对单一材料柔性薄膜和先进解聚合的投资。南美洲受益于巴西新建的ALPLA HDPE回收厂以及都市区千禧世代对机能饮料消费量的成长,实现了稳步增长。非洲市场虽然仍处于起步阶段,但凭藉着都市区扩张和低温运输物流的发展,已实现了两位数的销售成长。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 更轻的宝特瓶和rPET的大量应用

- 「功能性汽水」SKU的成长对高端包装的需求日益增长

- Z世代消费者要求随时随地购买纤细罐装饮料

- 建造瓶到瓶化学品回收能力

- 人工智慧设计平台缩短了包装开发前置作业时间

- 碳负排放的PEF和PHA试点计画达到商业规模

- 市场限制

- 生产者延伸责任制(EPR)费用挤压利润空间

- 铝价波动和供应瓶颈

- PFAS逐步淘汰对阻隔涂层纸板造成衝击

- 零售商禁止使用一次性再生塑料

- 监管环境

- 技术展望

- 波特五力分析

- 新进入者的威胁

- 供应商的议价能力

- 买方的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

- 投资分析(资本投资与曼德勒趋势)

第五章 市场规模与成长预测

- 材料

- 塑胶(PET、rPET、HDPE、生质塑胶)

- 金属(铝、钢)

- 玻璃

- 纸张和纸板

- 柔性可堆肥薄膜

- 依产品类型

- 瓶子

- 能

- 纸箱和无菌Brick

- 小袋和小袋

- 衬袋纸盒/分装包

- 按产能

- 少于250毫升

- 251~600ml

- 601ml~1 L

- 1公升或以上的家庭装

- 按封闭类型

- 螺旋盖和运动盖

- 皇冠和拉环

- 卡扣式/压入式

- 智慧/互联门锁

- 软性饮料类别

- 碳酸饮料

- 果汁和花蜜

- 能量饮料和功能饮料

- 即饮茶和咖啡

- 风味气泡水

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 澳洲

- 亚太其他地区

- 中东

- 以色列

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 埃及

- 其他非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Amcor PLC

- Ball Corporation

- Tetra Pak International SA

- Crown Holdings Inc.

- Toyo Seikan Group Holdings Ltd

- Owens-Illinois Inc.

- Graham Packaging Company

- Ardagh Group SA

- CAN-PACK SA

- Refresco Group NV

- CKS Packaging Inc.

- Pacific Can China Holdings

- Berry Global Group Inc.

- Silgan Holdings Inc.

- Huhtamaki Oyj

- Mondi plc

- WestRock Company

- Plastipak Holdings Inc.

- UFlex Ltd.

- Nihon Yamamura Glass Co. Ltd

- Vetropack Holding AG

- Visy Industries

第七章 市场机会与未来展望

The soft drink packaging market generated USD 165.1 billion in 2025 and is projected to reach USD 214.6 billion by 2030, advancing at a 5.4% CAGR.

Growth reflects rising regulatory demands for recyclability, accelerating brand investments in premium, connected packs, and rapid scale-up of chemical recycling assets. Stricter mandates-such as the European Union's requirement for 30% recycled content in PET bottles by 2030-are forcing redesigns across formats while spurring rPET capacity expansion. Brands are also pivoting toward lightweight bottles and bio-based polymers that lower carbon footprints, a shift intensified by Gen-Z preferences for portion-controlled, visually distinctive packs. Meanwhile, mergers such as the USD 8.4 billion Amcor-Berry Global deal highlight an industry racing to secure scale economies and innovation pipelines. Across regions, Asia-Pacific's urbanizing middle class anchors demand, and the Middle East posts the fastest growth as governments court local beverage production.

Global Soft Drinks Packaging Market Trends and Insights

Surge in PET bottle lightweighting and rPET integration

Regulatory targets and cost pressure are pushing converters to cut resin use, with some Japanese PET bottles now below 20 g-half the traditional weight. High collection rates-90% in Japan versus 75% in Europe-underpin closed-loop economics, while India's Ganesha Ecopet is scaling to 42,000 t rPET to capture 25% of local bottle waste by 2026. Lightweighting trims material cost 15-20% and lowers freight emissions, but demands superior oxygen and CO2 barriers to safeguard taste over shelf life.

Growth of "functional soda" SKUs demanding premium packs

Global functional beverage sales headed toward USD 198.1 billion by 2026 are forcing packs that signal health credentials and enable ingredient storytelling. Gen-Z already drives 38% of category expansion and values transparency, prompting PepsiCo to embed on-pack narratives that justify 20-30% higher packaging spend. Metal cans win favor for their light-blocking and superior gas barriers that protect active compounds without preservatives, sustaining shelf stability and delivering premium cues.

Extended Producer-Responsibility (EPR) fees squeezing margins

Five U.S. states have enacted EPR laws that shift 90% of curbside recycling costs to producers by 2031. Eco-modulated charges tied to design recyclability can push packaging spend up 2-3%, compressing beverage margins while firms retool to lighter, mono-material formats. Navigating multiple state PROs adds administrative load and penalty risk for non-compliance.

Other drivers and restraints analyzed in the detailed report include:

- On-the-go slim-can demand from Gen-Z consumers

- Bottle-to-bottle chemical recycling capacity build-out

- Volatile aluminium premiums and supply bottlenecks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

PET and rPET bottles dominated with 71% revenue in 2024, reflecting a decades-long alignment of cost, clarity, and line compatibility. The soft drink packaging market size for PET equated to USD 117.2 billion in 2025 and is set for stable mid-single-digit expansion as the supply of food-grade rPET improves. Avantium's PEF and Danimer's PHA pipelines underpin a 17.4% CAGR for bioplastics, a niche today but one poised to carve premium categories with superior barrier metrics and lower cradle-to-grave footprints.

Shifting brand targets, net-zero pledges, and recycled-content quotas are hastening rPET uptake even in price-sensitive markets, with India mandating 30% PCR by 2025. Aluminium cans benefit from infinite recyclability and a 76.1% European recycling rate, yet volatile premiums dent converter margins. Glass retains cachet in craft lines but carries logistics penalties, while paperboard innovators scramble to replace PFAS coatings before looming bans take hold.

Bottles commanded 59% of 2024 sales thanks to entrenched blow-molding fleets, broad SKU sizes, and wrap-label real estate. The soft drink packaging market size for bottles is forecast to cross USD 122 billion by 2030, aided by barrier innovations allowing lower-weight preforms. Slim aluminum cans, however, are surging at 8.9% CAGR as Gen-Z ranks portability and Instagram-ready silhouettes above volume.

Retailers embrace the format's shelf efficiencies, and brands glean up to 20% price uplifts on identical fill volumes. Cartons gain share in chilled juice aisles as Tetra Pak shifts to plant-derived HDPE caps. Sachets remain vital in emerging markets, delivering ultra-low-cost entry points even as eco-taxes loom.

The Soft Drinks Packaging Market Report Segments the Industry Into by Material (Plastic, Metal, Glass and More), Product Type (Bottle, Can, Cartons and Boxes), Capacity (Less Than 250 Ml, 251-600 Ml and More), Closure Type (Screw and Sports Caps, Crown and Pull-Tab and More), Soft-Drink Category (Carbonated Soft Drinks, Juices and Nectars and More) and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific's 43% revenue share stems from surging middle-class purchasing power, dense urban retail, and robust post-consumer PET recovery systems that fuel low-cost rPET loops. Japan's 90% PET collection rate supplies domestic converters, while China subsidizes chemical recycling hubs to beat ambitious recycled-content goals. India's EPR roadmap intensifies demand for bottle-grade rPET, positioning the region as a bellwether for circular-economy scale-up.

The Middle East posts the highest 7.1% CAGR to 2030 as Saudi Arabia and the UAE fast-track local can-sheet rolling lines and beverage plants in pursuit of food-security agendas. Youthful demographics gravitate to energy drinks packaged in sleek cans, reinforcing metal demand despite global aluminium price swings. Government incentives for sustainable industry clusters further spur adoption of rPET preforms in Gulf Cooperation Council filling lines.

North America wrestles with EPR-induced cost headwinds and aluminium sheet tightness, yet benefits from first-mover commercial trials of AI-driven design software that cuts new-SKU timelines. Europe continues to set the regulatory pace: the PPWR's recyclability mandates catalyze investment in mono-material flexible films and advanced depolymerization. South America secures steady gains through Brazil's new ALPLA HDPE recycling plant and rising consumption of functional drinks among urban millennials. Africa, still nascent, observes double-digit volume growth on the back of urban sprawl and expanding cold-chain logistics, though inadequate collection infrastructure tempers rPET uptake.

- Amcor PLC

- Ball Corporation

- Tetra Pak International SA

- Crown Holdings Inc.

- Toyo Seikan Group Holdings Ltd

- Owens-Illinois Inc.

- Graham Packaging Company

- Ardagh Group SA

- CAN-PACK SA

- Refresco Group NV

- CKS Packaging Inc.

- Pacific Can China Holdings

- Berry Global Group Inc.

- Silgan Holdings Inc.

- Huhtamaki Oyj

- Mondi plc

- WestRock Company

- Plastipak Holdings Inc.

- UFlex Ltd.

- Nihon Yamamura Glass Co. Ltd

- Vetropack Holding AG

- Visy Industries

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in PET bottle lightweighting and rPET integration

- 4.2.2 Growth of "functional soda" SKUs demanding premium packs

- 4.2.3 On-the-go slim-can demand from Gen-Z consumers

- 4.2.4 Bottle-to-bottle chemical recycling capacity build-out

- 4.2.5 AI-enabled design platforms cutting packaging development lead-times

- 4.2.6 Carbon-negative PEF and PHA pilots reaching commercial scale

- 4.3 Market Restraints

- 4.3.1 Extended Producer-Responsibility (EPR) fees squeezing margins

- 4.3.2 Volatile aluminium premiums and supply bottlenecks

- 4.3.3 PFAS phase-outs disrupting barrier-coated paperboard

- 4.3.4 Retailer bans on single-use secondary plastics

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

- 4.7 Investment Analysis (CapEx and MandA Trends)

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Material

- 5.1.1 Plastic (PET, rPET, HDPE, Bioplastics)

- 5.1.2 Metal (Aluminium, Steel)

- 5.1.3 Glass

- 5.1.4 Paper and Paperboard

- 5.1.5 Flexible and Compostable Films

- 5.2 By Product Type

- 5.2.1 Bottles

- 5.2.2 Cans

- 5.2.3 Cartons and Aseptic Bricks

- 5.2.4 Pouches and Sachets

- 5.2.5 Bag-in-Box / Dispense Packs

- 5.3 By Capacity

- 5.3.1 Less Than 250 ml

- 5.3.2 251-600 ml

- 5.3.3 601-1 L

- 5.3.4 More Than 1 L Family Packs

- 5.4 By Closure Type

- 5.4.1 Screw and Sports Caps

- 5.4.2 Crown and Pull-tab

- 5.4.3 Snap-on / Press-fit

- 5.4.4 Smart / Connected Closures

- 5.5 By Soft-Drink Category

- 5.5.1 Carbonated Soft Drinks

- 5.5.2 Juices and Nectars

- 5.5.3 Energy and Functional Drinks

- 5.5.4 RTD Tea and Coffee

- 5.5.5 Flavoured and Sparkling Water

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Israel

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 United Arab Emirates

- 5.6.5.4 Turkey

- 5.6.5.5 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Egypt

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Amcor PLC

- 6.4.2 Ball Corporation

- 6.4.3 Tetra Pak International SA

- 6.4.4 Crown Holdings Inc.

- 6.4.5 Toyo Seikan Group Holdings Ltd

- 6.4.6 Owens-Illinois Inc.

- 6.4.7 Graham Packaging Company

- 6.4.8 Ardagh Group SA

- 6.4.9 CAN-PACK SA

- 6.4.10 Refresco Group NV

- 6.4.11 CKS Packaging Inc.

- 6.4.12 Pacific Can China Holdings

- 6.4.13 Berry Global Group Inc.

- 6.4.14 Silgan Holdings Inc.

- 6.4.15 Huhtamaki Oyj

- 6.4.16 Mondi plc

- 6.4.17 WestRock Company

- 6.4.18 Plastipak Holdings Inc.

- 6.4.19 UFlex Ltd.

- 6.4.20 Nihon Yamamura Glass Co. Ltd

- 6.4.21 Vetropack Holding AG

- 6.4.22 Visy Industries

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

软性饮料包装市场-2026-2031年预测

软性饮料包装市场-2026-2031年预测 软性饮料包装市场(按包装材料、包装类型和最终用途行业)—2025-2032 年全球预测

软性饮料包装市场(按包装材料、包装类型和最终用途行业)—2025-2032 年全球预测 软性饮料包装市场机会、成长动力、产业趋势分析与预测 2025-2034

软性饮料包装市场机会、成长动力、产业趋势分析与预测 2025-2034 中东和非洲软性饮料包装:市场占有率分析、产业趋势、成长预测(2025-2030)北美软性饮料包装:市场占有率分析、行业趋势和成长预测(2025-2030 年)拉丁美洲软性饮料包装:市场占有率分析、行业趋势和成长预测(2025-2030 年)欧洲软性饮料包装:市场占有率分析、产业趋势、成长预测(2025-2030)美国软性饮料包装:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)

中东和非洲软性饮料包装:市场占有率分析、产业趋势、成长预测(2025-2030)北美软性饮料包装:市场占有率分析、行业趋势和成长预测(2025-2030 年)拉丁美洲软性饮料包装:市场占有率分析、行业趋势和成长预测(2025-2030 年)欧洲软性饮料包装:市场占有率分析、产业趋势、成长预测(2025-2030)美国软性饮料包装:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)