|

市场调查报告书

商品编码

1850219

数位行销软体:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)Digital Marketing Software Market - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

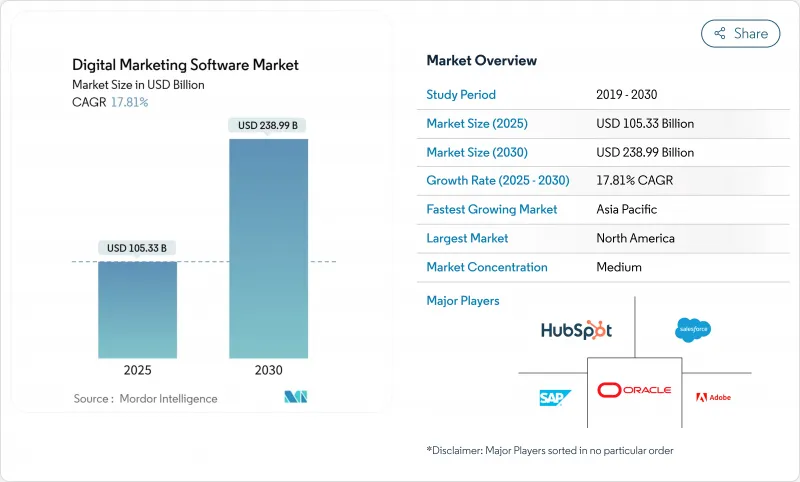

全球数位行销软体市场预计到 2025 年将累计1,053.3 亿美元的收入,到 2030 年将达到 2,389.9 亿美元,在此期间的复合年增长率为 17.81%。

朝向云端原生架构、人工智慧主导的自动化和无 Cookie 个人化的快速转型,使得行销技术支出占行销总预算的比例维持在 25.4%。企业现在正摒弃分散的独立解决方案(这些方案会增加整合成本),转而采用整合资料、内容和启动功能的整合套件。与使用量挂钩的订阅定价模式降低了前期投资,并推动了中型企业的采用。随着平台供应商整合生成式人工智慧辅助工具,缩短创新週期并扩展自助式分析功能,竞争持续加剧。

全球数位行销软体市场趋势与洞察

数位化优先的客户旅程激增

70%的B2B买家透过搜寻引擎开始调查,这迫使企业重新构想内容、数据和商务方面的互动模式。製造商正将75%的行销预算分配给数位管道,比上一周期增加了10个百分点。医疗服务提供者正在利用人工智慧编配,在入口网站和麵向患者的应用程式中提供合规且个人化的患者就医体验。欧洲企业将22.9%的数位转型病人历程分配给行销技术,并将客户体验视为关键的竞争优势。这种持续向数位化优先互动模式的转变,支撑了对用于管理客户获取、转换和留存的整合平台的持续需求。

人工智慧驱动的内容和宣传活动优化

Adobe GenStudio 等生成式人工智慧平台能够大规模地产生动态素材变体,在缩短 50% 製作时间的同时,也能将电子邮件转换率提升一倍。 HubSpot 在 2024 年 9 月发布的 Breeze AI 中整合了 80 多项人工智慧功能,用于自动化宣传活动设计。亚太地区的企业正在加速投资人工智慧,59% 的企业计划在 2025 年增加人工智慧预算。企业采用 Salesforce Agentforce 等自主代理,证明行销工作流程可以在极少人工干预的情况下运作。人工智慧能力正迅速成为一项基本要求,而非差异化优势。

与传统行销技术堆迭整合的复杂性

企业平均拥有 130 个应用程序,但只有不到五分之一的应用程式实现了完全整合。行销长指出,资料分散、管治不善和实施技能不足是他们面临的最大障碍。转型为 MACH(微服务、API 优先、云端原生、无头)架构需要许多中型企业所缺乏的技术专长,这不仅延长了专案週期,也推高了整体拥有成本。欧洲製造商中只有三分之二实现了数位成熟,而美国同行中这一比例接近五分之四,这一事实凸显了二者之间的差距。

细分市场分析

预计到2024年,云端交付将占总营收的65.5%,并在2030年之前以18.5%的复合年增长率持续成长,占据数位行销软体市场份额。弹性基础设施、持续更新和更低的维护成本,在提高扩充性的同时,降低了整体拥有成本。在资料驻留和客製化整合至关重要的监管领域,本地部署仍然占据主导地位,但随着云端供应商获得更高级别的安全认证,其市场份额正在萎缩。

此外,人工智慧功能通常仅在云端版本中提供,这促使企业更倾向于选择云端版本。虽然供应商提供混合模式以简化过渡,但随着企业优先考虑速度和灵活性,全面采用SaaS的趋势似乎已不可逆转。

2024年,软体授权收入将占总收入的54.9%,而随着企业寻求专业知识以释放平台价值,服务收入将以19.2%的复合年增长率快速成长。系统整合、资料清理和变更管理将成为初期计划的主导,而託管服务则负责长期最佳化。人工智慧的普及应用将进一步推动数位行销软体服务市场规模的成长,因为人工智慧需要模型训练、管治和迭代效能调优。

随着技术栈日趋复杂,外部合作伙伴正在填补能力缺口,尤其是在多重云端和可组合架构方面。供应商将咨询和託管服务打包到订阅计划中,从而创造稳定的经常性收入并加深客户忠诚度。培训机构和认证计画也日益普及,旨在提升客户团队的技能并加速平台投资报酬率的实现。

数位行销软体市场配置(云端和本地部署)、组件(软体和服务)、最终用户公司规模(大型企业和中小企业)、最终用户行业(IT和电信、银行、金融服务和保险、零售和电子商务、製造业等)以及地区进行细分。市场预测以美元(USD)计价。

区域分析

2024年,北美将占全球营收的41.9%,这主要得益于云端运算的深度普及、高技能的劳动力以及Adobe、Salesforce和HubSpot等平台供应商的集中布局。创业投资持续支持人工智慧主导的营销科技Start-Ups,进一步推动了该地区的创新发展。随着技术应用日趋成熟,产品更换週期延长,北美地区的成长将保持稳健但适度的态势。

预计到2030年,亚太地区的复合年增长率将达到20.6%,成为全球成长最快的地区。各国政府都在积极推动数位转型,企业正在采用尊重语言和文化差异的在地化人工智慧模型,製造业和金融服务业的现代化项目正在加速平台应用,而本土供应商也不断涌现以应对监管方面的特殊挑战。因此,儘管竞争日益激烈,亚太地区的数位行销软体市场预计仍将快速成长。

欧洲市场依然强劲,但监管也十分严格。欧盟仅有66%的製造商实现了端到端数位化,然而56%的高阶主管计划在2025年增加技术预算。 GDPR将推动对隐私优先平台的需求,同时也延长实施週期并增加成本。拥有合规设计架构的供应商将找到积极的买家,而随着其他司法管辖区效仿隐私法规,欧洲累积的专业知识也日益输出。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 数位化优先的客户体验的激增

- 云端原生SaaS的成本优势

- 人工智慧驱动的内容和宣传活动优化

- 来自 B2C 和 B2B 的全通路互动需求

- 零方资料和无 Cookie 个人化

- Gen-AI 辅助驾驶系统大幅缩短创新製作时间

- 市场限制

- 与传统行销技术堆迭整合的复杂性

- 资料隐私和同意管理合规成本

- 第一方资料增强的单位成本不断上升

- 人工智慧主导的宣传活动设计领域客户体验人才短缺

- 价值链分析

- 监管环境

- 技术展望

- 波特五力模型

- 新进入者的威胁

- 买方/消费者的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 透过部署

- 云

- 本地部署

- 按组件

- 软体

- 服务

- 按最终用户公司规模划分

- 大公司

- 小型企业

- 按最终用户行业划分

- 资讯科技和通讯

- 媒体与娱乐

- BFSI

- 零售与电子商务

- 製造业

- 医疗保健和生命科学

- 其他的

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 俄罗斯

- 西班牙

- 瑞士

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 马来西亚

- 新加坡

- 越南

- 印尼

- 亚太其他地区

- 中东和非洲

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 其他中东地区

- 非洲

- 奈及利亚

- 南非

- 其他非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Adobe Inc.

- Salesforce, Inc.

- Oracle Corp.

- SAP SE

- Microsoft Corp.

- HubSpot Inc.

- IBM Corp.

- Google LLC

- SAS Institute Inc.

- Teradata Corp.

- Criteo SA

- Infor Inc.

- Marketo Engage(Adobe)

- ActiveCampaign LLC

- Klaviyo Inc.

- Intuit Mailchimp

- Sendinblue(Brevo)

- Zoho Corporation

- Constant Contact

- Sitecore

- Acoustic LP

- Insider Inc.

- Sprinklr

- Braze Inc.

第七章 市场机会与未来展望

The global digital marketing software market posted USD 105.33 billion revenue in 2025 and is forecast to touch USD 238.99 billion by 2030, advancing at a 17.81% CAGR over the period.

Rapid migration to cloud-native architectures, AI-driven automation, and cookieless personalization keeps spending on marketing technology at 25.4% of overall marketing budgets. Enterprises now favor integrated suites that unify data, content, and activation functions, replacing fragmented point solutions that raise integration costs. Subscription pricing tied to usage reduces up-front capital outlays, encouraging adoption among mid-market firms. Competitive intensity continues to rise as platform vendors embed generative AI copilots that shorten creative cycles and expand self-service analytics.

Global Digital Marketing Software Market Trends and Insights

Surge in Digital-First Customer Journeys

Seventy percent of B2B buyers now initiate research via search engines, forcing enterprises to re-engineer engagement models across content, data, and commerce. Manufacturing firms allocate 75% of marketing budgets to digital channels, up 10 percentage points versus past cycles. Healthcare providers use AI orchestration to deliver compliant, personalized journeys across web portals and patient apps. European organizations devote 22.9% of digital transformation budgets to marketing technology, recognizing customer experience as a primary competitive lever. The persistent shift toward digital-first engagement underpins sustained demand for unified platforms that manage acquisition, conversion, and retention.

AI-Powered Content and Campaign Optimization

Generative AI platforms such as Adobe GenStudio enable dynamic asset variation at scale, cutting production times by 50% while raising email conversion rates two-fold. HubSpot embedded more than 80 AI features in its Breeze AI release of September 2024, underscoring the race to automate campaign design. Asia-Pacific firms are accelerating investment, with 59% planning higher AI budgets in 2025. Enterprise deployments of autonomous agents, as seen in Salesforce Agentforce, prove marketing workflows can operate with minimal human intervention. AI capability is rapidly becoming a baseline requirement rather than a differentiator.

Integration Complexity with Legacy Martech Stacks

Enterprises average 130 applications in the stack, yet fewer than one-fifth are fully integrated, inflating operational costs and delaying ROI. CMOs cite disconnected data, poor governance, and limited implementation skills as top barriers. Moving to MACH (microservices, API-first, cloud-native, headless) architectures demands technical expertise that many mid-market firms lack, extending timelines and inflating total cost of ownership. European manufacturers illustrate the gap, with only two-thirds achieving digital maturity, compared with nearly four-fifths of US peers.

Other drivers and restraints analyzed in the detailed report include:

- Omnichannel Engagement Demand from B2C and B2B

- Gen-AI Copilots Slashing Creative Production Time

- Data-Privacy and Consent-Management Compliance Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud delivery controlled 65.5% of 2024 revenue, and its share of the digital marketing software market size is projected to expand at an 18.5% CAGR through 2030. The economics remain compelling: elastic infrastructure, continuous updates, and lower maintenance overheads drive total cost of ownership down while improving scalability. On-premise installations persist in regulated verticals where data residency and bespoke integration remain critical, but their share shrinks as cloud providers earn advanced security certifications.

Cost alignment with usage encourages mid-market entry, and AI functionality is often available first in cloud editions, reinforcing preference. Vendors offer hybrid models to ease transition, yet the momentum toward full SaaS deployment appears irreversible as enterprises prioritize speed and flexibility.

Software licenses represented 54.9% of 2024 revenue, yet services revenue is set to grow faster at 19.2% CAGR as firms seek expertise to unlock platform value. System integration, data hygiene, and change-management engagements dominate initial projects, while managed services sustain long-term optimization. The digital marketing software market size for service engagements is further buoyed by AI adoption, which requires model training, governance, and iterative performance tuning.

As stacks grow more complex, external partners fill capability gaps, particularly around multi-cloud and composable architectures. Vendors bundle advisory and managed-service offerings into subscription plans, generating sticky recurring revenue and deepening customer lock-in. Training academies and certification programs proliferate to upskill client teams and accelerate platform ROI.

Digital Marketing Software Market is Segmented by Deployment (Cloud and On-Premise), Component (Software and Services), End-User Enterprise Size (Large Enterprises and Small and Medium Enterprises (SMEs)), End-User Vertical (IT and Telecom, BFSI, Retail and E-Commerce, Manufacturing and More) and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America held 41.9% revenue in 2024, driven by deep cloud penetration, a skilled workforce, and dense concentration of platform vendors such as Adobe, Salesforce, and HubSpot. Venture capital continues to favor AI-led martech startups, reinforcing the local innovation flywheel. Growth is steady but moderates as penetration approaches maturity and replacement cycles lengthen.

Asia-Pacific is projected to record a 20.6% CAGR to 2030, the fastest worldwide. Governments incentivize digital transformation, and enterprises are adopting localized AI models that respect linguistic and cultural nuances. Manufacturing and financial-services modernization programs accelerate platform uptake, and domestic vendors emerge to address regulatory specifics. The digital marketing software market size attributable to Asia-Pacific will therefore expand rapidly, even as competition intensifies.

Europe remains a solid but regulated adopter. While only 66% of EU manufacturers have achieved end-to-end digitalization, 56% of executives plan higher technology budgets in 2025. GDPR catalyzes demand for privacy-first platforms, yet also stretches implementation timelines and cost structures. Vendors with compliance-by-design architectures find receptive buyers, and expertise developed in Europe is increasingly exported as other jurisdictions replicate privacy statutes.

- Adobe Inc.

- Salesforce, Inc.

- Oracle Corp.

- SAP SE

- Microsoft Corp.

- HubSpot Inc.

- IBM Corp.

- Google LLC

- SAS Institute Inc.

- Teradata Corp.

- Criteo SA

- Infor Inc.

- Marketo Engage (Adobe)

- ActiveCampaign LLC

- Klaviyo Inc.

- Intuit Mailchimp

- Sendinblue (Brevo)

- Zoho Corporation

- Constant Contact

- Sitecore

- Acoustic L.P.

- Insider Inc.

- Sprinklr

- Braze Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in digital-first customer journeys

- 4.2.2 Cloud-native SaaS cost advantages

- 4.2.3 AI-powered content and campaign optimization

- 4.2.4 Omnichannel engagement demand from B2C and B2B

- 4.2.5 Zero-party data and cookieless personalization

- 4.2.6 Gen-AI copilots slashing creative production time

- 4.3 Market Restraints

- 4.3.1 Integration complexity with legacy martech stacks

- 4.3.2 Data-privacy and consent-management compliance costs

- 4.3.3 Rising unit prices for 1st-party data enrichment

- 4.3.4 CX talent shortage for AI-led campaign design

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment

- 5.1.1 Cloud

- 5.1.2 On-premise

- 5.2 By Component

- 5.2.1 Software

- 5.2.2 Services

- 5.3 By End-user Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Mid-sized Enterprises

- 5.4 By End-user Industry

- 5.4.1 IT and Telecom

- 5.4.2 Media and Entertainment

- 5.4.3 BFSI

- 5.4.4 Retail and E-commerce

- 5.4.5 Manufacturing

- 5.4.6 Healthcare and Life Sciences

- 5.4.7 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Russia

- 5.5.3.6 Spain

- 5.5.3.7 Switzerland

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Malaysia

- 5.5.4.6 Singapore

- 5.5.4.7 Vietnam

- 5.5.4.8 Indonesia

- 5.5.4.9 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 Nigeria

- 5.5.5.2.2 South Africa

- 5.5.5.2.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Adobe Inc.

- 6.4.2 Salesforce, Inc.

- 6.4.3 Oracle Corp.

- 6.4.4 SAP SE

- 6.4.5 Microsoft Corp.

- 6.4.6 HubSpot Inc.

- 6.4.7 IBM Corp.

- 6.4.8 Google LLC

- 6.4.9 SAS Institute Inc.

- 6.4.10 Teradata Corp.

- 6.4.11 Criteo SA

- 6.4.12 Infor Inc.

- 6.4.13 Marketo Engage (Adobe)

- 6.4.14 ActiveCampaign LLC

- 6.4.15 Klaviyo Inc.

- 6.4.16 Intuit Mailchimp

- 6.4.17 Sendinblue (Brevo)

- 6.4.18 Zoho Corporation

- 6.4.19 Constant Contact

- 6.4.20 Sitecore

- 6.4.21 Acoustic L.P.

- 6.4.22 Insider Inc.

- 6.4.23 Sprinklr

- 6.4.24 Braze Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

公关分析软体市场分析及预测(至2035年):依类型、产品类型、服务、技术、元件、应用、部署类型、最终使用者及解决方案划分数位行销软体市场分析及预测(至 2035 年):按类型、产品类型、服务、技术、组件、应用、部署方式、最终用户、解决方案划分

公关分析软体市场分析及预测(至2035年):依类型、产品类型、服务、技术、元件、应用、部署类型、最终使用者及解决方案划分数位行销软体市场分析及预测(至 2035 年):按类型、产品类型、服务、技术、组件、应用、部署方式、最终用户、解决方案划分 全球数位行销软体市场规模、份额、趋势和成长分析报告(2026-2034)

全球数位行销软体市场规模、份额、趋势和成长分析报告(2026-2034) 按客户规模、客製化类型、最终用户产业、部署模式和应用程式类型分類的目录资讯亭客製化服务市场 - 全球预测 2026-2032按组件、部署类型和应用程式分類的目录资讯亭市场 - 全球预测(2026-2032 年)

按客户规模、客製化类型、最终用户产业、部署模式和应用程式类型分類的目录资讯亭客製化服务市场 - 全球预测 2026-2032按组件、部署类型和应用程式分類的目录资讯亭市场 - 全球预测(2026-2032 年) 日本数位行销软体市场报告:按组件、部署类型、组织规模、最终用途和地区划分,2026-2034 年

日本数位行销软体市场报告:按组件、部署类型、组织规模、最终用途和地区划分,2026-2034 年 数位行销软体市场规模、份额和成长分析(按组件、部署类型、组织规模、垂直产业和地区划分)-2026-2033年产业预测按类型、部署模式、组织规模和最终用户产业分類的重定向软体市场-全球预测,2025-2032年2025 年至 2033 年数位行销软体市场报告(按解决方案、服务、部署类型、组织规模、最终用途和地区)

数位行销软体市场规模、份额和成长分析(按组件、部署类型、组织规模、垂直产业和地区划分)-2026-2033年产业预测按类型、部署模式、组织规模和最终用户产业分類的重定向软体市场-全球预测,2025-2032年2025 年至 2033 年数位行销软体市场报告(按解决方案、服务、部署类型、组织规模、最终用途和地区) 数位行销软体市场规模、份额和趋势分析报告:按类型、软体、服务、部署、公司规模、最终用途、地区和细分市场预测,2025 年至 2033 年

数位行销软体市场规模、份额和趋势分析报告:按类型、软体、服务、部署、公司规模、最终用途、地区和细分市场预测,2025 年至 2033 年