|

市场调查报告书

商品编码

1850365

自动驾驶卡车:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)Autonomous Truck - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

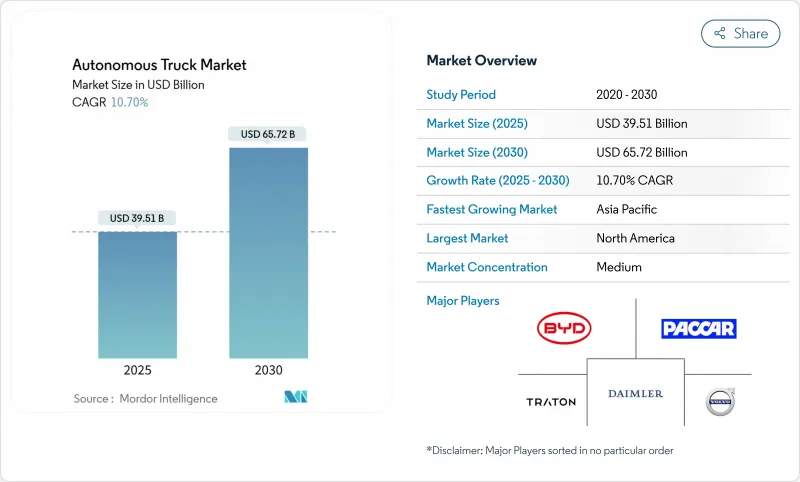

预计到 2025 年,自动驾驶卡车市场规模将达到 395.1 亿美元,到 2030 年将达到 657.2 亿美元,预测期(2025-2030 年)的复合年增长率为 10.70%。

司机短缺和人事费用上涨给传统车队带来了巨大挑战,促使企业采用资产利用率更高的重型平台。紧急煞车系统等监管要求以及感测器价格的下降正在加速现代化进程和商业试点。随着L4级自动驾驶卡车在远距运输中展现出可靠性,相关人员将受益于更快的投资回收期、更高的拖车周转率以及燃油和排放气体的节省,从而推动自动驾驶卡车市场走向广泛部署。

全球自动驾驶卡车市场趋势与洞察

公路运输司机短缺和人事费用上升

美国卡车运输协会报告称,到2024年,将有超过8万名重型卡车司机失业,而且随着司机退休人数超过新入职人数,预计这一缺口还会扩大。强制休息时间和高额加班费推高了车辆总拥有成本,因此,对于超过500英里的线路而言,全天候自动驾驶在经济上更具吸引力。德克萨斯一条走廊上成功的L4级自动驾驶试点项目,使拖车週转率翻了一番,并将每英里的人事费用降低了35%以上。物流巨头们正在重新设计他们的运输网络,采用自动驾驶主干线,并辅以人工操作的「最后一公里」环线。

对全天候枢纽间物流的需求

电子商务的履约窗口和即时生产模式需要全天候的运能。州际公路的管控通行有利于感测器感知和冗余配置,使车队能够以预期路线调度自动驾驶的8级牵引车。 Aurora公司于2024年完成了达拉斯至休士顿之间1200英里的无人驾驶测试,检验了枢纽到枢纽模式的执行时间承诺。零售商将由此带来的等待时间缩短与库存减少联繫起来,从而推动了专用自动驾驶运力的长期合约签订。

全球法规和跨国责任的零碎化

加州AB316法案限制重量超过10,000磅的无人驾驶卡车必须在无人驾驶人员的操控下行驶,凸显了美国政策的碎片化。儘管布鲁塞尔方面力推在2026年前建立统一的框架,但欧盟成员国之间也存在类似的政策不一致。这些不一致导致需要分别办理许可证、购买保险附加条款以及建立数据报告流程,从而削弱了规模经济效益,并延缓了全欧范围内的推广。

细分市场分析

到2024年,重型牵引车将占自动驾驶卡车市场规模的64.5%,这反映了远距线路自动化带来的经济效益,因为在长途运输中,人事费用是最大的支出项目,超过了燃油成本。车队财务长模型预测,对于运行里程超过500英里且运转率达到95%的L4级自动驾驶系统,其投资回收期不到四年。中型卡车将专注于区域性杂货和小包裹运输,需要在更严格的车辆重量限制和日益严格的都市区通行限制之间取得平衡。受电子商务业务量成长的推动,轻型自动驾驶货车将以15.1%的复合年增长率实现最快成长。

技术合作巩固了戴姆勒在重型车辆领域的领先地位:戴姆勒卡车向Torc Robotics公司交付了一批具备自动驾驶能力的Freightliner Cascadia牵引车,用于在德克萨斯州进行测试,这体现了这家汽车製造商致力于在工厂预装冗余架构的决心。同时,轻型车辆製造商则利用仅基于摄影机的感知技术来降低材料成本,并随着政府法规的演变,为「最后一公里」自动驾驶做好准备。这种发展轨迹的分化预示着市场将呈现哑铃状的碎片化模式。

儘管SAE 1-2级驾驶辅助系统将在2024年占据自动驾驶卡车市场58.2%的份额,但市场焦点将转向L4级自动驾驶,预计到2030年,L4级自动驾驶将以26.25%的复合年增长率增长。 2024年至2025年,年度无人驾驶试点部署数量将成长140%,而拥有L4级蓝图的公司将获得更多资金。沃尔沃的VNL自动驾驶平台计划于2025年交付客户,显示该汽车製造商坚信全路线自动驾驶将带来加值服务合约。虽然L3级自动驾驶仍然是法规要求具备备用方案的过渡解决方案,但随着监管机构坚持在某些路段完全取消驾驶员,其商业性窗口正在缩小。

投资者正在支持这项转型:Waabi 在由 Uber 和英伟达主导的B 轮融资中获得了 2 亿美元,用于完善其人工智慧优先的模拟技术,并将道路测试里程减少 80%。这笔资金的注入巩固了人们的信念:可扩展的虚拟训练将加快 L4 级参与企业的认证速度,并缩短其实现收益所需的时间。随着高清地图成本的下降,市场分析师预计,到 2030 年,L4 级自动驾驶的货运里程占比将超过 30%,从而重塑资产调度逻辑和保险承保规则。

自动驾驶卡车市场按卡车类型(轻型卡车、其他)、自动驾驶等级(SAE 1-2级(驾驶辅助)、其他)、ADAS功能(主动车距控制巡航系统、车道偏离预警、其他)、组件(雷射雷达、雷达、摄影机、其他)、驱动方式(内燃机、纯电动、混合动力、其他)和地区进行细分。市场预测以价值(美元)和销售(辆)为单位。

区域分析

北美在2024年占据了33.7%的自动驾驶卡车市场份额,这主要得益于各州推行的试点框架以及支援车道中心自动驾驶的4.8万英里州际公路系统。德克萨斯州拥有连接达拉斯、休士顿、埃尔帕索和凤凰城的商业路线,Aurora、Kodiak、Volvo和DHL等公司都在经营这些路线,并创造了收益的收入。资金筹措依然强劲,新兴企业在2024年至2025年间筹集了超过10亿美元的资金,反映出投资人对近期收益的信心。

欧洲在2024年贡献了约三分之一的收益。德国、瑞典和荷兰在测试方面处于领先地位,率先采用了联合国欧洲经济委员会(UNECE)的网路安全和车道维持指令。沃尔沃和戴姆勒的软体合资企业将为欧盟原始设备製造商(OEM)提供一个可透过空中升级的平台,以便在2026年全球安全路线(GSR)分阶段推出之前进行升级。跨境货运正透过诸如斯堪的斯堪地那维亚-汉堡路线等数位化走廊试点计画向前推进,但各国的认证时间表仍然不均衡,阻碍了整个欧洲大陆的规模化发展。

亚太地区仍是成长最快的地区,复合年增长率高达21.4%。中国交通运输运输部核准一项全国性的智慧高速公路计划,旨在帮助中国企业在2025年中期实现2000万公里的行驶里程。日本的目标是到2027年实现主要道路L4级自动驾驶覆盖,并结合自动驾驶奖励以及对氢燃料电池和电池充电站的支援。韩国的「K-Mobility 2030」计画正在加速车载资讯服务技术的应用,而印度则将目光投向了自动驾驶采矿和港口运输这两个先行领域。像Autoware这样的开放原始码堆迭为区域整合商提供了立足点,使其能够针对左舵驾驶的城市道路网路客製化感知系统。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 远距运输面临司机短缺和劳动成本上升的问题

- 对全天候枢纽间物流的需求

- 加强安全法规(例如,美国的自动驾驶汽车法案、欧盟的车辆安全法规)

- 编队行驶可节省燃油并控制排放气体

- 自动驾驶与零排放动力系统之间的协同效应

- 开放原始码自主协定栈降低了准入门槛

- 市场限制

- 国际监管不完善和跨境责任

- 网路安全与OTA更新风险

- 光达/感测器套件高成本

- 除一级走廊外,缺乏高解析度高清地图

- 价值链/供应链分析

- 监管格局

- 技术展望

- 波特五力模型

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模及成长预测(价值(美元)及销售量(单位))

- 按卡车类型

- 小型货车

- 中型卡车

- 大型卡车

- 依自主程度

- SAE 1-2级(驾驶辅助)

- SAE 3级(有条件)

- SAE 4级(进阶)

- SAE 5级(完整版)

- 透过ADAS功能

- 主动车距控制巡航系统

- 车道偏离预警

- 交通壅塞辅助

- 高速公路导航

- 自动紧急制动

- 盲点侦测

- 车道维持辅助

- 按组件

- 骑士

- 雷达

- 相机

- 超音波和其他感测器

- AI运算模组

- 按驱动类型

- 内燃机

- 电池驱动

- 杂交种

- 氢燃料电池

- 按地区

- 北美洲

- 美国

- 加拿大

- 北美其他地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 澳洲

- 其他亚太地区

- 中东和非洲

- GCC

- 土耳其

- 南非

- 其他中东和非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- AB Volvo

- Daimler Truck AG

- Traton SE

- PACCAR Inc.

- BYD Co. Ltd.

- Tesla, Inc.

- TuSimple

- Aurora Innovation

- Waymo Via

- Plus.ai

- Torc Robotics

- Kodiak Robotics

- Nikola Corp.

- Einride

- Embark Technology

- Hyzon Motors

- Gatik AI

- Volvo-Uber ATG JV

- Scania

- Navistar

第七章 市场机会与未来展望

The Autonomous Truck Market size is estimated at USD 39.51 billion in 2025, and is expected to reach USD 65.72 billion by 2030, at a CAGR of 10.70% during the forecast period (2025-2030).

Persistent driver shortages and rising labor costs challenge traditional fleets, driving the adoption of heavy-duty platforms with high asset utilization. Regulatory mandates, such as emergency-braking systems, and falling sensor prices are accelerating modernization and commercial pilots. As Level 4 trucks prove reliable on long-haul routes, stakeholders benefit from faster pay-back cycles, increased trailer turnover, and fuel and emission savings, advancing the autonomous truck market toward scaled deployment.

Global Autonomous Truck Market Trends and Insights

Driver Shortage & Rising Line-Haul Labor Cost

The American Trucking Associations reported more than 80,000 unfilled heavy-duty positions in 2024, a gap expected to widen as driver retirements outpace new entrants. Mandatory rest breaks and overtime premiums inflate total cost of ownership, making 24/7 autonomous operation financially attractive on routes exceeding 500 miles. Successful Level 4 pilots along Texas corridors have doubled trailer turns and cut per-mile labor spend by over 35%. Logistics majors are now redesigning networks with autonomous trunk lines complemented by human-driven last-mile loops.

Demand for 24/7 Hub-to-Hub Logistics

E-commerce fulfillment windows and just-in-time manufacturing call for clock-round capacity. The controlled access of interstate highways suits sensor perception and redundancy targets, allowing fleets to dispatch autonomous Class 8 tractors on predictable lanes. Aurora completed a 1,200-mile driver-out run between Dallas and Houston in 2024, validating the uptime promise of hub-to-hub models. Retail shippers link the resulting latency reductions to inventory shrink, propelling long-term contracts for dedicated autonomous capacity.

Patchwork Global Regulation & Cross-Border Liability

California's AB 316, which restricts autonomous trucks above 10,000 lb without on-board human operators, underscores the fragmented U.S. policy landscape. Similar inconsistencies appear across EU member states despite Brussels' push for a unified framework by 2026. These mismatches require separate permitting, insurance riders, and data-reporting workflows, diluting economies of scale and postponing continent-wide deployments.

Other drivers and restraints analyzed in the detailed report include:

- Tightening Safety Regulations

- Platooning-Driven Fuel Savings & Emission Mandates

- Cyber-Security & OTA Update Risks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Heavy-duty tractors accounted for 64.5% of the autonomous truck market size in 2024, reflecting the economic leverage of automating long-haul lanes where labor costs eclipse fuel as the largest expense line. Fleet CFO models show pay-back periods under four years when Level 4 systems pass 500-mile duty cycles at 95% uptime. Medium-duty units focus on regional grocery and parcel runs, balancing tighter curbweight limits with growing urban-access restrictions. Light-duty autonomous vans, boosted by e-commerce volumes, post the fastest growth at a 15.1% CAGR, aided by simplified form-factor sensor integration.

Technology partnerships reinforce heavy-duty leadership. Daimler Truck shipped a batch of autonomous-ready Freightliner Cascadia tractors to Torc Robotics for Texas trials, demonstrating OEM commitment to factory-installed redundancy architectures. Meanwhile, light-duty builders exploit camera-only perception to trim bill-of-material costs, positioning for last-mile autonomy once municipal rules evolve. The divergent trajectories suggest a barbell market split: high-value interstate rigs on one end and agile city vans on the other.

SAE 1-2 driver-assist suites represented 58.2% of the autonomous truck market share 2024, but the spotlight is shifting to Level 4 and set to foresee a growth of 26.25% CAGR by 2030. Annualized deployments of driver-out pilots rose 140% between 2024 and 2025, and capital inflows favor companies with L4 roadmaps. Volvo's VNL Autonomous platform, slated for customer delivery in 2025, illustrates OEM faith that full-route autonomy will unlock premium service contracts. Level 3 remains a bridging solution where regulations require fallback readiness, yet its commercial window is narrowing as regulators warm to complete driver removal in set corridors.

Investors endorse the transition: Waabi secured USD 200 million in a Series B round led by Uber and Nvidia to refine AI-first simulation, cutting road-test miles by 80%. This influx underscores the belief that scalable virtual training will speed homologation and compress time-to-revenue for Level 4 entrants. As high-definition mapping costs fall, market analysts expect Level 4 to pass 30% share of active freight miles by 2030, reshaping asset-scheduling logic and insurance underwriting norms.

The Autonomous Truck Market is Segmented by Truck Type (Light-Duty Trucks, and More), Level of Autonomy (SAE Level 1-2 (Driver Assist), and More), ADAS Features (Adaptive Cruise Control, Lane Departure Warning, and More), Component (LIDAR, RADAR, Cameras, and More), Drive Type (IC Engine, Battery-Electric, Hybrid, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Geography Analysis

North America captured 33.7% of the autonomous truck market share in 2024 due to permissive state-level pilot frameworks and a 48,000-mile Interstate system favoring lane-centered autonomy. Texas hosts commercial routes linking Dallas, Houston, El Paso, and Phoenix, where Aurora, Kodiak, Volvo, and DHL operate revenue-generating loads. Venture funding remains robust: start-ups raised more than USD 1 billion across 2024-2025, reflecting investor confidence in near-term monetisation.

Europe contributed roughly one-third of the 2024 revenue. Germany, Sweden, and the Netherlands spearhead testing thanks to early adoption of UNECE cybersecurity and lane-keeping directives. The Volvo-Daimler software JV positions EU OEMs to deliver over-the-air-upgradable platforms ahead of the 2026 GSR phase-in. Cross-border freight edges forward via digital corridor pilots such as Scandinavia-Hamburg, yet variable national certification timelines still hamper continent-wide scale.

Asia-Pacific remains the fastest-growing region at a 21.4% CAGR. China's Ministry of Transport endorsed nationwide smart-highway projects, enabling local players to rack up 20 million driver-out kilometres by mid-2025. Japan targets Level 4 coverage of trunk lines by 2027, pairing autonomy incentives with support for hydrogen and battery charging depots. South Korea's K-Mobility 2030 plan accelerates telematics coverage, while India eyes autonomous mining and port haulage as first-mover niches. Open-source stacks like Autoware give regional integrators a springboard to customise perception for left-hand-drive urban grids.

- AB Volvo

- Daimler Truck AG

- Traton SE

- PACCAR Inc.

- BYD Co. Ltd.

- Tesla, Inc.

- TuSimple

- Aurora Innovation

- Waymo Via

- Plus.ai

- Torc Robotics

- Kodiak Robotics

- Nikola Corp.

- Einride

- Embark Technology

- Hyzon Motors

- Gatik AI

- Volvo-Uber ATG JV

- Scania

- Navistar

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Driver shortage & rising line-haul labor cost

- 4.2.2 Demand for 24/7 hub-to-hub logistics

- 4.2.3 Tightening safety regulations (e.g., U.S. AV bills, EU GSR)

- 4.2.4 Platooning-driven fuel savings & emission mandates

- 4.2.5 Synergy of autonomy with zero-emission powertrains

- 4.2.6 Open-source autonomy stacks lowering entry barriers

- 4.3 Market Restraints

- 4.3.1 Patchwork global regulation & cross-border liability

- 4.3.2 Cyber-security & OTA update risks

- 4.3.3 High LiDAR / sensor-suite costs

- 4.3.4 Scarcity of high-resolution HD maps beyond Tier-1 corridors

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD) and Volume (Units))

- 5.1 By Truck Type

- 5.1.1 Light-Duty Trucks

- 5.1.2 Medium-Duty Trucks

- 5.1.3 Heavy-Duty Trucks

- 5.2 By Level of Autonomy

- 5.2.1 SAE Level 1-2 (Driver Assist)

- 5.2.2 SAE Level 3 (Conditional)

- 5.2.3 SAE Level 4 (High)

- 5.2.4 SAE Level 5 (Full)

- 5.3 By ADAS Feature

- 5.3.1 Adaptive Cruise Control

- 5.3.2 Lane Departure Warning

- 5.3.3 Traffic Jam Assist

- 5.3.4 Highway Pilot

- 5.3.5 Automatic Emergency Braking

- 5.3.6 Blind-Spot Detection

- 5.3.7 Lane-Keeping Assist

- 5.4 By Component

- 5.4.1 LiDAR

- 5.4.2 RADAR

- 5.4.3 Cameras

- 5.4.4 Ultrasonic & Other Sensors

- 5.4.5 AI Compute Modules

- 5.5 By Drive Type

- 5.5.1 Internal-Combustion

- 5.5.2 Battery-Electric

- 5.5.3 Hybrid

- 5.5.4 Hydrogen Fuel-Cell

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Spain

- 5.6.3.5 Russia

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 GCC

- 5.6.5.2 Turkey

- 5.6.5.3 South Africa

- 5.6.5.4 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 AB Volvo

- 6.4.2 Daimler Truck AG

- 6.4.3 Traton SE

- 6.4.4 PACCAR Inc.

- 6.4.5 BYD Co. Ltd.

- 6.4.6 Tesla, Inc.

- 6.4.7 TuSimple

- 6.4.8 Aurora Innovation

- 6.4.9 Waymo Via

- 6.4.10 Plus.ai

- 6.4.11 Torc Robotics

- 6.4.12 Kodiak Robotics

- 6.4.13 Nikola Corp.

- 6.4.14 Einride

- 6.4.15 Embark Technology

- 6.4.16 Hyzon Motors

- 6.4.17 Gatik AI

- 6.4.18 Volvo-Uber ATG JV

- 6.4.19 Scania

- 6.4.20 Navistar

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

自动驾驶卡车市场:2026-2032年全球市场预测(按自动驾驶等级、卡车类型、动力传动系统类型和应用划分)

自动驾驶卡车市场:2026-2032年全球市场预测(按自动驾驶等级、卡车类型、动力传动系统类型和应用划分) 互联车队管理市场:策略洞察与预测(2026-2031 年)自动驾驶卡车市场规模、份额、成长及全球产业分析:按类型、应用和地区划分,并对2026-2034年进行预测

互联车队管理市场:策略洞察与预测(2026-2031 年)自动驾驶卡车市场规模、份额、成长及全球产业分析:按类型、应用和地区划分,并对2026-2034年进行预测 2025-2029年全球自动驾驶卡车市场

2025-2029年全球自动驾驶卡车市场 半自动和全自动卡车市场-全球产业规模、份额、趋势、机会和预测(按ADAS功能、自动驾驶等级、组件、应用、燃料类型、地区和竞争格局划分),2021-2031年全球自动驾驶场内卡车解决方案市场(按车辆类型、动力系统、有效载荷能力、自动驾驶等级、连接技术、应用和最终用户划分),2026-2032 年预测全球自动驾驶卡车市场-按车辆类型、动力类型、组件类型、自动驾驶等级、地区和竞争格局分類的产业规模、份额、趋势、机会和预测(2021-2031年预测)

半自动和全自动卡车市场-全球产业规模、份额、趋势、机会和预测(按ADAS功能、自动驾驶等级、组件、应用、燃料类型、地区和竞争格局划分),2021-2031年全球自动驾驶场内卡车解决方案市场(按车辆类型、动力系统、有效载荷能力、自动驾驶等级、连接技术、应用和最终用户划分),2026-2032 年预测全球自动驾驶卡车市场-按车辆类型、动力类型、组件类型、自动驾驶等级、地区和竞争格局分類的产业规模、份额、趋势、机会和预测(2021-2031年预测) 自动驾驶卡车市场规模、份额和趋势分析报告:按动力类型、车辆类型、自动驾驶等级、感测器类型、应用、ADAS功能、地区和细分市场预测(2026-2033年)

自动驾驶卡车市场规模、份额和趋势分析报告:按动力类型、车辆类型、自动驾驶等级、感测器类型、应用、ADAS功能、地区和细分市场预测(2026-2033年) 2032 年自动驾驶卡车市场预测:按卡车类型、自动化程度、零件、推进系统、应用、最终用户和地区进行的全球分析

2032 年自动驾驶卡车市场预测:按卡车类型、自动化程度、零件、推进系统、应用、最终用户和地区进行的全球分析 B2B 互联车队服务的全球市场

B2B 互联车队服务的全球市场