|

市场调查报告书

商品编码

1851424

快速消费品包装:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)FMCG Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

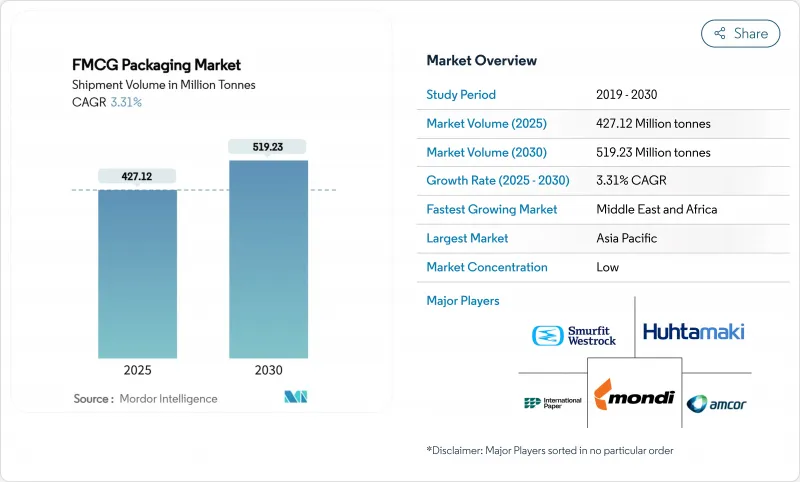

预计到 2025 年,快速消费品包装市场将达到 4.2712 亿吨,到 2030 年将扩大到 5.1923 亿吨,年复合成长率为 3.31%。

成长的驱动力来自家庭对基本包装的稳定需求、不断扩大的电子商务交易量以及鼓励使用可回收和可重复填充解决方案的政策措施。大型加工商正在重新设计包装形式,以减少材料用量和运输成本,同时保护商品在更长、更复杂的供应链中流通。生物基基材和化学回收树脂正从试点阶段走向商业化生产,但塑胶因其阻隔性和轻质特性仍然至关重要。亚太地区的需求成长主要得益于快速的都市化和家庭消费规模的缩小,而中东和非洲地区则由于现代零售业的普及,经历了最快的吨位增长。

全球快速消费品包装市场趋势与洞察

电子商务的快速成长需要轻巧、防护性强的包装。

如今,线上零售商在组装包装设计方案时,会重点考虑小包裹的耐用性、尺寸重量限制以及便捷的退货流程。品牌拥有者则指定使用缓衝邮件袋、气柱袋和客製尺寸的纸箱,以减少包装空隙和降低运费。包装厂正在增设数位印刷生产线,使每个托运人都能携带可扫描的条码,用于验证真伪或触发补货服务。能够显示衝击和温度不当情况的智慧指示器正逐渐成为高端包装的标配,而小包裹保险公司为可追溯包装提供更低保费的做法也进一步强化了这一趋势。这些需求持续推高了对柔性薄膜和瓦楞纸板的需求,促使树脂供应商开发出能够保持其机械性能的可直接替代型再生树脂。

亚洲都市区单份消费的蓬勃发展推动了便利商店业态的发展

在中国、印度和东南亚,单人家庭的增加和交通拥堵正在推动分装袋、杯装和小袋包装食品的普及。製造商正在实现高速灌装封口生产线的自动化,从而在价格分布竞争的同时,减少因大包装产品部分使用而造成的食物废弃物。零售商正在为可重复密封的零食包装和单份即食食品分配更多货架空间,这促使加工商加强隔离层确保内容物新鲜直至最后一份。这种成长趋势也蔓延至家居和个人保养用品,可重复填充的胶囊和便于携带的迷你包装迎合了忙碌的都市生活方式。对兼具易撕口和抗摔性能的复合材料的需求,正在推动亚洲产能的显着增长。

树脂价格波动会为规划带来不确定性。

原油和石脑油基准价格的波动扰乱了季度合约谈判,迫使加工商对冲原料风险或加快回收和生物基替代。规模较小的公司难以负担价格飙升,利润空间受到挤压,资本支出放缓。特种添加剂的突然短缺(通常与地缘政治事件相关)迫使企业临时调整配方,从而导致停工和客户罚款。为因应这种情况,跨国公司会分散采购管道并签订多年供应协议,同时财务团队会实施与产业基准挂钩的成本转嫁条款。这种动盪局面有利于拥有综合树脂资产和充足营运成本的製造商。

细分市场分析

预计到2024年,塑胶仍将占据快速消费品包装市场62.45%的份额,这反映了其无与伦比的强度重量比和广泛的加工性能。生物基和可堆肥塑胶虽然仍处于小众市场,但随着加工商将具有增强氧气和水分阻隔性能的PLA和PHA共混物商业化,其市场份额正以6.85%的复合年增长率增长。由于可无限循环利用,硬金属在高端饮料包装领域备受青睐;而纸板在干货和个人保健产品领域市场份额不断扩大,因为这些领域可以使用纤维基壁材。在快速消费品包装市场,聚乙烯和聚丙烯因其成本效益,仍是柔性复合材料的首选材料。然而,化学回收目前在北美和欧洲正在蓬勃发展,高品质的消费后树脂有望缓解原生塑胶的需求。反应涂层生产线的创新使得纸杯无需塑胶内衬即可盛装酸性果汁,从而为塑胶替代开闢了新的途径。

塑胶供应商正透过推出经认证的循环利用型聚乙烯(PE)和热解(PP)产品来应对永续性压力,这些产品源自于热解油,为品牌商提供了一种无需更换即可减少排放且无需更换现有生产线的便捷途径。随着政府绿色采购政策的逐步实施,预计到2030年,生物基树脂在快速消费品包装市场的市场规模将超过800万吨。同时,铝材在气雾罐和宠物食品托盘等产品中的轻盈优势,恰好满足了需要经久耐用、可多次循环使用的填充站的需求。玻璃在对口味完整性要求极高的领域仍然占有一席之地,但由于重量和易碎性等问题,其市场份额受到限制。总而言之,材料的选择取决于功能性能、法规遵循和整体碳排放影响之间的平衡,而不仅仅是单位成本。

到2024年,软包装将以54.65%的市占率主导快速消费品包装市场,并在2030年之前以6.35%的复合年增长率成长。品牌拥有者看重的是软包装低材料与产品比、高图形表现力以及更高的包装效率,这使得每个托盘可以容纳更多产品。电子商务的兴起推动了对便于邮寄的枕形包装和无需额外填充即可承受自动化分类的多层包装袋的需求。零嘴零食和糖果甜点产品正透过连续运动的水平成形充填密封(HFFS)生产线以每分钟超过1500包的速度进行生产,这凸显了递归式包装优化带来的营运优势。

在结构和可重复密封性至关重要的细分市场中,硬质容器仍然占据主导地位。 PET宝特瓶是碳酸饮料的首选包装,而玻璃瓶则代表高檔酱料的质感。采用模压盖的「硬质-软质」混合型包装袋设计融合了两种材质的优点,与同等尺寸的玻璃容器相比,重量最多可减轻70%。快速消费品硬包装的市场规模预计将以个位数低成长率成长,这反映出成熟品类的市场饱和,但可重复灌装的个人护理用品分配器领域则蕴藏着新的机会。设备製造商现在提供模组化填充模组,可在同一生产线上加工灌装好的包装袋、罐子和瓶子,使加工商能够对冲不同包装形式之间的需求波动。

快速消费品包装市场报告按材料类型(纸/纸板、塑胶、金属、玻璃、生物基和可堆肥材料)、包装类型(软包装、硬包装)、最终用途行业(食品、食品饮料、个人护理和化妆品、其他)、分销管道(直销、间接销售)和地区进行细分。市场预测以吨为单位。

区域分析

到2024年,亚太地区将占全球出货量的45.63%,成为快速消费品包装市场的核心。中国和印度将凭藉其树脂裂解厂、薄膜挤出厂和加工厂集群,满足庞大的国内需求并支撑出口。都市区微型厨房和便利的饮食习惯正在推动单份包装袋的普及,而各国减少塑胶用量的政策则加速了纸基软包装的试验。可支配所得的成长正促使个人护理产品转向高端包装,进而提升人均包装强度。在印度和东南亚,政府支持的低温运输将进一步推动保温运输箱和防篡改密封件的需求。

北美市占率持续保持稳定,这主要得益于电子商务的普及和瓦楞纸包装产能的成长。 Smurfit 和 WestRock 的合併案价值 200 亿美元,体现了企业透过扩大规模来降低固定成本、为循环经济研发提供资金的策略。例如,Green Bay Packaging 在阿肯色州投资 10 亿美元兴建的牛皮箱纸板厂,增强了国内供应的稳定性,并拓展了轻质衬板产品线。美国各州关于饮料容器中再生材料含量的法规,促进了 PET 回收计划的发展,并鼓励当地加工商取得 rPET 原料。加拿大和墨西哥预计将从近岸外包中获益,近岸外包是指将消费品填充生产线转移到更靠近核心需求地的地区。

欧洲成熟市场正利用技术创新来满足包装废弃物法规中严格的可回收性目标。德国和法国正在升级其物料回收设施和化学回收检测设施,以达到再生材料含量的最低标准。高端糖果甜点品牌正选择使用具有生物阻隔性能的纤维性包装,而英国超级市场正在进行可重复填充试用,以测试消费者对可回收包装袋的接受度。这些措施将保持包装吨位的稳定,但将价值重心转移到更高规格的材料和相关的数位化服务。

儘管基数较低,但中东和非洲地区仍将以6.58%的复合年增长率实现最快增长,这主要得益于有组织零售业的扩张以及人口增长带动包装食品需求的增长。海湾国家将投资建造先进的弹性生产线,以满足国内速食连锁店和出口订单的需求。南非和肯亚将吸引行动牛奶和果汁纸盒填充设备,从而延长无冷藏地区的保质期。来自欧洲和亚洲的外国直接投资将引进多层挤出技术,以提升当地产能。

在南美洲,巴西和哥伦比亚的经济改革提振了消费支出,推动了消费的稳定成长。巴西以甘蔗为原料的生物基聚乙烯(bioPE)产能也使全球品牌能够专注于可再生材料。关税结构持续影响工厂位置决策,促使加工商采取跨国布局,业务遍及南方共同市场和太平洋联盟。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 电子商务的快速成长需要既能提供保护又轻巧的包装。

- 亚洲都市区单份消费的蓬勃发展推动了便利商店业态的兴起

- 即饮饮料的快速成长推动了高阻隔袋的应用。

- 个人护理产品的优质化推动了智慧化和装饰性包装的发展

- 新兴市场低温运输的扩展将推动多层薄膜的使用。

- 市场限制

- 树脂价格波动会为规划带来不确定性。

- 开发中国家缺乏回收基础设施

- 一次性塑料禁令也波及传统软塑胶

- 供应链分析

- 监理展望

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 依材料类型

- 纸和纸板

- 塑胶

- 聚乙烯(低密度聚乙烯/高密度聚乙烯)

- 聚丙烯(PP)

- 聚对苯二甲酸乙二醇酯(PET)

- 其他塑胶(PVC、PS 等)

- 金属

- 玻璃

- 生物基和可堆肥材料

- 按包装类型

- 软包装

- 小袋和袋子

- 薄膜和包装

- 其他软包装

- 硬包装

- 瓶子和罐子

- 能

- 托盘和容器

- 其他硬质包装

- 软包装

- 按最终用途行业划分

- 食物

- 饮料

- 个人护理和化妆品

- 家居用品

- 医药和医疗保健

- 其他终端用户产业

- 透过分销管道

- 直销

- 间接销售

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲和纽西兰

- 亚太其他地区

- 中东和非洲

- 中东

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 埃及

- 其他非洲地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Amcor plc

- Ball Corporation

- Mondi Group

- International Paper Co.

- Sealed Air Corporation

- Constantia Flexibles

- Smurfit Westrock Plc

- Crown Holdings Inc.

- Coveris Holdings SA

- Graphic Packaging International LLC

- Tetra Pak International

- Stora Enso Oyj

- Sonoco Products Co.

- Huhtamaki Oyj

- Toyo Seikan Group HD

- Nampak Ltd

- Mpact Pty Ltd

- Albea SA

- Owens-Illinois(OI)

- Verallia SA

- Napco National

- 3P Gulf Group

第七章 市场机会与未来展望

The FMCG packaging market reached 427.12 million tonnes in 2025 and is forecast to climb to 519.23 million tonnes by 2030, advancing at a 3.31% CAGR.

Growth rests on steady household demand for packaged essentials, expanding e-commerce volumes, and policy measures that reward recyclable and refillable solutions. Large converters are redesigning formats to trim material use and freight costs while protecting goods that travel through longer, more complex supply chains. Bio-based substrates and chemical-recycled resins are moving from pilot to commercial scale, yet plastics remain indispensable in high-barrier and lightweight roles. Regional demand is led by Asia-Pacific thanks to rapid urbanization and small-household purchasing, while Middle East and Africa (MEA) offers the quickest tonnage expansion as modern retail spreads.

Global FMCG Packaging Market Trends and Insights

Rapid Growth of E-commerce Requiring Protective, Lightweight Packs

Online retail now frames design briefs around parcel durability, dimensional weight limits, and friction-free returns. Brand owners specify cushioned mailers, air-column pouches, and fit-to-size cartons that slash void space and freight spend. Packaging plants add digital print lines so each shipper can carry scannable codes that confirm authenticity or trigger replenishment services. Smart indicators that reveal impact or temperature misuse are becoming standard on premium categories, a trend reinforced by parcel insurers who offer lower premiums for traceable packs. These needs keep flexible films and corrugated board in high demand and encourage resin suppliers to accelerate drop-in recycled grades that retain mechanical properties.

Urban Single-Serve Consumption Boom in Asia Boosting Convenience Formats

Rising numbers of single-person households and congested commutes in China, India, and Southeast Asia spur uptake of portion-controlled pouches, cups, and sachets. Manufacturers are automating high-speed fill-seal lines to reach price points competitive with bulk packs while trimming food waste from partially used larger units. Retailers dedicate premium shelf space to resealable snack packs and ready-to-eat meals sized for one, pushing converters to enhance barrier layers that keep contents fresh until the last serving. Growth spills into home-care and personal-care items, where refill pods and travel-friendly minis fit hectic urban lifestyles. Demand for laminates that couple easy-tear openings with drop-resistance underpins a notable slice of incremental Asian capacity additions.

Resin Price Volatility Creating Planning Uncertainty

Fluctuating crude-oil and naphtha benchmarks upset quarterly contract negotiations, prompting converters to hedge feedstock or accelerate substitution toward recycled and bio-based grades. Smaller firms lacking scale struggle to absorb spikes, which compress margins and slow capital investment. Sudden shortages of specialty additives, often linked to geopolitical events, force ad-hoc reformulations that risk downtime and customer penalties. In response, multinationals diversify sourcing and lock in multi-year supply pacts, while financial teams roll out cost-pass-through clauses keyed to industry indices. Such turbulence favors producers with integrated resin assets and strong working-capital positions.

Other drivers and restraints analyzed in the detailed report include:

- RTD Beverage Surge Driving High-Barrier Pouch Adoption

- Premiumisation in Personal-Care Triggering Smart and Decorative Packs

- Single-Use-Plastic Bans Dampening Conventional Flexibles

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Plastics maintained a 62.45% share of the FMCG packaging market in 2024, reflecting unmatched strength-to-weight ratios and broad processability. Bio-based and compostable grades, though still niche, are expanding at 6.85% CAGR as converters commercialize PLA and PHA blends with enhanced oxygen and moisture barriers. Rigid metals find favor in premium beverage lines for infinite recyclability, and paperboard gains share where dry food or personal-care formats permit fiber-based walls. The FMCG packaging market continues to favor polyethylene and polypropylene in flexible laminates thanks to cost efficiency, but chemical recycling, now scaling in North America and Europe, promises high-quality post-consumer resins that moderate virgin demand. Innovations in reactive coating lines let paper cups hold acidic juices without plastic liners, opening another pathway for plastics displacement.

Plastics suppliers counter sustainability pressures by launching certified-circular PE and PP grades derived from pyrolysis oil, giving brand owners a drop-in route to lower emissions while retaining incumbent converting lines. The FMCG packaging market size for bio-based resins is projected to surpass 8 million tonnes by 2030 as governmental green-procurement rules take hold. Meanwhile, aluminum's light-weight advantage in aerosol cans and pet-food trays aligns with refill stations that prefer robust formats surviving multiple cycles. Glass stays relevant where taste neutrality is prized, yet weight and breakage limit its volume share. Overall, material choice now hinges on balancing functional performance, regulatory compliance, and total carbon impact rather than unit price alone.

With a 54.65% share in 2024, flexible formats dominate the FMCG packaging market and are tracking a 6.35% CAGR to 2030. Brand owners value lower material-to-product ratios, high graphics potential, and pack-out efficiency that allows more units per pallet. The shift to e-commerce adds demand for mail-friendly pillow packs and multi-layer sachets that endure automated sortation without extra void fill. Continuous-motion horizontal form-fill-seal (HFFS) lines supply snack and confectionery categories at speeds exceeding 1,500 packs per minute, highlighting the operational gains that recursive format optimisation delivers.

Rigid options still command niches where structure and reclosability are critical. PET bottles retain leadership in carbonated soft drinks, while glass jars project premium cues in gourmet sauces. Hybrid "rigid-in-flexible" pouch designs with molded caps combine both worlds, slicing weight by up to 70% versus equivalently sized glass containers. The FMCG packaging market size for rigid formats is forecast to post low-single-digit growth, reflecting saturation in mature categories but fresh opportunities in refillable personal-care dispensers. Equipment builders now offer modular filler blocs that handle fitment pouches, jars, and bottles on one line, letting converters hedge against demand swings across formats.

The FMCG Packaging Market Report is Segmented by Material Type (Paper and Paperboard, Plastics, Metal, Glass, Bio-Based and Compostable Materials), Packaging Type (Flexible Packaging, Rigid Packaging), End-Use Industry (Food, Beverages, Personal Care and Cosmetics, and More), Distribution Channel (Direct Sales, Indirect Sales), and Geography. The Market Forecasts are Provided in Terms of Volume (Tonnes).

Geography Analysis

Asia-Pacific generated 45.63% of 2024 shipments, positioning the region as the anchor of the FMCG packaging market. China and India supply mammoth domestic demand and serve export flows, leveraging clusters of integrated resin crackers, film extruders, and converting plants. Urban micro-kitchens and on-the-go eating habits fuel single-serve pouch uptake, while national plastic-reduction mandates accelerate trials of paper-based flexibles. Rising disposable incomes enable trading-up to premium personal-care formats, deepening per-capita packaging intensity. Government-backed cold-chain corridors in India and Southeast Asia unleash further need for insulated shippers and tamper-evident seals.

North America follows with a stable share rooted in broad e-commerce penetration and advanced corrugated capacity. The Smurfit-WestRock merger, valued at USD 20 billion, exemplifies the push for scale to dilute fixed costs and fund circular-economy R&D. Investments such as Green Bay Packaging's USD 1 billion kraft linerboard mill in Arkansas strengthen domestic supply security and expand lightweight liner offerings. United States state regulations on recycled content in beverage containers catalyze PET reclaim projects, pushing local converters to lock in rPET feedstock. Canada and Mexico gain from near-shoring that relocates consumer-goods filling lines closer to core demand.

Europe's mature market taps innovation to meet its stringent recyclability targets under the Packaging and Packaging Waste Regulation. Germany and France upgrade MRFs and chemical-recycling pilots to satisfy minimum recycled-content thresholds, while brand owners redesign individual packs to pass "sort-ability" tests. Premium confectionery chooses fiber-based wrapping with bio-barriers, and UK supermarkets roll out refill trials that test shopper uptake of returnable pouches. These initiatives stabilize overall tonnage but shift value toward higher-spec materials and linked digital services.

Middle East and Africa register the fastest 6.58% CAGR, albeit from a lower base, as organized retail expands and population growth drives packaged staples. Gulf states invest in state-of-the-art flexible plants that supply both domestic fast-food chains and export orders. South Africa and Kenya attract mobile filling units for milk and juice cartons that extend shelf life in areas lacking refrigeration. Foreign direct investment from European and Asian groups introduces multilayer extrusion technology, lifting local capabilities.

South America offers steady upside as economic reforms in Brazil and Colombia revive consumer spending. Regional fiber availability supports cost-competitive corrugated, and sugar-cane-based bio-PE capacity in Brazil gives global brands a renewable-content narrative. Tariff structures still influence plant-location decisions, nudging converters to adopt multinational footprints that straddle Mercosur and Pacific Alliance blocs.

- Amcor plc

- Ball Corporation

- Mondi Group

- International Paper Co.

- Sealed Air Corporation

- Constantia Flexibles

- Smurfit Westrock Plc

- Crown Holdings Inc.

- Coveris Holdings S.A.

- Graphic Packaging International LLC

- Tetra Pak International

- Stora Enso Oyj

- Sonoco Products Co.

- Huhtamaki Oyj

- Toyo Seikan Group HD

- Nampak Ltd

- Mpact Pty Ltd

- Albea S.A.

- Owens-Illinois (O-I)

- Verallia SA

- Napco National

- 3P Gulf Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Growth of E-commerce Requiring Protective, Lightweight Packs

- 4.2.2 Urban Single-Serve Consumption Boom in Asia Boosting Convenience Formats

- 4.2.3 RTD Beverage Surge Driving High-Barrier Pouch Adoption

- 4.2.4 Premiumisation in Personal-Care Triggering Smart and Decorative Packs

- 4.2.5 Cold-Chain Expansion in Emerging Markets Raising Multilayer Film Usage

- 4.3 Market Restraints

- 4.3.1 Resin Price Volatility Creating Planning Uncertainty

- 4.3.2 Recycling-Infrastructure Deficit in Developing Nations

- 4.3.3 Single-Use-Plastic Bans Dampening Conventional Flexibles

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VOLUME)

- 5.1 By Material Type

- 5.1.1 Paper and Paperboard

- 5.1.2 Plastics

- 5.1.2.1 Polyethylene (LDPE/HDPE)

- 5.1.2.2 Polypropylene (PP)

- 5.1.2.3 Polyethylene Terephthalate (PET)

- 5.1.2.4 Other Plastics (PVC, PS,etc)

- 5.1.3 Metal

- 5.1.4 Glass

- 5.1.5 Bio-based and Compostable Materials

- 5.2 By Packaging Type

- 5.2.1 Flexible Packaging

- 5.2.1.1 Pouches and Bags

- 5.2.1.2 Films and Wraps

- 5.2.1.3 Other Flexible Packaging

- 5.2.2 Rigid Packaging

- 5.2.2.1 Bottles and Jars

- 5.2.2.2 Cans

- 5.2.2.3 Trays and Containers

- 5.2.2.4 Other Rigid Packaging

- 5.2.1 Flexible Packaging

- 5.3 By End-use Industry

- 5.3.1 Food

- 5.3.2 Beverages

- 5.3.3 Personal Care and Cosmetics

- 5.3.4 Household Care Products

- 5.3.5 Pharmaceuticals and Healthcare

- 5.3.6 Other End-use Industry

- 5.4 By Distribution Channel

- 5.4.1 Direct Sales

- 5.4.2 Indirect Sales

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia and New Zealand

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 Middle East

- 5.5.4.1.1 United Arab Emirates

- 5.5.4.1.2 Saudi Arabia

- 5.5.4.1.3 Turkey

- 5.5.4.1.4 Rest of Middle East

- 5.5.4.2 Africa

- 5.5.4.2.1 South Africa

- 5.5.4.2.2 Nigeria

- 5.5.4.2.3 Egypt

- 5.5.4.2.4 Rest of Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Amcor plc

- 6.4.2 Ball Corporation

- 6.4.3 Mondi Group

- 6.4.4 International Paper Co.

- 6.4.5 Sealed Air Corporation

- 6.4.6 Constantia Flexibles

- 6.4.7 Smurfit Westrock Plc

- 6.4.8 Crown Holdings Inc.

- 6.4.9 Coveris Holdings S.A.

- 6.4.10 Graphic Packaging International LLC

- 6.4.11 Tetra Pak International

- 6.4.12 Stora Enso Oyj

- 6.4.13 Sonoco Products Co.

- 6.4.14 Huhtamaki Oyj

- 6.4.15 Toyo Seikan Group HD

- 6.4.16 Nampak Ltd

- 6.4.17 Mpact Pty Ltd

- 6.4.18 Albea S.A.

- 6.4.19 Owens-Illinois (O-I)

- 6.4.20 Verallia SA

- 6.4.21 Napco National

- 6.4.22 3P Gulf Group

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

居家照护包装市场规模、份额、趋势和预测:按产品类型、材料、包装形式和地区划分,2026-2034年

居家照护包装市场规模、份额、趋势和预测:按产品类型、材料、包装形式和地区划分,2026-2034年 快速消费品包装市场规模、份额、成长及全球产业分析:按类型、应用和地区划分,并预测至2026-2034年日常消费品包装市场规模、份额、趋势及预测(按包装类型、材料、最终用途行业和地区划分,2026-2034年)

快速消费品包装市场规模、份额、成长及全球产业分析:按类型、应用和地区划分,并预测至2026-2034年日常消费品包装市场规模、份额、趋势及预测(按包装类型、材料、最终用途行业和地区划分,2026-2034年) 2026年全球居家护理产品包装市场报告

2026年全球居家护理产品包装市场报告 月饼包装市场:2026-2032年全球预测(按包装类型、材料、包装形式、印刷技术、最终用户和分销管道划分)

月饼包装市场:2026-2032年全球预测(按包装类型、材料、包装形式、印刷技术、最终用户和分销管道划分) 欧洲消费品包装市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031年)居家护理包装市场-2026-2031年预测

欧洲消费品包装市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031年)居家护理包装市场-2026-2031年预测 家居护理包装市场规模、份额及成长分析(按材料、产品类型、包装类型、最终用途和地区划分)-产业预测(2026-2033)

家居护理包装市场规模、份额及成长分析(按材料、产品类型、包装类型、最终用途和地区划分)-产业预测(2026-2033) 快速消费品包装市场规模、份额、成长分析(按类型、材料、最终用途和地区)- 2025-2032 年产业预测

快速消费品包装市场规模、份额、成长分析(按类型、材料、最终用途和地区)- 2025-2032 年产业预测 全球居家护理包装市场

全球居家护理包装市场