|

市场调查报告书

商品编码

1851425

热交换器:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)Heat Exchanger - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

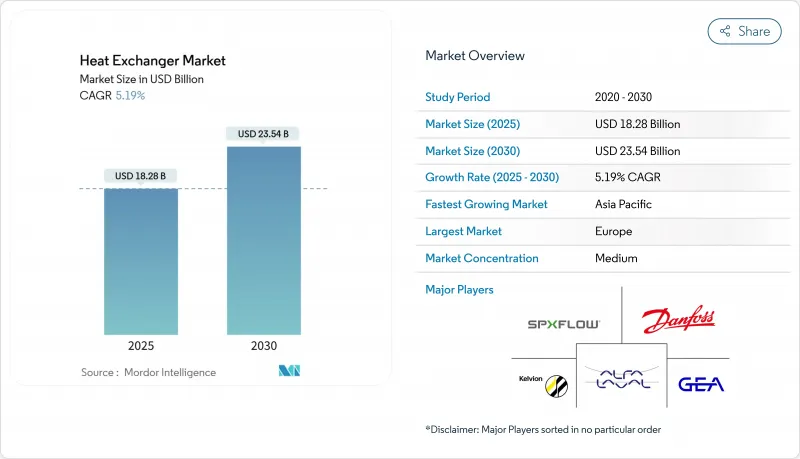

据估计,到 2025 年,热交换器市场规模将达到 182.8 亿美元,预计到 2030 年将达到 235.4 亿美元,在预测期(2025-2030 年)内,复合年增长率将达到 5.19%。

液化天然气基础设施的建设、资料中心液冷技术的应用以及鼓励提高工业锅炉和区域能源网路效率的法规,共同推动了产业成长。儘管壳管式技术仍然是高压应用的主流,但随着节水概念的推动,空冷设备正迅速普及。氢气先导计画和超临界二氧化碳动力循环正在推动对特种合金的需求,而模组化印刷电路设计在极端压力和空间限制并存的领域也越来越受欢迎。同时,专业製造商正瞄准低温液化天然气装置和200巴氢气装置等细分市场。

全球热交换器市场趋势与洞察

液化天然气计划激增带动低温热交换器需求成长

全球中大型液化天然气(LNG)装置的建造需要能够在低于-150 度C的温度下运作并满足严格热性能要求的盘管式和板翅式热交换器,这加速了对高等级不銹钢和铝合金的采购。模组化热交换器撬装设备缩短了工期,减少了成本超支,并使采用3D列印流板以减轻重量和增强湍流的製造商受益。预计2025年至2026年,墨西哥湾沿岸和卡达的大型企划将主导热交换器市场,而亚洲各地棕地改造带来的额外需求也将推动市场成长。拥有ASME第八卷认证且交货週期为12週的供应商有望获得框架合同,因为EPC公司正在规范设备清单以降低工期风险。

海湾合作委员会和东南亚地区冷冻业务的扩张推动了平板车销售。

在杜拜、利雅德和新加坡等潮湿的都市区,为了降低电力高峰负荷,政府持续补贴区域冷却系统,促使电力公司指定使用垫片式板框热交换器,因为这种热交换器体积小巧且易于扩容。这些热交换器采用不銹钢或钛合金板片来防止海水腐蚀,区域运营商要求99%的可用性保证。随着特许经营业者转向基于绩效的维护模式,捆绑状态监测感测器的特许经营设备製造商(OEM)有望获得持续的业务收益。

镍和钛价格波动促进了耐腐蚀单元的发展

自2024年以来,一级镍和航太级钛的价格环比波动高达35%,这削弱了氢能、海洋和海上计划的订单量,因为这些项目的材料规格无法降低。加工商将额外费用转嫁给EPC客户,但预算超支导致计划延期,近期热交换器市场销售萎缩。不銹钢复合板可以部分抵消价格波动的影响,但异种金属的扩散焊接使焊接完整性认证变得复杂。

细分市场分析

到2024年,壳管式热交换器将占据35%的市场份额,在压力超过60巴且结垢容差较高的情况下,它仍将是首选方案。 TEMA标准化分类简化了炼油厂、液化天然气预处理装置和硫磺回收装置的规格,从而促进了管束和垫片的重复订单,进而增加了售后市场收入。同时,由于印度、德克萨斯和中东等缺水地区的电力公司优先考虑零液体排放策略,并采用强制通风风机和低噪音齿轮箱驱动机组,空冷式热交换器的年复合成长率达到了6%。

从2025年到2030年,随着设计人员寻求传统壳体无法满足的紧凑型设计,印刷电路板式和螺旋缠绕式热交换器可能会在高压氢气和超临界二氧化碳循环领域蚕食市场份额。儘管如此,对于现有设施的维修,棕地市场仍将继续青睐壳管式热交换器,因为现有喷嘴位置可以纳入改造方案,且生命週期成本更容易预测。采用不銹钢壳体和铜镍管的船舶洗涤器将满足IMO 2020合规预算的需求,从而推动销售量小幅成长。

到2024年,不锈钢将维持30%的热交换器市场份额。在食品饮料和製药行业,其卫生级表面处理和低碳含量使製造商无需使用更昂贵的合金即可满足法规要求。钛、镍、因科洛伊合金和哈氏合金等特殊合金到2030年将以6.5%的复合年增长率增长,用于氢气捕获、海水淡化和海上风力发电平台等应用,在这些应用中,由于氯化物含量高的盐水和氢脆问题,不銹钢不再适用。

聚合物和复合材料从微小基体开始生长,例如聚四氟乙烯(PTFE)和石墨块在强酸性或含氟流体中性能优于金属,尤其是在半导体湿蚀刻和锂离子电池回收领域。积层製造技术能够建造双材料晶格,仅在腐蚀风险高的区域使用高合金材料,从而降低成本和重量。诸如此类的创新正推动热交换器产业超越传统的不銹钢材料范畴,迈向应用导向冶金技术。

热交换器市场报告按类型(壳管式、板框式、空冷式、其他)、结构材料(不銹钢、碳钢、其他)、流动布置(逆流式、并流式、交叉流式、混合/多通道式)、终端用户行业(石油和天然气、发电、水和污水处理、其他)以及地区(北美、亚太、南美、其他)进行细分。

区域分析

到2024年,欧洲将占全球销售额的33%,这主要得益于欧盟的生态设计指令,该指令旨在促进锅炉维修和区域能源部署。德国的综合氢能策略正将资金投入电解槽工厂的印刷电路原型研发中,从而支撑了热交换器市场的高价值领域。法国正在加速推进小型模组化反应器(SMR)计划需要紧凑型安全等级的热交换器;而北欧国家则率先开发利用钛板组件和环境海水的低温区域循环系统。随着执行时间保证在竞标评分中占据重要地位,持有EN13445压力容器认证的原始设备製造商(OEM)和区域备件中心将获得更多市场份额。

亚太地区到2030年将以5.9%的复合年增长率实现最快增速,销量增长主要得益于中国石化产能扩张、印度电力装机容量扩张以及东盟区域供冷权益。国内製造商正利用成本优势的供应链赢得壳管式冷凝器订单,而日韩企业则专注于为氨裂解中试装置生产钛镍基冷凝器。本地工程总承包商重视能够提供10週或更短交货期的模组化撬装设备的供应商,迫使全球品牌将生产在地化。

北美受益于墨西哥湾沿岸的液化天然气出口终端以及维吉尼亚、德克萨斯州和魁北克省的资料中心园区扩建。美国能源局氢能中心为采用扩散焊接镍合金的粉末煤气化装置(PCHE)示范试验提供津贴。加拿大油砂业者正在维修气动翅片装置,以减少用水量并为风扇辅助设备创建二次吸力。在拉丁美洲,采矿精矿和太阳热能发电发电厂正在推动精品订单,而中东的海水淡化和石化大型综合体则支撑着需求。非洲的成长动能虽然不强劲,但十分稳健,这得益于铜带地区冶炼厂的升级改造。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 液化天然气计划激增带动低温热交换器需求成长

- 海湾合作委员会和东南亚地区区域冷却的扩张推动了平板车架的销售

- 氢气中试装置采用印刷电路板式热交换器,工作压力为 200 巴

- 欧盟强制工业锅炉升级改造重点在于改造管束

- 小型模组化反应器(SMR)部署需要小型、安全的热交换器。

- 资料中心液冷部署加速微通道技术的应用

- 市场限制

- 镍和钛的价格波动推高了耐腐蚀部件的价格。

- 生物製程的结垢问题限制了其在生物炼製厂的应用。

- EPC对12週前置作业时间的需求抑制了订单订单设计。

- 直接空气冷却会蚕食发电厂中的空冷式热交换器。

- 供应链分析

- 监理展望

- 技术展望

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 按类型

- 壳管

- 板材及框架(垫片板、硬焊板、焊接板)

- 空气冷却(翅片管式、板翅式、微通道式)

- 再生式(旋转式和平板式)

- 印刷电路

- 其他(双管、螺旋、同轴)

- 按建筑材料

- 防锈的

- 碳钢

- 有色金属(铜、铝)

- 特殊合金(钛、镍、哈氏合金)

- 聚合物和复合材料(聚四氟乙烯、石墨、陶瓷)

- 按流程布置

- 反向电流

- 平行线

- 交叉流

- 混合/多路径

- 按最终用途行业划分

- 石油和天然气

- 化工/石油化工

- 发电(包括核能)

- 饮食

- 纸浆和造纸

- 水和污水处理

- 其他产业(汽车及运输、冶金、采矿、暖通空调冷冻、製药及生技)

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 北欧国家

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 东南亚国协

- 澳洲

- 亚太其他地区

- 南美洲

- 巴西

- 阿根廷

- 智利

- 哥伦比亚

- 其他南美洲

- 中东和非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 南非

- 埃及

- 其他中东和非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略性倡议(併购、伙伴关係、购电协议)

- 市场占有率分析(主要企业的市场排名/份额)

- 公司简介

- Alfa Laval AB

- Kelvion Holding GmbH

- Danfoss A/S

- SPX Flow Inc.

- GEA Group AG

- Hisaka Works Ltd.

- Xylem Inc.

- Thermax Ltd.

- Mersen SA

- API Heat Transfer Inc.

- GE Vernova Inc.

- Barriquand Technologies Thermiques SAS

- Koch Heat Transfer Company LP

- SWEP International AB

- Heatric

- Kobelco Steel Ltd.

- Accessen Group

- Funke WarmeaustauscherGmbH

- Tranter Inc.

- HRS Heat Exchangers Ltd.

- Hamon Thermal Europe SA

- Graham Corporation

- United Heat Transfer Ltd.

- KRN Heat Exchanger & Refrigeration Ltd.

第七章 市场机会与未来展望

The Heat Exchanger Market size is estimated at USD 18.28 billion in 2025, and is expected to reach USD 23.54 billion by 2030, at a CAGR of 5.19% during the forecast period (2025-2030).

Growth is fueled by LNG infrastructure build-outs, data-center liquid-cooling adoption, and regulations that force efficiency upgrades in industrial boilers and district energy networks. Shell-and-tube systems remain the mainstay for high-pressure duties, yet air-cooled equipment is scaling rapidly as water conservation drives procurement decisions. Exotic alloy demand rises in line with hydrogen pilot projects and super-critical CO2 power cycles, while modular printed-circuit designs gain traction where extreme pressures converge with space constraints. Competitive dynamics stay moderately fragmented: global incumbents rely on broad portfolios and aftermarket reach, whereas specialists target niches such as cryogenic LNG trains and 200-bar hydrogen units.

Global Heat Exchanger Market Trends and Insights

Surge in LNG Liquefaction Projects Boosting Demand for Cryogenic Exchangers

Global build-outs of mid-scale and large LNG trains require coil-wound and plate-fin units that perform below -150 °C while maintaining tight thermal approaches, accelerating procurement of high-grade stainless steels and aluminum alloys . Modular exchanger skids shorten construction schedules and curb cost overruns, benefiting fabricators integrating 3D-printed flow plates for weight reduction and enhanced turbulence. During 2025-2026, Gulf Coast and Qatari megaprojects are expected to anchor the heat exchanger market, with secondary demand arising from brownfield debottlenecking across Asia. Suppliers that certify to ASME Section VIII while offering 12-week delivery windows will secure framework contracts as EPC firms standardize equipment lists to de-risk timelines.

District-Cooling Expansion in GCC & Southeast Asia Driving Plate-Frame Sales

High-humidity metros such as Dubai, Riyadh, and Singapore continue to subsidize district-cooling systems to shave peak power loads, prompting utilities to specify gasketed plate-frame exchangers owing to compact footprints and easy capacity scaling . These deployments rely on stainless and titanium plates to mitigate brine corrosion, with district operators demanding 99% availability guarantees. OEMs that bundle condition-monitoring sensors will capture recurring service revenue as concession operators pivot toward performance-based maintenance models.

Nickel and Titanium Price Volatility Inflating Corrosion-Resistant Units

Class 1 nickel and aerospace-grade titanium prices have swung by up to 35% quarter-on-quarter since 2024, undermining order pipelines for hydrogen, marine, and offshore projects that cannot down-spec materials. Fabricators pass surcharges to EPC clients, but budget overruns trigger project deferrals, trimming short-term volumes in the heat exchanger market. Stainless-steel clad plates partly offset exposure, yet diffusion bonding of dissimilar metals complicates weld integrity certification.

Other drivers and restraints analyzed in the detailed report include:

- Hydrogen Pilot Plants Adopting Printed-Circuit Exchangers for 200-Bar Service

- Data-Centre Liquid-Cooling Uptake Accelerating Micro-Channel Adoption

- Bio-Process Fouling Issues Limiting Adoption in Biorefineries

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Shell-and-tube designs retained 35% of the heat exchanger market share in 2024, upholding their position as the default choice where pressures exceed 60 bar and fouling margins are high. Their standardized TEMA classifications simplify specification for refineries, LNG pretreatment trains, and sulfur recovery units, supporting repeat orders for tube bundles and gaskets that underpin aftermarket revenues. At the same time, air-cooled variants are climbing at a 6% CAGR as water-stressed utilities in India, Texas, and the Middle East prioritize zero-liquid-discharge strategies, driving units with forced-draft fans and low-noise gearboxes.

Across 2025-2030, printed-circuit and spiral-wound formats will nibble share in high-pressure hydrogen and super-critical CO2 cycles as designers seek compact footprints that conventional shells cannot match. Nevertheless, the heat exchanger market will continue to favor shell-and-tube for brownfield revamps because existing nozzle locations fit retrofit bundles, keeping life-cycle costs predictable. Suppliers that blend stainless-steel shells with copper-nickel tubes for marine scrubbers will tap IMO 2020 compliance budgets, adding a modest lift to volumes.

Stainless steel maintained 30% of the heat exchanger market size in 2024 because grades such as 316L balance corrosion resistance and cost efficiency. In food, beverage, and pharmaceutical lines, sanitary finishes and low-carbon content fulfill regulatory mandates without premium alloy surcharges. Exotic alloys-titanium, nickel, Incoloy, and Hastelloy-are moving at a 6.5% CAGR through 2030, capturing hydrogen, desalination, and offshore wind converter platforms where chloride-rich brines or hydrogen embrittlement preclude stainless options.

Polymers and composites grow from a small base as PTFE and graphite blocks outperform metals under highly acidic or fluoride-laden streams, notably in semiconductor wet-etch and lithium-ion battery recycling. Additive manufacturing unlocks dual-material lattices that place high-alloy material only where corrosion is severe, trimming cost and weight. Such innovations cement the heat exchanger industry's transition toward application-specific metallurgy rather than defaulting to legacy stainless catalogues.

The Heat Exchanger Market Report is Segmented by Type (Shell and Tube, Plate Frame, Air-Cooled, and Others), Material of Construction (Stainless Steel, Carbon Steel and Others), Flow Arrangement (Counter-Current, Parallel, Cross-Flow, and Hybrid/Multi-Pass), End-User Industry (Oil and Gas, Power Generation, Water and Waste-Water Treatment, and Others), and Geography (North America, Europe, Asia-Pacific, South America and Others).

Geography Analysis

Europe commanded 33% of 2024 global revenue, propelled by EU Eco-design directives that push boiler retrofits and district energy rollouts. Germany's integrated hydrogen strategy channels funding toward printed-circuit prototypes for electrolyzer plants, anchoring a high-value corner of the heat exchanger market. France accelerates SMR projects that require compact safety-class exchangers, while Nordic countries pioneer low-temperature district loops using titanium plate packs to exploit ambient seawater. OEMs maintaining EN13445 pressure-vessel accreditations and in-region spare-parts hubs capture share as uptime guarantees dominate tender scoring.

Asia-Pacific posts the fastest 5.9% CAGR to 2030, with China's petrochemical capacity additions, India's expanding power fleet, and ASEAN district-cooling concessions underpinning volume growth. Domestic manufacturers leverage cost-advantaged supply chains to win shell-and-tube orders, while Japanese and Korean firms focus on titanium and nickel PCHEs for ammonia-cracking pilots. Local EPCs value suppliers that offer modular skids shipped within 10 weeks, compelling global brands to localize fabrication or risk losing relevance amid aggressive pricing.

North America benefits from LNG export terminals along the Gulf Coast and data-center campus expansions across Virginia, Texas, and Quebec. The US Department of Energy's hydrogen hubs funnel grants into PCHE demonstrations that use diffusion-bonded nickel alloys. Canada's oil-sands operators retrofit air-fin units to curtail water withdrawals, creating a secondary pull on fan-assisted equipment. Across Latin America, mining concentrates and solar-thermal plants drive boutique orders, whereas the Middle East leans on desalination and petrochemical mega-complexes to sustain demand. Africa's momentum remains gradual but steady, tied to copper-belt smelting upgrades.

- Alfa Laval AB

- Kelvion Holding GmbH

- Danfoss A/S

- SPX Flow Inc.

- GEA Group AG

- Hisaka Works Ltd.

- Xylem Inc.

- Thermax Ltd.

- Mersen SA

- API Heat Transfer Inc.

- GE Vernova Inc.

- Barriquand Technologies Thermiques SAS

- Koch Heat Transfer Company LP

- SWEP International AB

- Heatric

- Kobelco Steel Ltd.

- Accessen Group

- Funke WarmeaustauscherGmbH

- Tranter Inc.

- HRS Heat Exchangers Ltd.

- Hamon Thermal Europe SA

- Graham Corporation

- United Heat Transfer Ltd.

- KRN Heat Exchanger & Refrigeration Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in LNG liquefaction projects boosting demand for cryogenic exchangers

- 4.2.2 District-cooling expansion in GCC & SE-Asia driving plate-frame sales

- 4.2.3 Hydrogen pilot plants adopting printed-circuit exchangers for 200-bar service

- 4.2.4 Mandatory EU industrial boiler upgrades spurring retrofit tube bundles

- 4.2.5 SMR (small modular reactor) roll-out needing compact safety-class exchangers

- 4.2.6 Data-centre liquid cooling uptake accelerating micro-channel adoption

- 4.3 Market Restraints

- 4.3.1 Nickel & titanium price volatility inflating corrosion-resistant units

- 4.3.2 Bio-process fouling issues limiting adoption in biorefineries

- 4.3.3 EPC demand for 12-week lead-times curbing engineered-to-order designs

- 4.3.4 Direct air-cooling in power plants cannibalising air-cooled exchangers

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Type

- 5.1.1 Shell and Tube

- 5.1.2 Plate and Frame (Gasketed Plate, Brazed Plate, Welded Plate)

- 5.1.3 Air-Cooled (Fin and Tube, Plate-Fin, Micro-Channel)

- 5.1.4 Regenerative (Rotary and Plate)

- 5.1.5 Printed Circuit

- 5.1.6 Others (Double-Pipe, Spiral, Coaxial)

- 5.2 By Material of Construction

- 5.2.1 Stainless Steel

- 5.2.2 Carbon Steel

- 5.2.3 Non-Ferrous (Copper, Aluminium)

- 5.2.4 Exotic Alloys (Titanium, Nickel, Hastelloy)

- 5.2.5 Polymers and Composites (PTFE, Graphite, Ceramic)

- 5.3 By Flow Arrangement

- 5.3.1 Counter-Current

- 5.3.2 Parallel

- 5.3.3 Cross-Flow

- 5.3.4 Hybrid/Multi-Pass

- 5.4 By End-Use Industry

- 5.4.1 Oil and Gas

- 5.4.2 Chemical and Petrochemical

- 5.4.3 Power Generation (incl. Nuclear)

- 5.4.4 Food and Beverage

- 5.4.5 Pulp and Paper

- 5.4.6 Water and Waste-water Treatment

- 5.4.7 Other Industries (Automotive and Transportation, Metallurgy, Mining, HVACR, Pharmaceutical and Biotechnology)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Nordic Countries

- 5.5.2.7 Russia

- 5.5.2.8 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 ASEAN Countries

- 5.5.3.6 Australia

- 5.5.3.7 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Chile

- 5.5.4.4 Colombia

- 5.5.4.5 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 South Africa

- 5.5.5.4 Egypt

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, Recent Developments)

- 6.4.1 Alfa Laval AB

- 6.4.2 Kelvion Holding GmbH

- 6.4.3 Danfoss A/S

- 6.4.4 SPX Flow Inc.

- 6.4.5 GEA Group AG

- 6.4.6 Hisaka Works Ltd.

- 6.4.7 Xylem Inc.

- 6.4.8 Thermax Ltd.

- 6.4.9 Mersen SA

- 6.4.10 API Heat Transfer Inc.

- 6.4.11 GE Vernova Inc.

- 6.4.12 Barriquand Technologies Thermiques SAS

- 6.4.13 Koch Heat Transfer Company LP

- 6.4.14 SWEP International AB

- 6.4.15 Heatric

- 6.4.16 Kobelco Steel Ltd.

- 6.4.17 Accessen Group

- 6.4.18 Funke WarmeaustauscherGmbH

- 6.4.19 Tranter Inc.

- 6.4.20 HRS Heat Exchangers Ltd.

- 6.4.21 Hamon Thermal Europe SA

- 6.4.22 Graham Corporation

- 6.4.23 United Heat Transfer Ltd.

- 6.4.24 KRN Heat Exchanger & Refrigeration Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

金属衣架带市场按材料、应用、最终用户、分销管道和销售模式划分,全球预测(2026-2032年)

金属衣架带市场按材料、应用、最终用户、分销管道和销售模式划分,全球预测(2026-2032年) 热交换器市场 - 全球产业规模、份额、趋势、机会及预测(按产品类型、材料、最终用户、地区和竞争格局划分),2021-2031年石墨热交换器市场 - 全球产业规模、份额、趋势、机会及预测(按类型、材料、应用、最终用途产业、地区和竞争格局划分),2021-2031年

热交换器市场 - 全球产业规模、份额、趋势、机会及预测(按产品类型、材料、最终用户、地区和竞争格局划分),2021-2031年石墨热交换器市场 - 全球产业规模、份额、趋势、机会及预测(按类型、材料、应用、最终用途产业、地区和竞争格局划分),2021-2031年 2026-2030年全球卫生级垫片板式热交换器市场按产品类型、材料、流型和最终用途产业分類的锁扣式热交换器市场,全球预测,2026-2032年橡胶过马路板市场:按材料、应用、终端用户产业和分销管道划分 - 全球预测(2026-2032 年)

2026-2030年全球卫生级垫片板式热交换器市场按产品类型、材料、流型和最终用途产业分類的锁扣式热交换器市场,全球预测,2026-2032年橡胶过马路板市场:按材料、应用、终端用户产业和分销管道划分 - 全球预测(2026-2032 年) 日本热交换器市场报告(按类型、材料、最终用途产业和地区划分,2026-2034年)

日本热交换器市场报告(按类型、材料、最终用途产业和地区划分,2026-2034年) 按类型、应用和地区分類的蓄热式热交换器市场规模、份额和成长分析 - 2026-2033 年产业预测

按类型、应用和地区分類的蓄热式热交换器市场规模、份额和成长分析 - 2026-2033 年产业预测 板式热交换器市场规模、份额及成长分析(按产品类型、材质、应用和地区划分)-2026-2033年产业预测

板式热交换器市场规模、份额及成长分析(按产品类型、材质、应用和地区划分)-2026-2033年产业预测 热交换器市场规模、份额和趋势分析报告:按产品、材质、最终用途、地区和细分市场预测(2026-2033 年)

热交换器市场规模、份额和趋势分析报告:按产品、材质、最终用途、地区和细分市场预测(2026-2033 年)