|

市场调查报告书

商品编码

1851466

气雾罐:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)Aerosol Cans - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

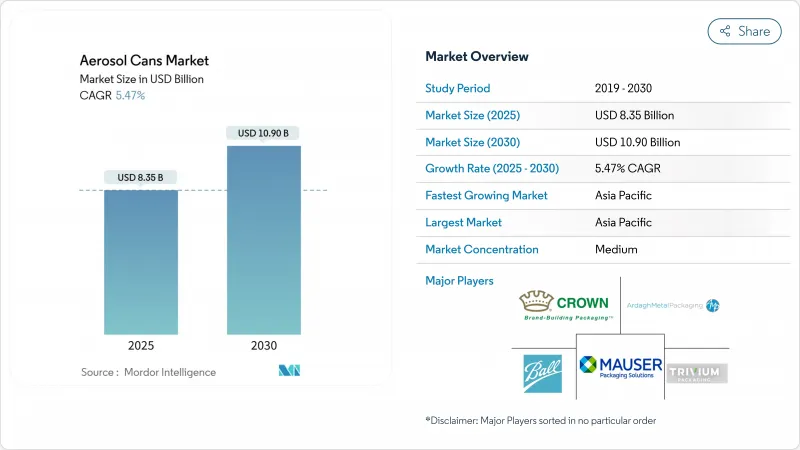

预计到 2025 年,气雾罐市场规模将达到 83.5 亿美元,到 2030 年将达到 109 亿美元,年复合成长率为 5.47%。

包装产业向可回收材料转型、监管政策与循环经济目标保持一致,以及铝製容器在满足更严格的挥发性有机化合物 (VOC) 法规方面展现出的卓越性能,将推动其持续成长。电子商务的蓬勃发展,促使品牌商对能够承受复杂履约网路衝击、且密封性好、可直接上架的包装形式提出更高要求。低全球暖化潜势 (GWP) 推进剂和单一材料罐体设计的创新,正在增强市场领导的竞争优势。同时,原料成本的波动以及可重复灌装概念的快速兴起,正在限制短期净利率。

全球气雾罐市场趋势与洞察

将可回收性与循环经济结合

铝的无限可回收性使其成为品牌所有者的关键材料,他们必须根据生产者延伸责任计划记录产品生命週期结束时的性能。波尔公司(Ball Corporation)的ReAl合金在保持强度的同时,将罐体的碳排放减少了50%,充分利用了现有全球回收基础设施的闭合迴路优势,该基础设施使75%的铝始终处于循环利用状态。这种可靠性为与面临气候变迁报告要求和塑胶减量目标的消费品製造商签订长期供应协议提供了支持。

个人护理和化妆品需求激增

高端个人护理产品线正越来越多地采用拉丝金属外观和特殊阀门,以提升用户体验并实现更高的定价。 Ball & Meadow 计划于 2025 年推出可重复填充的 MEADOW KAPSUL 喷雾罐,这表明高端护肤和护髮品牌正转向使用优雅的铝製气雾剂,以透过永续性和设计来脱颖而出。电子商务正在加速这一趋势,因为金属容器在最后一公里配送过程中不易凹陷和洩漏,同时还能提供 360 度全方位展示,方便数位商品行销。

严格的挥发性有机化合物和废弃物管理规定

美国环保署(EPA)于2025年7月生效的新规将对产品的反应活性设定加权上限,迫使配方师替换反应活性较高的溶剂,否则将面临处罚。处置规则要求使用过的罐子必须按照既定通讯协定进行通风和打包,这增加了处理成本,并催生了像Republic Services公司那样专门建造的回收设施等专业回收解决方案。

细分市场分析

到2024年,铝的回收量将占总回收量的85.34%,凸显了其完善的基础设施以及大多数回收法规的认可。这一领先地位有助于实现经济高效的封闭式供应,并与欧盟已实施的生产者延伸责任制法规相契合。气雾槽市场正受惠于ReAl合金技术的进步,该技术可在不影响抗凹陷性的前提下,将厚度降低15%,降低碳排放指数,同时维持单位成本的竞争力。

塑胶气雾剂以每年 8.64% 的速度成长,满足了品牌对完全透明、防碎裂和与酸性配方相容性的需求。 Plastipak 的无金属 SprayPET 革新表明,随着树脂供应商采用先进的隔离层,以及塑料在个人护理和食品喷雾应用领域站稳脚跟(这些应用领域关注金属味和冷衝击),聚合物可以满足压力阈值并与主流 PET 回收基础设施兼容。儘管发展势头强劲,但单一材料法规和金属价格波动意味着铝仍然是气雾剂罐市场的核心策略。

采用单次衝击挤压工艺,最大限度地减少焊缝,简化品管,一体式单体生产线在 2024 年的产量占总产量的 65.34%。这种结构的均匀壁厚有助于提高产品的韧性和跌落测试中的高内压等级,这对于髮胶喷雾和汽车煞车清洁剂等产品中的易燃推进剂至关重要。

两片式罐体正以7.37%的复合年增长率迅速普及,这得益于伺服控製成型技术的进步,该技术提高了侧缝强度,并实现了混合金属厚度,从而减少了材料用量。品牌商们对两片式罐体能够生产高挑纤细的罐身以及高精度光刻技术(可实现无变形的圆柱形罐体封装)的能力讚赏有加。随着季节性产品销售下滑,快速的设计週转成为必要,製造商们正投资研发模组化模具,以便在一体式和两片式罐体之间切换,从而应对不断变化的市场偏好。

区域分析

到2024年,亚太地区将占全球消费量的40.01%,年复合成长率达8.21%。都市化和可支配所得的成长将推动个人护理气雾剂的普及,同时,各地政府也纷纷推出回收政策,以契合铝的封闭式回收优势。日本品牌商正转向单一材料设计,而印度的美容市场也在加速发展,带动了本地填充剂用量的成长。

欧洲在技术和监管方面仍然处于领先地位,德国和英国在轻量化罐体研发方面处于领先地位,东欧工厂正在扩大低成本灌装产能,以满足该地区快速消费品(FMCG)的合约需求。由于传统品类的销售饱和限制了其扩张,市场成长正向高端和永续产品倾斜。

北美市场将展现出稳定且由创新主导的需求。美国环保署(美国)的反应法规迫使配方重新设计,但强劲的研发资金正帮助当地加工商维持产品组合的弹性。美国在非处方医疗保健和DIY涂料气雾剂领域处于领先地位,而墨西哥作为近岸製造地的地位日益巩固。加拿大消费者对低气味家用喷雾表现出浓厚的兴趣,推动了水性推进剂的普及。这些趋势将使这一成熟且盈利的全部区域保持中等个位数的成长。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 可回收性和循环经济

- 个人护理和化妆品需求激增

- 向低挥发性有机化合物/绿色推进剂过渡

- 电子商务「可上架」差异化

- 加强对单一材料包装的监管

- 膳食补充剂/非处方药气雾剂形式的出现

- 市场限制

- 严格的挥发性有机化合物和废弃物管理规定

- 铝和钢价格波动

- 补充装和浓缩液的兴起

- 消费者对气雾剂的环境意识

- 供应链分析

- 监管环境

- 技术展望

- 波特五力分析

- 买方的议价能力

- 供应商的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 生命週期与碳足迹分析

第五章 市场规模与成长预测

- 依材料类型

- 铝

- 钢

- 锡

- 塑胶

- 其他材料类型

- 可以透过类型

- 一体化(单体式)

- 两件套

- 三件套

- 按推进剂类型

- 压缩气体

- 液化气

- 碳氢化合物

- DME

- 其他液化气体

- 阀门式袋

- 以体积(毫升)

- 少于100毫升

- 101-300mL

- 301-500mL

- 500毫升或以上

- 按最终用户行业划分

- 个人护理和化妆品

- 家居用品

- 汽车和工业机械

- 医疗保健和製药

- 饮食

- 油漆和清漆

- 其他终端用户产业

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲和纽西兰

- 亚太其他地区

- 中东和非洲

- 中东

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 埃及

- 其他非洲地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Ball Corporation

- Crown Holdings Inc.

- Ardagh Metal Packaging SA

- Trivium Packaging

- Mauser Packaging Solutions

- Toyo Seikan Co. Ltd

- CCL Container

- Colep Packaging Portugal SA

- CPMC Holdings Limited

- Nampak Ltd

- Graham Packaging Company

- SGD Pharma

- Silgan Holdings

- DS Containers

- Montebello Packaging

- Tubex GmbH

- Grupo Zapata(Exal)

- Hindustan Tin Works

- Thai Beverage Can

- Bharat Containers

第七章 市场机会与未来展望

The aerosol cans market size stood at USD 8.35 billion in 2025 and is projected to reach USD 10.90 billion by 2030, advancing at a 5.47% CAGR.

Sustained growth is shaped by the packaging sector's pivot toward recyclable materials, regulatory alignment with circular-economy targets, and the proven ability of aluminum containers to meet stricter volatile-organic-compound (VOC) limits. E-commerce expansion adds momentum as brands seek leak-proof, shelf-ready pack formats that withstand complex fulfillment networks. Innovation in low-GWP propellants and mono-material can designs is strengthening the competitive differentiation of market leaders. At the same time, raw-material cost volatility and fast-rising refillable concepts temper near-term margins.

Global Aerosol Cans Market Trends and Insights

Recyclability and circular-economy alignment

Aluminum's infinite recyclability has turned it into a decisive material for brand owners that must document end-of-life performance under extended producer responsibility schemes. Ball Corporation's ReAl alloy cuts the can body's carbon footprint by 50% while maintaining strength, reinforcing the closed-loop advantages of an existing global recycling infrastructure where 75% of aluminum ever produced remains in active circulation. Such credentials underpin long-term supply contracts with consumer-goods majors that face climate-reporting requirements and plastic-reduction targets.

Surging demand from personal-care and cosmetics

Premium personal-care lines increasingly specify brushed-metal aesthetics and specialized valves that elevate user experience and enable higher pricing. Ball and Meadow's 2025 launch of refillable MEADOW KAPSUL cartridges illustrates how luxury skin- and hair-care brands turn to elegant aluminum aerosols to differentiate on sustainability and design. E-commerce accelerates this trend because metallic containers resist dents and leakage during last-mile delivery while offering 360-degree imaging for digital merchandising.

Stringent VOC and disposal regulations

EPA amendments effective July 2025 enforce product-weighted reactivity ceilings that oblige formulators to swap high-reactivity solvents or face penalties. Parallel F-gas restrictions in Europe intensify compliance complexity, pushing smaller firms to outsource R&D or exit affected lines.Disposal rules now require spent cans to be vented and baled under documented protocols that elevate processing costs, yet also spur specialized recycling solutions such as Republic Services' dedicated facilities.

Other drivers and restraints analyzed in the detailed report include:

- Transition to low-VOC/green propellants

- E-commerce "shelf-ready" differentiation

- Volatility in aluminum and steel prices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Aluminum captured 85.34% of the 2024 volume, underscoring its entrenched infrastructure and acceptance under most recycling codes. This leadership supports cost-efficient closed-loop supply and aligns with extended-producer-responsibility statutes already active in the EU. The aerosol cans market benefits from ReAl alloy advances that trim gauge weight by 15% without compromising dent resistance, keeping unit economics competitive while lowering carbon metrics.

Plastic aerosols, growing 8.64% annually, address brand requirements for full transparency, shatter resistance, and compatibility with acidic formulas. Plastipak's metal-free SprayPET Revolution validates that polymers can meet pressure thresholds and remain compatible with mainstream PET recycling infrastructures as resin suppliers roll out advanced barrier layers, plastics secure footholds in personal-care and food spray applications where metal taste or cold shock are concerns. Even with this momentum, mono-material legislation and metal price volatility keep aluminum at the core of the aerosol cans market strategy.

One-piece monobloc lines own 65.34% of 2024 unit output thanks to single-stroke impact-extrusion that minimizes weld seams and simplifies quality control. The configuration's uniform wall thickness supports a reputation for drop-test resilience and elevated internal pressures, essential for flammable propellants in hair-spray or automotive brake-cleaner SKUs.

Two-piece cans, posting a 7.37% CAGR, gain traction as servo-controlled body-maker technology enhances side-seam strength and allows hybrid metal gauges that lower material use. Brand owners appreciate the ability to produce tall, slim profiles and high-definition lithography that wraps around the cylindrical body without distortion. With demand for fast design turnarounds in seasonal product drops, manufacturers invest in modular tooling that switches between monobloc and two-piece runs, hedging against market preference shifts.

The Aerosol Cans Market Report is Segmented by Material Type (Aluminium, Steel, Tinplate, and More ), Can Type (One-Piece (Monobloc), Two-Piece, Three-Piece), Propellant Type (Compressed Gas, Bag-On-Valve, and More), Capacity (ml) (Less Than 100, 101-300, and More), End-User Industry (Personal Care and Cosmetics, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific composed 40.01% of 2024 consumption and is rising at an 8.21% CAGR, anchored by China's dual role as leading consumer and production hub. Urbanization and disposable-income growth support wider adoption of personal-care aerosols, while regional authorities impose recycling mandates that dovetail with aluminum's closed-loop advantages. Japanese brand owners advance mono-material designs, and India's accelerating beauty segment amplifies volumes for local fillers.

Europe remains a technology and regulation frontrunner. F-gas and VOC ceilings prompt swift migration to green propellants, rewarding incumbents with compliant product portfolios.Germany and the United Kingdom lead in lightweight-can R&D, while Eastern European plants extend low-cost filling capacity to pan-regional FMCG contracts. Market growth leans toward premium and sustainable offerings as volume saturation limits expansion in traditional categories.

North America demonstrates steady, innovation-driven demand. EPA reactivity rules compel formula redesigns, yet robust R&D funding helps local converters maintain portfolio agility. The United States leads in OTC healthcare and DIY paint aerosols, while Mexico strengthens as a near-shore manufacturing base. Canadian consumers show elevated interest in low-odor household sprays, bolstering adoption of water-based propellants. Together these trends sustain mid-single-digit growth across a maturing yet profitable regional landscape.

- Ball Corporation

- Crown Holdings Inc.

- Ardagh Metal Packaging SA

- Trivium Packaging

- Mauser Packaging Solutions

- Toyo Seikan Co. Ltd

- CCL Container

- Colep Packaging Portugal SA

- CPMC Holdings Limited

- Nampak Ltd

- Graham Packaging Company

- SGD Pharma

- Silgan Holdings

- DS Containers

- Montebello Packaging

- Tubex GmbH

- Grupo Zapata (Exal)

- Hindustan Tin Works

- Thai Beverage Can

- Bharat Containers

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Recyclability and circular?economy alignment

- 4.2.2 Surging demand from personal-care and cosmetics

- 4.2.3 Transition to low-VOC/green propellants

- 4.2.4 e-commerce "shelf-ready" differentiation

- 4.2.5 Regulatory push for mono-material packaging

- 4.2.6 Emergence of nutraceutical/OTC aerosol formats

- 4.3 Market Restraints

- 4.3.1 Stringent VOC and disposal regulations

- 4.3.2 Volatility in aluminium and steel prices

- 4.3.3 Rise of refillable and concentrated formats

- 4.3.4 Consumer eco-perception of aerosols

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Lifecycle and Carbon-Footprint Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Aluminium

- 5.1.2 Steel

- 5.1.3 Tinplate

- 5.1.4 Plastic

- 5.1.5 Other Material Type

- 5.2 By Can Type

- 5.2.1 One-piece (Monobloc)

- 5.2.2 Two-piece

- 5.2.3 Three-piece

- 5.3 By Propellant Type

- 5.3.1 Compressed Gas

- 5.3.2 Liquefied Gas

- 5.3.2.1 Hydrocarbon

- 5.3.2.2 DME

- 5.3.2.3 Other Liquefied Gas

- 5.3.3 Bag-on-Valve

- 5.4 By Capacity (ml)

- 5.4.1 Less than 100

- 5.4.2 101-300

- 5.4.3 301-500

- 5.4.4 More than 500

- 5.5 By End-User Industry

- 5.5.1 Personal Care and Cosmetics

- 5.5.2 Household Care

- 5.5.3 Automotive and Industrial

- 5.5.4 Healthcare and Pharmaceutical

- 5.5.5 Food and Beverage

- 5.5.6 Paints and Varnishes

- 5.5.7 Other End-User Industry

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Russia

- 5.6.2.7 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Australia and New Zealand

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 Middle East

- 5.6.4.1.1 United Arab Emirates

- 5.6.4.1.2 Saudi Arabia

- 5.6.4.1.3 Turkey

- 5.6.4.1.4 Rest of Middle East

- 5.6.4.2 Africa

- 5.6.4.2.1 South Africa

- 5.6.4.2.2 Nigeria

- 5.6.4.2.3 Egypt

- 5.6.4.2.4 Rest of Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Ball Corporation

- 6.4.2 Crown Holdings Inc.

- 6.4.3 Ardagh Metal Packaging SA

- 6.4.4 Trivium Packaging

- 6.4.5 Mauser Packaging Solutions

- 6.4.6 Toyo Seikan Co. Ltd

- 6.4.7 CCL Container

- 6.4.8 Colep Packaging Portugal SA

- 6.4.9 CPMC Holdings Limited

- 6.4.10 Nampak Ltd

- 6.4.11 Graham Packaging Company

- 6.4.12 SGD Pharma

- 6.4.13 Silgan Holdings

- 6.4.14 DS Containers

- 6.4.15 Montebello Packaging

- 6.4.16 Tubex GmbH

- 6.4.17 Grupo Zapata (Exal)

- 6.4.18 Hindustan Tin Works

- 6.4.19 Thai Beverage Can

- 6.4.20 Bharat Containers

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

气雾罐市场按推进剂类型、产品类型、材质类型、设计、容量范围、分销管道和应用划分 - 2025-2032 年全球预测

气雾罐市场按推进剂类型、产品类型、材质类型、设计、容量范围、分销管道和应用划分 - 2025-2032 年全球预测 2025 年至 2033 年气雾槽市场报告(依产品类型、材料、所用推进剂、容量、应用和地区)

2025 年至 2033 年气雾槽市场报告(依产品类型、材料、所用推进剂、容量、应用和地区) 2025年全球气雾罐市场报告日本气雾罐市场报告(按产品类型、材料、推进剂用途、容量、应用和地区)2025-2033

2025年全球气雾罐市场报告日本气雾罐市场报告(按产品类型、材料、推进剂用途、容量、应用和地区)2025-2033 北美气雾罐:市场占有率分析、行业趋势和成长预测(2025-2030 年)

北美气雾罐:市场占有率分析、行业趋势和成长预测(2025-2030 年) 全球气雾罐市场:未来预测(2025-2030)

全球气雾罐市场:未来预测(2025-2030) 气雾罐市场 - 全球行业规模、份额、趋势、机会和预测,细分,按产品类型、按推进剂类型、按最终用户、按地区和竞争,2020-2030F

气雾罐市场 - 全球行业规模、份额、趋势、机会和预测,细分,按产品类型、按推进剂类型、按最终用户、按地区和竞争,2020-2030F 气雾罐市场机会、成长动力、产业趋势分析与 2025 - 2034 年预测中东和非洲的气雾罐:市场占有率分析、产业趋势和成长预测(2025-2030)亚太地区气雾罐:市场占有率分析、产业趋势和成长预测(2025-2030 年)

气雾罐市场机会、成长动力、产业趋势分析与 2025 - 2034 年预测中东和非洲的气雾罐:市场占有率分析、产业趋势和成长预测(2025-2030)亚太地区气雾罐:市场占有率分析、产业趋势和成长预测(2025-2030 年)