|

市场调查报告书

商品编码

1851520

生物基琥珀酸:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)Bio-Based Succinic Acid - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

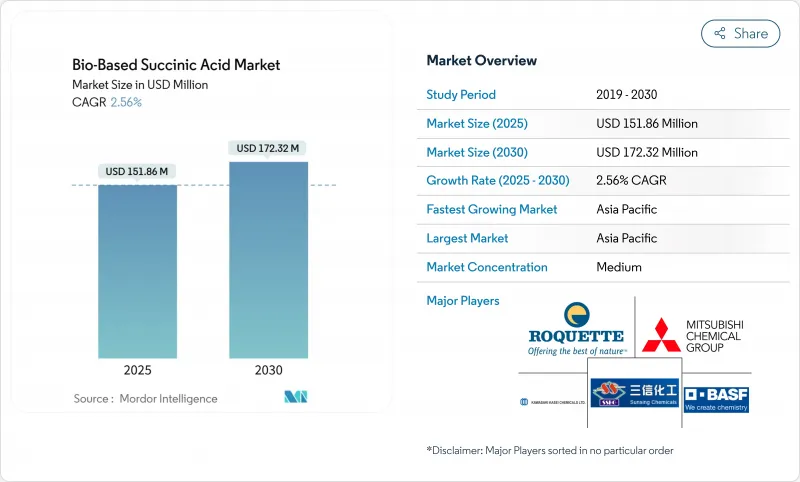

预计到 2025 年,生物基琥珀酸市场规模将达到 1.5186 亿美元,到 2030 年将达到 1.7232 亿美元,在预测期(2025-2030 年)内复合年增长率为 2.56%。

儘管生物基琥珀酸与油基琥珀酸的价格差距依然存在,但受发酵效率提高、原料选择多样化和下游应用范围扩大等因素的推动,生物基琥珀酸市场需求持续成长。由于琥珀酸在聚丁二酸丁二醇酯(PBS)和聚氨酯链中的应用广泛,工业聚合物製造商仍然是主要买家。区域扩张与政策密切相关:亚太地区受益于中国对生物製造的投资和日本的脱碳蓝图,正在加速发展;而欧洲的成长则得益于碳定价体系,奖励低碳足迹的中间体。由于目前尚无生产者拥有决定性的成本优势,市场竞争依然激烈,促使企业开展规模化合作、原料避险以及进行严格的认证宣传活动,以检验其永续性声明。

全球生物基琥珀酸市场趋势及洞察

工业聚合物中绿色化学品的应用日益增多

工程塑胶、热固性塑胶和弹性体製造商正持续以经认证的生物基替代品取代化石原料。BASF宣布其60多种产品组合以及一种含有40%可再生的生物基丙烯酸乙酯已获得ISCC+认证。同时,聚氨酯产业链正致力于利用直接从琥珀酸发酵中提取的生物基1,4-丁二醇。该製程由Genomatica公司率先开发,并透过授权给中国製造商进一步扩大规模。由于PBS树脂本身就是由琥珀酸和1,4-丁二醇合成的,因此琥珀酸产量的任何增长都将对包装、多层薄膜和一次性家电组件产生连锁反应。随着品牌所有者扩大其范围3脱碳目标,采购团队更倾向于选择能够提供温室气体减排证明的供应商,而生物基琥珀酸的市场需求也日益转向大规模生产的聚合物应用领域。

原油价格波动促使人们转向生物基路线

原油价格在每桶80美元以上波动时,会週期性地削弱石化产品琥珀酸的成本优势,迫使加工商签订生物基路线的承购协议,以规避原料价格波动的影响。欧盟委员会的工业碳管理计画透过将资本津贴和税额扣抵与替代化石中间体的计划挂钩,进一步促进了这一经济成长。日本领先的三菱化学、三井化学和旭化成等公司正在积极应对,在其石脑油裂解装置中试用生物质石脑油,以降低价格波动,同时履行其国家净零排放承诺。儘管低原油价格时期可能会暂时抑制市场动能,但采购部门越来越多地利用机率加权原油价格走势模型来模拟总拥有成本情景,即使在原油价格预测悲观的情况下,也能在生物基琥珀酸市场保持战略优势。

与石油基琥珀酸相比,生产成本更高

技术经济模型预测,在目前公用事业收费下,商业生物基琥珀酸的价格下限为每公斤2.5至2.7美元,即使在低油价情境下,也高于石油衍生同类产品的频宽价格。这一Delta源自于灭菌、多级沉淀等製程的能源需求以及不銹钢发酵槽的高资本投入。碳附加费和高端市场需求在一定程度上抵消了这一价差,但树脂和涂料的大批量用户仍然对价格非常敏感。製程强化-例如连续发酵、原位产品去除和低pH耐受微生物-展现出良好的前景,但实现价格持平的时间取决于能否加快这些技术从试点阶段到5万吨额定产能的转换。

细分市场分析

至2024年,工业应用将占生物基琥珀酸市场份额的43.18%,主要应用于PBS包装薄膜、可生物降解地膜和聚氨酯中间体。加工商已签署多年照付不议协议,以维持工厂产能,因此这些渠道的需求预计将如预期般增长,从而稳定整个生物基琥珀酸市场。个人护理领域将呈现最强劲的成长曲线,在预测期内复合年增长率将达到3.79%,这主要得益于免洗祛痘产品、天然除臭剂和温和去角质产品等特殊剂型的推动。皮肤病学研究表明,1%的琥珀酸凝胶可以抑制痤疮丙酸桿菌的生长,且不会引起刺激,这使得品牌可以将这种更环保的活性成分与现有的β-羟基酸并列销售。同时,被覆剂製造商正在试验基于琥珀酸的多元醇,这种多元醇在保持生物降解性的同时,也能提供高固态。

随着销售成长,不同终端市场的价格差异也十分显着。工业树脂买家在维持稳定销售的同时,正努力争取更低的吨价。个人护理和製药用户则因微生物纯度和可追溯性要求而接受溢价,这为生产商提供了利润对冲的机会。这种动态促成了双渠道模式的形成:早期采用者将基准产能用于聚合物生产,并使用升级后的发酵槽生产特殊批次产品。随着下游各产业优先考虑生命週期评估指标,跨领域综效也随之显现。例如,医药检验能够增强化妆品功效的可信度,而包装的机械可回收性测试则能让消费品所有者确信,产品的最终处置符合循环经济的承诺。综上所述,这些模式证实,应用多样性在提升生物基琥珀酸市场的收入稳定性方面发挥核心作用。

区域分析

亚太地区占据最大的区域市场份额,预计到2024年将占生物基琥珀酸市场32.75%的份额,到2030年复合年增长率将达到3.70%。中国各省政府正向工业产业园区提供低利率贷款,以推动专用于生产琥珀酸和1,4-丁二醇的5万吨级发酵槽的快速扩建。国家发展和改革委员会已将生物质纳入五年规划奖励措施,增加税收优惠以降低现金成本的损益平衡点。日本的「绿色成长策略」旨在实现碳中和,该策略为生物质石脑油共加工提供补贴,鼓励三菱化学、三井化学和旭化成联合投资建造以琥珀酸为原料的聚酯裂解试验装置。韩国透过其生物战略技术蓝图支持类似的雄心壮志,而印度则透过扩大其碎米乙醇计画来专注于原料供应,该计画可以将糖化液分流至化学发酵槽。总而言之,这些倡议将政策支持与规模经济相结合,旨在巩固亚太地区生物基琥珀酸市场的领先地位。

北美凭藉着先进的合成生物学产业丛集、风险接受度强的创业投资资金以及各州层级的无污染燃料激励措施,维持着强劲的产业活力。美国农业部已在其2025年生物质研发议程中将琥珀酸列为优先产品,并设立了菌株工程和废弃物流资源化利用的津贴拨款。加州的低碳燃料标准为生物源二氧化碳的利用提供积分倍增机制,发酵公司可以利用此机制在整合碳捕获设备时获得额外收入。 Green Plains公司的Clean Sugar子公司已证明,其葡萄糖原料的二氧化碳排放减少了40%,目前内布拉斯加州的一家合约发酵企业正在测试该原料。加拿大为生化设备提供加速折旧政策,墨西哥正在评估生物中间体权益,以促进其北部工业走廊的发展。这些政策和基础设施共同建构了一个肥沃的生态系统,为该地区生物基琥珀酸市场的稳定扩张提供了强大支撑。

欧洲的发展轨迹取决于加强监管,将每吨石化产品的碳成本纳入考量。欧盟委员会的《2040年气候中和路线蓝图》优先考虑将碳捕获和利用产品纳入公共采购。德国的国家生物经济策略与研发补贴和原料物流计画相辅相成,旨在将甘蔗残渣整合到诸如勒纳(Leuna)等化工园区。法国正在试行消费品碳足迹标籤,从而提升对检验的低排放中间体的需求。英国的工业碳移除差价合约机制保障了最低支付标准,并鼓励发酵厂与北海碳封存井毗邻而建。儘管生产成本高于亚洲平均水平,但品牌所有者的压力和绿色融资工具的便利性使其保持了竞争力。因此,欧洲已成为生物基琥珀酸的主要高端市场,对高纯度等级和特殊规格的需求旺盛,支撑了更高的价格。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 工业聚合物中绿色化学品的应用日益增多

- 原油价格波动促使人们转向生物基路线

- 政府奖励和碳定价

- 基因工程微生物可降低下游成本

- 品牌拥有者必须采用循环经济采购模式

- 市场限制

- 与石油基琥珀酸相比,生产成本更高

- 农产品原物料价格波动

- 与新兴的生物己二酸途径的竞争

- 价值链分析

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章 市场规模与成长预测

- 透过使用

- 产业

- 製药

- 个人护理

- 油漆和涂料

- 其他用途

- 按原料来源

- 玉米来源的葡萄糖

- 甘蔗和甜菜蔗糖

- 木质纤维素生物质

- 粗甘油和废弃物流

- 二氧化碳耦合生物化学路线

- 按地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 亚太其他地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率(%)/排名分析

- 公司简介

- Anhui Sunsing Chemicals Co. Ltd.

- BASF SE

- dsm-firmenich

- Kawasaki Kasei Chemicals Ltd.

- Mitsubishi Chemical Group Corporation

- Reverdia

- Roquette Freres

- Technip Energies NV

第七章 市场机会与未来展望

The Bio-Based Succinic Acid Market size is estimated at USD 151.86 million in 2025, and is expected to reach USD 172.32 million by 2030, at a CAGR of 2.56% during the forecast period (2025-2030).

The bio-based succinic acid market has entered a measured maturation phase in which incremental fermentation efficiencies, diversified feedstock options, and expanding downstream uses keep demand advancing even though price gaps versus petro-routes persist. Industrial polymer makers remain the anchor buyers because polybutylene succinate (PBS) and polyurethane chains incorporate high volumes of the molecule, while personal-care and pharmaceutical formulators are scaling adoption to capture its multifunctional antimicrobial and pH-buffer benefits. Regional expansion is tied closely to policy: Asia-Pacific accelerates on the back of China's biomanufacturing investments and Japan's decarbonization roadmap, whereas Europe's growth stems from carbon-pricing schemes that reward low-footprint intermediates. Competitive intensity stays elevated because no producer yet controls a decisive cost advantage, prompting scale-up collaborations, feedstock hedging, and rigorous certification campaigns to validate sustainability claims.

Global Bio-Based Succinic Acid Market Trends and Insights

Increasing Adoption of Green Chemicals in Industrial Polymers

Manufacturers of engineering plastics, thermoset resins, and elastomers continue to swap fossil building blocks for certified bio-alternatives. BASF secured ISCC+ certification for more than 60 portfolio products and introduced a bio-based ethyl acrylate featuring 40% renewable content that cuts cradle-to-gate emissions by 30%. Parallel initiatives in polyurethane chains rely on bio-1,4-butanediol derived directly from succinic acid fermentations, a pathway pioneered by Genomatica and scaled further through technology licensing to Chinese producers. Because PBS resin is already synthesized from succinic acid and 1,4-butanediol, every incremental gain in succinate output ripples through packaging, mulch film, and single-use appliance parts. As brand owners escalate scope-3 decarbonization targets, procurement teams favor suppliers able to document greenhouse-gas savings, reinforcing the pull on the bio-based succinic acid market toward high-volume polymer applications.

Volatility in Crude-Oil Prices Prompting Switch to Bio-Routes

Oil-price swings above the USD 80 per-barrel threshold regularly erode the cost advantage enjoyed by petrochemical succinic acid, nudging converters to lock in offtake agreements for bio-routes that insulate them from feedstock shocks. The European Commission's industrial carbon-management plan complements this economic push by aligning capital grants and tax credits with projects that displace fossil intermediates. Japanese majors Mitsubishi Chemical, Mitsui Chemicals, and Asahi Kasei have responded by trialing biomass naphtha in naphtha crackers to derisk volatility while meeting national net-zero pledges. Although low oil phases can stall momentum temporarily, purchasing departments increasingly model total-cost-of-ownership scenarios that assign probability-weighted oil trajectories, keeping a strategic wedge for the bio-based succinic acid market even under bearish crude forecasts.

Higher Production Costs Versus Petro-Based Succinic Acid

Techno-economic models place the price floor for commercial bio-based succinic acid between USD 2.5 and 2.7 per kilogram at today's utility tariffs, a band still above the spot price of petro-derived equivalents in low-oil scenarios. The delta stems from sterilization energy demand, multi-step precipitation, and the capital intensity of stainless-steel fermenters. While carbon levies and premium niches partially offset the spread, large-volume users in resins and coatings remain price sensitive. Process intensification-continuous fermentation, in-situ product removal, and low-pH tolerant microbes-holds promise, but the timeline for parity hinges on accelerating these technologies from pilot to 50 kiloton nameplate capacity.

Other drivers and restraints analyzed in the detailed report include:

- Government Incentives & Carbon-Pricing Regulations

- Engineered Micro-Organisms Slashing Downstream Costs

- Agricultural Feedstock Price Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Industrial uses captured 43.18% of the bio-based succinic acid market share in 2024, anchored by PBS packaging films, biodegradable mulch, and polyurethane intermediates that together consume multi-kiloton volumes. Demand in these channels scales predictably because converters sign multi-year take-or-pay contracts that underpin plant-load factors, thereby stabilizing the overall bio-based succinic acid market. Over the forecast horizon, personal care presents the sharpest growth curve at a 3.79% CAGR, lifting contribution from specialty formats such as leave-on acne treatments, natural deodorants, and mild exfoliants. Dermatology studies confirm that 1% succinic acid gels diminish Propionibacterium acnes proliferation without triggering irritation, which allows brands to position greener actives alongside existing beta-hydroxy acids. Pharmaceutical uptake continues steadily as formulators incorporate succinate buffers to maintain pH in controlled-release matrices, while coatings makers experiment with succinate-based polyols that give high-solids content yet ensure biodegradability.

Parallel to volume expansion, price realization differs widely among end markets. Industrial resin buyers negotiate lower per-tonne tariffs yet provide consistent offtake. Personal care and pharmaceutical users accept a premium due to microbiological purity and traceability requirements, creating a margin hedge for producers. These dynamics encourage a dual-channel model in which early adopters allocate baseline capacity to polymers and consume upgraded fermenter runs for specialty batches. Because each downstream sector prioritizes life-cycle-assessment metrics, cross-segment synergies emerge: credentials validated in medicine lend credibility to cosmetic claims, while mechanical recyclability tests in packaging reassure consumer-goods owners that end-of-life outcomes align with circular-economy pledges. Together, these patterns affirm the central role of application diversity in extending revenue stability across the bio-based succinic acid market.

The Bio-Based Succinic Acid Market Report is Segmented by Application (Industrial, Pharmaceuticals, Personal Care, Paints and Coatings, Other Applications), Feedstock Source (Corn-Derived Glucose, Sugarcane & Beet Sucrose, Lignocellulosic Biomass, and More), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific owned the largest regional slice, representing 32.75% of the bio-based succinic acid market in 2024 and cruising toward a 3.70% CAGR through 2030. China's provincial governments funnel low-interest loans into industrial-biotech parks, enabling rapid scale-up of 50 kiloton fermenters dedicated to succinic acid and 1,4-butanediol. The National Development and Reform Commission integrates bio-chemicals into its Five-Year Plan incentives, adding tax holidays that lower cash-cost breakevens. In Japan, the Green Growth Strategy for Carbon Neutrality allocates subsidies for biomass naphtha co-processing, prompting Mitsubishi Chemical, Mitsui Chemicals, and Asahi Kasei to co-invest in pilot crackers that will feed succinate-based polyesters. South Korea supports similar ambitions through its Bio-Strategic Technology blueprint, while India focuses on feedstock supply by expanding broken-rice ethanol programs that could divert saccharified streams into chemical fermenters. Altogether, these initiatives compound policy support with scale economies, reinforcing Asia-Pacific's leadership in the bio-based succinic acid market.

North America sustains robust activity through advanced synthetic-biology clusters, risk-tolerant venture funding, and state-level clean-fuel incentives. The United States Department of Agriculture frames succinic acid as a high-priority product in its 2025 Biomass Research and Development Agenda, unlocking grant pools for strain engineering and waste-stream valorization. California's Low Carbon Fuel Standard awards credit multipliers to biogenic CO2 utilization, a mechanism that fermentation plants leverage for additional revenue when they integrate carbon capture units. Green Plains' clean-sugar subsidiary demonstrated 40% lower carbon footprint dextrose, a feedstock now trialed by contract fermenters in Nebraska. Canada provides accelerated depreciation for equipment deployed in biochemicals, and Mexico evaluates concessions for bio-intermediates to spur northern industrial corridors. Collectively, these policy and infrastructure elements create a fertile ecosystem that underpins steady expansion of the bio-based succinic acid market within the region.

Europe's trajectory hinges on regulatory stringency that embeds carbon costs into every tonne of petrochemical output. The European Commission's 2040 climate-neutral roadmap positions carbon-capture-and-utilization products for priority offtake in public procurement. Germany's National Bioeconomy Strategy supplements R&D grants with feedstock logistics programs to integrate sugar-beet residues into chemical parks such as Leuna. France pilots carbon-footprint labeling on consumer goods, elevating demand for verified low-emission intermediates. The United Kingdom's Contracts for Difference-style mechanism for industrial carbon removal assures payment floors, encouraging fermentation plants to co-locate with sequestration wells in the North Sea. While production costs exceed Asian averages, brand-owner pressure and access to green-finance instruments maintain competitive momentum. Consequently, Europe operates as the principal premium market within the bio-based succinic acid market, absorbing high-purity grades and specialty volumes that justify elevated pricing.

- Anhui Sunsing Chemicals Co. Ltd.

- BASF SE

- dsm-firmenich

- Kawasaki Kasei Chemicals Ltd.

- Mitsubishi Chemical Group Corporation

- Reverdia

- Roquette Freres

- Technip Energies N.V.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing adoption of green chemicals in industrial polymers

- 4.2.2 Volatility in crude-oil prices prompting switch to bio-routes

- 4.2.3 Government incentives and carbon-pricing regulations

- 4.2.4 Engineered micro-organisms slashing downstream costs

- 4.2.5 Circular-economy sourcing mandates from brand owners

- 4.3 Market Restraints

- 4.3.1 Higher production costs versus petro-based succinic acid

- 4.3.2 Agricultural feedstock price volatility

- 4.3.3 Competition from emerging bio-adipic acid pathways

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Application

- 5.1.1 Industrial

- 5.1.2 Pharmaceuticals

- 5.1.3 Personal Care

- 5.1.4 Paints and Coatings

- 5.1.5 Other Applications

- 5.2 By Feedstock Source

- 5.2.1 Corn-derived Glucose

- 5.2.2 Sugarcane and Beet Sucrose

- 5.2.3 Lignocellulosic Biomass

- 5.2.4 Crude Glycerol and Waste Streams

- 5.2.5 CO2-coupled Bio-electrochemical Routes

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 Japan

- 5.3.1.3 India

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Anhui Sunsing Chemicals Co. Ltd.

- 6.4.2 BASF SE

- 6.4.3 dsm-firmenich

- 6.4.4 Kawasaki Kasei Chemicals Ltd.

- 6.4.5 Mitsubishi Chemical Group Corporation

- 6.4.6 Reverdia

- 6.4.7 Roquette Freres

- 6.4.8 Technip Energies N.V.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Sustainable Dyes Made from Bio-based Succinic Acid

全球聚丁二酸丁二醇酯市场规模、份额、趋势和成长分析报告(2026-2034年)琥珀酸全球市场规模、份额、趋势和成长分析报告(2026-2034)

全球聚丁二酸丁二醇酯市场规模、份额、趋势和成长分析报告(2026-2034年)琥珀酸全球市场规模、份额、趋势和成长分析报告(2026-2034) 2026-2030年全球琥珀酸市场

2026-2030年全球琥珀酸市场 磺基琥珀酸酯市场机会、成长要素、产业趋势分析及2026年至2035年预测

磺基琥珀酸酯市场机会、成长要素、产业趋势分析及2026年至2035年预测 琥珀酸市场规模、份额及成长分析(按类型、应用、终端用户产业和地区划分)-产业预测(2026-2033)

琥珀酸市场规模、份额及成长分析(按类型、应用、终端用户产业和地区划分)-产业预测(2026-2033) 生物琥珀酸衍生聚酯多元醇市场规模、份额和趋势分析报告:按产品、应用、地区和细分市场预测(2025-2033 年)

生物琥珀酸衍生聚酯多元醇市场规模、份额和趋势分析报告:按产品、应用、地区和细分市场预测(2025-2033 年) Polybutylene Succinate的全球市场

Polybutylene Succinate的全球市场 琥珀酸:市场占有率分析、产业趋势、统计数据、成长预测(2025-2030)琥珀酸市场规模(按类型、最终用途行业、地区和预测)

琥珀酸:市场占有率分析、产业趋势、统计数据、成长预测(2025-2030)琥珀酸市场规模(按类型、最终用途行业、地区和预测) 2030 年琥珀酸市场预测:按类型、应用程式、最终用户和地区分類的全球分析

2030 年琥珀酸市场预测:按类型、应用程式、最终用户和地区分類的全球分析