|

市场调查报告书

商品编码

1851772

OSAT(半导体外包组装和测试):市场份额分析、行业趋势、统计数据、成长预测(2025-2030 年)Outsourced Semiconductor Assembly And Test (OSAT) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

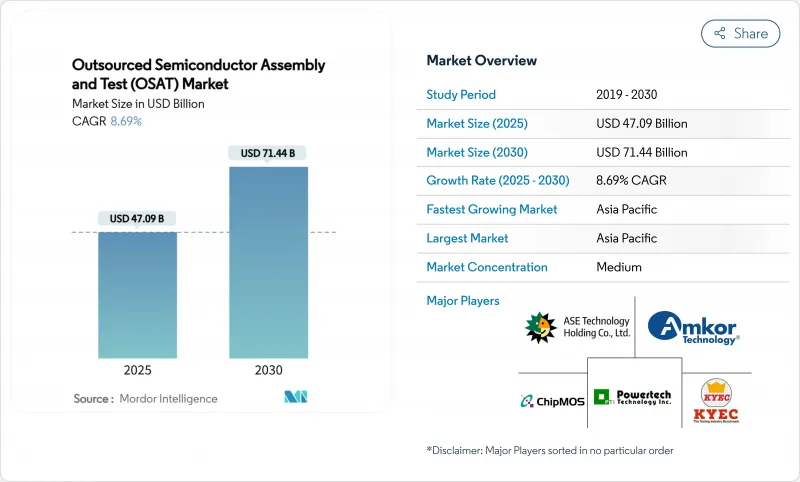

预计到 2025 年,OSAT(外包半导体组装和测试)市场规模将达到 470.9 亿美元,到 2030 年将达到 714.4 亿美元,年复合成长率为 8.69%。

人工智慧、高效能运算和汽车电气化的持续进步推动了对先进封装和安全关键型测试流程的需求,从而扩大了专业后端服务供应商的潜在市场。亚太地区的供应商凭藉成熟的生态系统保持了价格竞争力,而北美和欧洲受政策主导的产能扩张已开始重塑全球供应格局。混合晶片架构提升了异质整合的重要性,促使企业对扇出型晶圆级和2.5D/3D平台进行策略性投资。同时,日益严格的贸易法规和永续性要求鼓励客户将部分工作负载转移到地理位置分散、单位吞吐量能耗更低的地区。由于晶圆代工产能持续紧张,小型晶圆厂半导体公司继续将后端营运外包,这进一步巩固了外包半导体组装测试(OSAT)市场在下一个规划週期中的结构性重要性。

全球OSAT(半导体外包组装与测试)市场趋势与洞察

每车半导体产量快速成长

随着汽车原始设备製造商 (OEM) 向软体定义平台转型,每辆车的半导体元件数量不断增加,从而推动了对高可靠性封装的需求。大众汽车集团与安森美半导体 (ON Semiconductor) 在牵引逆变器伙伴关係凸显了碳化硅元件的日益普及,而碳化硅元件需要具有良好散热性能的功率封装。这家透过 AEC-Q100 和 ISO 26262 认证的 OSAT 供应商赢得了新的设计订单,并与电动车供应商签订了多年产能预订协议。

5G推动对先进射频封装的需求

商用5G基地台部署已将无线电前端推进毫米波领域,这需要低损耗基板、共形屏蔽和紧凑的SiP封装。 Finwave Semiconductor在GLOBALFOUNDRIES完成的E型MISHEMT整合标誌着一种新型氮化镓装置的商业化部署,该装置需要特殊的射频封装,预计将于2026年完成量产认证。 6G测试平台已开始采用共封装光元件,这促使OSAT公司扩展其混合讯号组装能力和先进的热感解决方案。

主要晶圆代工厂与整合元件製造商之间的垂直整合

台积电的晶圆厂2.0策略整合了封装和测试流程,并提供承包服务,降低了独立OSAT厂商的产能。三星也采取了类似的策略,英特尔则扩展了其代工服务,涵盖了先进的中介层装置。这些措施降低了第三方厂商在高利润领域的市场份额,迫使OSAT厂商专注于汽车安全和光电等细分领域。

细分市场分析

预计2025年至2030年,其复合年增长率将达到10.8%,超过封装产业的扩张速度,但其基数较小。人工智慧和高效能运算设计需要係统级测试覆盖率,以检验晶片互连延迟、动态热节流以及深度热感工作负载在不同电压下的性能。半导体组装和测试外包市场已透过将自适应机器学习演算法整合到自动化测试设备中来应对这一挑战,从而缩短测试时间并提高故障隔离能力。

2024年,封装业务仍占总收入的77.5%,但其产品组合已转向扇出型面板、2.5D中介层和共封装光学元件。随着客户整合供应商,OSAT集团推出了整合夹具设计、最终测试和物流的承包产品。爱德万测试在其V93000系列产品中加入了人工智慧分析功能,连续第六年蝉联组装检测设备市场第一。

球栅阵列(BGA)技术面向主流消费和工业平台,这些平台优先考虑机械强度,预计到2024年其市场份额将维持在24.3%。然而,随着行动处理器和人工智慧加速器向高密度线路重布迁移,扇出型晶圆级封装(FAP)将以11.5%的复合年增长率成长。这一趋势强化了半导体组装和测试市场的外包需求,因为只有少数供应商能够在不影响产量比率的情况下处理大尺寸面板。

日月光(ASE)斥资2亿美元拓展310mm x 310mm玻璃面板业务,彰显了其在经济高效的大面积製造方面的资本投入。在高频宽记忆体堆迭技术中,穿透硅通孔和玻璃通孔等多种通孔技术已被广泛应用。 FC-BGA基板受益于先进製程节点的采用,弥合了有机层压板和硅中介层在网路ASIC晶片中的差距。

OSAT(外包半导体组装和测试)市场按服务类型(封装、测试)、封装类型(球栅阵列、晶片级封装、其他)、应用(通讯、消费性电子、汽车、运算/网路、其他)、技术节点(≥28 奈米、16/14 纳米、10/7 北美、其他)和地区(≥28 奈米、16/14 纳米、10/7 北美、其他)和地区(北北美、南美细分。

区域分析

预计到2024年,亚太地区将维持其在OSAT(半导体外包组装和测试)市场收入中73.5%的份额,并在2030年之前以9.6%的复合年增长率增长。台湾、中国大陆和韩国因其靠近晶圆代工厂和基板製造商而成为产业丛集的支撑地,但不断升级的贸易紧张局势正促使企业将生产基地多元化转移至马来西亚、越南和菲律宾。印度已加快推出激励措施,核准了凯恩斯科技公司在古吉拉突邦投资4.13亿美元的工厂项目以及塔塔电子公司在阿萨姆邦投资30亿美元的封装测试一体化工厂项目。

得益于《晶片技术创新法案》(CHIPS Act)的资金支持,北美地区重获战略地位。安姆科(Amcor)在亚利桑那州破土动工兴建先进封装工厂,为美国国内汽车和人工智慧客户供货。德克萨斯)累计600亿美元用于建造多个晶圆厂及相应的后端产能,而Skyhar以9,300万美元收购英飞凌(Infineon)位于奥斯汀的晶圆厂,进一步增强了其自主研发能力。

欧洲已从利基研发转向大规模生产。 Silicon Box公司在义大利投资13亿欧元(约14.7亿美元)建造面板级晶圆厂,目标年产能超过1亿片SiP晶片,并已获得欧盟核准。泰雷兹、Radiall和富士康寻求在法国建立OSAT联盟,为国防和航空航天用户提供服务。安森美半导体在捷克共和国投资20亿美元建造碳化硅生产线,以确保电动车计划的本地供应。中东和非洲仍然是新兴市场,以色列和阿联酋正在评估相关政策框架,以吸引后端投资者。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 每辆车半导体含量不断提高

- 5G主导了先进射频封装的需求

- AI/HPC Chiplet 架构需要异质集成

- 晶圆代工产能不足导致轻晶圆厂外包模式兴起

- 美国《晶片製造和整合产品法案》(CHIPS Act)和欧盟《晶片製造和整合产品法案》(CHIPS Act)为建立区域性外包半导体製造和测试中心(OSAT)提供了奖励。

- 永续性要求推动晶圆级扇出型晶片的普及

- 市场限制

- 主要晶圆代工厂与整合元件製造商之间的垂直整合

- 资本投资强度和设备前置作业时间

- 对先进工具的地缘政治出口管制

- 先进封装工程领域熟练劳工短缺

- 价值链分析

- 监管环境

- 技术展望

- 宏观经济因素的影响

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 按服务类型

- 包装

- 测试

- 按包装类型

- 球栅阵列(BGA)

- 晶片级封装(CSP)

- 四方扁平封装/双列直插封装 (QFP/DIP)

- 多晶片模组(MCM)

- 晶圆层次电子构装(WLP)

- 扇出型封装(FO-WLP/FO-BGA)

- 系统级封装(SiP)

- 硅穿孔电极(2.5D/3D TSV)

- 覆晶(FC-BGA/FC-CSP)

- 透过使用

- 通讯

- 消费性电子产品

- 车

- 电脑与网路

- 产业

- 其他用途

- 依技术节点

- 28奈米或以上

- 16/14 nm

- 10/7 nm

- 5奈米或更小

- 传统(90-65 奈米)

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲国家

- 欧洲

- 德国

- 法国

- 英国

- 义大利

- 荷兰

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 台湾

- 韩国

- 日本

- 新加坡

- 马来西亚

- 印度

- 亚太其他地区

- 中东和非洲

- 中东

- 以色列

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 其他非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- ASE Technology Holding Co., Ltd.

- Amkor Technology, Inc.

- Jiangsu Changjiang Electronics Technology Co., Ltd.

- Siliconware Precision Industries Co., Ltd.

- Powertech Technology Inc.

- King Yuan Electronics Co., Ltd.

- Tongfu Microelectronics Co., Ltd.

- Tianshui Huatian Technology Co., Ltd.

- UTAC Holdings Ltd.

- Unisem(M)Berhad

- Hana Micron Inc.

- ChipMOS Technologies Inc.

- Formosa Advanced Technologies Co., Ltd.

- Chipbond Technology Corporation

- Lingsen Precision Industries, Ltd.

- Suchi Semicon Pvt. Ltd.

- Nepes Corporation

- Silicon Box Pte. Ltd.

- Shinko Electric Industries Co., Ltd.

- Carsem(M)Sdn. Bhd.

- SFA Semicon Co., Ltd.

- Stats ChipPAC Pte. Ltd.

- Orient Semiconductor Electronics, Ltd.

- Integra Technologies LLC

- Anam Semiconductor Inc.

第七章 市场机会与未来展望

The outsourced semiconductor assembly and test market size reached USD 47.09 billion in 2025 and is forecast to attain USD 71.44 billion by 2030, advancing at an 8.69% CAGR.

Sustained progress in artificial intelligence, high-performance computing, and automotive electrification raised demand for advanced packages and safety-critical test flows, thereby widening the total addressable opportunity for specialized backend service providers. Asia-Pacific suppliers preserved pricing leverage owing to mature ecosystems, yet policy-driven capacity build-outs in North America and Europe began to reshape global supply allocation. Hybrid chiplet architectures elevated the importance of heterogeneous integration, motivating strategic investments in fan-out wafer-level and 2.5D/3D platforms. Meanwhile, tighter trade controls and sustainability mandates encouraged customers to shift part of the workload to geographically diversified sites that can demonstrate lower energy use per unit throughput. As foundry capacity remained strained, fab-lite semiconductor companies continued to outsource backend steps, reinforcing the structural relevance of the outsourced semiconductor assembly and test market in the next planning cycle.

Global Outsourced Semiconductor Assembly And Test (OSAT) Market Trends and Insights

Soaring Semiconductor Content Per Vehicle

Automotive OEMs transitioned toward software-defined platforms, lifting semiconductor bill-of-materials per car and intensifying demand for high-reliability packages. Volkswagen Group's traction inverter partnership with onsemi highlighted the rising adoption of silicon carbide devices that need thermally robust power packages.Imec's Automotive Chiplet Program, supported by ASE, BMW, and Bosch, illustrated cross-value-chain alignment on standardized chiplet packaging for functional safety compliance. OSAT providers that qualify to AEC-Q100 and ISO 26262, therefore, captured new design wins and secured multiyear capacity reservations with electric-vehicle suppliers.

5G-Led Demand for Advanced RF Packages

Commercial 5G base-station roll-outs moved the radio front-end into millimetre-wave territory, necessitating low-loss substrates, conformal shielding, and compact SiP footprints. Finwave Semiconductor's E-mode MISHEMT integration at GlobalFoundries signalled commercial deployment of novel gallium-nitride devices that require specialised RF packaging, with mass qualification targeted for 2026. The pipeline for 6G testbeds already incorporates co-packaged optics, urging OSAT firms to expand mixed-signal assembly capabilities and advanced thermal solutions.

Vertical Integration by Leading Foundries and IDMs

TSMC's Wafer Manufacturing 2.0 strategy integrated packaging and testing flows, offering turnkey services that reduced addressable volume for stand-alone OSAT companies. Samsung pursued a similar path, while Intel grew its foundry services to include advanced interposers. These moves compressed third-party share in high-margin segments and obliged OSAT firms to double down on niches such as automotive safety or photonics.

Other drivers and restraints analyzed in the detailed report include:

- AI/HPC Chiplet Architectures Needing Heterogeneous Integration

- Foundry Capacity Shortages Driving Fab-Lite Outsourcing

- Cap-Ex Intensity and Long Equipment Lead-Times

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Testing captured a 10.8% CAGR forecast for 2025-2030, a pace outstripping packaging's expansion yet starting from a smaller base. AI and high-performance computing designs demanded system-level test coverage that verifies chiplet interconnect latency, dynamic thermal throttling, and deep-learning workload performance under varied voltages. The outsourced semiconductor assembly and test market responded by integrating adaptive machine-learning algorithms in automatic test equipment, cutting test time while improving fault isolation.

Packaging retained 77.5% of 2024 revenue, but its composition evolved toward fan-out panel-level, 2.5D interposer, and co-packaged optics lines. As customers consolidated suppliers, OSAT groups bundled turnkey offerings that merge fixture design, final test, and logistics. Advantest secured its sixth consecutive leadership in assembly test equipment after adding AI-enabled analytics to its V93000 series.

Ball grid array technology maintained a 24.3% share in 2024 by serving mainstream consumer and industrial platforms that value mechanical robustness. However, fan-out wafer-level packages expanded at 11.5% CAGR as mobile processors and AI accelerators transitioned to high-density redistribution layers. This trend strengthened the outsourced semiconductor assembly and test market because only a limited pool of vendors can process larger panel formats without yield drift.

ASE's USD 200 million panel-level expansion to 310 mm X 310 mm glass panels illustrated a cap-ex commitment toward cost-effective, large-area builds. Through-silicon-via and through-glass-via variants proliferated in high-bandwidth memory stacks. FC-BGA substrates benefited from advanced node adoption, bridging the gap between organic laminates and silicon interposers for networking ASICs.

Outsourced Semiconductor Assembly and Test (OSAT) Market is Segmented by Service Type (Packaging, and Testing), Packaging Type (Ball Grid Array, Chip-Scale Package, and More), Application (Communication, Consumer Electronics, Automotive, Computing and Networking, and More), Technology Node (>=28 Nm, 16/14 Nm, 10/7 Nm, and More), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa).

Geography Analysis

Asia-Pacific retained 73.5% share of outsourced semiconductor assembly and test market revenue in 2024 and posted a 9.6% CAGR outlook through 2030. Taiwan, China, and South Korea anchored the cluster owing to proximity to foundries and substrate makers, yet escalating trade frictions prompted diversification into Malaysia, Vietnam, and the Philippines. India accelerated incentive programmes, endorsing Kaynes Technology's USD 413 million plant in Gujarat and Tata Electronics' USD 3 billion Assam package-test complex.

North America regained strategic weight following the CHIPS Act funding. Amkor broke ground on an advanced packaging facility in Arizona designed to supply domestic automotive and AI customers. Texas Instruments earmarked USD 60 billion for multiple wafer fabs and corresponding backend capacity, while SkyWater's USD 93 million acquisition of Infineon's Austin fab added sovereign redundancy.

Europe moved from niche R&D toward scaled production. Silicon Box obtained EU approval for a EUR 1.3 billion (USD 1.47 billion) panel-level plant in Italy, targeting >100 million SiP units per year. Thales, Radiall, and Foxconn explored a French OSAT alliance to serve defence and aeronautics users. Onsemi committed USD 2 billion to a silicon-carbide line in the Czech Republic, assuring local supply for e-mobility projects. The Middle East and Africa remained an emerging frontier, with Israel and the UAE assessing policy frameworks to attract backend investors.

- ASE Technology Holding Co., Ltd.

- Amkor Technology, Inc.

- Jiangsu Changjiang Electronics Technology Co., Ltd.

- Siliconware Precision Industries Co., Ltd.

- Powertech Technology Inc.

- King Yuan Electronics Co., Ltd.

- Tongfu Microelectronics Co., Ltd.

- Tianshui Huatian Technology Co., Ltd.

- UTAC Holdings Ltd.

- Unisem (M) Berhad

- Hana Micron Inc.

- ChipMOS Technologies Inc.

- Formosa Advanced Technologies Co., Ltd.

- Chipbond Technology Corporation

- Lingsen Precision Industries, Ltd.

- Suchi Semicon Pvt. Ltd.

- Nepes Corporation

- Silicon Box Pte. Ltd.

- Shinko Electric Industries Co., Ltd.

- Carsem (M) Sdn. Bhd.

- SFA Semicon Co., Ltd.

- Stats ChipPAC Pte. Ltd.

- Orient Semiconductor Electronics, Ltd.

- Integra Technologies LLC

- Anam Semiconductor Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Soaring semiconductor content per vehicle

- 4.2.2 5G-led demand for advanced RF packages

- 4.2.3 AI/HPC chiplet architectures needing heterogeneous integration

- 4.2.4 Foundry capacity shortages driving fab-lite outsourcing

- 4.2.5 U.S. CHIPS and EU Chips Acts incentivising local OSAT build-out

- 4.2.6 Sustainability mandates pushing wafer-level fan-out adoption

- 4.3 Market Restraints

- 4.3.1 Vertical integration by leading foundries and IDMs

- 4.3.2 Cap-ex intensity and long equipment lead-times

- 4.3.3 Geopolitical export controls on advanced tools

- 4.3.4 Skilled-labour shortages in advanced packaging engineering

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Packaging

- 5.1.2 Testing

- 5.2 By Packaging Type

- 5.2.1 Ball Grid Array (BGA)

- 5.2.2 Chip-Scale Package (CSP)

- 5.2.3 Quad Flat / Dual-Inline (QFP/DIP)

- 5.2.4 Multi-Chip Module (MCM)

- 5.2.5 Wafer-Level Packaging (WLP)

- 5.2.6 Fan-Out Packaging (FO-WLP / FO-BGA)

- 5.2.7 System-in-Package (SiP)

- 5.2.8 Through-Silicon Via (2.5D/3D TSV)

- 5.2.9 Flip-Chip (FC-BGA / FC-CSP)

- 5.3 By Application

- 5.3.1 Communication

- 5.3.2 Consumer Electronics

- 5.3.3 Automotive

- 5.3.4 Computing and Networking

- 5.3.5 Industrial

- 5.3.6 Other Applications

- 5.4 By Technology Node

- 5.4.1 >=28 nm

- 5.4.2 16/14 nm

- 5.4.3 10/7 nm

- 5.4.4 5 nm and below

- 5.4.5 Legacy (90-65 nm)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 France

- 5.5.3.3 United Kingdom

- 5.5.3.4 Italy

- 5.5.3.5 Netherlands

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Taiwan

- 5.5.4.3 South Korea

- 5.5.4.4 Japan

- 5.5.4.5 Singapore

- 5.5.4.6 Malaysia

- 5.5.4.7 India

- 5.5.4.8 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Israel

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Saudi Arabia

- 5.5.5.1.4 Turkey

- 5.5.5.1.5 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 ASE Technology Holding Co., Ltd.

- 6.4.2 Amkor Technology, Inc.

- 6.4.3 Jiangsu Changjiang Electronics Technology Co., Ltd.

- 6.4.4 Siliconware Precision Industries Co., Ltd.

- 6.4.5 Powertech Technology Inc.

- 6.4.6 King Yuan Electronics Co., Ltd.

- 6.4.7 Tongfu Microelectronics Co., Ltd.

- 6.4.8 Tianshui Huatian Technology Co., Ltd.

- 6.4.9 UTAC Holdings Ltd.

- 6.4.10 Unisem (M) Berhad

- 6.4.11 Hana Micron Inc.

- 6.4.12 ChipMOS Technologies Inc.

- 6.4.13 Formosa Advanced Technologies Co., Ltd.

- 6.4.14 Chipbond Technology Corporation

- 6.4.15 Lingsen Precision Industries, Ltd.

- 6.4.16 Suchi Semicon Pvt. Ltd.

- 6.4.17 Nepes Corporation

- 6.4.18 Silicon Box Pte. Ltd.

- 6.4.19 Shinko Electric Industries Co., Ltd.

- 6.4.20 Carsem (M) Sdn. Bhd.

- 6.4.21 SFA Semicon Co., Ltd.

- 6.4.22 Stats ChipPAC Pte. Ltd.

- 6.4.23 Orient Semiconductor Electronics, Ltd.

- 6.4.24 Integra Technologies LLC

- 6.4.25 Anam Semiconductor Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

半导体组装和测试服务市场(按产品类型、技术类型、封装材料、服务类型、製造流程、晶片类型、应用和最终用户产业划分)—2025-2032年全球预测

半导体组装和测试服务市场(按产品类型、技术类型、封装材料、服务类型、製造流程、晶片类型、应用和最终用户产业划分)—2025-2032年全球预测 2025年半导体组装与测试外包全球市场报告

2025年半导体组装与测试外包全球市场报告 全球外包半导体组装与测试(OSAT)市场

全球外包半导体组装与测试(OSAT)市场 半导体组装·试验受託(OSAT)市场,规模,占有率,趋势,产业分析报告:各服务形式,包装类别,各终端用户,各地区-2025年~2034年市场预测外包半导体组装与测试市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测全球电脑网路 OSAT 市场通讯和设备全球 OSAT 市场

半导体组装·试验受託(OSAT)市场,规模,占有率,趋势,产业分析报告:各服务形式,包装类别,各终端用户,各地区-2025年~2034年市场预测外包半导体组装与测试市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测全球电脑网路 OSAT 市场通讯和设备全球 OSAT 市场 半导体组装製程设备市场,按组件、按设备类型、按技术、按工艺、按最终用户、按国家/地区 - 2025 年至 2032 年全球行业分析、市场规模、市场份额及预测

半导体组装製程设备市场,按组件、按设备类型、按技术、按工艺、按最终用户、按国家/地区 - 2025 年至 2032 年全球行业分析、市场规模、市场份额及预测 半导体组装和测试服务 (OSAT) 市场:2025-2030 年预测

半导体组装和测试服务 (OSAT) 市场:2025-2030 年预测 全球 OSAT 市场 2025-2029

全球 OSAT 市场 2025-2029