|

市场调查报告书

商品编码

1766200

外包半导体组装与测试市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Outsourced Semiconductor Assembly and Testing Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

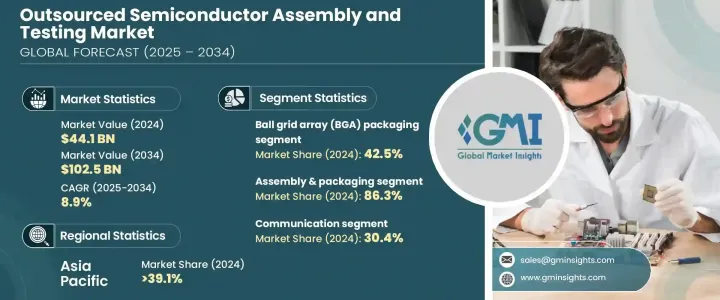

2024年,全球外包半导体封装测试市场规模达441亿美元,预计2034年将以8.9%的复合年增长率成长,达到1,025亿美元。这一成长主要源于消费性电子产业的扩张,包括智慧型手机、穿戴式装置和智慧家居设备,以及对经济高效且专业的封装测试解决方案日益增长的需求。随着电子产业不断追求设备小型化和效能提升,OSAT服务的需求也日益增长,以确保产品的可靠性和效率。

随着现代半导体封装和测试的复杂性不断增加,越来越多的公司将这些作业外包,以控制内部生产带来的高昂成本。这一趋势导致对OSAT基础设施的大量投资,尤其是在多个行业对这些服务的需求持续增长的情况下。对成本优化的日益关注,使得许多半导体公司(包括主要的行业领导者)都依赖外包封装和测试服务。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 441亿美元 |

| 预测值 | 1025亿美元 |

| 复合年增长率 | 8.9% |

透过外包这些关键职能,半导体製造商可以避免与内部营运相关的巨额资本支出。这些支出通常包括新建或扩建设施、购买昂贵设备以及聘用大量专业团队。外包使公司能够将资源重新分配到核心研发、产品开发和其他高优先领域,同时降低管理内部组装线的复杂性和营运成本。

2024年,组装和封装市场规模达382亿美元,预计复合年增长率将达9.1%。该领域尤其受到人工智慧 (AI)、高效能运算和其他创新半导体技术的进步的推动,这些技术需要专业的封装和测试服务。随着半导体装置日益复杂和微型化,对高度精密的组装和封装解决方案的需求也持续成长。 3D封装、系统级封装 (SiP) 和多晶片模组 (MCM) 等先进封装技术的集成,对于确保尖端装置的可靠性和性能至关重要,从而推动了该领域的成长。

2024年,消费性电子市场规模达113亿美元,预估复合年增长率为10.2%。这一成长主要源自于市场对更小、更有效率、功能更强大的电子设备日益增长的需求。随着手机、平板电脑、穿戴式装置和其他便携式装置的不断发展,製造商越来越依赖外包半导体组装和测试服务,以满足对小型化和性能的严格要求。随着这些设备变得越来越紧凑和复杂,它们需要先进的封装解决方案来确保高效能、热管理和更高的可靠性。

2024年,美国外包半导体封装测试市场规模达107亿美元,复合年增长率为9.2%。美国政府正努力透过《晶片法案》(CHIPS Act)等措施来促进国内半导体生产,旨在减少对全球供应链的依赖,并促进本土製造业的发展。各大公司正获得大量投资,以提升其封装测试能力,进而巩固美国在OSAT(封测外包半导体製造)市场的关键地位。

外包半导体封装测试市场的知名公司包括日月光科技控股股份有限公司、安靠科技股份有限公司、南茂科技股份有限公司、力成科技股份有限公司及京元电子股份有限公司。为了巩固其在外包半导体封装测试市场的地位,各公司正在大力投资尖端技术和先进的基础设施。许多OSAT供应商正致力于提升其在高阶封装解决方案方面的能力,以满足日益增长的复杂半导体产品需求。与半导体公司建立策略合作伙伴关係和协作对于扩展服务范围和提高营运效率也至关重要。此外,各公司正在采用自动化技术来简化生产流程、降低成本并加强品质控制。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 川普政府关税分析

- 对贸易的影响

- 贸易量中断

- 报復措施

- 对产业的影响

- 供给侧影响

- 价格波动

- 供应链重组

- 生产成本影响

- 需求面影响

- 价格传导至终端市场

- 市占率动态

- 消费者反应模式

- 供给侧影响

- 受影响的主要公司

- 策略产业反应

- 供应链重组

- 定价和产品策略

- 政策参与

- 展望与未来考虑

- 对贸易的影响

- 产业衝击力

- 成长动力

- 5G基础设施的扩展

- 汽车电子技术的进步

- 消费性电子产品的普及

- 对经济高效的製造解决方案的需求

- 小型化和先进封装技术

- 陷阱与挑战

- 严格的品质和可靠性标准

- 高资本投资要求

- 成长动力

- 成长潜力分析

- 监管格局

- 技术格局

- 未来市场趋势

- 差距分析

- 波特的分析

- Pestel 分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 策略仪表板

第五章:市场估计与预测:按服务类型,2021 年至 2034 年

- 主要趋势

- 组装和包装

- 测试

第六章:市场估计与预测:依包装类型,2021 年至 2034 年

- 主要趋势

- 球栅阵列(BGA)封装

- 晶片级封装(CSP)

- 堆迭晶片封装

- 多晶片封装

- 四方扁平和双列直插式封装

第七章:市场估计与预测:按应用,2021 年至 2034 年

- 主要趋势

- 沟通

- 消费性电子产品

- 汽车

- 运算和网路

- 工业的

- 其他的

- 服务

第八章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

第九章:公司简介

- ASE Technology Holding Co. Ltd

- Amkor Technology Inc.

- Powertech Technology Inc.

- ChipMOS Technologies Inc.

- King Yuan Electronics Co. Ltd

- Formosa Advanced Technologies Co. Ltd

- Jiangsu Changjiang Electronics Technology Co. Ltd

- UTAC Holdings Ltd

- Lingsen Precision Industries Ltd

- Tongfu Microelectronics Co.

- Chipbond Technology Corporation

- Hana Micron Inc.

- Integrated Micro-electronics Inc.

- Tianshui Huatian Technology Co. Ltd

The Global Outsourced Semiconductor Assembly and Testing Market was valued at USD 44.1 billion in 2024 and is estimated to grow at a CAGR of 8.9% to reach USD 102.5 billion by 2034. This growth is primarily driven by the expansion of the consumer electronics sector, which includes smartphones, wearables, and smart home devices, as well as the increasing demand for cost-effective and specialized packaging and testing solutions. As the electronics industry continues to miniaturize devices and enhance performance, there is a growing need for OSAT services to ensure product reliability and efficiency.

With the complexity of modern semiconductor packaging and testing, more companies are outsourcing these operations to manage the high costs associated with in-house production. This trend has led to significant investments in OSAT infrastructure, especially as the demand for these services continues to rise across multiple industries. The growing focus on cost optimization has led many semiconductor companies, including major industry leaders, to rely on outsourcing assembly and testing services.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $44.1 Billion |

| Forecast Value | $102.5 Billion |

| CAGR | 8.9% |

By outsourcing these essential functions, semiconductor manufacturers can avoid significant capital expenses associated with in-house operations. These expenses often include building or expanding facilities, purchasing expensive equipment, and employing large teams of specialized workers. Outsourcing allows companies to redirect resources toward core R&D, product development, and other high-priority areas while reducing the complexity and overhead involved in managing in-house assembly lines.

The assembly and packaging segment was valued at USD 38.2 billion in 2024, with projections indicating a robust growth rate of 9.1% CAGR. This segment is particularly driven by advancements in artificial intelligence (AI), high-performance computing, and other innovative semiconductor technologies that demand specialized packaging and testing services. As semiconductor devices become increasingly complex and miniaturized, the need for highly sophisticated assembly and packaging solutions continues to rise. The integration of advanced packaging techniques, such as 3D packaging, system-in-package (SiP), and multi-chip modules (MCM), has become critical to ensuring the reliability and performance of cutting-edge devices, thereby driving growth in this sector.

The consumer electronics segment was valued at USD 11.3 billion in 2024 and is estimated to grow at a CAGR of 10.2%. This growth is fueled by the increasing demand for smaller, more efficient, and highly functional electronic devices. With the continuous evolution of mobile phones, tablets, wearables, and other portable gadgets, manufacturers are relying heavily on outsourced semiconductor assembly and testing services to meet the rigorous demands of miniaturization and performance. As these devices become more compact and sophisticated, they require advanced packaging solutions that ensure high performance, thermal management, and enhanced reliability.

U.S Outsourced Semiconductor Assembly and Testing Market generated USD 10.7 billion in 2024 with a CAGR of 9.2%. The U.S. government is making efforts to bolster domestic semiconductor production through initiatives like the CHIPS Act, aimed at reducing reliance on global supply chains and boosting local manufacturing. Major companies are receiving significant investments to enhance their packaging and testing capabilities, reinforcing the U.S. as a key player in the OSAT market.

Prominent companies in the Outsourced Semiconductor Assembly and Testing Market include ASE Technology Holding Co. Ltd, Amkor Technology Inc., ChipMOS Technologies Inc., Powertech Technology Inc., and King Yuan Electronics Co. Ltd. To strengthen their presence in the outsourced semiconductor assembly and testing market, companies are investing heavily in state-of-the-art technologies and advanced infrastructure. Many OSAT providers are focusing on increasing their capabilities in high-end packaging solutions to cater to the growing demand for sophisticated semiconductor products. Strategic partnerships and collaborations with semiconductor companies are also pivotal for expanding service offerings and improving operational efficiency. Additionally, companies are embracing automation to streamline production processes, minimize costs, and enhance quality control.

Table of Contents

Chapter 1 Methodology and scope

- 1.1 Market scope and Definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.1.3 Impact on the industry

- 3.2.1.3.1 Supply-side impact

- 3.2.1.3.1.1 Price volatility

- 3.2.1.3.1.2 Supply chain restructuring

- 3.2.1.3.1.3 Production cost implications

- 3.2.1.3.2 Demand-side impact

- 3.2.1.3.2.1 Price transmission to end markets

- 3.2.1.3.2.2 Market share dynamics

- 3.2.1.3.2.3 Consumer response patterns

- 3.2.1.3.1 Supply-side impact

- 3.2.1.4 Key companies impacted

- 3.2.1.5 Strategic industry responses

- 3.2.1.5.1 Supply chain reconfiguration

- 3.2.1.5.2 Pricing and product strategies

- 3.2.1.5.3 Policy engagement

- 3.2.1.6 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Expansion of 5G infrastructure

- 3.3.1.2 Advancements in automotive electronics

- 3.3.1.3 Proliferation of consumer electronics

- 3.3.1.4 Demand for cost-effective manufacturing solutions

- 3.3.1.5 Miniaturization and advanced packaging technologies

- 3.3.2 Pitfalls and challenges

- 3.3.2.1 Stringent quality and reliability standards

- 3.3.2.2 High capital investment requirements

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 Pestel analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market estimates and forecast, by Service Type, 2021 – 2034 (USD million)

- 5.1 Key trends

- 5.2 Assembly & Packaging

- 5.3 Testing

Chapter 6 Market estimates and forecast, by Packaging Type, 2021 – 2034 (USD million)

- 6.1 Key trends

- 6.2 Ball grid array (BGA) packaging

- 6.3 Chip scale packaging (CSP)

- 6.4 Stacked die packaging

- 6.5 Multi chip packaging

- 6.6 Quad Flat and Dual-inline Packaging

Chapter 7 Market estimates and forecast, by Application, 2021 – 2034 (USD million)

- 7.1 Key trends

- 7.2 Communication

- 7.3 Consumer electronics

- 7.4 Automotive

- 7.5 Computing and networking

- 7.6 Industrial

- 7.7 Others

- 7.8 Services

Chapter 8 Market estimates and forecast, by Region, 2021 – 2034 (USD million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company profiles

- 9.1 ASE Technology Holding Co. Ltd

- 9.2 Amkor Technology Inc.

- 9.3 Powertech Technology Inc.

- 9.4 ChipMOS Technologies Inc.

- 9.5 King Yuan Electronics Co. Ltd

- 9.6 Formosa Advanced Technologies Co. Ltd

- 9.7 Jiangsu Changjiang Electronics Technology Co. Ltd

- 9.8 UTAC Holdings Ltd

- 9.9 Lingsen Precision Industries Ltd

- 9.10 Tongfu Microelectronics Co.

- 9.11 Chipbond Technology Corporation

- 9.12 Hana Micron Inc.

- 9.13 Integrated Micro-electronics Inc.

- 9.14 Tianshui Huatian Technology Co. Ltd

半导体组装测试外包服务市场:2026-2032年全球市场预测(依产品类型、技术类型、封装材料、服务类型、製造流程、晶片类型、应用与最终用户产业划分)

半导体组装测试外包服务市场:2026-2032年全球市场预测(依产品类型、技术类型、封装材料、服务类型、製造流程、晶片类型、应用与最终用户产业划分) 半导体组装测试外包服务市场:依服务类型、应用、最终用户、国家及地区划分-产业分析、市场规模、市场占有率及2025年至2032年预测

半导体组装测试外包服务市场:依服务类型、应用、最终用户、国家及地区划分-产业分析、市场规模、市场占有率及2025年至2032年预测 半导体组装测试外包全球市场报告(2026)

半导体组装测试外包全球市场报告(2026) OSAT(外包半导体封装测试)市场:市场份额分析、行业趋势和统计数据、成长预测(2026-2031)

OSAT(外包半导体封装测试)市场:市场份额分析、行业趋势和统计数据、成长预测(2026-2031) 全球外包半导体组装与测试(OSAT)市场

全球外包半导体组装与测试(OSAT)市场 半导体组装·试验受託(OSAT)市场,规模,占有率,趋势,产业分析报告:各服务形式,包装类别,各终端用户,各地区-2025年~2034年市场预测全球电脑网路 OSAT 市场通讯和设备全球 OSAT 市场半导体组装製程设备市场,按组件、按设备类型、按技术、按工艺、按最终用户、按国家/地区 - 2025 年至 2032 年全球行业分析、市场规模、市场份额及预测

半导体组装·试验受託(OSAT)市场,规模,占有率,趋势,产业分析报告:各服务形式,包装类别,各终端用户,各地区-2025年~2034年市场预测全球电脑网路 OSAT 市场通讯和设备全球 OSAT 市场半导体组装製程设备市场,按组件、按设备类型、按技术、按工艺、按最终用户、按国家/地区 - 2025 年至 2032 年全球行业分析、市场规模、市场份额及预测 半导体组装和测试服务 (OSAT) 市场:2025-2030 年预测

半导体组装和测试服务 (OSAT) 市场:2025-2030 年预测