|

市场调查报告书

商品编码

1851800

数位地图:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)Digital Map - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

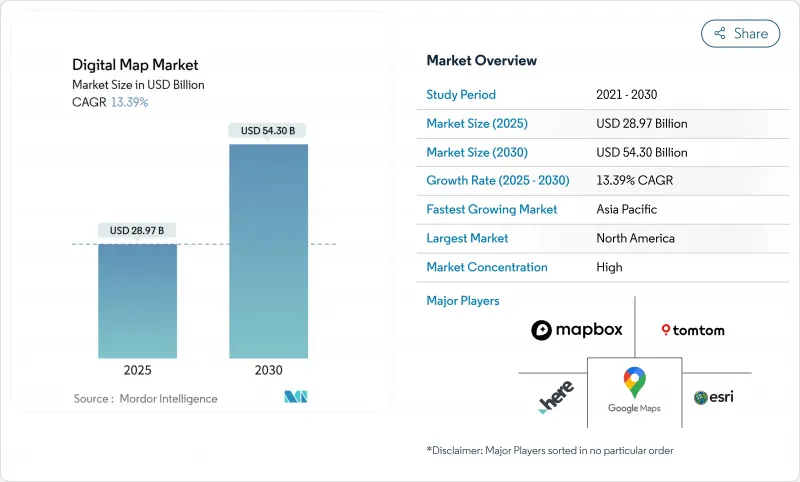

数位地图市场预计将从 2025 年的 289.7 亿美元成长到 2030 年的 543 亿美元,复合年增长率为 13.39%。

成长的驱动力来自向云端原生、人工智慧驱动平台的转型,这些平台支援自动驾驶汽车、智慧城市数位双胞胎和即时地理资讯系统。欧盟eCall等监管指令以及新兴企业的Scope 3碳排放测绘规则正在推动其应用范围超越传统导航。

全球数位地图市场趋势与洞察

高清地图在ADAS和自动驾驶车辆中的快速应用

BMW于2024年推出了德国首个L3级自动驾驶系统,该系统采用HERE高清即时地图,在定位、路线规划和营运设计区域检验实现了17公分以内的车道级精度。 HERE的高精度地图目前支援5300万辆车,比2023年增长了40%,显示汽车製造商对承包高清数据的依赖程度很高。 TomTom的Orbis Maps 3D覆盖了8,600万公里的道路,并整合了基于车道的导航和电动车充电层。日本的动态地图平台将于2025年获得政府支持,以服务L4级自动驾驶卡车,并将高清地图扩展到机场和港口。基于人工智慧的特征提取降低了更新成本,缩短了地图製作週期,并为能够近乎即时更新网路的供应商提供了竞争优势。

联网汽车OTA地图更新生态系的爆炸性成长

联网汽车正在将地图更新从静态授权模式转向定期OTA服务。哈曼的Smart Delta技术可将地图更新檔案压缩高达97%,在降低资料传输成本的同时,确保软体定义车辆的安全性。全球十分之九的OEM厂商已采用HERE的智慧速度辅助地图,以满足欧盟通用安全法规的要求,并为全车更新创建标准化的OTA路径。宾士将于2025年1月透过OTA更新整合电动智慧与越野追踪功能,展示地图资料如何协助售后功能变现。

厘米级地图持续更新的成本不断上升

在都市区,道路建设和交通变化需要对地图进行车道级更新,这显着增加了营运成本。 TomTom 现在融合了包括卫星、雷射雷达和行车记录器在内的多感测器数据,以实现特征提取的自动化并缩短测绘週期。 GetNexar 的人工智慧视觉技术利用众包方式获取行车记录器影像,从而降低了地图製作成本。成本压力促使各公司透过合作和选择性外包来维持地图更新速度,同时又不牺牲地图精度。

细分市场分析

到2024年,软体解决方案将占据数位地图市场61.40%的份额,这反映出企业对可配置、API驱动的平台的需求,这些平台能够跨行业整合空间分析功能。功能丰富的SDK使开发人员能够将地图、路线规划和地理编码整合到出行、物流和零售应用程式中。随着企业将传统GIS迁移到云端环境,并需要託管整合、资料品质调优和使用者赋能计划,复杂性也随之增加。现代平台中的AI模组可自动侦测线路标记、识别标誌和评估资产状况,进而提高营运效率。

使用专业服务也体现了合规要求,即对位置资料管道进行专家审核。实施计划中内建了文件、授权管理工具和地理围栏策略引擎,以确保跨境合法部署。随着企业资料量的成长,供应商营运的託管服务越来越多地负责资料摄取、标准化和近即时串流传输,从而确保持续收入,而不仅仅是一次性授权费用。

预计到2024年,云端部署将占数位地图市场规模的65.70%,并在2030年之前以15.70%的复合查询成长。弹性运算和储存可实现亚秒的查询效能,每天处理数十亿次路线请求,而自动扩展功能则可应对恶劣天气和假期季节期间的交通高峰。边缘资料收集节点将最新的探测资料推送至集中式储存库,确保叫车、物流和紧急应变等应用场景的地图资料始终保持最新。

儘管国防、航空和监管严格的金融业仍在继续采用本地部署,但随着主权云端区域、专用託管选项和机密运算飞地等安全反对意见的缓解,本地部署正在减少。成本模式正从资本支出 (capex) 转向计量收费(opex),从而释放资金用于人工智慧实验和跨域资料整合。企业越来越倾向于将地图绘製视为更广泛的资料平台策略中的微服务,而不是独立的地理资讯系统 (GIS) 功能。

数位地图市场按解决方案(软体、服务)、配置(本地部署、云端部署)、地图类型(导航地图、高清即时地图、地形图和专题地图)、最终用户产业(汽车、工程建设、通讯等)以及地区进行细分。市场预测以美元计价。

区域分析

到2024年,北美将占据数位地图市场29.6%的份额,这主要得益于软体定义车辆、云端地理资讯系统(GIS)和国防地理空间专案的早期应用。联邦机构正在推动开放空间框架的构建,汽车製造商也积极开发自动化研发项目。大型基础设施计划正在采用数位地形模型和全球导航卫星系统(GNSS)机器控制技术,以缩短施工週期并提高资产生命週期的可视性。像车辆远端资讯处理供应商这样的数据货币化领导企业,正在持续提供匿名化的探测数据,从而确保区域地图的精度。

到2030年,亚太地区将以15.4%的复合年增长率领跑,主要得益于5G用户成长、智慧运输资金投入以及政府对数位双胞胎技术的推动。日本工业界将收集高清走廊数据,用于大都会圈的卡车编队行驶和无人驾驶出租车试点项目,这将加速对高清地图的需求。中国云端服务供应商将开放大规模位置API,以提升电子商务物流;印度的5G网路将促进公共和农业领域的地理资讯系统(GIS)现代化。对区域超大规模资料中心的投资也将有助于落实资料主权规则,使全球供应商能够透过国内终端服务本地客户。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 高清地图在ADAS和自动驾驶车辆中的快速应用

- 联网汽车OTA地图更新生态系的爆炸性成长

- 云端原生GIS平台的主流应用

- 智慧城市数位双胞胎位孪生计画在全球扩展

- 欧盟电子呼叫强制令及下一代道路安全法规

- 企业范围 3 碳排放测绘要求

- 市场限制

- 地图逐公分更新成本不断上升

- 加强资料隐私和在地化法律(GDPR、PIPL)

- 数据提供者与原始设备製造商之间的知识产权许可纠纷

- 人们对人工智慧生成地图的演算法偏见和责任问题感到担忧

- 价值/供应链分析

- 监管环境

- 技术展望

- 波特五力模型

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 透过解决方案

- 软体

- 服务

- 透过部署

- 本地部署

- 云

- 按地图类型

- 导航地图

- 高清即时地图

- 地形图和专题地图

- 按最终用途行业划分

- 车

- 工程与施工

- 通讯领域

- 公共部门和国防部门

- 零售和地理行销

- 其他最终用户

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 欧洲

- 德国

- 英国

- 法国

- 荷兰

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 澳洲和纽西兰

- 亚太其他地区

- 中东和非洲

- 中东

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 其他非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Alphabet(Google Maps, Waze)

- HERE Technologies

- TomTom International BV

- Esri

- Mapbox

- Apple Inc.(Apple Maps)

- Maxar Technologies(DigitalGlobe)

- Collins Bartholomew

- Digital Map Products

- Digital Mapping Solutions

- DMTI Spatial

- Lepton Software

- ThinkGeo

- MapData Services

- NavInfo Co. Ltd.

- AutoNavi(Gaode, Alibaba)

- Baidu Maps

- Nearmap Ltd

- Zenrin Co. Ltd.

- Trimble Inc.

- CARTO

- OpenStreetMap Foundation

- MapQuest(Verizon)

第七章 市场机会与未来展望

The digital map market is valued at USD 28.97 billion in 2025 and is projected to reach USD 54.30 billion by 2030, advancing at a 13.39% CAGR.

Growth stems from the transition toward AI-powered, cloud-native platforms that support autonomous vehicles, smart-city digital twins, and real-time geographic information systems. Regulatory mandates such as EU eCall and emerging corporate Scope 3 carbon-mapping rules broaden adoption beyond conventional navigation.

Global Digital Map Market Trends and Insights

Rapid Uptake of HD Maps for ADAS and Autonomous Vehicles

BMW launched Germany's first Level 3 system in 2024 using HERE HD Live Map that delivers lane-level accuracy within 17 cm for localization, path planning, and operational-design-domain validation. HERE's high-precision coverage now supports 53 million vehicles, a 40% rise over 2023, indicating OEM reliance on turnkey HD data. TomTom's Orbis Maps 3D spans 86 million km of roads and integrates lane-based navigation with electric-vehicle charging layers. Japan's Dynamic Map Platform received government backing in 2025 to expand HD maps to airports and ports, targeting Level 4 autonomous trucks. AI-based feature extraction lowers refresh costs and shortens map-creation cycles, delivering competitive advantage to providers able to update networks in near-real time.

Explosive Growth of Connected-Car OTA Map-Update Ecosystems

Connected vehicles are shifting maps from static licenses to recurring over-the-air services. HARMAN's Smart Delta technology compresses map-update files by up to 97%, cutting data-transfer costs while maintaining software-defined-vehicle safety integrity. Nine of ten global OEMs deploy HERE's Intelligent Speed Assistance Map to address EU General Safety Regulation compliance, creating standardized OTA pathways for fleet-wide updates. Mercedes-Benz integrated electric-intelligence and off-road tracking features via its January 2025 OTA release, illustrating how map data enables post-sale feature monetization.

Escalating Costs of Continuous, Centimeter-Level Map Refresh

Lane-level refresh requirements drive substantial operational costs as construction and traffic changes intensify in urban zones. TomTom now fuses multi-sensor data-satellite, LiDAR, onboard cameras-to automate feature extraction and cut survey cycles. GetNexar's AI vision reduces cartography expense by crowd-sourcing dash-cam imagery, yet capital requirements remain onerous for smaller vendors. Cost pressures encourage alliances and selective outsourcing to maintain update cadence without sacrificing map accuracy.

Other drivers and restraints analyzed in the detailed report include:

- Mainstream Adoption of Cloud-Native GIS Platforms

- Smart-City Digital-Twin Programs Scaling Globally

- Heightened Data-Privacy and Localization Statutes (GDPR, PIPL)

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software solutions captured 61.40% of the digital map market in 2024, reflecting enterprise demand for configurable, API-driven platforms that consolidate spatial analytics across departments. Feature-rich SDKs allow developers to embed maps, routing, and geocoding into mobility, logistics, and retail applications. Services revenue, growing at 13.50% CAGR, mirrors rising complexity as organizations migrate legacy GIS to cloud environments and seek managed integration, data-quality tuning, and user-enablement programs. AI modules within modern platforms automate line-mark detection, sign recognition, and asset-condition scoring, catalyzing operational efficiencies.

Professional-services uptake also reflects compliance mandates that require expert audits of location-data pipelines. Documentation, consent-management tools, and geo-fencing policy engines are bundled into implementation projects to ensure lawful deployment across borders. As enterprise data volumes scale, vendor-operated managed services increasingly handle ingestion, normalization, and near-real-time streaming, locking in recurring revenue beyond one-time license fees.

Cloud deployment held 65.70% share of the digital map market size in 2024 and is forecast to expand at 15.70% CAGR through 2030. Elastic compute and storage enable sub-second query performance for billions of daily route requests while auto-scaling manages traffic peaks during severe-weather or holiday seasons. Edge ingestion nodes push fresh probe data into centralized repositories, ensuring map freshness for ride-hailing, logistics, and emergency response.

On-premise installations persist in defense, aviation, and highly regulated finance but trend downward as sovereign-cloud regions, dedicated host options, and confidential-computing enclaves mitigate security objections. Cost models shift from capex to pay-as-you-go opex, freeing capital for AI experimentation and cross-domain data fusion. Enterprises increasingly view mapping as a micro-service consumed within broader data-platform strategies rather than a standalone GIS function.

Digital Map Market is Segmented by Solution (Software, Services), Deployment (On-Premise, Cloud), Map Type (Navigation Maps, HD and Real-Time Maps, Topographic and Thematic Maps), End User Industry (Automotive, Engineering and Construction, Telecommunications and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America accounted for 29.6% digital map market share in 2024, anchored by early adoption of software-defined vehicles, cloud GIS, and defense geospatial programs. Federal agencies promote open spatial frameworks, and automotive OEMs maintain deep research pipelines for automation. Large-scale infrastructure projects employ digital terrain models and GNSS machine-control to shorten build cycles and enhance asset lifecycle visibility. Data-monetization champions such as fleet telematics providers continuously feed anonymized probe data that sustain regional map accuracy.

Asia-Pacific delivers the highest 15.4% CAGR through 2030, powered by 5G subscriber growth, smart-mobility funding, and government-backed digital-twin mandates. Japan's industry collects HD corridor data for truck platooning and metropolitan robo-taxi pilots, accelerating HD mapping demand. China's cloud providers expose high-volume location APIs to power e-commerce logistics, while India's 5G networks stimulate GIS modernization across utilities and agriculture. Investments in regional hyperscale data centers also address data-sovereignty rules, enabling global vendors to serve local customers via in-country endpoints.

- Alphabet (Google Maps, Waze)

- HERE Technologies

- TomTom International B.V.

- Esri

- Mapbox

- Apple Inc. (Apple Maps)

- Maxar Technologies (DigitalGlobe)

- Collins Bartholomew

- Digital Map Products

- Digital Mapping Solutions

- DMTI Spatial

- Lepton Software

- ThinkGeo

- MapData Services

- NavInfo Co. Ltd.

- AutoNavi (Gaode, Alibaba)

- Baidu Maps

- Nearmap Ltd

- Zenrin Co. Ltd.

- Trimble Inc.

- CARTO

- OpenStreetMap Foundation

- MapQuest (Verizon)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid uptake of HD maps for ADAS and autonomous vehicles

- 4.2.2 Explosive growth of connected-car OTA map-update ecosystems

- 4.2.3 Mainstream adoption of cloud-native GIS platforms

- 4.2.4 Smart-city digital-twin programs scaling globally

- 4.2.5 Mandatory EU eCall and next-gen road-safety regulations

- 4.2.6 Corporate Scope-3 carbon mapping requirements

- 4.3 Market Restraints

- 4.3.1 Escalating costs of continuous, centimetre-level map refresh

- 4.3.2 Heightened data-privacy and localization statutes (GDPR, PIPL)

- 4.3.3 IP-licensing disputes among data providers and OEMs

- 4.3.4 Algorithmic bias and liability concerns in AI-generated maps

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Solution

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment

- 5.2.1 On-Premise

- 5.2.2 Cloud

- 5.3 By Map Type

- 5.3.1 Navigation Maps

- 5.3.2 HD and Real-time Maps

- 5.3.3 Topographic and Thematic Maps

- 5.4 By End-use Industry

- 5.4.1 Automotive

- 5.4.2 Engineering and Construction

- 5.4.3 Telecommunications

- 5.4.4 Public Sector and Defense

- 5.4.5 Retail and Geomarketing

- 5.4.6 Other End User

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Netherlands

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Alphabet (Google Maps, Waze)

- 6.4.2 HERE Technologies

- 6.4.3 TomTom International B.V.

- 6.4.4 Esri

- 6.4.5 Mapbox

- 6.4.6 Apple Inc. (Apple Maps)

- 6.4.7 Maxar Technologies (DigitalGlobe)

- 6.4.8 Collins Bartholomew

- 6.4.9 Digital Map Products

- 6.4.10 Digital Mapping Solutions

- 6.4.11 DMTI Spatial

- 6.4.12 Lepton Software

- 6.4.13 ThinkGeo

- 6.4.14 MapData Services

- 6.4.15 NavInfo Co. Ltd.

- 6.4.16 AutoNavi (Gaode, Alibaba)

- 6.4.17 Baidu Maps

- 6.4.18 Nearmap Ltd

- 6.4.19 Zenrin Co. Ltd.

- 6.4.20 Trimble Inc.

- 6.4.21 CARTO

- 6.4.22 OpenStreetMap Foundation

- 6.4.23 MapQuest (Verizon)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

数位地图市场按产品类型、技术、资料来源、最终用户、应用、用户设备和垂直产业划分-2025-2032年全球预测

数位地图市场按产品类型、技术、资料来源、最终用户、应用、用户设备和垂直产业划分-2025-2032年全球预测 全球数位地图市场(按解决方案和用例)预测(至 2030 年)

全球数位地图市场(按解决方案和用例)预测(至 2030 年) 2025年全球数位地图市场报告

2025年全球数位地图市场报告 2025 年至 2033 年数位地图市场报告(按类型、用途、解决方案、部署模式、应用、最终用途产业和地区)

2025 年至 2033 年数位地图市场报告(按类型、用途、解决方案、部署模式、应用、最终用途产业和地区) 2025-2029年全球数位地图市场

2025-2029年全球数位地图市场 全球数位地图市场研究报告 - 产业分析、规模、份额、成长、趋势及 2025 年至 2033 年预测

全球数位地图市场研究报告 - 产业分析、规模、份额、成长、趋势及 2025 年至 2033 年预测 数位地图市场分析及预测(至 2034 年):类型、产品、服务、技术、组件、应用、最终用户、功能、部署

数位地图市场分析及预测(至 2034 年):类型、产品、服务、技术、组件、应用、最终用户、功能、部署 数位地图市场:各零件,各部署模式,各用途,各业界,各地区,机会,预测,2017年~2031年

数位地图市场:各零件,各部署模式,各用途,各业界,各地区,机会,预测,2017年~2031年 数位地图市场规模、份额、成长分析、按产品、按地图类型、按用途、按规模、按地区 - 行业预测,2024-2031 年全球数位地图市场规模:地区、范围和预测

数位地图市场规模、份额、成长分析、按产品、按地图类型、按用途、按规模、按地区 - 行业预测,2024-2031 年全球数位地图市场规模:地区、范围和预测