|

市场调查报告书

商品编码

1851889

立式袋:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)Stand-Up Pouches - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

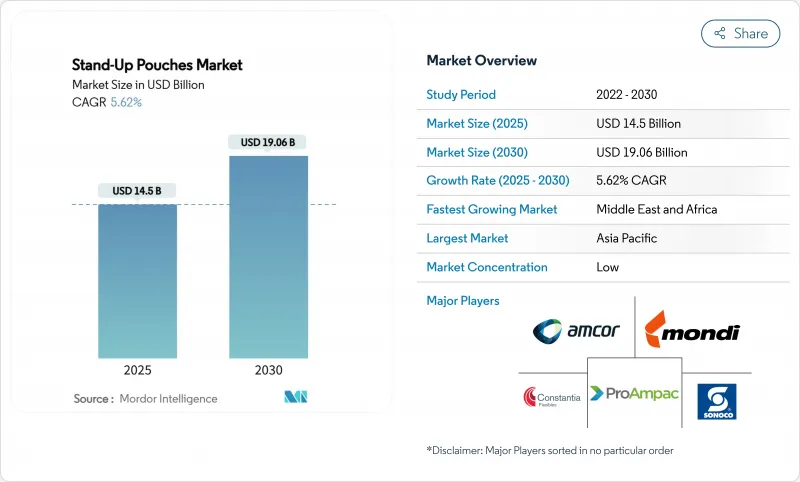

预计到 2024 年,吸嘴袋市场规模将达到 145 亿美元,到 2030 年将达到 190.6 亿美元,2025 年至 2030 年的复合年增长率为 5.62%。

对轻巧、可重复密封且外观精美的包装日益增长的需求,正推动着这一增长势头。欧洲的监管改革、东亚机能饮料的创新,以及北美宠物食品品牌从硬质包装转向软包装,都在加速软包装的普及。率先采用单一材料、可回收的包装形式,为製造商带来了成本和声誉优势;同时,热填充蒸馏性能的提升,也为食品、饮料和家居用品等终端应用领域开闢了新的可能性。亚太地区的生产规模、拉丁美洲的技术进步,以及以安姆科、蒙迪和索诺科主导的积极併购活动,正在重新定义追求效率和循环经济的企业之间的竞争格局。

全球立式袋市场趋势与洞察

欧盟迅速转向使用单一材料可回收包装袋结构

欧盟的《包装废弃物法规》于2025年2月生效,要求所有消费包装到2030年必须可回收,其中塑胶的消费后回收率必须达到30%。生产商正迅速从多层铝箔结构过渡到与路边回收系统相容的单层聚乙烯薄膜。安姆科的Liquiflex AmPrima包装袋符合这些标准,与传统复合材料相比,二氧化碳排放减少了79%,用水量减少了84%。早期采用者可以享受更低的生产者延伸责任费和更佳的货架吸引力,而后期采用者则面临更高的研发成本和货架破损风险。随着加工商获得新的密封技术许可并在不影响阻隔性的前提下降低薄膜厚度,带吸嘴包装袋市场正在蓬勃发展。

东亚地区即饮机能饮料的蓬勃发展推动了热填充装袋的发展

东亚消费者正逐渐接受蛋白奶昔、维生素凝胶和代餐饮料等便利食品。热填充填充(85°C以上)的特性使加工业者能够省去防腐剂,延长常温保质期,并提供营养丰富的配方。森永株式会社的「in Jelly Energy Long Life」能量胶袋在日本的防灾物资货架上使用了五年之久,充分展现了其优异的阻隔性和蒸馏性能。一家韩国新兴企业推出了一款针对千禧世代女性的单一蛋白粉吸嘴包装,使其年销售额较去年同期成长三倍。这些突破性创新推动了东南亚便利商店和高端健身房对吸嘴包装袋的广泛应用,为吸嘴包装袋市场带来了新的成长动力。

美国多层复合材料的回收管道有限

美国需要360亿至430亿美元的基础建设投资,才能在2030年前将塑胶回收率提高到61%。在材料回收设施能够识别和分离柔性复合材料之前,品牌商对扩大多层包装袋的生产规模持谨慎态度。因此,生产商正在加速推动单一材料包装袋的生产,但过渡成本和旧设备的风险暂时减缓了吸嘴包装袋市场的成长。

细分市场分析

2024年,塑胶材质的吸嘴袋占据了71.89%的市场份额,这主要得益于加工商对聚乙烯密封性、聚丙烯热稳定性和PET透明度的青睐。受监管和消费者需求的推动,可生物降解吸嘴袋的年复合成长率预计到2030年将达到7.14%,但目前仍主要面向小批量产品。 Accredo Packaging公司生产的甘蔗基树脂吸嘴袋可直接投入使用,每个吸嘴袋可减少43克二氧化碳排放。同时,Amcor公司的AmFiber纸基阻隔复合材料则瞄准了寻求无铝保质期的零食生产商。特製的EVOH阻隔层和尼龙扎带层继续为对氧气敏感的填充物提供保护,但成本上升正推动市场转型为高价值营养补充品产品线。预计到2028年,可生物降解吸嘴袋的市场规模将超过10亿美元,但塑胶吸嘴袋仍是食品和饮料核心产品的主要支撑。不断演变的回收设计指南正在刺激快速的实验,使塑胶成为吸嘴袋市场生存和创新的画布。

预计到2024年,圆底袋的市占率将达到38.66%,主要得益于成熟的成型设备和广泛的应用。然而,由于角底袋底部稳定性更佳,无需二次包装即可支援更大的填充量,因此预计其复合年增长率将达到5.77%。 K型封口和Delta封口等不同封口方式尤其受到需要防篡改保护的製药灌装商的青睐。餐饮服务采购商对2公升和5公升的角底袋(用于酱料和调味品)的需求量很大,他们认为角底袋可以提高托盘利用率,并且与高密度聚乙烯(HDPE)瓶相比,排放减少了79%。然而,技术挑战——主要是1公升以上规格产品在高温高压蒸馏过程中的顶部空间管理——减缓了欧洲汤品生产线的转型步伐。目前正在进行的关于侧边折角形状和瓶盖排气方面的研发,旨在最大限度地减少压力差,预计将推动带嘴袋市场份额的成长。

区域分析

到2024年,亚太地区将占据38.68%的吸嘴袋市场份额,这主要得益于中国的大型加工厂、日本的热填充研发以及韩国的优质化策略。预计聚乙烯供应过剩将促使到2025年新增500万吨产能。安姆科收购位于古吉拉突邦的Phoenix Flexibles公司,将扩大其在印度价值2,000万美元的医疗包装细分市场的业务,并加速在地化生产。

北美凭藉着完善的食品加工基础设施和以宠物为中心的消费文化,支撑着稳定的需求。然而,基础设施缺口庞大,到2030年,需要400亿美元用于材料回收设施的现代化。即将实施的25%树脂关税加剧了成本压力,但也刺激了区域内对树脂的投资和再生树脂的测试。加之加州2026年可回收物含量强制令,这些政策正推动吸嘴袋市场朝向单一材料聚乙烯(PE)蒸馏形式发展。

欧洲在带吸嘴包装袋市场推行可回收设计法规方面处于领先地位。 Amcor、Mondi 和 Bischof+Klein 等先驱者已将符合 30% PCR 标准的 PP 和 PE 单层包装袋商业化,与 PET/Alu/OPE 三层层级构造相比,可减少 79% 的二氧化碳排放。北欧的补充装计画证明,当低碳包装与便利的线上购买结合时,消费者接受度可以迅速提高。

拉丁美洲已成为产能热点地区:巴西食品产业成长了7.2%,百事公司正在投资2.4亿美元维修一家工厂,计划于2025年运作三台八通道袋装灌装机。墨西哥和哥伦比亚正在扩大循环包装投资的税额扣抵抵免,以吸引跨国加工商,并根据美墨加协定条款开闢对美国的出口通道。

中东和非洲将以8.84%的复合年增长率实现最快成长,主要得益于无菌牛奶、风味水和无铝包装果汁的需求。 SIG Prime 55在肯亚的投入使用以及利乐公司在奈及利亚的促销宣传活动降低了市场进入门槛。节能高效的灭菌技术和经济实惠的安装方案是提升该地区吸嘴袋市场份额的关键因素。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 欧盟快速过渡到可回收的单一材料包装袋结构

- 东亚地区即机能饮料的蓬勃发展推动了热填充吸嘴袋的发展

- 北美宠物湿食品包装从金属罐过渡到杀菌袋

- 非洲无菌乳製品分销的成长为无铝包装袋提供了支持

- 易于倾倒的补充装产品引领北欧美妆电商市场

- 随着硬质包装向软包装的转换加速,巴西的软包装生产线投资激增。

- 市场限制

- 美国多层复合材料的回收管道有限。

- 不稳定的EVOH和尼龙树脂价格给亚太地区的加工商带来压力。

- 品牌所有者对再生材料转型的担忧

- 欧洲1公升以上汤料包装的蒸馏顶部空间不足

- 供应链分析

- 监理展望

- 技术展望

- 波特五力分析

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

- 地缘政治情境的影响评估

第五章 市场规模与成长预测

- 依材料类型

- 塑胶

- 聚对苯二甲酸乙二醇酯(PET)

- 聚乙烯(PE)

- 聚丙烯(PP)

- 乙烯 - 乙烯醇共聚物(EVOH)

- 其他塑料

- 纸

- 金属箔

- 可生物降解和可堆肥材料

- 塑胶

- 依产品类型

- 圆底/圆底

- K 封

- 犁/角底

- 其他产品类型

- 透过使用

- 食物

- 烤肉

- 零嘴零食

- 宠物食品

- 糖果甜点

- 其他食物

- 饮料

- 个人护理和化妆品

- 医疗保健和製药

- 宠物护理

- 其他应用

- 食物

- 透过分销管道

- 直销

- 间接销售

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲和纽西兰

- 亚太其他地区

- 中东和非洲

- 中东

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 埃及

- 其他非洲地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Amcor Plc

- Mondi plc

- Sonoco Products Company

- Constantia Flexibles GmbH

- ProAmpac LLC

- Smurfit WestRock

- Swiss Pac USA

- Winpak Ltd

- Uflex Limited

- Glenroy Inc.

- Flair Flexible Packaging Corp.

- Sealed Air Corp.

- Huhtamaki Oyj

- Bischof+Klein SE

- Interflex Group

- DoyPak Solutions

- Clondalkin Group

第七章 市场机会与未来展望

The spouted pouches market size reached USD 14.5 billion in 2024 and is forecast to expand to USD 19.06 billion by 2030, reflecting a 5.62% CAGR during 2025-2030.

Rising demand for lightweight, resealable, and visually engaging packaging underpins this growth momentum. Regulatory reforms in Europe, functional-beverage innovation in East Asia, and a rigid-to-flexible packaging shift among North American pet food brands are accelerating volume adoption. Early moves toward mono-material, recyclable formats give manufacturers cost and reputation advantages, while improvements in hot-fill and retort performance broaden end-use possibilities across food, beverage, and household categories. Production scale in Asia-Pacific, technology upgrades in Latin America, and a vibrant M&A pipeline led by Amcor, Mondi, and Sonoco are redefining competitive boundaries as companies chase efficiency and circularity.

Global Stand-Up Pouches Market Trends and Insights

Rapid Shift to Mono-Material Recyclable Pouch Structures in EU

The European Union Packaging and Packaging Waste Regulation effective February 2025 requires all consumer packs to be recyclable by 2030 and to contain 30% post-consumer recycled content for plastics. Producers are quickly moving from multi-layer aluminum structures to mono-material polyethylene films that remain compatible with curbside recycling streams. Amcor's Liquiflex AmPrima pouch meets these criteria and reports a 79% reduction in carbon emissions alongside an 84% cut in water use against legacy laminates. Brand owners adopting early see lower extended producer responsibility fees and improved shelf-appeal messaging, while late movers face R&D cost spikes and possible shelf-space loss. The pivot strengthens the spouted pouches market as converters license new sealing technologies and downgauge films without compromising barrier integrity.

On-the-Go Functional Beverage Boom in East Asia Spurring Hot-Fill Pouches

East-Asian consumers are embracing protein shakes, vitamin gels, and meal-replacement drinks in portable portions. Hot-fill tolerance beyond 85 °C allows processors to skip preservatives, extend ambient shelf life, and deliver nutrient-dense formulas. Japan's disaster-preparedness aisle now features Morinaga Seika's five-year "in Jelly Energy Long Life" pouch, validating extreme barrier and retort performance expectations. Start-ups in South Korea triple their year-over-year sales by marketing single-serve spouts for protein mixes targeting female millennials. These breakthroughs inspire adoption in Southeast-Asian convenience stores and premium gyms, giving the spouted pouches market fresh volume pipelines.

Limited Recycling Streams for Multi-Layer Laminates in United States

The U.S. requires USD 36-43 billion in infrastructure upgrades to lift plastics recycling rates to 61% by 2030. Until material recovery facilities can recognize and separate flexible laminates, brand owners hesitate to scale multilayer pouches. Producers are therefore accelerating mono-material development, but transition costs and legacy equipment risks temporarily slow the spouted pouches market.

Other drivers and restraints analyzed in the detailed report include:

- Migration from Metal Cans to Retort Pouches for Wet Pet Food in North America

- Growth of Aseptic Dairy Distribution in Africa Favoring Aluminum-Free Pouches

- Volatile EVOH & Nylon Resin Prices Squeezing APAC Converters

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Plastic structures controlled 71.89% of the spouted pouches market in 2024 as processors valued polyethylene's sealability, polypropylene's heat stability, and PET's clarity. Biodegradable options record a 7.14% CAGR through 2030 on regulatory and consumer pull, yet still address small-run SKUs. Accredo Packaging's sugarcane-derived resin pouch offsets 43 grams of CO2 per unit while offering drop-in machinability. Meanwhile, Amcor's AmFiber paper-based barrier laminate targets snack producers searching for aluminum-free shelf life. Specialty EVOH barriers and nylon tie layers continue to protect oxygen-sensitive fillings, but cost spikes reposition them toward high-value nutraceutical lines. The spouted pouches market size for biodegradable grades is projected to cross USD 1 billion by 2028, yet plastics will still anchor core food and beverage volumes. Evolving design-for-recycle guidelines stimulate rapid experimentation, positioning plastics as both incumbent and innovation canvas in the spouted pouches market.

Round-bottom (Doyen) pouches enjoyed 38.66% revenue share in 2024, leveraging mature forming equipment and broad application adoption. Corner-bottom designs, however, climb at 5.77% CAGR due to improved base stability that supports larger fill volumes without secondary cartons. K-seal and delta-seal variants appeal to pharmaceutical fillers needing tamper-evident integrity. Foodservice buyers pursue 2-L and 5-L corner-bottom pouches for sauces and condiments, citing pallet efficiency and 79% emission savings over HDPE bottles. Nonetheless, technical challenges-chiefly head-space management during retort for SKUs exceeding 1 L-slow migration in European soup lines. Continuous R&D in gusset geometry and cap venting aims to minimize pressure differentials, promising to unlock new spouted pouches market share gains.

The Spouted Pouches Market Report is Segmented by Material Type (Plastic, Paper, and More), Product Type (Doyen/Round Bottom, K-Seal, Plow/Corner Bottom, Other Product Types), Application (Food, Beverage, Personal Care and Cosmetics, Healthcare and Pharmaceuticals, Pet Care, Other Application), Distribution Channel (Direct Sales, Indirect Sales), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific dominated with 38.68% share of the spouted pouches market in 2024, underpinned by China's large-scale converting facilities, Japan's hot-fill R&D, and South Korea's premiumization playbook. Expected polyethylene oversupply-5 million tons of new capacity in 2025-pressures film pricing, offering converters raw-material leverage but compressing margins. Amcor's acquisition of Phoenix Flexibles in Gujarat extends reach into India's USD 20 million medical-packaging niche and accelerates localized production.

North America leverages entrenched food-processing infrastructure and pets-first culture to anchor steady demand. Infrastructure gaps loom large, with a USD 40 billion funding requirement to modernize material recovery facilities before 2030. Imminent 25% resin tariffs amplify cost pressures yet are stimulating regional resin investment and recycled resin trials. Coupled with California's 2026 recyclable-content mandate, such policies push the spouted pouches market toward mono-material PE retort formats.

Europe stands at the regulatory vanguard, compelling design-for-recycling across the spouted pouches market. Early adopters-Amcor, Mondi, and Bischof + Klein-already commercialize PP and PE single-web pouches that satisfy the 30% PCR threshold and deliver 79% CO2 cuts versus PET/Alu/OPE triplex structures. Nordic refill programmes prove that consumer uptake can be rapid when lower-carbon packaging meets online convenience.

Latin America emerges as a capacity hotspot. Brazil registers 7.2% food-industry growth, and PepsiCo's USD 240 million plant upgrade will commission three eight-lane pouch fillers in 2025. Mexico and Colombia extend tax credits for circular-packaging investments, attracting multinational converters and opening export corridors into the United States under USMCA provisions.

The Middle East and Africa experiences the fastest CAGR at 8.84%, led by aseptic milk, flavored water, and fruit nectar packed in aluminum-free pouches. SIG's Prime 55 installation in Kenya and Tetra Pak's promotional campaigns in Nigeria lower entry barriers. Energy-efficient sterilization and fitment affordability remain success factors poised to grow regional share within the spouted pouches market.

- Amcor Plc

- Mondi plc

- Sonoco Products Company

- Constantia Flexibles GmbH

- ProAmpac LLC

- Smurfit WestRock

- Swiss Pac USA

- Winpak Ltd

- Uflex Limited

- Glenroy Inc.

- Flair Flexible Packaging Corp.

- Sealed Air Corp.

- Huhtamaki Oyj

- Bischof + Klein SE

- Interflex Group

- DoyPak Solutions

- Clondalkin Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid shift to mono-material recyclable pouch structures in EU

- 4.2.2 On-the-go functional beverage boom in East Asia spurring hot-fill spouted pouches

- 4.2.3 Migration from metal cans to retort pouches for wet pet food in North America

- 4.2.4 Growth of aseptic dairy distribution in Africa favouring aluminium-free pouches

- 4.2.5 Nordic beauty e-commerce driving refill pouch SKUs with easy-pour features

- 4.2.6 CapEx surge in Brazilian pouch-filling lines accelerating rigid-to-flexible switch

- 4.3 Market Restraints

- 4.3.1 Limited recycling streams for multi-layer laminates in the U.S.

- 4.3.2 Volatile EVOH and nylon resin prices squeezing APAC converters

- 4.3.3 Brand-owner concerns over recycled-content migration

- 4.3.4 Retort head-space failures in >1-L European soup packs

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assessment of Geopolitical Scenario Impact

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Plastic

- 5.1.1.1 Polyethylene Terephthalate (PET)

- 5.1.1.2 Polyethylene (PE)

- 5.1.1.3 Polypropylene (PP)

- 5.1.1.4 Ethylene Vinyl Alcohol Copolymer (EVOH)

- 5.1.1.5 Other Plastics

- 5.1.2 Paper

- 5.1.3 Metal Foil

- 5.1.4 Biodegradable and Compostable Materials

- 5.1.1 Plastic

- 5.2 By Product Type

- 5.2.1 Doyen / Round Bottom

- 5.2.2 K-Seal

- 5.2.3 Plow / Corner Bottom

- 5.2.4 Other Product Types

- 5.3 By Application

- 5.3.1 Food

- 5.3.1.1 Baked Food

- 5.3.1.2 Snacked Food

- 5.3.1.3 Pet Food

- 5.3.1.4 Confectionery

- 5.3.1.5 Other Food

- 5.3.2 Beverage

- 5.3.3 Personal Care and Cosmetics

- 5.3.4 Healthcare and Pharmaceuticals

- 5.3.5 Pet Care

- 5.3.6 Other Application

- 5.3.1 Food

- 5.4 By Distribution Channel

- 5.4.1 Direct Sales

- 5.4.2 Indirect Sales

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia and New Zealand

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 Middle East

- 5.5.4.1.1 United Arab Emirates

- 5.5.4.1.2 Saudi Arabia

- 5.5.4.1.3 Turkey

- 5.5.4.1.4 Rest of Middle East

- 5.5.4.2 Africa

- 5.5.4.2.1 South Africa

- 5.5.4.2.2 Nigeria

- 5.5.4.2.3 Egypt

- 5.5.4.2.4 Rest of Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Amcor Plc

- 6.4.2 Mondi plc

- 6.4.3 Sonoco Products Company

- 6.4.4 Constantia Flexibles GmbH

- 6.4.5 ProAmpac LLC

- 6.4.6 Smurfit WestRock

- 6.4.7 Swiss Pac USA

- 6.4.8 Winpak Ltd

- 6.4.9 Uflex Limited

- 6.4.10 Glenroy Inc.

- 6.4.11 Flair Flexible Packaging Corp.

- 6.4.12 Sealed Air Corp.

- 6.4.13 Huhtamaki Oyj

- 6.4.14 Bischof + Klein SE

- 6.4.15 Interflex Group

- 6.4.16 DoyPak Solutions

- 6.4.17 Clondalkin Group

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

2025年全球吸嘴袋市场报告2025年全球立式袋市场报告

2025年全球吸嘴袋市场报告2025年全球立式袋市场报告 立式袋市场预测(至 2032 年):按材料类型、封口、产能、最终用户和地区进行的全球分析

立式袋市场预测(至 2032 年):按材料类型、封口、产能、最终用户和地区进行的全球分析 自立袋市场按类型、材料、封口类型、结构、容量和最终用途划分—2025-2030 年全球预测

自立袋市场按类型、材料、封口类型、结构、容量和最终用途划分—2025-2030 年全球预测 全球吸嘴袋市场

全球吸嘴袋市场 全球吸嘴袋市场研究报告 - 产业分析、规模、份额、成长、趋势及预测(2025 年至 2033 年)2030 年化妆品喷袋市场预测:按产品类型、材料、尺寸、分销管道、最终用户和地区进行全球分析

全球吸嘴袋市场研究报告 - 产业分析、规模、份额、成长、趋势及预测(2025 年至 2033 年)2030 年化妆品喷袋市场预测:按产品类型、材料、尺寸、分销管道、最终用户和地区进行全球分析 2025 年至 2033 年吸嘴袋市场报告(按组件、材料、吸嘴袋尺寸、封口类型、最终用户和地区)

2025 年至 2033 年吸嘴袋市场报告(按组件、材料、吸嘴袋尺寸、封口类型、最终用户和地区) 自立袋市场 - 全球产业规模、份额、趋势、机会和预测,按形式、类型、封闭类型、应用、地区和竞争细分,2020-2030 年预测

自立袋市场 - 全球产业规模、份额、趋势、机会和预测,按形式、类型、封闭类型、应用、地区和竞争细分,2020-2030 年预测 立式袋市场规模、份额和增长分析(按形式、类型、封口类型、材料、容量、应用和地区)- 2025-2032 年行业预测

立式袋市场规模、份额和增长分析(按形式、类型、封口类型、材料、容量、应用和地区)- 2025-2032 年行业预测