|

市场调查报告书

商品编码

1906002

骑乘装备:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Riding Gear - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

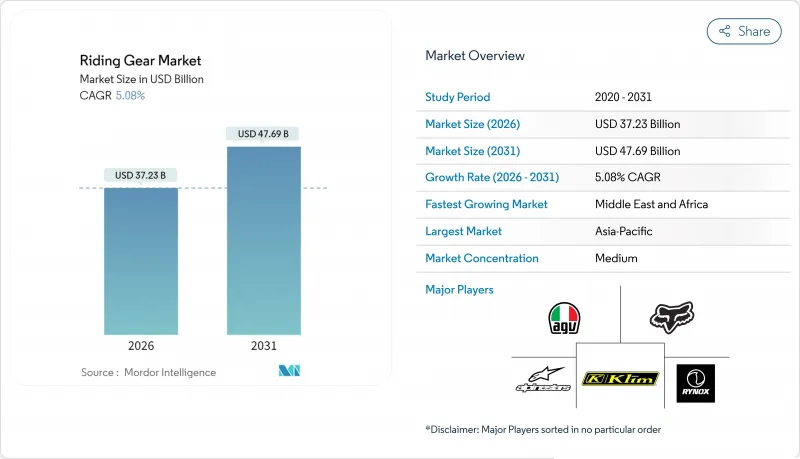

2025年骑行装备市场价值为354.3亿美元,预计到2031年将达到476.9亿美元,高于2026年的372.3亿美元。

预计在预测期(2026-2031 年)内,复合年增长率将达到 5.08%。

强制佩戴头盔、女性骑士的崛起以及气囊夹克的快速普及正在改变市场需求模式,推动摩托车装备从基础防护向创新互联的安全生态系统转型。技术主导的差异化正在缩小高端市场和大众市场之间的差距,碳纤维复合材料和电子感测器等技术正从精英赛车装备走向主流产品。监管协调,特别是欧盟法规2016/425引入CE标誌,使认证装备成为法律强制要求而非个人生活方式选择,从而扩大了目标市场。同时,哈雷戴维森和凯旋等品牌推出的OEM生活风格产品模糊了防护衣和时尚潮流之间的界限,即使在宏观经济波动的情况下,也能支撑其高平均售价。儘管分散的竞争格局持续加剧价格战,但英国驾驶员和车辆标准局(DVSA)等机构对假冒仿冒品的打击,正促使消费者回归值得信赖的品牌,并强化质量至上的购买观念。

全球骑乘装备市场趋势与洞察

新兴市场摩托车拥有量不断成长

印度、印尼和越南摩托车的迅速普及催生了对认证头盔、骑行服和手套的新需求,在短短几个季度内就实现了已开发国家需要数十年才能达到的市场发展水平。印度电动摩托车市场在过去一年中快速成长,显示消费者对安全设备的接受度不断提高,潜在客户群也日益扩大。预计到2024年,中国将出口大量摩托车,占全球出货量的一半以上,将巩固中国作为骑行装备市场大规模生产中心的地位。在这些国家,现代安全法规与机动化进程同步推进,迅速加快了安全装备的普及速度,并使认证装备以前所未有的速度取代了非品牌替代品。能够根据热带气候和价格敏感型客户的需求,量身定制功能丰富的中等价格分布产品线的製造商,正在赢得客户的早期忠诚度,这种忠诚度往往会持续到整个使用周期结束。

更严格的全球安全法规强制要求穿戴防护装备

监管趋势正从建议转向强制性规定。欧盟委员会的EN 17092标准(2018年生效)引入了检验的耐磨性、衝击强度和缝线强度等级,零售商必须在销售点展示这些等级。个人防护设备(PPE)法规加强了对不合规产品的处罚力度,并在海关检查点预先拦截不合格产品。北美机构正在参考类似的ANSI/UL通讯协定,巴西和印尼正在起草类似的法规,预计2026年生效。合规要求提高了技术最低标准,为拥有内部测试实验室或与认证机构长期伙伴关係的生产商创造了优势。缺乏认证预算的新参与企业越来越多地转向与知名品牌签订贴牌生产协议,导致製造技术集中在少数人手中。从中长期来看,统一的全球标准将减少滋生假冒仿冒品贸易的灰色地带,并使高端品牌能够在量产产品中应用传统奢侈品技术,同时降低法律责任风险。

经认证的高级防护装备高成本

认证费、多层材料成本和品牌使用费共同推高了溢价,使得一些新兴市场的买家望而却步。相容安全气囊的皮夹克零售价可高达1,100美元(大致相当于印度一辆普通通勤自行车的价格),迫使骑乘者在购买车辆和全面防护之间做出选择。虽然模组化设计可以降低长期更换零件的成本,但初始成本仍然是一大障碍,尤其是在强制佩戴安全帽的地区。製造商正在尝试与小额信贷机构合作以及订阅模式(将付款分摊到多个季度),但这些模式在北美和欧洲以外的地区应用有限。如果没有大规模的成本创新,一旦早期用户达到饱和,溢价成长速度可能会放缓。

细分市场分析

到2025年,头盔仍将是骑乘装备市场的主导产品,占总收入的24.46%。监管要求和普遍的风险意识意味着头盔不再是可有可无的商品,而是在发生事故或五年使用寿命结束后,必须进行更换的固定产品。头盔技术正在不断发展,例如多密度内衬、旋转力缓解系统和整合式抬头显示器等,这些技术都在推高平均售价,但并未阻碍销量成长。同时,气囊夹克/背心细分市场预计将以5.29%的复合年增长率成长,从而推动对适用于所有摩托车类型的躯干保护解决方案的高端需求。

随着通勤人群的成长,他们越来越多地购买入门级全罩式安全帽,而将购买全套骑乘服的计画推迟到可支配收入增加时。这改变了他们的购买週期,并提高了客户的终身价值。赛车和越野赛事持续推动最尖端科技创新,MotoGP 和 WorldSBK 的 FIM 认证标准使得相关技术能够在两到三个赛季内转移到消费级产品。欧洲一些赛道禁止在头盔上安装运动摄影机,凸显了对空气力学和安全认证的重视,间接推动了对原厂相机介面的需求——这项功能既能支援内容创作者,又能保持安全帽外壳的强度。这些产品类型之间的差异表明,虽然头盔是骑乘装备市场的基础,但电子安全气囊系统正日益成为高端防护装备的代名词。

截至2025年,皮革製品将占骑行装备市场53.11%的份额,这印证了其基于耐磨性和与摩托车文化紧密联繫而经久不衰的吸引力。鞣製牛皮和袋鼠皮因其在公路上的耐用性,在赛车领域仍然备受欢迎。然而,环境问题和不断上涨的皮革成本正促使人造皮革和植物来源合成材料涌现,这些材料在模仿木纹结构的同时,也能减少二氧化碳排放。碳纤维复合材料预计将以5.26%的复合年增长率成长,其重量仅为皮革的几分之一,却能有效分散衝击能量。它们正吸引着那些重视轻量化材料以提升操控性能的高性能骑士的目光。整合到手套和靴子中的碳芳香聚酰胺织物形成超薄保护层,在不牺牲减震性能的前提下,增强了操控灵活性。克维拉、诺梅克斯和考杜拉纤维则占据了中等价格分布市场,它们可水洗、耐候,为温暖气候下的骑行季提供了更多选择。

混合製造技术将滑行区的皮革外层与衝击点的碳纤维或克维拉纤维面板相结合,兼顾了安全性和轻量化,使其在各个价格分布都广受欢迎。这种整合方式实现了供应链的模组化,使供应商能够根据监管法规和客户预算调整材料配比。传统上被丢弃的复合材料边角料,如今正透过热解和化学解聚等方式进行回收利用,将高端创新与永续性理念相结合,从而赢得了年轻骑士的青睐。整体而言,材料技术的进步正推动传统皮革产品保持其销售优势,而利润率和品牌价值则日益集中在尖端复合材料领域。

区域分析

到2025年,亚太地区将占全球摩托车收入的38.55%,其销售密度远超其他任何地区,主要得益于中国3,676万辆的摩托车出口量以及印度电动摩托车的快速普及。该地区的骑行装备市场规模受益于政府强制要求骑士和乘客佩戴认证头盔,从而迅速提升了安全标准。本土製造商正透过与天猫和Flipkart等正规电商平台合作,快速扩大规模,并将业务拓展至先前依赖非正规管道的郊区和城市地区。从纱线纺织到最终组装的垂直整合,使亚洲企业能够在不影响CE认证的前提下,以低于进口价格的价格销售产品,从而巩固了该地区的自主性。

中东和非洲地区将迎来最快成长,到2031年复合年增长率将达到5.37%。基础建设和共享出行平台的普及,使得摩托车通勤在开罗、内罗毕和拉各斯等城市根深蒂固。海湾地区的富裕爱好者偏好欧洲奢侈品牌,而快速成长的非洲送货车队则优先考虑能够抵御热带暴雨的耐用纺织服装。发展机构正在推广穿戴式安全装备的津贴,并辅以捐助者资助的头盔支持,以加速零工经济骑士佩戴防护服的普及。同时,拉丁美洲将实现个位数的温和成长,其中巴西和哥伦比亚将引领这一成长。由于国内服装产能仅能满足五分之三的需求,因此需要进口经过认证的欧洲和亚洲产品。

北美和欧洲市场成熟且盈利,平均更换週期为四到六年,但骑乘者愿意为更高的安全性支付额外费用。欧元区的通货膨胀并未抑制对二级防护装备和内置安全气囊的需求,这表明高所得群体对价格具有弹性。德国的「EcoBonus」政策(该政策将适用于2025年之前的冬季通勤用电加热手套)就是一个很好的例子,说明地方法规如何鼓励人们使用夹克和头盔以外的其他配件。虽然安全标准在各地区日益全球化,供应链也日益同质化,但气候多样性仍对区域产品开发产生影响。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 新兴市场摩托车拥有量不断成长

- 更严格的全球安全法规强制要求穿戴防护装备

- 探险旅行和长途骑行文化的蓬勃发展

- 摩托车品牌拓展OEM生活风格产品

- 由于价格下降,气囊夹克迅速普及。

- 女性骑士人数的成长导致对专业服装的需求增加。

- 市场限制

- 经认证的高级防护装备高成本

- 由于假冒CE标誌产品氾滥,导致信任度下降。

- 寒冷地区季节性需求下降

- 永续性议题引发了对动物源皮革材料的强烈反对

- 价值/供应链分析

- 监管环境

- 技术展望

- 波特五力模型

- 新进入者的威胁

- 买方/消费者的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模及成长预测(价值(美元))

- 依产品类型

- 夹克

- 头盔

- 手套

- 裤子/裤子

- 靴子/鞋子

- 防弹衣

- 安全气囊外套/背心

- 材料

- 皮革

- 纺织品

- 网

- 碳纤维复合材料

- 克维拉/芳香聚酰胺混合物

- 延伸阅读

- 透过分销管道

- 在线的

- 离线

- 最终用户

- 公路驾驶

- 越野/摩托车越野赛

- 探险与旅游

- 通勤者

- 按价格分布

- 优质的

- 中檔

- 经济

- 按地区

- 北美洲

- 美国

- 加拿大

- 北美其他地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 亚太其他地区

- 中东和非洲

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 土耳其

- 埃及

- 南非

- 其他中东和非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- AGVSport

- Alpinestars SpA

- Dainese SpA

- Fox Racing Inc.

- Klim Technical Riding Gear

- REV'IT!Sport International

- ScorpionEXO

- Icon Motorsports

- Royal Enfield Gear

- HJC Helmets

- Shoei Co., Ltd.

- Arai Helmet Ltd.

- Bell Helmets

- Rynox Gears India Pvt. Ltd.

- Spartan ProGear Co.

- Kushitani Co., Ltd.

- Held GmbH

- Sena Technologies Inc.

- LS2 Helmets

- Studds Accessories Ltd.

- Komine Co., Ltd.

- Oxford Products Ltd.

- Thor MX

第七章 市场机会与未来展望

The Riding Gear Market was valued at USD 35.43 billion in 2025 and estimated to grow from USD 37.23 billion in 2026 to reach USD 47.69 billion by 2031, at a CAGR of 5.08% during the forecast period (2026-2031).

Mandatory helmet laws, widening female rider participation, and rapid adoption of air-bag jackets have reshaped demand patterns, pivoting the category from basic protection toward innovative, connected safety ecosystems. Technology-led differentiation tightens the gap between premium and mass segments as carbon-fiber composites and electronic sensors migrate from elite racing gear to mainstream products. Regulatory harmonization, most notably CE Marking under Regulation (EU) 2016/425, has expanded the addressable base by making certified gear a legal necessity rather than a lifestyle choice. At the same time, OEM lifestyle merchandising by brands such as Harley-Davidson and Triumph is blurring the divide between protective apparel and aspirational fashion, sustaining higher average selling prices despite macro-economic volatility. Fragmented competition continues to spur price rivalry, yet counterfeit crackdowns by agencies like the U.K. Driver and Vehicle Standards Agency are steering consumers back to reputable labels, reinforcing quality-driven purchasing behavior.

Global Riding Gear Market Trends and Insights

Rising Motorcycle Ownership In Emerging Markets

Spiraling two-wheeler uptake in India, Indonesia, and Vietnam translates into first-time purchases of certified helmets, jackets, and gloves, compressing what took decades in developed economies into a few selling seasons. Over the past year, sales in India's electric two-wheeler market have surged, underscoring robust growth and heightened consumer acceptance, instantly widening the safety-gear addressable base. China exported a huge number of motorcycles in 2024, more than half of global unit shipments, strengthening the country's status as the volume engine of the riding gear market. Because these countries implement modern safety rules concurrently with motorization, penetration curves steepen quickly, letting certified gear displace unbranded alternatives in record time. Manufacturers able to calibrate feature-rich mid-range lines for tropical climates and price-sensitive customers are capturing early loyalty that tends to persist through the ownership cycle.

Stricter Global Safety Regulations Mandating Protective Gear

Regulatory momentum continues to move from recommendation toward obligation. The European Commission's EN 17092 classification, effective 2018, introduced verifiable abrasion, impact, and seam-strength gradations that retailers must display at point of sale. The Personal Protective Equipment Regulation amplifies penalties for non-compliance, pre-emptively banning sub-standard imports at customs checkpoints. North American agencies reference similar ANSI/UL protocols, while Brazil and Indonesia are drafting mirror statutes slated for 2026. Compliance requirements raise the minimum technological baseline and create a moat around producers with in-house testing labs or long-standing notified-body partnerships. Market entrants lacking certification budgets now pivot toward private-label contracts for established brands, effectively consolidating manufacturing know-how under fewer roof-tops. Over the medium term, uniform global standards shrink the gray zone that fueled counterfeit trade, allowing premium players to cascade former high-end technologies into volume ranges with reduced liability exposure.

High Cost Of Certified Premium Protective Gear

Certification fees, multi-layer material bills, and brand royalties add sizable premiums that price out a portion of emerging-market buyers. An airbag-ready leather jacket can retail at USD 1,100-nearly the same as a basic commuter motorcycle in India-forcing riders to choose between vehicle acquisition and comprehensive protection. While modular design lowers replacement part costs over time, initial outlay remains a sticking point, particularly where helmet-only laws dominate. Manufacturers experiment with micro-financing partnerships and subscription models that spread payments across riding seasons, but adoption has been limited outside North America and Europe. Absent large-scale cost innovation, premium growth could decelerate once early adopters saturate.

Other drivers and restraints analyzed in the detailed report include:

- Boom In Adventure-Touring And Long-Distance Riding Culture

- OEM Lifestyle Merchandise Expansion By Motorcycle Brands

- Proliferation Of Counterfeit Ce-Marked Products Eroding Trust

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The riding gear market size attributed to helmets remained dominant in 2025 as the category captured 24.46% of revenue. Regulatory mandates and universal risk acknowledgment ensure helmets remain non-discretionary, delivering predictable replacement cycles tied to crash events and five-year age limits. Helmet technology is evolving toward multi-density liners, rotational-force mitigation systems, and integrated heads-up displays, each feature nudging average selling prices upward without deterring unit growth. Simultaneously, the airbag jackets and vests sub-segment, forecast to expand at a 5.29% CAGR, channels premium demand toward torso protection solutions that can pair with any motorcycle style.

A growing segment of commuters now buys entry-level integral helmets first and postpones full riding suits until disposable income improves, creating staggered purchase cycles that enlarge lifetime customer value. Racing and off-road disciplines continue to dictate top-tier innovation, with FIM homologation for MotoGP and WorldSBK feeding trickle-down tech to consumer models within two to three seasons. Helmet-mounted action-camera bans in several European tracks emphasize the premium placed on aerodynamics and safety certification, indirectly lifting demand for factory-integrated camera ports, which maintain shell integrity while serving content creators. Collectively, these product-type nuances affirm that while helmets secure the broad base of the riding gear market, electronic airbag systems increasingly frame the narrative around premium protection.

Leather accounted for 53.11% of the riding gear market share in 2025, underscoring its enduring appeal built on abrasion resistance and cultural association with motorcycling. Tanned cowhide and kangaroo leather remain favored in racing for their slide durability. Still, environmental scrutiny and rising hide costs are opening avenues for lab-grown or plant-based synthetics that mimic grain structure while lowering CO2 footprints. Carbon-fiber composites, projected for a 5.26% CAGR, achieve crash energy dispersion at fractions of leather's weight, capturing the imagination of performance riders who equate reduced mass with handling gains. Integrated carbon-aramid weaves in gloves and boots yield ultra-thin protective layers, supporting dexterity without sacrificing impact mitigation. Kevlar, Nomex, and Cordura textiles fill the mid-market niche, offering washable, weather-proof alternatives that expand riding seasons in temperate climates.

Hybrid manufacturing combines leather exteriors for slide zones with carbon-fiber or Kevlar panels over impact points, achieving a safety-weight equilibrium that appeals across price tiers. Such fusion builds modularity into supply chains, letting vendors dial material splits based on regulatory destination and customer budget. Recycling pathways for composite off-cuts traditionally landfill waste are emerging through pyrolysis and chemical depolymerization, aligning premium innovation with sustainability credentials that resonate with younger riders. Altogether, material advancements ensure that heritage-rich leather continues to dominate unit volumes, yet cutting-edge composites are where margins and branding prestige now concentrate.

The Riding Gear Market Report is Segmented by Product Type (Jackets and More), Material (Leather, Textile, and More), Distribution Channel (Online and Offline), End-User (On-Road Riding, Off-road/Motocross, and More), Price Range (Premium, Mid-Range, and Economy), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific contributed 38.55% of global revenue in 2025, rivaled by no other region in sheer unit density due to China's 36.76 million motorcycle exports and India's surging electric two-wheeler adoption. The riding gear market size in the area benefits from governments enforcing the use of certified helmets for riders and pillion riders alike, instantly elevating baseline protection standards. Local manufacturers scale rapidly by partnering with regulated e-commerce platforms, such as T-Mall and Flipkart, thereby amplifying their reach to peri-urban clusters that were previously dependent on informal channels. Vertical integration-from yarn spinning to final assembly enables Asian companies to undercut imported gear without compromising CE compliance, thereby cementing regional self-sufficiency.

The Middle East and Africa region registers the fastest 5.37% CAGR through 2031 as infrastructural upgrades and ride-sharing platforms normalize two-wheel commuting across Cairo, Nairobi, and Lagos. Gulf states' affluent hobbyist riders gravitate toward premium European labels, yet burgeoning African courier fleets prefer rugged textile gear capable of enduring tropical downpours. Development agencies advocate wearable safety grants in conjunction with donor-funded helmets, fostering early adoption of protective jackets among gig-economy riders. Meanwhile, Latin America records mid-single digit growth anchored by Brazil and Colombia, where domestic apparel capacity meets only three-fifth of demand, opening import lanes for certified European and Asian products.

North America and Europe remain mature but lucrative; replacement cycles average 4-6 years, but riders willingly pay premiums for incremental safety gains. Eurozone inflation has not dampened demand for Level-2 armor and integrated airbags, indicating price elasticity in upper-income segments. Policy tools such as Germany's 2025 eco-bonus for electrically heated gloves during winter commuting illustrate how municipal regulations can nudge accessory uptake beyond core jackets and helmets. Across all geographies, convergence toward global safety standards homogenizes supply chains, yet climatic diversity keeps product development regionally nuanced.

- AGVSport

- Alpinestars S.p.A.

- Dainese S.p.A.

- Fox Racing Inc.

- Klim Technical Riding Gear

- REV'IT! Sport International

- ScorpionEXO

- Icon Motorsports

- Royal Enfield Gear

- HJC Helmets

- Shoei Co., Ltd.

- Arai Helmet Ltd.

- Bell Helmets

- Rynox Gears India Pvt. Ltd.

- Spartan ProGear Co.

- Kushitani Co., Ltd.

- Held GmbH

- Sena Technologies Inc.

- LS2 Helmets

- Studds Accessories Ltd.

- Komine Co., Ltd.

- Oxford Products Ltd.

- Thor MX

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Motorcycle Ownership In Emerging Markets

- 4.2.2 Stricter Global Safety Regulations Mandating Protective Gear

- 4.2.3 Boom In Adventure-Touring And Long-Distance Riding Culture

- 4.2.4 OEM Lifestyle Merchandise Expansion By Motorcycle Brands

- 4.2.5 Rapid Adoption Of Airbag-Integrated Jackets After Price Drop

- 4.2.6 Growing Female Rider Segment Demanding Tailored Apparel

- 4.3 Market Restraints

- 4.3.1 High Cost Of Certified Premium Protective Gear

- 4.3.2 Proliferation Of Counterfeit Ce-Marked Products Eroding Trust

- 4.3.3 Seasonality Dampening Demand In Cold Regions

- 4.3.4 Sustainability Backlash Against Animal-Based Leather Materials

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD))

- 5.1 By Product Type

- 5.1.1 Jackets

- 5.1.2 Helmets

- 5.1.3 Gloves

- 5.1.4 Pants / Trousers

- 5.1.5 Boots / Shoes

- 5.1.6 Body Armor & Protectors

- 5.1.7 Airbag Jackets & Vests

- 5.2 By Material

- 5.2.1 Leather

- 5.2.2 Textile

- 5.2.3 Mesh

- 5.2.4 Carbon-Fiber Composites

- 5.2.5 Kevlar / Aramid Blends

- 5.2.6 Other Materials

- 5.3 By Distribution Channel

- 5.3.1 Online

- 5.3.2 Offline

- 5.4 By End-user

- 5.4.1 On-road Riding

- 5.4.2 Off-road / Motocross

- 5.4.3 Adventure & Touring

- 5.4.4 Commuter

- 5.5 By Price Range

- 5.5.1 Premium

- 5.5.2 Mid-range

- 5.5.3 Economy

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 Turkey

- 5.6.5.4 Egypt

- 5.6.5.5 South Africa

- 5.6.5.6 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 AGVSport

- 6.4.2 Alpinestars S.p.A.

- 6.4.3 Dainese S.p.A.

- 6.4.4 Fox Racing Inc.

- 6.4.5 Klim Technical Riding Gear

- 6.4.6 REV'IT! Sport International

- 6.4.7 ScorpionEXO

- 6.4.8 Icon Motorsports

- 6.4.9 Royal Enfield Gear

- 6.4.10 HJC Helmets

- 6.4.11 Shoei Co., Ltd.

- 6.4.12 Arai Helmet Ltd.

- 6.4.13 Bell Helmets

- 6.4.14 Rynox Gears India Pvt. Ltd.

- 6.4.15 Spartan ProGear Co.

- 6.4.16 Kushitani Co., Ltd.

- 6.4.17 Held GmbH

- 6.4.18 Sena Technologies Inc.

- 6.4.19 LS2 Helmets

- 6.4.20 Studds Accessories Ltd.

- 6.4.21 Komine Co., Ltd.

- 6.4.22 Oxford Products Ltd.

- 6.4.23 Thor MX

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

摩托车防护骑乘装备市场:依产品类型、材料、技术、性别、销售管道和最终用户划分-2026-2032年全球市场预测

摩托车防护骑乘装备市场:依产品类型、材料、技术、性别、销售管道和最终用户划分-2026-2032年全球市场预测 摩托车骑行装备市场规模、份额及成长分析(按产品、应用和地区划分)-2026-2033年产业预测

摩托车骑行装备市场规模、份额及成长分析(按产品、应用和地区划分)-2026-2033年产业预测 全球拉力赛骑乘装备市场

全球拉力赛骑乘装备市场 固定齿轮自行车市场按应用、车架材料和地区划分

固定齿轮自行车市场按应用、车架材料和地区划分 摩托车骑行装备市场-全球产业规模、份额、趋势、机会和预测,按产品类型(防护装备、服装、鞋类)、配销通路(线上、线下)、地区和竞争情况细分,2020-2030 年预测

摩托车骑行装备市场-全球产业规模、份额、趋势、机会和预测,按产品类型(防护装备、服装、鞋类)、配销通路(线上、线下)、地区和竞争情况细分,2020-2030 年预测 摩托车防护骑乘装备市场:全球2025-2029

摩托车防护骑乘装备市场:全球2025-2029 摩托车骑乘装备市场规模、份额、趋势分析报告:按产品、通路、地区、细分市场预测,2025-2030 年

摩托车骑乘装备市场规模、份额、趋势分析报告:按产品、通路、地区、细分市场预测,2025-2030 年 摩托车骑行装备市场,按产品、按材料、按配销通路、按国家和地区 - 2024-2032 年行业分析、市场规模、市场份额和预测

摩托车骑行装备市场,按产品、按材料、按配销通路、按国家和地区 - 2024-2032 年行业分析、市场规模、市场份额和预测 拉力运动骑乘装备:市场占有率分析、产业趋势/统计、成长预测(2024-2029)

拉力运动骑乘装备:市场占有率分析、产业趋势/统计、成长预测(2024-2029)