|

市场调查报告书

商品编码

1906984

欧洲塑胶瓶盖和封盖:市场份额分析、行业趋势、统计数据和成长预测(2026-2031 年)Europe Plastic Caps And Closures - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

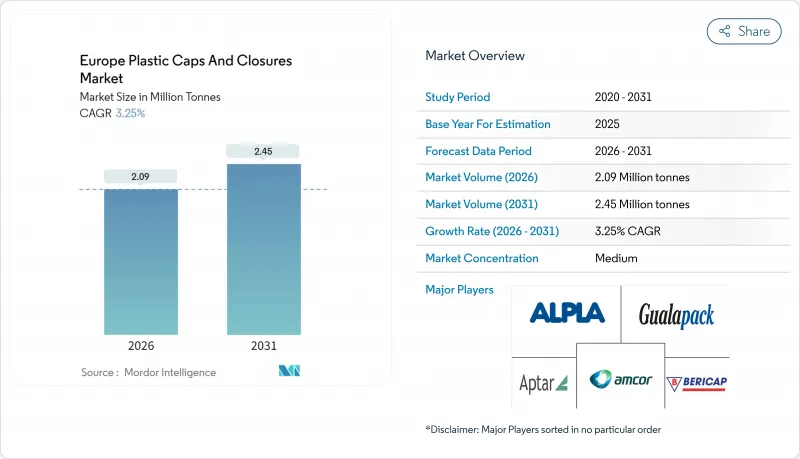

2025 年欧洲塑胶瓶盖和封盖市场价值为 202 万吨,预计到 2031 年将达到 245 万吨,高于 2026 年的 209 万吨。

预计在预测期(2026-2031年)内,该产业将以3.25%的复合年增长率成长。包装和包装废弃物法规(PPWR)的监管力度,以及对再生材料含量要求的不断提高,正在推动该行业销量稳步增长。

轻量化项目将每个瓶盖的树脂用量减少了15-20%,品牌所有者对其供应链碳足蹟的审查日益严格,以及酒类和化妆品包装的高端化趋势,都有助于维持市场需求的韧性。据估计,全部区域用于改造繫绳式维修的资本投资高达3亿欧元,这正在加速技术更新换代,使拥有先进射出成型能力的製造商受益。同时,由于再生树脂短缺和押金返还计划(DRS)的推出,饮料容器转向铝製替代品,这将限製成长空间,但不会影响整体成长轨迹。竞争强度仍然适中,材料创新和智慧封盖功能是关键的差异化因素。

欧洲塑胶瓶盖及封盖市场趋势及分析

轻量化需求推动材料创新

塑胶包装法规 (PPWR) 迫使加工商在保持性能的前提下降低树脂重量,推动聚合物共混物的试验和精密模具设计的更新。这些努力已成功将瓶盖平均重量降低至 0.8 克,且未影响性能。树脂价格波动已对加工商的毛利率造成压力,使其跌破 8%,促使主要企业进行垂直整合并建立内部回收循环以稳定供应。 PET 的轻量化进展,得益于可实现 0.8 毫米侧壁厚度的取向技术,与此聚合物类别 4.39% 的复合年增长率 (CAGR) 相符。 ISO 11469 和 EN 13427 的合规要求增加了研发难度,并巩固了拥有深厚材料专业知识的现有企业的市场份额。中期来看,预计轻量化将使该聚合物类别的预期复合年增长率提高约 0.8 个百分点。

捆绑式总量控制重塑生产经济。

自2024年7月起,所有容量小于3公升的饮料容器都必须使用繫绳式瓶盖,这意味着欧洲约有1350条填充生产线需要维修(每条生产线的成本为15万至30万欧元)。利乐公司已投资3亿欧元,并计划在2024年中期交付超过120亿个符合标准的瓶盖。统一标准EN 17665:2022+A1:2023提供了清晰的合规路径,鼓励射出成型铰链解决方案,并减少监管方面的不确定性。消费者调查显示,基于环保效益,消费者对新标准的接受度高达73%,降低了品牌拥有者的转型风险。短期实施将使市场需求成长1.2个百分点,同时也将增加小型竞争对手的资金门槛。

立式袋改变了家用化学品包装方式

由于可节省 60% 的材料且货架展示效果出色,软包装正从硬质 HDPE 瓶手中夺取清洁剂和清洁产品市场 15-20% 的年市场份额。德国和法国的品牌商试点计画发现,中低价位 SKU 的消费者对软包装袋的接受度高达 68%。到 2030 年,家用化学品瓶盖的需求量可能会下降 8-12%,随着加工商转向使用吸嘴袋的配件,整体复合年增长率 (CAGR) 将降低 0.7 个百分点。

细分市场分析

聚丙烯凭藉其优异的耐化学性和高成本绩效,将在2025年继续保持其在欧洲塑胶瓶盖市场的领先地位,市占率将达到44.38%。此细分市场利用成熟的供应物流和射出成型基础设施,为饮料、食品和家用化学品产业提供大量产品。即使树脂价格波动,透过轻量化措施,每单位产品可减少10-15%的聚丙烯用量,确保成本优势。

聚对苯二甲酸乙二醇酯(PET)重量轻、阻隔性能优异,尤其适用于繫绳盖和无菌乳製品应用,预计将成为成长最快的细分市场,到2031年复合年增长率将达到4.28%。随着回收成分的增加,特别是化学回收获得监管部门核准,欧洲PET塑胶盖和封盖市场规模预计将同步成长。低密度聚乙烯(LDPE)和高密度聚乙烯(HDPE)将在需要柔性分配应用和耐化学腐蚀性的细分市场中保持其地位,而聚氯乙烯(PVC)则因永续性压力而持续失去市场份额。

由于通用相容性和高速生产线效率,标准螺帽在单位经济性方面将继续保持优势,到 2025 年将占据 47.10% 的最大市场份额。然而,随着特殊形状螺帽的普及,预计螺帽在欧洲的市场份额将略有下降。

受药品生产能力扩张以及膳食补充剂和医用大麻产品安全标准不断提高的推动,预计到2031年,儿童安全瓶盖的复合年增长率将达到4.32%。精准计量机制的分配瓶盖将推动个人保健产品和电商补充装生态系统的新需求。按扣式瓶盖和运动专用瓶盖满足了人们随时随地饮用的需求,而带有嵌入式认证晶片的防篡改密封盖则为高端烈酒提供了仿冒品解决方案。

欧洲塑胶瓶盖和封盖市场报告按材料类型(例如,聚对苯二甲酸乙二醇酯 (PET)、聚丙烯 (PP))、产品类型(例如,螺旋盖、按扣盖)、製造类型(例如,射出成型、压缩成型、吹塑成型)、终端用户行业(例如,饮料、食品、药和医疗保健)以及地区进行分析。市场预测以吨为单位。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 欧盟包装和包装废弃物法规要求减轻重量

- 在2024年欧盟指令截止日期前,繫留式容量盖的渗透率很高。

- 乳製品即饮生产线对阻隔性性无菌盖的需求日益增长

- 品牌所有者正在逐步过渡到使用再生瓶盖

- 精酿烈酒的蓬勃发展推动了对优质防篡改瓶盖的需求。

- 电子商务补充装形式的快速成长需要密封封装

- 市场限制

- 立式袋正逐步占领家用化学品市场。

- 押金返还制度鼓励饮料生产商改用铝罐。

- 全大陆范围内供不应求

- 现有PET生产线的繫绳帽改造需要高资本投入。

- 产业价值链分析

- 监管环境

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 竞争对手之间的竞争

- 替代品的威胁

第五章 市场规模与成长预测

- 依材料类型

- 聚对苯二甲酸乙二醇酯(PET)

- 聚丙烯(PP)

- 低密度聚乙烯(LDPE)

- 高密度聚苯乙烯(HDPE)

- 聚氯乙烯(PVC)

- 其他材料

- 依产品类型

- 螺帽

- 卡扣式帽

- 分配盖

- 儿童安全帽

- 防篡改盖

- 其他产品类型

- 透过製造方法

- 射出成型

- 压缩成型

- 吹塑成型

- 按最终用户行业划分

- 饮料

- 食物

- 製药和医疗保健

- 化妆品和盥洗用品

- 家用化学品

- 其他行业

- 按国家/地区

- 德国

- 英国

- 西班牙

- 法国

- 义大利

- 斯洛维尼亚

- 奥地利

- 瑞士

- 匈牙利

- 克罗埃西亚

- 罗马尼亚

- 希腊

- 俄罗斯

- 其他欧洲地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- BERICAP GmbH and Co. KG

- Guala Closures Group

- Pelliconi and CSpA

- UNITED CAPS Luxembourg SA

- Closure Systems International Europe GmbH

- AptarGroup Inc.

- Amcor plc

- ALPLA Werke Alwin Lehner GmbH and Co KG

- Georg Menshen GmbH and Co. KG

- Weener Plastics Group

- Tetra Pak International SA

- Coral Products PLC

- Greiner Packaging International GmbH

- Logoplaste

- Pano Cap Europe Ltd.

第七章 市场机会与未来展望

The Europe plastic caps and closures market was valued at 2.02 million tonnes in 2025 and estimated to grow from 2.09 million tonnes in 2026 to reach 2.45 million tonnes by 2031, at a CAGR of 3.25% during the forecast period (2026-2031).Regulatory momentum under the Packaging and Packaging Waste Regulation (PPWR) drives steady volume expansion as recycled-content mandates tighten.

Lightweighting programs that trim 15-20% resin per cap, heightened brand-owner scrutiny of supply-chain carbon footprints, and premiumization of spirits and cosmetics packaging collectively sustain demand resilience. Capital expenditure on tethered-cap retrofits, estimated at EUR 300 million across the region, accelerates technology refresh cycles and favors manufacturers with advanced injection-molding capabilities. Meanwhile, recycled-resin shortages and deposit-return-scheme (DRS) roll-outs channel beverage volumes into aluminum alternatives, tempering upside but not derailing the overall growth trajectory. Competitive intensity remains moderate, with material innovation and smart-closure functionality serving as primary differentiation levers.

Europe Plastic Caps And Closures Market Trends and Insights

Lightweighting mandates drive material innovation

The PPWR compels converters to shave resin weight while safeguarding performance, prompting polymer-blend experimentation and precision-mold design updates that collectively cut average cap weight to 0.8 g without performance loss. Converter gross margins, already under pressure from resin volatility, narrow below 8%, pushing tier-one players toward vertical integration and captive recycling loops for supply security. PET-oriented lightweighting gains align with a 4.39% CAGR for that polymer class, aided by orientation technologies that permit 0.8 mm sidewalls. ISO 11469 and EN 13427 compliance hurdles elevate R&D thresholds and consolidate share in favor of incumbents with deep materials expertise. Over the medium term, lightweighting is expected to add roughly 0.8 percentage points to the forecast CAGR.

Tethered cap compliance reshapes production economics

From July 2024, every beverage container up to 3 L must feature a tethered closure, triggering retrofits on roughly 1,350 European bottling lines priced at EUR 150,000-300,000 each.Tetra Pak's EUR 300 million investment delivered more than 12 billion compliant caps by mid-2024. Harmonized standard EN 17665:2022+A1:2023 offers a clear compliance pathway that favors injection-molded hinge solutions and mitigates regulatory ambiguity. Consumer research shows 73% acceptance based on environmental benefits, easing brand-owner transition risks. Short-term implementation lifts demand by 1.2 percentage points but also raises capital barriers for smaller competitors.

Stand-up pouches disrupt household chemical packaging

Flexible packaging captures 15-20% annual share from rigid HDPE bottles in detergents and cleaners, courtesy of 60% material savings and strong shelf appeal.Brand-owner trials in Germany and France verify 68% consumer acceptance for pouches in budget and mid-tier SKUs. Closure demand in household chemicals could decline 8-12% through 2030, trimming the overall CAGR by 0.7 percentage points as converters pivot toward spouted pouch fitments.

Other drivers and restraints analyzed in the detailed report include:

- Aseptic packaging evolution in dairy RTD segment

- Brand-owner shift toward recycled-content caps

- Deposit-return schemes favor alternative packaging

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polypropylene leads the Europe plastic caps and closures market with 44.38% share in 2025 due to versatile chemical resistance and attractive cost-to-performance ratios. The segment serves beverages, food, and household chemicals at scale, capitalizing on established supply logistics and mature injection-molding infrastructure. Lightweighting initiatives that cut PP usage by 10-15% per unit lock in cost advantages even as resin prices fluctuate.

Polyethylene terephthalate follows as the fastest mover at a 4.28% CAGR through 2031, propelled by lightweight profiles and robust barrier characteristics that align with tethered-cap and aseptic dairy applications. The Europe plastic caps and closures market size for PET is projected to climb in tandem with its recycled-content credentials, especially as chemical recycling gains regulatory approvals. LDPE and HDPE retain relevance in flexible dispensing and chemical-resistant niches, while PVC continues to lose ground under sustainability pressure.

Standard screw caps maintain the largest footprint at 47.10% of 2025 volumes as universal compatibility and high-speed line efficiency keep per-unit economics compelling. The Europe plastic caps and closures market share for screw caps, however, is likely to edge lower as specialized formats proliferate.

Child-resistant closures enjoy a 4.32% CAGR through 2031, buoyed by expanding pharmaceutical capacity and tightening safety codes across nutraceuticals and cannabis products. Dispensing closures experience renewed momentum in personal-care and e-commerce refill ecosystems, leveraging precision dosing mechanisms. Snap-on and specialty sports caps address on-the-go beverage needs, while tamper-evident seals embed authentication chips to curb counterfeits in premium spirits.

The Europe Plastic Caps and Closures Market Report is Segmented by Material Type (Polyethylene Terephthalate (PET), Polypropylene (PP), and More), Product Type (Screw Caps, Snap-On Caps, and More), Manufacturing Type (Injection Molding, Compression Molding, Blow Molding), End-User Industry (Beverage, Food, Pharmaceutical and Healthcare, and More), and Geography. The Market Forecasts are Provided in Terms of Volume (Tonnes).

List of Companies Covered in this Report:

- BERICAP GmbH and Co. KG

- Guala Closures Group

- Pelliconi and C. S.p.A.

- UNITED CAPS Luxembourg S.A.

- Closure Systems International Europe GmbH

- AptarGroup Inc.

- Amcor plc

- ALPLA Werke Alwin Lehner GmbH and Co KG

- Georg Menshen GmbH and Co. KG

- Weener Plastics Group

- Tetra Pak International S.A.

- Coral Products PLC

- Greiner Packaging International GmbH

- Logoplaste

- Pano Cap Europe Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Lightweighting mandates from EU Packaging and Packaging-Waste Regulation

- 4.2.2 High adoption of tethered caps ahead of 2024 EU directive deadline

- 4.2.3 Growing demand for high-barrier, aseptic-ready closures in dairy RTD lines

- 4.2.4 Brand-owner shift toward recycled-content caps

- 4.2.5 Craft spirits boom driving premium, tamper-evident closures

- 4.2.6 Rapid growth of e-commerce refill formats requiring leak-proof closures

- 4.3 Market Restraints

- 4.3.1 Stand-up pouches encroaching on household-chemical SKUs

- 4.3.2 Deposit-return schemes steering beverage players to aluminum cans

- 4.3.3 Lack of continent-wide rPET/rHDPE food-grade supply

- 4.3.4 High capital intensity for tethered-cap retrofits in legacy PET lines

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Intensity of Competitive Rivalry

- 4.7.5 Threat of Substitute Products

5 MARKET SIZE AND GROWTH FORECASTS (VOLUME)

- 5.1 By Material Type

- 5.1.1 Polyethylene Terephthalate (PET)

- 5.1.2 Polypropylene (PP)

- 5.1.3 Low-Density Polyethylene (LDPE)

- 5.1.4 High-Density Polyethylene (HDPE)

- 5.1.5 Polyvinyl Chloride (PVC)

- 5.1.6 Other Materials

- 5.2 By Product Type

- 5.2.1 Screw Caps

- 5.2.2 Snap-On Caps

- 5.2.3 Dispensing Closures

- 5.2.4 Child-Resistant Closures

- 5.2.5 Tamper-Evident Closures

- 5.2.6 Other Product Types

- 5.3 By Manufacturing Type

- 5.3.1 Injection Molding

- 5.3.2 Compression Molding

- 5.3.3 Blow Molding

- 5.4 By End-User Industry

- 5.4.1 Beverage

- 5.4.2 Food

- 5.4.3 Pharmaceutical and Healthcare

- 5.4.4 Cosmetics and Toiletries

- 5.4.5 Household Chemicals

- 5.4.6 Other Industries

- 5.5 By Country

- 5.5.1 Germany

- 5.5.2 United Kingdom

- 5.5.3 Spain

- 5.5.4 France

- 5.5.5 Italy

- 5.5.6 Slovenia

- 5.5.7 Austria

- 5.5.8 Switzerland

- 5.5.9 Hungary

- 5.5.10 Croatia

- 5.5.11 Romania

- 5.5.12 Greece

- 5.5.13 Russia

- 5.5.14 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 BERICAP GmbH and Co. KG

- 6.4.2 Guala Closures Group

- 6.4.3 Pelliconi and C. S.p.A.

- 6.4.4 UNITED CAPS Luxembourg S.A.

- 6.4.5 Closure Systems International Europe GmbH

- 6.4.6 AptarGroup Inc.

- 6.4.7 Amcor plc

- 6.4.8 ALPLA Werke Alwin Lehner GmbH and Co KG

- 6.4.9 Georg Menshen GmbH and Co. KG

- 6.4.10 Weener Plastics Group

- 6.4.11 Tetra Pak International S.A.

- 6.4.12 Coral Products PLC

- 6.4.13 Greiner Packaging International GmbH

- 6.4.14 Logoplaste

- 6.4.15 Pano Cap Europe Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

塑胶盖子与封口装置市场:2026-2032年全球市场预测(按产品类型、材料、最终用途和分销管道划分)

塑胶盖子与封口装置市场:2026-2032年全球市场预测(按产品类型、材料、最终用途和分销管道划分) 美国塑胶瓶盖和封盖:市场份额分析、行业趋势和统计数据、成长预测(2026-2031 年)

美国塑胶瓶盖和封盖:市场份额分析、行业趋势和统计数据、成长预测(2026-2031 年) 全球塑胶瓶盖和封盖市场规模、份额、趋势和成长分析报告(2026-2034年)

全球塑胶瓶盖和封盖市场规模、份额、趋势和成长分析报告(2026-2034年) 2026年全球塑胶瓶盖和封盖市场报告

2026年全球塑胶瓶盖和封盖市场报告 塑胶瓶盖和封盖市场 - 全球产业规模、份额、趋势、机会和预测(按产品类型、容器类型、原材料、技术、最终用途行业、地区和竞争格局划分,2021-2031年)

塑胶瓶盖和封盖市场 - 全球产业规模、份额、趋势、机会和预测(按产品类型、容器类型、原材料、技术、最终用途行业、地区和竞争格局划分,2021-2031年) 70mm塑胶瓶盖市场规模、份额和趋势分析报告:按材料、应用、地区和细分市场预测,2026-2033年北美塑胶瓶盖及封盖市场:市占率分析、产业趋势、统计及成长预测(2026-2031)

70mm塑胶瓶盖市场规模、份额和趋势分析报告:按材料、应用、地区和细分市场预测,2026-2033年北美塑胶瓶盖及封盖市场:市占率分析、产业趋势、统计及成长预测(2026-2031) 塑胶瓶盖和封盖:全球市场份额和排名、总销售额和需求预测(2025-2031 年)

塑胶瓶盖和封盖:全球市场份额和排名、总销售额和需求预测(2025-2031 年) 2032年塑胶瓶盖和封口市场预测:依产品类型、原料、製造流程、应用和地区分析塑胶瓶盖和封盖:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)

2032年塑胶瓶盖和封口市场预测:依产品类型、原料、製造流程、应用和地区分析塑胶瓶盖和封盖:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)