|

市场调查报告书

商品编码

1910546

LED照明:市场占有率分析、产业趋势与统计、成长预测(2026-2031年)LED Lighting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

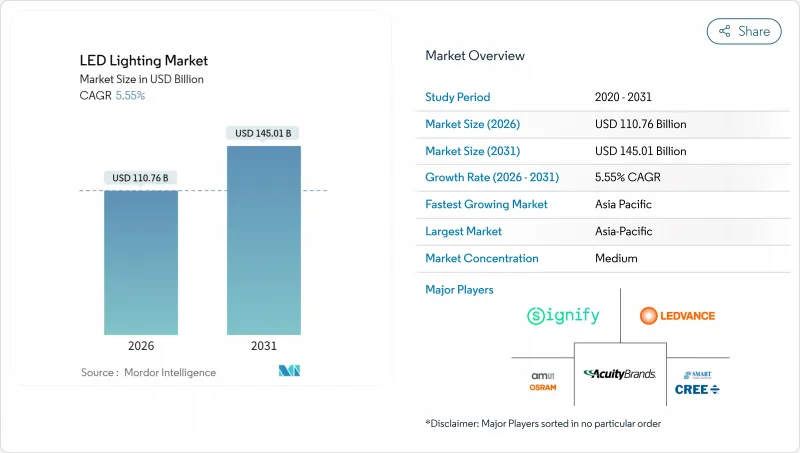

LED照明市场预计将从2025年的1,049.3亿美元成长到2026年的1,107.6亿美元,预计到2031年将达到1,450.1亿美元,2026年至2031年的复合年增长率为5.55%。

这一转变标誌着产业正从快速普及的早期阶段过渡到稳定的、以替换为主导的阶段,在这个阶段,品质差异化和整合控制将决定竞争优势。政府逐步淘汰低效率照明设备、2014年至2016年间安装设备的二次更换需求以及智慧城市计画的加速推进,都是关键的需求驱动因素。将感测器、网路介面和附加价值服务与LED硬体整合的製造商,更有可能获得大规模的合约和长期的客户关係。同时,以三星计画退出市场为代表的供应端整合,加剧了剩余供应商之间的竞争,加速了争夺销售管道和维持利润率的竞赛。

全球LED照明市场趋势与洞察

政府奖励与逐步淘汰政策推动市场转型

政策干预仍然是LED照明市场最强的驱动力。澳洲的《温室气体和能源最低标准条例》(2026年3月生效)提高了最低能源效率标准,并将白炽灯禁令延长至2030年,为製造商提供了明确的合规时间表,并降低了库存积压的风险。美国也呈现类似的趋势,联邦标准指导州和地方政府的采购,从而建立了可预测的大量采购管道。费城更换13.1万个照明灯具(消费量降低50%,每年节省240万美元)等城市规模的改造项目,已向其他城市证明了其合理性。这些政策确保只有符合标准的高品质灯具才能在市场上销售,从而推高了平均售价,并使拥有强大认证组合的品牌受益。

智慧城市基础建设加速LED普及

智慧城市投资正在将照明转变为城市管理的数据基础设施,从而提升每盏照明设备的战略价值。米尔顿凯恩斯部署了2万盏配备感测器的LED路灯,节能40%,并增加了交通和空气品质监测功能。帕拉马塔实现了65%的节能,并将照明节点整合到覆盖全市的物联网网路中,从而支援照明功能以外的产生收入服务。这些案例表明,LED照明市场正在从销售商品产品转向销售具有长期服务合约和数据平台收入来源的多学科计划。

高昂的初始成本限制了高端市场的扩张。

入门级和高阶智慧灯具之间的价格差异依然显着,这在对成本敏感的地区阻碍了其普及。虽然组件成本逐年下降,但可调频谱、整合感测器和强大的温度控管等先进功能仍然推高了组件成本。因此,LED照明市场呈现两极化,基础型号的竞争完全依赖价格,而高级产品则主打降低生命週期成本,但部分买家仍然低估了其价值。新兴市场、中小企业以及资金有限的市政预算面临着最为严峻的限制,减缓了高利润率的智慧化和人性化产品的普及。

细分市场分析

2025年,灯具将占LED照明销售额的61.45%,这显示消费者对整合光学元件、散热器和控制系统的一体化设计需求旺盛。这项优势使得能够根据特定建筑和工业规范开发产品的全套灯具供应商能够获得更大的LED照明市场份额。灯具品类平均售价高,更换週期长,有助于稳定製造商的现金流。同时,受住宅和轻型商业插座二次更换需求的推动,灯泡市场预计将以8.29%的复合年增长率成长。 Cree LED的XLamp XFL灯泡采用紧凑型机壳,亮度高达20,000流明,是灯泡技术创新的典范,为便携式照明提供了显着的性能提升。

随着二次更换趋势的兴起,对于那些希望快速提升照明性能而无需布线或安装天花板的业主来说,灯具变得更加重要。然而,在LED照明市场,那些整合网路控制功能并支援公用事业补贴申请流程的灯具製造商,透过增强客户留存率,持续获得竞争优势。企业同时提供维修灯具和新型连网灯具的混合策略,能够有效地满足既注重预算又注重效能的客户的需求。

到2025年,批发零售通路将占据53.55%的市场份额,因为承包商和设施管理人员重视产品的即时可得性、技术指导和售后支援。该通路透过确保计划进度并符合当地法规和规范,为LED照明市场奠定了基础。然而,由于住宅消费者和小型企业越来越多地选择直接送货上门,预计到2031年,电子商务将以6.62%的复合年增长率实现最快增长。像哈维尔斯(Havells)这样的製造商正在利用双渠道模式,在南卡罗来纳州安德森开设库存充足的仓库,同时也与独立的照明分销商保持合作关係。

数位化购买流程利用标准化的产品目录和丰富的多媒体内容,简化了产品选择流程。然而,对于复杂的商业维修,能够提供光度布局、返利协调和现场故障排除服务的批发商仍然具有优势。因此,将线上配置器与本地取货或快速配送相结合的全通路策略能够触及最广泛的客户群。

区域分析

亚太地区在2025年将以42.10%的收入份额引领LED照明市场,这主要得益于中国的大规模製造业和印度的基础建设。印度政府的「UJALA」灯泡分发计画和广泛的智慧城市计画等措施持续推动着市场需求,而本土製造商则利用其成本优势为海外计划供货。预计到2031年,该地区将以7.58%的复合年增长率实现最高增速,这主要得益于加速的都市化、奖励策略的建筑需求以及人们对互联照明生态系统日益增长的需求。来自韩国和日本元件製造商的高效晶片供应,使亚太地区的照明品牌能够在性能和价格方面都具备全球竞争力。

北美地区仍保持强劲的市场地位,这得益于严格的节能标准、能源服务公司(ESCO)合约以及联邦政府优先发展LED基础设施的支出。各州政府的奖励措施,加上市政永续性发展目标,正在推动路灯和公共设施中LED照明的快速普及。商业新建计划正在部署智慧连网灯具以满足居住者健康标准,而仓库和物流设施也逐步采用高棚LED灯以降低营运成本。然而,供应链中断在某些情况下导致计划延期,迫使许多买家从多个供应商采购驱动器和晶片组。

在欧洲,《建筑能源性能指令》和「维修浪潮」推动了成员国大规模的维修,并从中受益。公用事业收费和碳排放税强化了LED升级的经济合理性,而公共采购中的在地采购规则也有利于欧洲品牌。斯堪地那维亚的城市正在领先人性化的照明试点项目,并推广可调光白光照明灯具的广泛应用。同时,中东和非洲的进展并不均衡。虽然石油资源丰富的海湾国家正在投资建立智慧城市模式,但许多非洲国家仍专注于基础电气化,并依赖捐助者资助的LED部署。在拉丁美洲,公共照明专案的能源补贴和特许经营的减少,促进了基于绩效的合约的采用,从而带来了渐进式的进展。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 政府对白炽灯和节能灯的激励措施和逐步淘汰计划

- LED价格下降和效率提高

- 智慧城市基础建设

- 商业建筑和维修蓬勃发展

- 2014年至2016年间安装的LED照明灯具的二次更换週期

- 人性化(昼夜节律)照明解决方案的兴起

- 市场限制

- 高品质LED照明灯具的初始成本较高

- 在恶劣环境下对温度和电压敏感

- 大量劣质、低价进口商品涌入

- 关键供应商退出或併购导致供应链波动;

- 产业价值链分析

- 宏观经济因素的影响

- 监管环境

- 技术展望

- 波特五力分析

- 新进入者的威胁

- 供应商的议价能力

- 买方的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 依产品类型

- 灯

- 照明灯具/照明设备

- 透过分销管道

- 直销

- 批发/零售

- 电子商务

- 按安装类型

- 新推出

- 维修工程

- 透过使用

- 销售办事处

- 零售店

- 饭店业

- 产业

- 高速公路和地方道路

- 建筑学

- 公共场所

- 医院

- 园艺花园

- 住宅

- 车

- 其他(化工、石油天然气、农业)

- 最终用户

- 室内的

- 户外

- 车

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他的

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 其他欧洲

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 东南亚

- 亚太其他地区

- 中东和非洲

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 其他非洲地区

- 中东

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Signify NV

- ams OSRAM AG

- Acuity Brands Lighting Inc.

- Cree LED(SMART Global Holdings)

- LEDVANCE GmbH

- Zumtobel Group AG

- Nichia Corporation

- Seoul Semiconductor Co. Ltd.

- Everlight Electronics Co. Ltd.

- Dialight plc

- LSI Industries Inc.

- Havells India Ltd.

- Syska LED Lights Pvt. Ltd.

- Opple Lighting Co. Ltd.

- Yankon Group Co. Ltd.

- Fagerhult Group

- Current Lighting Solutions LLC

- Leedarson Lighting Co. Ltd.

- TOSPO Lighting Co. Ltd.

- MLS Co. Ltd.

- Hubbell Lighting Inc.

- Panasonic Corporation(Lighting)

- Bridgelux Inc.

- Valmont Industries(Lighting)

第七章 市场机会与未来展望

The LED lighting market is expected to grow from USD 104.93 billion in 2025 to USD 110.76 billion in 2026 and is forecast to reach USD 145.01 billion by 2031 at 5.55% CAGR over 2026-2031.

This trajectory illustrates the sector's transition from rapid early adoption to a stable, replacement-driven phase, where quality differentiation and integrated controls drive competitive success. Government phase-outs of inefficient lamps, a secondary replacement wave for installations completed between 2014 and 2016, and the acceleration of smart-city programs form the primary demand engines. Manufacturers that integrate LED hardware with sensors, network interfaces, and value-added services tend to secure larger contracts and longer customer relationships. Meanwhile, supply-side consolidation, illustrated by Samsung's planned exit, intensifies rivalry among remaining suppliers as they race to secure channel loyalty and defend margins.

Global LED Lighting Market Trends and Insights

Government Incentives and Phase-Outs Drive Market Transformation

Policy intervention remains the strongest accelerator for the LED lighting market. Australia's Greenhouse and Energy Minimum Standards regulation, effective March 2026, raises minimum efficacy thresholds and extends the incandescent ban through 2030, providing manufacturers with clear compliance schedules and mitigating the risk of stranded inventory. Similar dynamics in the United States, where federal standards guide state and municipal procurement, create predictable bulk-purchase pipelines. Citywide conversions such as Philadelphia's 131,000-fixture program, which delivered 50% energy savings and USD 2.4 million annual savings, prove the financial logic to other municipalities. These policies narrow the viable product spectrum to compliant, higher-quality lamps and luminaires, raising the average selling price and rewarding brands with strong certification portfolios.

Smart City Infrastructure Accelerates LED Adoption

Smart-city investments convert lighting into a data backbone for urban management, raising the strategic value of each luminaire. Milton Keynes' deployment of 20,000 sensor-enabled LED streetlights cut energy use by 40% while adding traffic and air-quality monitoring functions.Parramatta achieved 65% energy savings and integrated lighting nodes into city-wide IoT networks that support revenue-generating services beyond illumination. These examples illustrate how the LED lighting market is shifting from commodity product sales to multidisciplinary infrastructure projects that command long-term service contracts and data platform revenue streams.

High Upfront Costs Limit Premium Segment Penetration

Price differentials between entry-level lamps and premium connected luminaires remain sizeable, deterring adoption in cost-sensitive regions. Although component costs decline annually, advanced features such as tunable spectra, integrated sensors, and robust thermal management add to the bill-of-materials pressure. The result is a bifurcated LED lighting market where basic models compete purely on price, while premium offerings rely on lifecycle savings narratives that some buyers still discount. Emerging markets, small businesses, and municipal budgets with limited capital face the sharpest constraints, resulting in slower penetration of high-margin smart and human-centric products.

Other drivers and restraints analyzed in the detailed report include:

- Commercial Construction Boom Fuels Retrofit Demand

- Secondary Replacement Cycle Creates Sustained Demand

- Supply Chain Consolidation Creates Market Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Luminaires captured 61.45% of 2025 revenue, demonstrating how buyers prefer integrated form factors that combine optics, heat sinks, and controls. This dominance has increased the market share of full-fixture vendors in the LED lighting market, which can tailor products to meet specific architectural and industrial specifications. The luminaire category commands higher average selling prices and longer replacement intervals, stabilizing cash flows for manufacturers. Meanwhile, the lamp segment is expected to expand at an 8.29% CAGR, driven by the secondary replacement wave in residential and light-commercial sockets. Cree LED's XLamp XFL, delivering up to 20,000 lumens in compact footprints, exemplifies lamp innovation that supplies specific performance gains for portable lighting.

The secondary replacement trend elevates lamps as owners seek quick performance upgrades without the need for rewiring or ceiling work. Nonetheless, the LED lighting market continues to reward luminaire makers that integrate networked controls and support utility rebate paperwork, deepening customer lock-in. Hybrid strategies, in which firms offer retrofit lamps alongside new connected fixtures, help address both budget-driven and feature-seeking buyers.

Wholesale and retail outlets held a 53.55% share in 2025 because contractors and facility managers rely on immediate product availability, technical guidance, and after-sales support. This channel anchors the LED lighting market by safeguarding project timelines and ensuring compliance with local codes and specifications. E-commerce, however, is on track for the fastest 6.62% CAGR through 2031, as residential consumers and small businesses increasingly adopt direct-to-door fulfillment. Manufacturers such as Havells tapped a dual-channel model by opening a fully stocked warehouse in Anderson, South Carolina, while maintaining relationships with independent lighting agents.

Digital purchase journeys capitalize on catalog standardization and rich media content that demystify the product selection process. Yet complex commercial retrofits still favor wholesalers who provide photometric layouts, rebate coordination, and on-site troubleshooting. Consequently, omni-channel strategies that blend online configurators with local pickup or rapid delivery serve the broadest customer base.

The LED Lighting Market Report is Segmented by Product Type (Lamps, and Luminaires/Fixtures), Distribution Channel (Direct Sales, Wholesale/Retail, and More), Installation Type (New Installation, and Retrofit Installation), Application (Commercial Offices, Retail Stores, and More), End User (Indoor, Outdoor, and More), and Geography (North America, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

The Asia-Pacific region led the LED lighting market, accounting for a 42.10% revenue share in 2025, driven by China's large-scale manufacturing and India's infrastructure development. Government schemes such as India's UJALA bulb distribution and widespread smart-city programs propel continuous demand, while domestic producers leverage cost advantages to supply foreign projects. The region is also expected to exhibit the fastest growth, with a 7.58% CAGR to 2031, underpinned by accelerating urbanization, stimulus-backed construction, and a growing preference for connected lighting ecosystems. Korean and Japanese component firms contribute high-efficacy chips, allowing regional fixture brands to compete globally on both performance and price.

North America maintains a robust position through stringent energy codes, ESCO contracting, and federal infrastructure spending that prioritizes LED conversions. State-level incentives combined with municipal sustainability targets drive high penetration in streetlights and public facilities. Commercial new-build projects integrate networked luminaires to meet occupant-wellness standards, while warehousing and logistics facilities migrate to high-bay LEDs for operational savings. Supply-chain disruptions, however, cause occasional project delays, prompting many buyers to dual-source drivers and chip packages.

Europe benefits from the Energy Performance of Buildings Directive and the Renovation Wave that compel deep retrofits across member states. Utility tariffs and carbon taxes strengthen the economic case for LED upgrades, and local content rules favor European brands for public tenders. Scandinavian cities are spearheading human-centric lighting pilots, advancing the adoption of tunable white fixtures. Conversely, the Middle East and Africa exhibit heterogeneous development; oil-rich Gulf states invest in smart-city showcase projects, while many African nations focus on basic electrification and rely on donor-funded LED rollouts. Latin America is experiencing gradual progress as energy subsidies decline and public lighting concessions encourage the adoption of performance-based contracting.

- Signify N.V.

- ams OSRAM AG

- Acuity Brands Lighting Inc.

- Cree LED (SMART Global Holdings)

- LEDVANCE GmbH

- Zumtobel Group AG

- Nichia Corporation

- Seoul Semiconductor Co. Ltd.

- Everlight Electronics Co. Ltd.

- Dialight plc

- LSI Industries Inc.

- Havells India Ltd.

- Syska LED Lights Pvt. Ltd.

- Opple Lighting Co. Ltd.

- Yankon Group Co. Ltd.

- Fagerhult Group

- Current Lighting Solutions LLC

- Leedarson Lighting Co. Ltd.

- TOSPO Lighting Co. Ltd.

- MLS Co. Ltd.

- Hubbell Lighting Inc.

- Panasonic Corporation (Lighting)

- Bridgelux Inc.

- Valmont Industries (Lighting)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government incentives and phase-outs of incandescent/CFL lighting

- 4.2.2 Falling LED prices and efficiency gains

- 4.2.3 Smart-city infrastructure roll-outs

- 4.2.4 Commercial construction and retrofit boom

- 4.2.5 Secondary replacement cycle for 2014-2016 LED installs

- 4.2.6 Rise of human-centric (circadian) lighting solutions

- 4.3 Market Restraints

- 4.3.1 High upfront cost of quality LED luminaires

- 4.3.2 Thermal/voltage sensitivity in harsh environments

- 4.3.3 Influx of sub-standard low-cost imports

- 4.3.4 Supply-chain volatility after major vendor exits and M&A

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Lamps

- 5.1.2 Luminaires / Fixtures

- 5.2 By Distribution Channel

- 5.2.1 Direct Sales

- 5.2.2 Wholesale / Retail

- 5.2.3 E-commerce

- 5.3 By Installation Type

- 5.3.1 New Installation

- 5.3.2 Retrofit Installation

- 5.4 By Application

- 5.4.1 Commercial Offices

- 5.4.2 Retail Stores

- 5.4.3 Hospitality

- 5.4.4 Industrial

- 5.4.5 Highway and Roadway

- 5.4.6 Architectural

- 5.4.7 Public Places

- 5.4.8 Hospitals

- 5.4.9 Horticulture Gardens

- 5.4.10 Residential

- 5.4.11 Automotive

- 5.4.12 Others (Chemicals, Oil and Gas, Agriculture)

- 5.5 By End User

- 5.5.1 Indoor

- 5.5.2 Outdoor

- 5.5.3 Automotive

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.4.1 UAE

- 5.6.4.5 South-East Asia

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Signify N.V.

- 6.4.2 ams OSRAM AG

- 6.4.3 Acuity Brands Lighting Inc.

- 6.4.4 Cree LED (SMART Global Holdings)

- 6.4.5 LEDVANCE GmbH

- 6.4.6 Zumtobel Group AG

- 6.4.7 Nichia Corporation

- 6.4.8 Seoul Semiconductor Co. Ltd.

- 6.4.9 Everlight Electronics Co. Ltd.

- 6.4.10 Dialight plc

- 6.4.11 LSI Industries Inc.

- 6.4.12 Havells India Ltd.

- 6.4.13 Syska LED Lights Pvt. Ltd.

- 6.4.14 Opple Lighting Co. Ltd.

- 6.4.15 Yankon Group Co. Ltd.

- 6.4.16 Fagerhult Group

- 6.4.17 Current Lighting Solutions LLC

- 6.4.18 Leedarson Lighting Co. Ltd.

- 6.4.19 TOSPO Lighting Co. Ltd.

- 6.4.20 MLS Co. Ltd.

- 6.4.21 Hubbell Lighting Inc.

- 6.4.22 Panasonic Corporation (Lighting)

- 6.4.23 Bridgelux Inc.

- 6.4.24 Valmont Industries (Lighting)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

LED 照明和 OLED 照明:市场分析和製造趋势

LED 照明和 OLED 照明:市场分析和製造趋势 LED嵌灯市场报告:按应用和地区划分(2026-2034年)

LED嵌灯市场报告:按应用和地区划分(2026-2034年) LED照明市场:2026-2032年全球市场预测(依产品类型、安装方式、技术、应用、最终用户及通路划分)相机LED照明市场:2026-2032年全球市场预测(依产品类型、照明类型、应用、最终用户及通路划分)

LED照明市场:2026-2032年全球市场预测(依产品类型、安装方式、技术、应用、最终用户及通路划分)相机LED照明市场:2026-2032年全球市场预测(依产品类型、照明类型、应用、最终用户及通路划分) 2026-2030年全球LED照明市场LED面板灯市场:按安装方式、面板尺寸、产品类型、色温、应用和分销管道划分-全球预测,2026-2032年橱柜LED照明市场:依产品类型、安装类型、安装方式、应用、通路和最终用途划分-2026-2032年全球预测LED灯带控制器市场按应用、颜色类型、控制技术、分销管道、控制方式、安装方式和电压类型划分,全球预测(2026-2032年)

2026-2030年全球LED照明市场LED面板灯市场:按安装方式、面板尺寸、产品类型、色温、应用和分销管道划分-全球预测,2026-2032年橱柜LED照明市场:依产品类型、安装类型、安装方式、应用、通路和最终用途划分-2026-2032年全球预测LED灯带控制器市场按应用、颜色类型、控制技术、分销管道、控制方式、安装方式和电压类型划分,全球预测(2026-2032年) 柔性照明箔市场规模、份额和成长分析:按产品类型、材料类型、应用、最终用户、分销管道、地区和行业预测,2026-2033年

柔性照明箔市场规模、份额和成长分析:按产品类型、材料类型、应用、最终用户、分销管道、地区和行业预测,2026-2033年 LED照明市场分析及预测(至2035年):按类型、产品类型、服务、技术、组件、应用、形状、材质、最终用户和功能划分

LED照明市场分析及预测(至2035年):按类型、产品类型、服务、技术、组件、应用、形状、材质、最终用户和功能划分