|

市场调查报告书

商品编码

1911807

欧洲LED照明:市场占有率分析、产业趋势与统计、成长预测(2026-2031年)Europe LED Lighting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

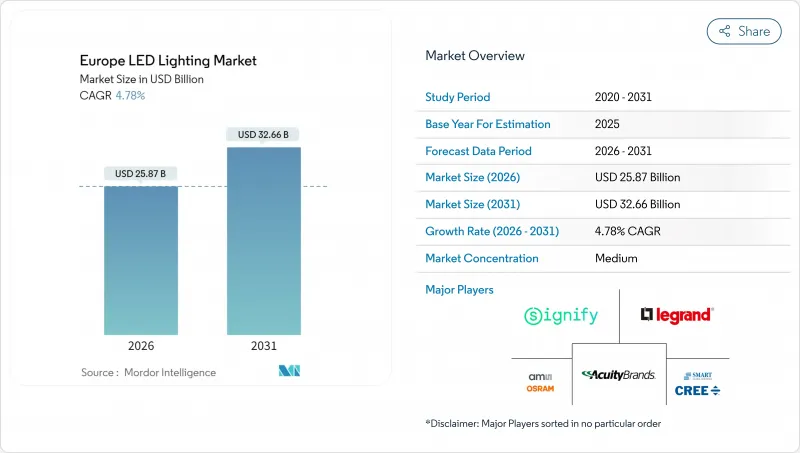

2025年欧洲LED照明市场价值为246.9亿美元,预计到2031年将达到326.6亿美元,高于2026年的258.7亿美元。

预计在预测期(2026-2031 年)内,复合年增长率将达到 4.78%。

这种成长反映了一个成熟的、以更新换代为主导的周期,在这个週期中,监管合规和永续性目标优先于纯粹的技术创新。欧盟范围内的能源效率强制令、卤素灯和萤光的逐步淘汰以及企业的净零排放蓝图将维持对维修的高需求,而每流明成本的下降和智慧城市竞标将扩大新安装的机会。现有供应商将利用安装服务、互联照明平台和循环经济设计来保护其市场份额,而电子商务管道正在降低利基市场新进入者的进入门槛。与稀土元素磷光体相关的供应链风险以及生态设计和废弃电子电气设备指令(WEEE)义务带来的行政负担将限制短期成长潜力,同时阻碍潜在的新竞争者,并稳定大型企业的利润率。

欧洲LED照明市场趋势与分析

欧盟严格的能源效率法规

将于2024年7月生效的《永续产品生态设计法规》(ESPR)将重塑采购模式,优先选择具备LED技术固有特性的产品,例如低能耗、长寿命和高可修復性。计划于2027年实施的数位化产品护照将要求製造商记录其环境足迹,这将加重传统照明设备的合规负担,并促使供应商更加青睐已公布生命週期数据的成熟LED品牌。该法规还禁止从2026年起处置未售出的产品,迫使经销商改善库存管理并迅速清理不合规库存。公共部门资金将透过诸如义大利国家復苏与韧性计画等倡议,重点用于支持合规照明设备。该计画拨款555.2亿欧元(约627.4亿美元)用于能源转型计划。

快速淘汰卤素灯和萤光

欧盟和英国的法规正迫使传统灯具退出市场,迫使各设施无论预算週期如何都必须过渡到LED照明。北欧国家製定了最严格的淘汰期限,引发了区域订单激增,库存充足的供应商从中受益。整合式LED灯具通常会取代整个机壳,儘管销量稳定,但会推高单位成本,从而推高平均售价。提供承包安装服务的製造商正利用监管合规的紧迫性,捆绑销售维护合同,以提高客户留存率。

中小企业价格敏感型维修的投资回收期

如果节能效果无法在两年内收回资本支出,中小企业就会推迟升级改造,这导致儘管监管期限临近,维修规模仍然不足。绩效合约模式,例如丹麦的Lumega计划,虽然免除了前期成本,但其设定的资格要求却阻碍了申请,使得相当一部分已安装照明设备的用户仍然依赖过时的照明系统。

细分市场分析

预计到2025年,灯具类产品将占据欧洲LED照明市场62.10%的份额,这主要得益于市场对整合了光引擎、光学元件和控制系统的全工程化灯具的需求。平均售价的上涨和企划为基础的安装服务推动了该细分市场的收入成长。虽然灯泡绝对值小规模,但预计到2031年将以7.45%的复合年增长率成长,这主要得益于成本下降和智慧灯泡功能推动的维修需求。轨道灯和紧急照明灯具正被广泛应用于商业办公场所,以满足保险法规对合规灯具的要求。循环经济设计,例如LEDVANCE的EVERLOOP系列,展示了可更换模组如何延长产品寿命并满足ESPR的可维修性要求。

就销量而言,灯具出货量成长更为迅速,因为更换灯具无需布线,更符合中小企业的融资需求。同时,照明计划通常与楼宇管理系统集成,产生资料流,设施管理人员可以透过入住率分析将其变现。这一服务层支援高价位,并降低了在日益同质化的硬体市场中利润率下降的风险。

到2025年,批发和零售网路将保持在欧洲LED照明市场51.70%的份额,这主要得益于电气承包商优先考虑物流整合和售前设计支援。同时,电子商务正以5.75%的复合年增长率快速成长,满足了那些重视价格透明和快速交付的中小型企业的需求。製造商目前正在部署混合模式;例如,宜家将线上订购其Jetstrom智慧面板与店内安装支援相结合。由于大型计划需要现场审核和客製化照明设计,直销仍然十分重要。

数位平台上的价格透明化正在挤压经销商的利润空间,同时为供应商提供即时需求数据并提高预测准确性。为了应对这项挑战,经销商正寻求透过增加多层附加价值服务来保障自身生存,例如现场试运行和保固管理。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 欧盟严格的能源效率法规

- 快速淘汰卤素灯和萤光

- 企业净零排放目标推动维修

- 降低LED每流明成本

- 现场可再生能源+直流微电网安装

- 智慧城市竞标项目,融合物联网感测器

- 市场限制

- 中小企业价格敏感型维修的投资回收期

- 稀土元素磷光体供应链的可变性

- 欧盟生态设计/符合WEEE(废弃电子电气设备)指令的复杂性

- 互联照明系统熟练安装人员短缺

- 产业价值链分析

- 宏观经济因素的影响

- 监管环境

- 技术展望

- 波特五力分析

- 新进入者的威胁

- 供应商的议价能力

- 买方的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 依产品类型

- 灯

- 照明灯具/照明设备

- 透过分销管道

- 直销

- 批发/零售

- 电子商务

- 按安装类型

- 新安装

- 维修和安装

- 透过使用

- 商业办公

- 零售店

- 饭店业

- 产业

- 高速公路/普通道路

- 建筑学

- 公共设施

- 医院

- 园艺和花园

- 住宅

- 车

- 其他(化工、石油天然气、农业)

- 最终用户

- 室内的

- 户外

- 车

- 按国家/地区

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 荷兰

- 瑞典

- 波兰

- 俄罗斯

- 其他欧洲地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Signify NV

- Zumtobel Group AG

- Osram Licht AG(ams-Osram)

- Schreder SA

- Fagerhult Group

- Acuity Brands Lighting Inc.

- Havells Sylvania Europe Ltd.

- Legrand SA

- Eaton Corporation plc(Cooper Lighting)

- TRILUX GmbH and Co. KG

- Thorn Lighting Ltd.

- FW Thorpe Plc

- LEDVANCE GmbH

- Helvar Oy Ab

- iGuzzini illuminazione SpA

- Glamox AS

- Cree Lighting Europe SpA

- ITECH LED Lighting

- Hella GmbH and Co. KGaA

- Nichia Europe GmbH

- Samsung Electronics Europe(LED business)

- LG Innotek Europe GmbH

- Valmont Industries(EU lighting poles)

- Opple Lighting Europe BV

第七章 市场机会与未来展望

The European LED lighting market was valued at USD 24.69 billion in 2025 and estimated to grow from USD 25.87 billion in 2026 to reach USD 32.66 billion by 2031, at a CAGR of 4.78% during the forecast period (2026-2031).

Growth reflects a mature, replacement-led cycle in which regulatory compliance and sustainability targets take precedence over the novelty of pure technology. EU-wide energy-efficiency mandates, phase-outs of halogen and fluorescent light bulbs, and corporate net-zero roadmaps keep retrofit momentum high, while falling costs per lumen and smart-city tenders expand new-installation opportunities. Incumbent suppliers capitalize on installation services, connected-lighting platforms, and circular-economy designs to defend share, though e-commerce channels lower barriers for niche entrants. Supply-chain risks surrounding rare-earth phosphors and the administrative burden of eco-design and WEEE obligations temper the near-term upside but also deter potential new competitors, keeping margins stable for scale players.

Europe LED Lighting Market Trends and Insights

Stringent EU Energy-Efficiency Regulations

The Ecodesign for Sustainable Products Regulation (ESPR), which took legal effect in July 2024, reshapes procurement by rewarding products with low energy use, long service life, and high repairability -attributes inherent to LED technology. Digital Product Passports, set for 2027, require manufacturers to document their environmental footprints, thereby increasing the compliance burden for legacy luminaires and strengthening supplier preference for established LED brands that already publish lifecycle data. The regulation also bans the destruction of unsold goods after 2026, compelling distributors to refine their inventory management and accelerate the clearance of non-compliant stock. Public-sector funding funnels into compliant lighting via instruments such as Italy's National Recovery and Resilience Plan, which allocated EUR 55.52 billion (USD 62.74 billion) for energy transition projects.

Rapid Phase-Out of Halogen and Fluorescent Lamps

EU and UK restrictions eliminate legacy lamps from circulation, obliging facilities to adopt LEDs regardless of budget cycles. Nordic countries enforce the shortest sunset dates and have triggered regional spikes in purchase orders that favor suppliers with well-stocked warehouses. Because integrated LED luminaires often replace entire housings, unit revenues rise even as unit counts remain stable, thereby lifting average selling prices. Manufacturers equipped with turnkey installation services capitalize on the urgency of compliance to bundle maintenance contracts, thereby deepening account lock-in.

Price-Sensitive Retrofit Payback Period in SMEs

Small enterprises defer upgrades when energy savings do not repay capital outlays within two years, thereby slowing retrofit volumes, even in the face of looming regulatory deadlines. Performance-contracting models, such as Denmark's Lumega scheme, remove upfront costs but impose qualification hurdles that discourage applicants, leaving a sizable portion of the installed base reliant on outdated lighting.

Other drivers and restraints analyzed in the detailed report include:

- Corporate Net-Zero Commitments Driving Retrofits

- Falling LED Cost per Lumen

- Supply-Chain Volatilities for Rare-Earth Phosphors

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The luminaires category secured 62.10 of % European LED lighting market share in 2025 through demand for fully engineered fixtures that merge light engines, optics, and controls. Segment revenues benefit from higher average selling prices and project-based installation services. Lamps, although smaller in absolute terms, are forecast to grow at a 7.45% CAGR to 2031 as costs decline and smart bulb features unlock retrofit spending. Track lighting and emergency luminaires are adopted in commercial offices where insurance regulations mandate compliant fittings. Circular-economy designs, such as LEDVANCE's EVERLOOP series, highlight how replaceable modules extend life cycles and satisfy ESPR repairability requirements.

In volume terms, lamp shipments rise faster because replacement work requires no rewiring, fitting SME cash-flow constraints. However, luminaire projects often integrate with building management systems, yielding data streams that facility managers monetize through occupancy analytics. This services layer supports premium pricing, reducing the risk of margin compression in an otherwise commoditized hardware landscape.

The wholesale and retail network maintained a 51.70% market share of the European LED lighting market in 2025, driven by electrical contractors who prefer bundled logistics and pre-sale design assistance. Yet e-commerce is expanding at a 5.75% CAGR, serving SMEs that value transparent pricing and rapid delivery. Manufacturers now deploy hybrid models; for instance, IKEA pairs online ordering of its JETSTROM smart panels with in-store support for configuration. Direct sales remain essential for large projects requiring site audits and bespoke photometric design.

Price transparency on digital platforms compresses distributor spreads while also providing suppliers with real-time demand data, thereby improving forecasting accuracy. Distributors respond by layering value-added services, such as on-site commissioning and warranty management, to protect their relevance.

The Europe LED Lighting Market Report is Segmented by Product Type (Lamps, and Luminaires/Fixtures), Distribution Channel (Direct Sales, Wholesale/Retail, and More), Installation Type (New Installation, and Retrofit Installation), Application (Commercial Offices, Retail Stores, and More), End User (Indoor, Outdoor, and More), and Country (United Kingdom, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Signify N.V.

- Zumtobel Group AG

- Osram Licht AG (ams-Osram)

- Schreder SA

- Fagerhult Group

- Acuity Brands Lighting Inc.

- Havells Sylvania Europe Ltd.

- Legrand S.A.

- Eaton Corporation plc (Cooper Lighting)

- TRILUX GmbH and Co. KG

- Thorn Lighting Ltd.

- FW Thorpe Plc

- LEDVANCE GmbH

- Helvar Oy Ab

- iGuzzini illuminazione S.p.A.

- Glamox AS

- Cree Lighting Europe S.p.A.

- ITECH LED Lighting

- Hella GmbH and Co. KGaA

- Nichia Europe GmbH

- Samsung Electronics Europe (LED business)

- LG Innotek Europe GmbH

- Valmont Industries (EU lighting poles)

- Opple Lighting Europe B.V.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stringent EU energy-efficiency regulations

- 4.2.2 Rapid phase-out of halogen and fluorescent lamps

- 4.2.3 Corporate net-zero commitments driving retrofits

- 4.2.4 Falling LED cost per lumen

- 4.2.5 On-site renewable + DC micro-grids adoption

- 4.2.6 Smart-city tenders bundling IoT sensors

- 4.3 Market Restraints

- 4.3.1 Price-sensitive retrofit payback period in SMEs

- 4.3.2 Supply-chain volatilities for rare-earth phosphors

- 4.3.3 Complexity of EU eco-design / WEEE compliance

- 4.3.4 Lack of skilled installers for connected lighting systems

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Lamps

- 5.1.2 Luminaires / Fixtures

- 5.2 By Distribution Channel

- 5.2.1 Direct Sales

- 5.2.2 Wholesale / Retail

- 5.2.3 E-commerce

- 5.3 By Installation Type

- 5.3.1 New Installation

- 5.3.2 Retrofit Installation

- 5.4 By Application

- 5.4.1 Commercial Offices

- 5.4.2 Retail Stores

- 5.4.3 Hospitality

- 5.4.4 Industrial

- 5.4.5 Highway and Roadway

- 5.4.6 Architectural

- 5.4.7 Public Places

- 5.4.8 Hospitals

- 5.4.9 Horticulture Gardens

- 5.4.10 Residential

- 5.4.11 Automotive

- 5.4.12 Others (Chemicals, Oil and Gas, Agriculture)

- 5.5 By End User

- 5.5.1 Indoor

- 5.5.2 Outdoor

- 5.5.3 Automotive

- 5.6 By Country

- 5.6.1 Germany

- 5.6.2 United Kingdom

- 5.6.3 France

- 5.6.4 Italy

- 5.6.5 Spain

- 5.6.6 Netherlands

- 5.6.7 Sweden

- 5.6.8 Poland

- 5.6.9 Russia

- 5.6.10 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Signify N.V.

- 6.4.2 Zumtobel Group AG

- 6.4.3 Osram Licht AG (ams-Osram)

- 6.4.4 Schreder SA

- 6.4.5 Fagerhult Group

- 6.4.6 Acuity Brands Lighting Inc.

- 6.4.7 Havells Sylvania Europe Ltd.

- 6.4.8 Legrand S.A.

- 6.4.9 Eaton Corporation plc (Cooper Lighting)

- 6.4.10 TRILUX GmbH and Co. KG

- 6.4.11 Thorn Lighting Ltd.

- 6.4.12 FW Thorpe Plc

- 6.4.13 LEDVANCE GmbH

- 6.4.14 Helvar Oy Ab

- 6.4.15 iGuzzini illuminazione S.p.A.

- 6.4.16 Glamox AS

- 6.4.17 Cree Lighting Europe S.p.A.

- 6.4.18 ITECH LED Lighting

- 6.4.19 Hella GmbH and Co. KGaA

- 6.4.20 Nichia Europe GmbH

- 6.4.21 Samsung Electronics Europe (LED business)

- 6.4.22 LG Innotek Europe GmbH

- 6.4.23 Valmont Industries (EU lighting poles)

- 6.4.24 Opple Lighting Europe B.V.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

LED 照明和 OLED 照明:市场分析和製造趋势

LED 照明和 OLED 照明:市场分析和製造趋势 LED嵌灯市场报告:按应用和地区划分(2026-2034年)

LED嵌灯市场报告:按应用和地区划分(2026-2034年) LED照明市场:2026-2032年全球市场预测(依产品类型、安装方式、技术、应用、最终用户及通路划分)相机LED照明市场:2026-2032年全球市场预测(依产品类型、照明类型、应用、最终用户及通路划分)

LED照明市场:2026-2032年全球市场预测(依产品类型、安装方式、技术、应用、最终用户及通路划分)相机LED照明市场:2026-2032年全球市场预测(依产品类型、照明类型、应用、最终用户及通路划分) 2026-2030年全球LED照明市场LED面板灯市场:按安装方式、面板尺寸、产品类型、色温、应用和分销管道划分-全球预测,2026-2032年橱柜LED照明市场:依产品类型、安装类型、安装方式、应用、通路和最终用途划分-2026-2032年全球预测LED灯带控制器市场按应用、颜色类型、控制技术、分销管道、控制方式、安装方式和电压类型划分,全球预测(2026-2032年)

2026-2030年全球LED照明市场LED面板灯市场:按安装方式、面板尺寸、产品类型、色温、应用和分销管道划分-全球预测,2026-2032年橱柜LED照明市场:依产品类型、安装类型、安装方式、应用、通路和最终用途划分-2026-2032年全球预测LED灯带控制器市场按应用、颜色类型、控制技术、分销管道、控制方式、安装方式和电压类型划分,全球预测(2026-2032年) 柔性照明箔市场规模、份额和成长分析:按产品类型、材料类型、应用、最终用户、分销管道、地区和行业预测,2026-2033年

柔性照明箔市场规模、份额和成长分析:按产品类型、材料类型、应用、最终用户、分销管道、地区和行业预测,2026-2033年 LED照明市场分析及预测(至2035年):按类型、产品类型、服务、技术、组件、应用、形状、材质、最终用户和功能划分

LED照明市场分析及预测(至2035年):按类型、产品类型、服务、技术、组件、应用、形状、材质、最终用户和功能划分