|

市场调查报告书

商品编码

1910724

欧洲消费品包装市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031年)Europe Consumer Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

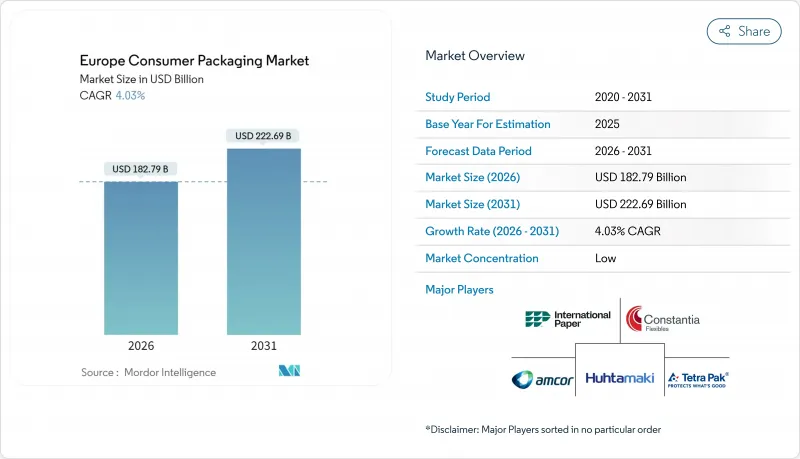

2025年欧洲消费品包装市场价值为1757.1亿美元,预计将从2026年的1827.9亿美元增长到2031年的2226.9亿美元,在预测期(2026-2031年)内复合年增长率为4.03%。

欧盟包装和包装废弃物法规的推出、品牌加速推动闭合迴路系统以及履约履约的持续成长,共同推动了市场成长。纤维、纯PET和轻质金属材料的替代品正在重塑资本配置,而能源价格飙升则迫使加工商调整营运规模。数位印刷技术缩短了从设计到上市的周期,并支持SKU细分,而押金返还计划则透过将回收材料引入高价值饮料应用领域,进一步改变了竞争格局。

欧洲消费品包装市场趋势与洞察

出于便利性考虑,对柔软性塑胶包装的需求增加。

随着都市区外带消费的復苏,软包装正逐渐取代玻璃和金属容器。分装袋包装,加上易开易封的特性,迎合了25至45岁人群的移动生活方式,他们重视便携性和保鲜性。价格波动幅度仍然不大。儘管7微米铝箔的价格在2024年底上涨了4%,但加工商正透过使用带有阻隔涂层的轻质薄膜来抵消成本上涨,从而在不增加体积的情况下延长保质期。如今,功能性比外形更重要,酱料和婴儿食品等液体产品正从较重的硬质容器转向吸嘴袋。因此,软包装在食品和个人护理领域的市场份额持续增长。

电子商务的快速成长催生了对最后一公里包装的需求。

直销物流模式增加了包装必须承受的多重接触点,包括输送机上的跌落、温度变化以及送货上门时的检查。包装废弃物法规 (PPWR) 规定,到 2030 年,40% 的运输和零售包装必须可重复使用,这迫使零售商在自动化和永续性之间寻求平衡。市场对兼具缓衝性和体积效率的模塑纤维内衬和精密设计的瓦楞纸箱的需求正在蓬勃发展。波兰和西班牙的电子商务渗透率成长最快,加剧了欧洲消费品包装市场的区域成长差距。品牌所有者正在利用数位印刷技术将每个小包裹变成行销画布,使开箱体验从成本中心转变为收入来源。

聚合物、纸浆和纸张价格波动

原料价格波动挤压了加工商的利润空间,并扰乱了与季度指数挂钩的固定价格合约。由于下游需求疲软,聚乙烯价格在2024年初走软;而当亚洲供应链不稳定时,PET价格则趋紧,显示预测投入品价格走势十分困难。在纺织业,由于造纸厂停产和物流瓶颈,涂布纸价格在2024年第二季飙升了约10%,之后趋于稳定。向回收和纸浆资产的垂直整合正在获得支持,但这会占用原本可用于创新和地理扩张的资金。

细分市场分析

2025年,纸和纸板市场将维持35.22%的销售份额,主要得益于电商物流供应商和餐饮服务业的一次性产品需求。在有利的法规和消费者意识的提升下,欧洲纸质消费包装市场规模预计将温和成长。然而,PET 5.74%的复合年增长率凸显了市场成长动能的显着转变,这主要得益于押金返还机制的经济效益以及品牌对使用食品级再生材料的承诺。到了2024年,单层PET饮料瓶的平均再生材料含量将达到24%,这推动欧洲消费包装市场份额的成长,也证明闭合迴路的可行性。同时,由于新的法规推动一次性瓶盖、刀叉餐具和轻质购物袋退出市场,PE(聚乙烯)和PP(聚丙烯)市场面临挑战。

PET的优势因其机械回收率可达75%(在优化后的工厂中)而进一步增强,从而缩小了与纤维基纸盒的碳排放差距。同时,玻璃产业协会呼吁投资200亿欧元用于熔炉电气化,但不断上涨的电价正在削弱其竞争力。铝在循环利用方面仍具有优势,但废旧铝罐片的供应量取决于各地区的回收率。特种聚合物在一些对性能要求高于可回收性的领域找到了成长机会,例如药品泡壳包装和个人保健产品的帮浦零件。

其他福利:

- Excel格式的市场预测(ME)表

- 分析师支持(3个月)

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 对注重便利性的柔软性塑胶包装的需求不断增长。

- 电子商务的快速成长催生了对最后一公里包装的需求。

- 转向更轻、更易开启的包装

- 欧盟的《一次性塑胶指令》正在推动对单一材料的研究和发展。

- 押金返还制度促进了对再生聚乙烯(rPET)的需求。

- 数位印刷技术实现了SKU多样化和小批量生产。

- 市场限制

- 聚合物、纸浆和纸张价格波动

- 欧盟扩大难以回收包装的禁令

- 多层柔性包装的回收缺口

- 由于能源价格大幅上涨,玻璃和金属成本也随之上涨。

- 产业供应链分析

- 监管环境

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 材料

- 塑胶

- PE(聚乙烯)

- PP(聚丙烯)

- PET(聚对苯二甲酸乙二醇酯)

- 聚氯乙烯(PVC)

- 其他塑料

- 纸和纸板

- 纸板

- 瓦楞纸板和衬纸

- 模塑纤维

- 玻璃

- 金属

- 能

- 瓶盖和封口

- 管子

- 其他金属

- 塑胶

- 按包装类型

- 难的

- 软包装

- 半刚性

- 按最终用户行业划分

- 食物

- 饮料

- 製药和医疗保健

- 化妆品、个人护理、居家护理

- 其他终端用户产业

- 按国家/地区

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 波兰

- 其他欧洲地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Amcor PLC

- Huhtamaki Oyj

- Mondi PLC

- International Paper Company

- Tetra Pak International SA

- Ardagh Group SA

- Crown Holdings, Inc.

- Constantia Flexibles Holding GmbH

- Sealed Air Corporation

- Sonoco Products Company

- Stora Enso Oyj

- Smurfit Kappa Group Limited

- Ball Corporation

- Berry Global, Inc.

- Greiner Packaging International GmbH

- Albea Group SAS

- Gerresheimer AG

- Vetropack Holding AG

- Massilly Holding

第七章 市场机会与未来展望

The Europe consumer packaging market was valued at USD 175.71 billion in 2025 and estimated to grow from USD 182.79 billion in 2026 to reach USD 222.69 billion by 2031, at a CAGR of 4.03% during the forecast period (2026-2031).

Growth is steered by the EU Packaging and Packaging Waste Regulation, accelerating brand commitments to closed-loop systems, and sustained momentum in e-commerce fulfillment. Material substitution toward fiber, mono-PET, and lightweight metal formats is reshaping capital allocation, while energy-price shocks force converters to reassess operating footprints. The competitive field is further altered by digital printing, which shortens design-to-launch cycles and supports SKU fragmentation, and by deposit-return infrastructure that channels recycled feedstock into high-value beverage applications.

Europe Consumer Packaging Market Trends and Insights

Convenience-driven demand for flexible plastic packs

Flexible formats continue to migrate volume from glass and metal as on-the-go consumption rebounds across urban corridors. Portion-controlled pouches with easy-open reclosable features meet the mobile lifestyle of 25- to 45-year-olds who prize portability and freshness. Price movements remain modest. 7-micron aluminum foil rose 4% in late 2024, but converters offset cost upticks through barrier-coated lightweight films that extend shelf life without adding bulk. Functionality now outweighs format loyalty, drawing liquid applications such as sauces and baby food toward spouted pouches and away from heavier rigid alternatives. The result is sustained share capture for flexibles in both food and personal-care aisles.

E-commerce boom creating last-mile packaging needs

Direct-to-consumer fulfillment adds multiple touchpoints where packs must survive conveyor drops, temperature shifts, and doorstep scrutiny. The PPWR mandates 40% reusable transport and sales packaging by 2030, pressuring retailers to harmonize automation with sustainability. Demand is surging for molded-fiber inserts and precision-engineered corrugated boxes that balance cushioning with dimensional efficiency. Poland and Spain show the steepest e-commerce penetration curves, widening the regional growth gap within the European consumer packaging market. Brand owners also leverage digital print to transform each parcel into a marketing canvas, elevating unboxing to a revenue lever rather than a cost center.

Volatile polymer and paper pulp prices

Feedstock swings erode converter margins and disrupt pricing contracts fixed on quarterly indices. Polyethylene values softened in early 2024 amid weak downstream demand, yet PET tightened when Asian supply lines faltered, demonstrating the difficulty of forecasting input trajectories. On the fiber side, coated paper spiked nearly 10% in Q2 2024 before easing, driven by mill maintenance outages and logistics bottlenecks. Vertical integration into recycling or pulp assets is gaining favor, but it locks capital that could fund innovation or geographic expansion.

Other drivers and restraints analyzed in the detailed report include:

- Shift toward lightweighting and easy-open formats

- EU Single-Use Plastics Directive spurring mono-material R&D

- Expanding EU bans on difficult-to-recycle formats

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Paper and board defended 35.22% of 2025 revenue on the strength of e-commerce shippers and foodservice disposables. The Europe consumer packaging market size for paper-based solutions is projected to expand modestly as regulatory goodwill and consumer perception remain supportive. However, PET's 5.74% CAGR underscores a decisive momentum swing driven by deposit-return economics and brand pledges for food-grade recycled content. Europe consumer packaging market share gains accrue to mono-PET beverage bottles that averaged 24% recycled resin in 2024, validating closed-loop viability. In contrast, PE and PP navigate headwinds from single-use caps, cutlery, and thin grocery bags disappearing under new bans.

The PET narrative is reinforced by mechanical recycling yields that reach 75% in optimized plants, narrowing the carbon delta versus fiber-based cartons. Meanwhile, glass lobbies are campaigning for EUR 20 billion in furnace electrification, but elevated electricity tariffs cloud competitiveness. Aluminum retains a strong circularity story, yet the liquidity of post-consumer can sheet fluctuates with regional redemption rates. Specialty polymers hold pockets of growth in pharma blister packs and personal-care pump components, where performance trumps uniform recyclability mandates.

The Europe Consumer Packaging Market Report is Segmented by Material (Plastic (PE, PP, PET, and More), Paper and Board (Cartonboard, Molded Fiber, and More), Glass, and Metal (Cans, Caps and Closures, Tubes, and More)), Packaging Format (Rigid, Flexible, and Semi-Rigid), End-User Industry (Food, Beverage, Pharmaceutical and Healthcare, and More), and Country. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Amcor PLC

- Huhtamaki Oyj

- Mondi PLC

- International Paper Company

- Tetra Pak International SA

- Ardagh Group S.A.

- Crown Holdings, Inc.

- Constantia Flexibles Holding GmbH

- Sealed Air Corporation

- Sonoco Products Company

- Stora Enso Oyj

- Smurfit Kappa Group Limited

- Ball Corporation

- Berry Global, Inc.

- Greiner Packaging International GmbH

- Albea Group S.A.S.

- Gerresheimer AG

- Vetropack Holding AG

- Massilly Holding

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Convenience-driven demand for flexible plastic packs

- 4.2.2 E-commerce boom creating last-mile packaging needs

- 4.2.3 Shift toward lightweighting and easy-open formats

- 4.2.4 EU Single-Use Plastics Directive spurring mono-material R&D

- 4.2.5 Deposit-return schemes scaling rPET demand

- 4.2.6 Digital printing enabling SKU proliferation and short-runs

- 4.3 Market Restraints

- 4.3.1 Volatile polymer and paper pulp prices

- 4.3.2 Expanding EU bans on difficult-to-recycle formats

- 4.3.3 Recycling gaps for multilayer flexibles

- 4.3.4 Energy-price shocks inflating glass and metal costs

- 4.4 Industry Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material

- 5.1.1 Plastic

- 5.1.1.1 PE (Polyethylene)

- 5.1.1.2 PP (Polypropylene)

- 5.1.1.3 PET (Polyethylene Terephthalate)

- 5.1.1.4 PVC (Polyvinyl Chloride)

- 5.1.1.5 Other Plastics

- 5.1.2 Paper and Board

- 5.1.2.1 Cartonboard

- 5.1.2.2 Containerboard and Linerboard

- 5.1.2.3 Molded Fiber

- 5.1.3 Glass

- 5.1.4 Metal

- 5.1.4.1 Cans

- 5.1.4.2 Caps and Closures

- 5.1.4.3 Tubes

- 5.1.4.4 Other Metals

- 5.1.1 Plastic

- 5.2 By Packaging Format

- 5.2.1 Rigid

- 5.2.2 Flexible

- 5.2.3 Semi-rigid

- 5.3 By End-user Industry

- 5.3.1 Food

- 5.3.2 Beverage

- 5.3.3 Pharmaceutical and Healthcare

- 5.3.4 Cosmetics, Personal and Home Care

- 5.3.5 Other End-user Industry

- 5.4 By Country

- 5.4.1 Germany

- 5.4.2 United Kingdom

- 5.4.3 France

- 5.4.4 Italy

- 5.4.5 Spain

- 5.4.6 Poland

- 5.4.7 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Amcor PLC

- 6.4.2 Huhtamaki Oyj

- 6.4.3 Mondi PLC

- 6.4.4 International Paper Company

- 6.4.5 Tetra Pak International SA

- 6.4.6 Ardagh Group S.A.

- 6.4.7 Crown Holdings, Inc.

- 6.4.8 Constantia Flexibles Holding GmbH

- 6.4.9 Sealed Air Corporation

- 6.4.10 Sonoco Products Company

- 6.4.11 Stora Enso Oyj

- 6.4.12 Smurfit Kappa Group Limited

- 6.4.13 Ball Corporation

- 6.4.14 Berry Global, Inc.

- 6.4.15 Greiner Packaging International GmbH

- 6.4.16 Albea Group S.A.S.

- 6.4.17 Gerresheimer AG

- 6.4.18 Vetropack Holding AG

- 6.4.19 Massilly Holding

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

居家照护包装市场:按产品类型、材料类型、分销管道和最终用户划分-2026-2032年全球市场预测

居家照护包装市场:按产品类型、材料类型、分销管道和最终用户划分-2026-2032年全球市场预测 居家照护包装市场规模、份额、趋势和预测:按产品类型、材料、包装形式和地区划分,2026-2034年

居家照护包装市场规模、份额、趋势和预测:按产品类型、材料、包装形式和地区划分,2026-2034年 快速消费品包装市场规模、份额、成长及全球产业分析:按类型、应用和地区划分,并预测至2026-2034年日常消费品包装市场规模、份额、趋势及预测(按包装类型、材料、最终用途行业和地区划分,2026-2034年)

快速消费品包装市场规模、份额、成长及全球产业分析:按类型、应用和地区划分,并预测至2026-2034年日常消费品包装市场规模、份额、趋势及预测(按包装类型、材料、最终用途行业和地区划分,2026-2034年) 2026年全球居家护理产品包装市场报告月饼包装市场:2026-2032年全球预测(按包装类型、材料、包装形式、印刷技术、最终用户和分销管道划分)居家护理包装市场-2026-2031年预测

2026年全球居家护理产品包装市场报告月饼包装市场:2026-2032年全球预测(按包装类型、材料、包装形式、印刷技术、最终用户和分销管道划分)居家护理包装市场-2026-2031年预测 家居护理包装市场规模、份额及成长分析(按材料、产品类型、包装类型、最终用途和地区划分)-产业预测(2026-2033)

家居护理包装市场规模、份额及成长分析(按材料、产品类型、包装类型、最终用途和地区划分)-产业预测(2026-2033) 快速消费品包装市场规模、份额、成长分析(按类型、材料、最终用途和地区)- 2025-2032 年产业预测

快速消费品包装市场规模、份额、成长分析(按类型、材料、最终用途和地区)- 2025-2032 年产业预测 全球居家护理包装市场

全球居家护理包装市场