|

市场调查报告书

商品编码

1910914

欧洲车队管理:市场占有率分析、产业趋势与统计、成长预测(2026-2031 年)Europe Fleet Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

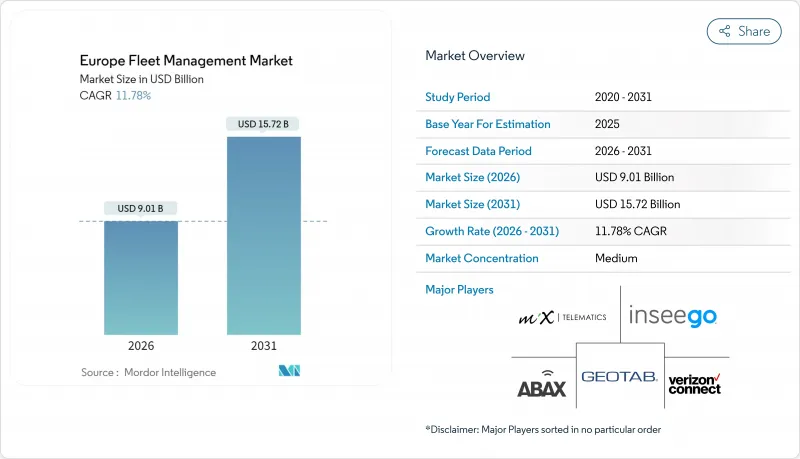

2025年欧洲车队管理市场价值为80.6亿美元,预计到2031年将达到157.2亿美元,高于2026年的90.1亿美元。

预测期(2026-2031 年)的复合年增长率预计为 11.78%。

监管压力不断加大、联网汽车架构的普及以及「最后一公里」物流的日益密集,共同推动了潜在需求的成长。欧盟智慧行车记录器第二阶段法规将于2025年生效,该法规将强制要求即时资料传输,使远端资讯处理技术从可选的效率提升工具转变为一项合规要求。电子商务交易量的成长增加了都市区配送里程,促使营运商进行更精细的路线优化和驾驶员行为分析。同时,蜂巢式物联网资费的下降和eSIM的广泛应用降低了连接成本,而5G网路覆盖范围的扩大将支援人工智慧影像安全监控等高频宽应用。汽车製造商正在开放应用程式介面(API)以实现车辆资料流的商业化,使车队营运商能够直接存取嵌入式远端资讯处理系统。最后,各国碳减量目标和低排放区的实施正在加速电气化进程,这需要更严格的能源和资产协调。

欧洲车队管理市场趋势与洞察

遵守欧盟智慧行车记录器强制令第二阶段的必要性

这项将于2025年6月生效的强制规定,将要求3.5吨以上的商用车辆持续传输位置和行驶时间数据,从定期数据下载转变为即时监控。违者将面临1500欧元至15,000欧元的自动罚款,以强制业者实施整合式远端资讯处理系统。德国大型物流公司已完成系统部署,以避免服务中断。供应商表示,小规模车队也越来越多地要求采用多车订阅模式,而非单一行车记录器。随着营运商倾向于使用统一的管理介面管理所有类型的车辆,这种需求也蔓延至小型货车和公司共乘领域,从而推动了整个平台的普及率。

电子商务的成长加速了最后一公里配送的优化

到2024年,线上销售额将占欧洲零售总额的13.4%,而小包裹递送业者的物流支出中,最后一公里成本将占41%。随着消费者期望隔日送达,轻型货车的行驶里程将比2024年增加23%。像Seur这样的营运商在实施基于人工智慧的调度系统后,将路线相关成本降低了15%,这充分体现了远端资讯处理技术的实际投资回报。巴塞隆纳、马德里和巴黎的低排放区透过限制时限的通行,进一步增加了复杂性,使得即时监管数据至关重要。因此,欧洲车队管理市场正受益于电子商务和环境压力的整合,这需要持续提供位置、交通和合规资讯。

GDPR合规性增加了实施的复杂性

根据GDPR,员工必须明确同意且可撤销地使用GPS追踪功能。 2024年德国的几起法院案例也证实,全面监控侵犯了员工的权利。对于中型车队而言,每年用于法律审查、资料保护官和软体重新设计的成本可能高达约12.5万欧元。跨国营运商在跨境时,如果遇到监管更为严格的国家,可能不得不禁用诸如驾驶员摄影机即时传输等功能,这会抵消远端资讯处理带来的效率提升,并延长实施週期。

细分市场分析

预计到2025年,云端服务将占据欧洲车队管理市场63.55%的份额,并在2031年之前以14.56%的复合年增长率增长,这主要得益于付费使用制和自动软体更新。德国电信指出,与本地部署解决方案相比,多租户架构透过避免伺服器采购和维护义务,可将整体拥有成本降低34%。对于车队管理人员而言,弹性资料储存无需手动扩展,并可协助他们应对资料量的季节性波动。儘管资料主权问题限制了一些关键基础设施车队使用私人伺服器,但云端服务供应商正在透过提供符合GDPR认证的欧盟资料中心来弥补合规性差距。

边缘运算如今已成为云端模式的延伸而非替代:对时间需求较高的驾驶辅助运算在车辆处理器上执行,而汇总的分析、报告和空中下载更新则透过中央枢纽进行路由。这种混合方法既满足了延迟要求,又满足了管治要求,巩固了云端作为欧洲车队管理市场新部署预设架构的地位。

到2025年,资产管理领域将占欧洲车队管理市场规模的26.72%,主要得益于所有营运商对位置和运转率数据的日益重视。同时,随着监管机构和保险公司将经济奖励与预防事故挂钩,安全合规工具将以14.34%的复合年增长率成长。安联为车队提供高达15%的保费折扣,前提是车队能够证明其积极开展驾驶员监控,这加速了高里程宅配服务采用此类工具。欧盟「零愿景」(Vision Zero)计画旨在在2050年实现道路零死亡,该计画已将基于人工智慧的疲劳检测和盲点警告作为多个成员国颁发营运许可证的先决条件。供应商现在将安全仪錶板与行车记录器檔案捆绑在一起,以确保无缝且检验的合规性提交。

其他福利

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 欧盟智慧行车记录器第二阶段强制实施(2025年)

- 电子商务推动轻型商用车行驶里程快速成长

- 蜂巢式物联网费率下降和 eSIM 的普及

- OEM开放API车载资讯服务货币化

- 欧盟排放交易体系(EU ETS)低二氧化碳排放车辆的碳信用额度

- 5G C-V2X 微型编队示范测试

- 市场限制

- GDPR 和 ePrivacy 合规的负担

- 人工智慧视讯远端资讯处理技术的高额资本投入

- 低排放城市区域的拼凑

- 车载资讯服务晶片供应中断

- 产业价值链分析

- 监管环境

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 依部署类型

- 按需(云端)

- 本地部署

- 透过使用

- 资产管理

- 资讯管理

- 驾驶员管理

- 安全合规管理

- 风险管理

- 营运管理

- 按最终用户行业划分

- 运输/物流

- 能源公共产业

- 建造

- 製造业

- 其他终端用户产业

- 按车队规模

- 小规模(1至50个单位)

- 中等规模(51-250 单位)

- 大型(251 套或以上)

- 按车辆类型

- 轻型商用车

- 大型商用车辆

- 巴士和长途汽车

- 按地区(国家)

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 其他欧洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- TomTom NV(WEBFLEET)

- Verizon Communications Inc.(Verizon Connect)

- Bridgestone Mobility Solutions BV(WEBFLEET)

- Masternaut Ltd.(MICHELIN Connected Fleet)

- Geotab Inc.

- MiX Telematics Ltd.

- Trimble Inc.

- Samsara Inc.

- Powerfleet Inc.(包括 Fleet Complete)

- ABAX Group AS

- Teletrac Navman(Vontier Corp.)

- AT&T Inc.

- Chevin Fleet Solutions Ltd.

- Gurtam(Wialon)

- Avrios International AG

- Mapon SIA

- Fleetster GmbH

- Shiftmove GmbH

- Transpoco Telematics Ltd.

- Fleetio(RareStep Inc.)

- Teltonika Telematics UAB

- Ruptela UAB

- Motive Technologies Inc.

第七章 市场机会与未来展望

The Europe fleet management market was valued at USD 8.06 billion in 2025 and estimated to grow from USD 9.01 billion in 2026 to reach USD 15.72 billion by 2031, at a CAGR of 11.78% during the forecast period (2026-2031).

Rising regulatory pressure, the spread of connected-vehicle architectures, and intensifying last-mile logistics are together expanding addressable demand. The EU smart-tachograph Phase II rule that starts in 2025 compels real-time data transmission, turning telematics from an optional efficiency tool into a compliance requirement. E-commerce volume growth elevates urban delivery mileage, pushing operators toward granular route optimization and driver behaviour analytics. At the same time, falling cellular-IoT tariffs and eSIM adoption lower connectivity costs while 5G coverage enables high-bandwidth applications such as AI video safety monitoring. OEMs are opening application programming interfaces to monetize in-vehicle data streams, giving fleets a direct path to embedded telematics. Finally, national carbon-reduction targets and low-emission zones speed up electrification, which requires tighter energy and asset coordination.

Europe Fleet Management Market Trends and Insights

EU Smart-Tachograph Phase II Mandate Creates Compliance Imperative

The mandate enforced from June 2025 forces every commercial vehicle above 3.5 t to transmit location and driver-hours data continuously, replacing periodic data downloads with real-time oversight. Automatic fines structured between EUR 1,500 and EUR 15,000 leave operators' little choice but to install integrated telematics suites. Large German logistics firms have already completed rollouts to avoid service disruption, and suppliers report that small fleets now request multi-vehicle subscriptions rather than standalone tachographs. Because operators prefer a single pane of glass across all classes of vehicles, demand is spilling into light vans and company-car pools, lifting total platform adoption.

E-Commerce Growth Intensifies Last-Mile Delivery Optimization

Online retail penetration climbed to 13.4% of European sales in 2024, and last-mile costs swallow 41% of logistics spend for parcel operators. Light vans now cover 23% more mileage than in 2024 as consumers expect next-day delivery. Operators such as Seur cut route-related costs by 15% after introducing AI-based scheduling, demonstrating tangible return on telematics. Low-emission zones in Barcelona, Madrid, and Paris add further complexity by restricting time-window access, making real-time regulatory data essential. The Europe fleet management market, therefore benefits from converging e-commerce and environmental pressures that require constant location, traffic, and compliance feeds.

GDPR Compliance Creates Implementation Complexity

Under GDPR, employee consent for GPS tracking must be explicit and revocable, and several German court cases in 2024 confirmed that blanket monitoring infringes worker rights. For medium fleets, annual spending on legal review, data-protection officers, and software redesign totals about EUR 125,000. Multinational operators must sometimes deactivate features such as driver-cam streaming when crossing borders with stricter rules, diluting the efficiency promise of telematics and extending deployment timelines.

Other drivers and restraints analyzed in the detailed report include:

- Cellular-IoT Cost Reductions Enable Mass-Market Adoption

- OEM Telematics Platforms Monetize Connected Vehicle Data

- AI Video Telematics Capital Requirements Limit SME Adoption

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud services captured 63.55% of Europe fleet management market share in 2025 and are climbing at a 14.56% CAGR through 2031, propelled by pay-as-you-go pricing and automatic software updates. Deutsche Telekom observes that a multi-tenant architecture trims total cost of ownership by 34% relative to on-premises hosting because operators avoid server procurement and maintenance obligations. For fleet managers, elastic data storage accommodates seasonal volume swings without manual scaling. Data-sovereignty concerns confined some critical infrastructure fleets to private servers, yet cloud providers have responded with EU-based data centers that carry GDPR certification, closing the compliance gap.

Edge computing now operates as an extension of the cloud model rather than a replacement. Time-sensitive driver-assistance calculations run on in-vehicle processors, while aggregate analysis, reporting, and over-the-air updates flow through centralized hubs. This hybrid approach satisfies both latency and governance requirements, cementing cloud as the default architecture for new deployments within the Europe fleet management market.

Asset management held 26.72% of Europe fleet management market size in 2025 because every operator values location and utilization data. Safety and compliance tools, however, are advancing at a 14.34% CAGR because regulators and insurers tie monetary incentives to incident prevention. Allianz provides up to 15% premium discounts when fleets demonstrate proactive driver monitoring, accelerating adoption among high-mileage courier services. The EU Vision Zero program, which aims for zero road fatalities by 2050, positions AI-enabled fatigue detection and blind-spot alerts as pre-requisites for operating licenses in several member states. Vendors now bundle safety dashboards with tachograph files, ensuring compliance submissions are seamless and verifiable.

The Europe Fleet Management Market Report is Segmented by Deployment Type (On-Demand Cloud, On-Premises), Application (Asset Management, Information Management, and More), End-User Vertical (Transportation and Logistics, Energy and Utilities, and More), Fleet Size, Vehicle Type (Light Commercial Vehicles, Heavy Commercial Vehicles, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- TomTom N.V. (WEBFLEET)

- Verizon Communications Inc. (Verizon Connect)

- Bridgestone Mobility Solutions B.V. (WEBFLEET)

- Masternaut Ltd. (MICHELIN Connected Fleet)

- Geotab Inc.

- MiX Telematics Ltd.

- Trimble Inc.

- Samsara Inc.

- Powerfleet Inc. (incl. Fleet Complete)

- ABAX Group AS

- Teletrac Navman (Vontier Corp.)

- AT&T Inc.

- Chevin Fleet Solutions Ltd.

- Gurtam ( Wialon )

- Avrios International AG

- Mapon SIA

- Fleetster GmbH

- Shiftmove GmbH

- Transpoco Telematics Ltd.

- Fleetio ( RareStep Inc. )

- Teltonika Telematics UAB

- Ruptela UAB

- Motive Technologies Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 EU smart-tachograph Phase II mandate (2025)

- 4.2.2 E-commerce-driven LCV mileage surge

- 4.2.3 Falling cellular-IoT tariffs and eSIM adoption

- 4.2.4 OEM open-API telematics monetisation

- 4.2.5 EU ETS-2 credits for low-CO? fleets

- 4.2.6 5G C-V2X micro-platooning pilots

- 4.3 Market Restraints

- 4.3.1 GDPR and ePrivacy compliance burden

- 4.3.2 High cap-ex for AI video telematics

- 4.3.3 Patchwork low-emission city zones

- 4.3.4 Telematics-chip supply disruptions

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Type

- 5.1.1 On-Demand (Cloud)

- 5.1.2 On-Premises

- 5.2 By Application

- 5.2.1 Asset Management

- 5.2.2 Information Management

- 5.2.3 Driver Management

- 5.2.4 Safety and Compliance Management

- 5.2.5 Risk Management

- 5.2.6 Operations Management

- 5.3 By End-user Vertical

- 5.3.1 Transportation and Logistics

- 5.3.2 Energy and Utilities

- 5.3.3 Construction

- 5.3.4 Manufacturing

- 5.3.5 Other End-Users Verticals

- 5.4 By Fleet Size

- 5.4.1 Small (1-50 vehicles)

- 5.4.2 Medium (51-250)

- 5.4.3 Large (251 +)

- 5.5 By Vehicle Type

- 5.5.1 Light Commercial Vehicles

- 5.5.2 Heavy Commercial Vehicles

- 5.5.3 Bus and Coach

- 5.6 By Geography (Country)

- 5.6.1 Germany

- 5.6.2 United Kingdom

- 5.6.3 France

- 5.6.4 Spain

- 5.6.5 Italy

- 5.6.6 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level overview, market-level overview, core segments, financials, strategic information, market rank/share, products and services, recent developments)

- 6.4.1 TomTom N.V. (WEBFLEET)

- 6.4.2 Verizon Communications Inc. (Verizon Connect)

- 6.4.3 Bridgestone Mobility Solutions B.V. (WEBFLEET)

- 6.4.4 Masternaut Ltd. (MICHELIN Connected Fleet)

- 6.4.5 Geotab Inc.

- 6.4.6 MiX Telematics Ltd.

- 6.4.7 Trimble Inc.

- 6.4.8 Samsara Inc.

- 6.4.9 Powerfleet Inc. (incl. Fleet Complete)

- 6.4.10 ABAX Group AS

- 6.4.11 Teletrac Navman (Vontier Corp.)

- 6.4.12 AT&T Inc.

- 6.4.13 Chevin Fleet Solutions Ltd.

- 6.4.14 Gurtam ( Wialon )

- 6.4.15 Avrios International AG

- 6.4.16 Mapon SIA

- 6.4.17 Fleetster GmbH

- 6.4.18 Shiftmove GmbH

- 6.4.19 Transpoco Telematics Ltd.

- 6.4.20 Fleetio ( RareStep Inc. )

- 6.4.21 Teltonika Telematics UAB

- 6.4.22 Ruptela UAB

- 6.4.23 Motive Technologies Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

车队管理系统市场:依解决方案类型、车辆类型、车队规模、应用、部署模式和最终用户产业划分-2026-2032年全球市场预测

车队管理系统市场:依解决方案类型、车辆类型、车队规模、应用、部署模式和最终用户产业划分-2026-2032年全球市场预测 全球汽车车队市场规模、份额、趋势和成长分析报告(2026-2034)车队管理市场:2026-2032年全球市场预测(依服务类型、实施方法、连接方式、车队类型、部署模式、车队规模、应用领域、最终用户产业、所有权模式和定价模式)

全球汽车车队市场规模、份额、趋势和成长分析报告(2026-2034)车队管理市场:2026-2032年全球市场预测(依服务类型、实施方法、连接方式、车队类型、部署模式、车队规模、应用领域、最终用户产业、所有权模式和定价模式) 2026年全球车队管理市场报告

2026年全球车队管理市场报告 东南亚车队管理市场报告 - 第二版

东南亚车队管理市场报告 - 第二版 车队行车记录器市场规模、份额和成长分析(按产品类型、车辆类型、功能、最终用户和地区划分)-2026-2033年产业预测

车队行车记录器市场规模、份额和成长分析(按产品类型、车辆类型、功能、最终用户和地区划分)-2026-2033年产业预测 车队管理市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、设备、部署类型及最终用户划分2026年全球电动车队管理市场报告

车队管理市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、设备、部署类型及最终用户划分2026年全球电动车队管理市场报告 车队管理市场-全球产业规模、份额、趋势、机会及预测(按车辆类型、组件、通讯技术、产业垂直领域、地区及竞争格局划分,2021-2031年)车队管理能力和解决方案市场:全球预测(2026-2032 年),按解决方案类型、部署模式、车队类型、车辆类型和最终用户行业划分

车队管理市场-全球产业规模、份额、趋势、机会及预测(按车辆类型、组件、通讯技术、产业垂直领域、地区及竞争格局划分,2021-2031年)车队管理能力和解决方案市场:全球预测(2026-2032 年),按解决方案类型、部署模式、车队类型、车辆类型和最终用户行业划分