|

市场调查报告书

商品编码

1910944

雷射打标:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Laser Marking - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

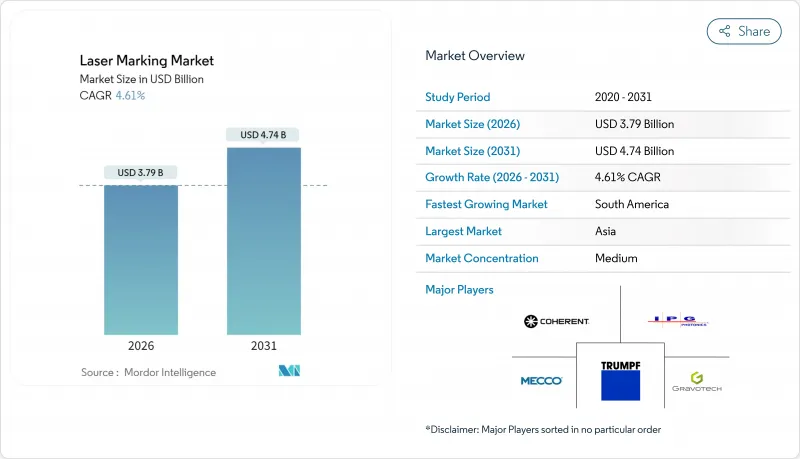

预计雷射打标市场将从 2025 年的 36.2 亿美元成长到 2026 年的 37.9 亿美元,到 2031 年将达到 47.4 亿美元,2026 年至 2031 年的复合年增长率为 4.61%。

全球法规强制要求对设备进行永久性标识,电动车电池生产需求不断增长,以及微型电子产品和永续封装对精度要求日益提高,这些因素共同推动了市场成长。由于本土供应商的准入门槛较低,亚洲在装机量方面继续占据主导地位,而以服务主导的经营模式在北美和欧洲正蓬勃发展。来自中国光纤雷射製造商的价格压力正在挤压硬体利润空间,但软体和预测性维护服务仍然盈利。航太复合材料、珠宝饰品印记和工业自动化等领域的新应用正在扩大基本客群,而高昂的资本投入则限制一些小规模製造商的发展。

全球雷射打标市场趋势与洞察

医疗设备强制性UDI(唯一设备识别码)和可追溯性法规推动了永久性标记的普及。

美国FDA和欧盟医疗设备法规(MDR)制定的严格的医疗设备标识(UDI)框架,使得永久性、高对比的器材编码成为一项法律要求。医院需要反覆对器械进行消毒,因此标记必须能够承受磨损、化学物质和高温。光纤和紫外线雷射系统能够满足钛植入、聚合物导管和陶瓷组件的这些耐久性要求。与製造执行系统(MES)的直接连接也简化了合规性审核。药品序列化法规正在推动需求成长,进而促进无需耗材即可列印复杂二维矩阵的雷射系统的整体生产线整合。能够将标记硬体和检验软体结合的供应商可以缩短您的认证週期并降低召回风险。

电动车电池产量快速成长,推动了对非接触式标记的需求。

目前,超级工厂会在每个电芯、模组和电池组上标记一个唯一的代码,用于召回和回收管理。雷射技术能够以生产线速度完成这种识别,且无需接触敏感的机壳,从而避免颗粒污染和机械应力。光纤雷射用于标记铝製机壳,而紫外线光束则用于将代码印刻在聚合物隔膜和柔性电路上。中国、韩国和美国对能够每小时标记数千件产品的高速视觉引导设备的需求正在迅速增长。电池生产线整合商正越来越多地将可追溯性模组与焊接和检测站整合在一起,以实现端到端的流程可视性。

高额资本投资是中小企业进入新兴市场的障碍。

整合视觉和物联网连接的工业级系统通常售价超过15万美元,这超出了拉丁美洲和非洲小型製造商的现金流能力。汇率波动推高了进口成本,而当地的融资利率又增加了额外的压力。携带式低成本光纤设备虽然入门价格较低,但缺乏汽车和医疗行业所需的精度和运作保证。租赁和按收费付费的合约正变得越来越普遍,但在第三方服务网路成熟之前,预计其普及速度将较为缓慢。

细分市场分析

到2025年,光纤雷射将占雷射打标市场收入的61.95%,这主要得益于其可靠性、高能效以及高速标记大多数金属的能力。汽车动力传动系统部件、外科手术器械和航太紧固件等行业都依赖光纤光束进行深而清晰的标记,这些标记能够承受恶劣环境的考验。随着亚洲和欧洲工业4.0相关维修的加速,光纤雷射打标市场预计将稳定成长。紫外线雷射目前仅占收入的一小部分,但由于对柔性电路基板和玻璃盖等精细基材上的微标记的需求不断增长,预计到2031年,紫外线雷射器的年复合增长率将达到6.6%。随着家用电子电器产量比率的提高,工厂正在改装紫外线加工能力,半导体晶圆厂也开始指定使用355nm光源进行晶圆级标识。

绿光雷射和超快脉衝解决方案在硅晶圆加工和玻璃中介层钻孔领域占据着独特的地位。儘管连贯、通快公司和IPG光电不断改进光束特性,但中国供应商已经缩小了技术差距,并获得了价格优势。如今,视觉引导对准和在线连续检验软体整合已成为供应商之间的差异化因素,而不是光束功率本身。

受汽车和航太产业对深度防篡改标记的需求推动,雕刻过程预计到2025年将占市场收入的38.15%。光纤系统能够快速去除材料,确保高对比度和耐久性。同时,除尘和视觉检验模组可维持生产效率。退火工艺是成长最快的工艺,复合年增长率达6.85%。医疗设备製造商青睐氧化层的颜色变化,这种变化能够保持表面光滑无菌。不銹钢工具和植入物零件对完美表面处理的需求将推动退火雷射打标市场份额的成长。

蚀刻和发泡仍然是消费品和包装生产线的主要工艺,尤其适用于浅层标记。碳化仍然是有机材料(特别是瓦楞纸板和工程木材)的主要标记方法。随着工厂寻求更灵活的生产线,能够在单一循环中切换雕刻、退火和蚀刻的多进程头需求量很大。

区域分析

预计到2025年,亚洲将占全球收入的46.05%,这主要得益于中国电子和汽车产业丛集的蓬勃发展,以及政府对智慧工厂的大规模支持。汉斯雷射和HGTECH等国内供应商提供价格极具竞争力的光纤设备,扩大了区域加工商和一级零件製造商的市场准入。日本和韩国专注于半导体和电动车电池模组等细分精密加工领域,而印度的认证和药品编码政策则正在开拓新的中端市场。随着製造商寻求可预测的成本和合规性,服务合约的增加正在创造持续的收入来源。

北美市场需求成熟且注重质量,主要集中在航太、医疗设备和汽车VIN码编码领域。监管和保固风险促使企业采用经过检验的流程监控的高阶系统。加拿大企业正在利用雷射编码技术开发采矿设备,而墨西哥汽车出口工厂则透过在线连续标记进行现代化改造,以满足美国车辆平台可追溯性标准。由于运作合约弥补了劳动力短缺,服务渗透率很高。

欧洲正努力在实现永续性目标的同时,兼顾严格的安全法规。德国动力传动系统和机械製造商正在采用深雕刻技术,而法国航太工厂则采用超短脉衝光束来製造轻质复合材料。英国和北欧地区的品牌选择雷射编码,以减少油墨的使用并降低碳排放。随着GS1数位连结标准的持续普及,欧洲包装生产线雷射打标市场正稳步扩张。东欧地区也受惠于近岸外包模式,波兰和捷克共和国都新增了相关设备。

南美洲将成为成长最快的地区,到2031年复合年增长率将达到5.88%,主要得益于巴西汽车出口和智利矿业自动化。高昂的资本成本和熟练工人短缺正在减缓小规模经济体采用数位化技术的速度,但租赁模式正开始解决这些障碍。随着宏观经济稳定性的改善,阿根廷和哥伦比亚政府对数位製造业的支持预计将加速其普及。中东和非洲地区呈现温和成长,海湾国家油气资产的发现和政府支持的工业园区正在形成需求丛集。然而,政治风险限制着该地区的长期发展。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 医疗设备强制UDI(唯一设备识别)和可追溯性法规(美国、欧盟、中国)

- 电动车电池产量快速成长,带动了对非接触式标记的需求增加。

- 小型化家用电子电器推动亚洲微行销

- 转型为永续包装?欧洲从喷墨列印转向雷射编码

- 北美汽车工厂工业4.0的在线连续集成

- 印度推动珠宝饰品鑑定政策数位化

- 市场限制

- 新兴市场中小企业的大资本投资(超过15万美元)

- 航太复合材料认证延误(对热影响区 (HAZ) 的担忧)

- 拉丁美洲工厂熟练工人短缺

- 来自低成本中国光纤雷射供应商的利润压力

- 产业生态系分析

- 监理与技术展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章 市场规模与成长预测

- 依雷射类型

- 光纤雷射

- 二氧化碳雷射

- 固体(Nd:YAG、Nd:YVO4)

- 紫外线雷射

- 绿光雷射

- 其他(二极体、YAG、混合式)

- 透过标记过程

- 退火

- 蚀刻

- 雕塑

- 发泡

- 碳化

- 报价

- 硬体

- 独立系统

- 整合/在线连续系统

- 软体

- 服务

- 硬体

- 按最终用户行业划分

- 汽车和航太

- 电子和半导体

- 医疗设备和医疗保健

- 食品/饮料包装

- 工业机械和工具机

- 珠宝饰品和奢侈品

- 其他产业(石油和天然气、国防等)

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 北欧国家

- 其他欧洲地区

- 南美洲

- 巴西

- 其他南美洲

- 亚太地区

- 中国

- 日本

- 印度

- 东南亚

- 亚太其他地区

- 中东和非洲

- 中东

- GCC

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 其他非洲地区

- 中东

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Coherent Corp.

- IPG Photonics Corp.

- TRUMPF Group

- Han's Laser Technology Co. Ltd.

- Keyence Corp.

- Novanta Inc.(FOBA)

- Videojet Technologies Inc.

- Gravotech Group

- Mecco Partners LLC

- Epilog Laser Inc.

- Trotec Laser GmbH

- LaserStar Technologies Corp.

- SIC Marking Group

- Rofin-Sinar UK Ltd.

- Panasonic Connect Co. Ltd.

- Omron Corporation

- Domino Printing Sciences plc

- SATO Holdings Corp.

- TYKMA Electrox Inc.

- Nichia Corp.

- Control Laser Corp.

第七章 市场机会与未来展望

The laser marking market is expected to grow from USD 3.62 billion in 2025 to USD 3.79 billion in 2026 and is forecast to reach USD 4.74 billion by 2031 at 4.61% CAGR over 2026-2031.

Growth is anchored in global regulations that require permanent device identification, expanding demand from electric vehicle battery production, and rising precision needs across miniaturised electronics and sustainable packaging. Asia continues to dominate installations as domestic suppliers cut entry costs, while service-led business models gain traction in North America and Europe. Pricing pressure from Chinese fiber-laser producers compresses hardware margins, but software and predictive-maintenance services preserve profitability. New use-cases in aerospace composites, jewellery hallmarking, and industrial automation widen the customer base even as high capital requirements constrain some small manufacturers.

Global Laser Marking Market Trends and Insights

Mandatory UDI and Traceability Regulations in Medical Devices Drive Permanent Marking Adoption

Stringent UDI frameworks created by the US FDA and the EU MDR make permanent, high-contrast device codes a legal necessity. Hospitals sterilise instruments repeatedly, so marks must resist abrasion, chemicals, and heat. Fiber and UV systems meet these durability needs on titanium implants, polymer catheters, and ceramic components, while direct connectivity to manufacturing execution systems simplifies compliance audits. Pharmaceutical serialization rules add volume, increasing overall line-integration demand for laser systems that print intricate 2D matrices without consumables. Suppliers that couple marking hardware with validation software shorten customer certification cycles and cut recall exposurre.

Surge in EV Battery Production Accelerates Contact-less Marking Demand

Gigafactories now stamp unique codes on every cell, module, and pack to manage recalls and recycling. Laser technology performs this identification at line speed without touching sensitive housings, avoiding particulate contamination and mechanical stress. Fiber lasers mark aluminum casings, while UV beams code polymer separators and flexible circuits. Demand for high-speed, vision-guided units capable of thousands of marks per hour is escalating across China, Korea, and the United States. Battery line integrators increasingly package traceability modules alongside welding and inspection stations for end-to-end process visibility.

High CAPEX Requirements Constrain SME Adoption in Emerging Markets

Industrial-grade systems with integrated vision and IoT connectivity often list above USD 150,000, exceeding the cashflow capacity of smaller Latin American and African manufacturers. Currency volatility inflates import costs, while local financing rates add further burden. Portable low-cost fiber units reduce entry price yet lack the precision and uptime guarantees demanded by automotive or medical lines. Leasing and pay-per-mark contracts are gaining popularity, but adoption remains gradual until third-party service networks mature

Other drivers and restraints analyzed in the detailed report include:

- Miniaturised Consumer Electronics Drive Micro-marking Precision Requirements

- Sustainable Packaging Shift Favors Laser Coding Over Inkjet Systems

- Qualification Delays for Aerospace Composites Create Validation Challenges

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fiber lasers held 61.95% of revenue in 2025, reflecting their reliability, high wall-plug efficiency, and ability to mark most metals at high speed. Automotive powertrain parts, surgical instruments, and aerospace fasteners rely on fiber beams for deep, legible engravings that survive harsh service. The laser marking market size for fiber systems is projected to expand steadily alongside Industry 4.0 retrofits in Asia and Europe. UV lasers, though smaller in revenue today, are advancing at a 6.6% CAGR through 2031 thanks to demand for micro-marking on sensitive substrates such as flexible circuits and glass covers. Rising yields in consumer electronics push factories to retrofit UV capabilities, while semiconductor fabs specify 355 nm sources for wafer-level ID.

Green and ultrashort-pulse solutions occupy niche roles in silicon wafer processing and glass interposer drilling. Coherent, TRUMPF, and IPG Photonics continue to refine beam characteristics, but Chinese vendors narrow the technology gap and undercut on price. Integration of vision-guided alignment and inline verification software now differentiates suppliers more than raw beam power.

Engraving accounted for 38.15% of market revenue in 2025, driven by automotive and aerospace requirements for deep, tamper-proof marks. Fiber systems remove material quickly, ensuring high contrast and durability, while dust extraction and vision verification modules sustain throughput. Annealing is the fastest-expanding process at a 6.85% CAGR because medical device makers prefer oxide-layer color changes that leave surfaces smooth and sterile. The laser marking market share for annealing rises whenever stainless tools or implantables demand pristine finishes.

Etching and foaming continue to support consumer goods and packaging lines where shallow marks suffice. Carbonisation remains a go-to method for organic materials, especially cardboard and engineered wood. Multi-process heads capable of switching between engraving, annealing, and etching in a single cycle gain popularity as factories seek flexible cells.

The Laser Marking Market Report is Segmented by Laser Type (Fiber Laser, CO2 Laser, Solid-State, UV Laser, and More), Marking Process (Annealing, Etching, Engraving, Foaming, and Carbonisation), Offering (Hardware, Software, and Services), End-User Industry (Automotive and Aerospace, Electronics and Semiconductors, Medical Devices and Healthcare, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia generated 46.05% of global revenue in 2025, anchored by China's electronics and automotive clusters and supported by large state incentives for smart factories. Domestic suppliers such as Han's Laser and HGTECH sell competitively priced fiber units, widening access for regional job shops and tier-one components firms. Japan and South Korea pursue niche precision applications in semiconductors and EV battery modules, while India's hallmarking and pharmaceutical coding policies open new mid-tier opportunities. Rising service contracts create recurring income streams as manufacturers seek predictable costs and regulatory compliance.

North America's demand is mature and quality-driven, centred on aerospace, medical devices, and automotive VIN coding. Regulations and warranty risk drive adoption of high-end systems with validated process monitoring. Canadian firms leverage laser coding for mining equipment while Mexico's automotive export plants modernise with inline marking to satisfy traceability standards for US vehicle platforms. Service penetration is high as uptime contracts offset labour shortages.

Europe balances sustainability objectives with strict safety regulations. German powertrain and machinery builders rely on deep engraving, while French aerospace plants adopt ultrashort-pulse beams for lightweight composites. Brands across the United Kingdom and the Nordic region choose laser coding to eliminate ink and lower carbon footprints. The laser marking market size attributed to European packaging lines grows steadily as GS1 Digital Link rollouts progress. Eastern Europe benefits from near-shoring, prompting new installations in Poland and the Czech Republic.

South America is the fastest-growing region at a 5.88% CAGR to 2031, led by Brazilian automotive exports and Chilean mining automation. High capital costs and a shortage of trained technicians slow the pace in smaller economies, yet leasing models are starting to remove barriers. Government incentives for digital manufacturing in Argentina and Colombia could accelerate adoption once macroeconomic stability improves. The Middle East and Africa register moderate growth, with oil and gas asset identification and government-backed industrial parks in the Gulf creating demand clusters, although political risk tempers longer-term forecasts.

- Coherent Corp.

- IPG Photonics Corp.

- TRUMPF Group

- Han's Laser Technology Co. Ltd.

- Keyence Corp.

- Novanta Inc. (FOBA)

- Videojet Technologies Inc.

- Gravotech Group

- Mecco Partners LLC

- Epilog Laser Inc.

- Trotec Laser GmbH

- LaserStar Technologies Corp.

- SIC Marking Group

- Rofin-Sinar UK Ltd.

- Panasonic Connect Co. Ltd.

- Omron Corporation

- Domino Printing Sciences plc

- SATO Holdings Corp.

- TYKMA Electrox Inc.

- Nichia Corp.

- Control Laser Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mandatory UDI and traceability regulations in medical devices (US, EU, CN)

- 4.2.2 Surge in EV battery production contact-less marking demand

- 4.2.3 Miniaturised consumer electronics driving micro-marking in Asia

- 4.2.4 Sustainable packaging shift ? laser coding over inkjet in Europe

- 4.2.5 Industry 4.0 inline integration in North-American automotive plants

- 4.2.6 Jewellery hallmarking digitisation policy boost in India

- 4.3 Market Restraints

- 4.3.1 High CAPEX (Above USD 150 k) for SMEs in emerging markets

- 4.3.2 Qualification delay for aerospace composites (HAZ concerns)

- 4.3.3 Skilled-operator shortage in Latin-American factories

- 4.3.4 Margin pressure from low-cost Chinese fiber-laser suppliers

- 4.4 Industry Ecosystem Analysis

- 4.5 Regulatory and Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Degree of Competition

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Laser Type

- 5.1.1 Fiber Laser

- 5.1.2 CO? Laser

- 5.1.3 Solid-State (Nd:YAG, Nd:YVO?)

- 5.1.4 UV Laser

- 5.1.5 Green Laser

- 5.1.6 Others (Diode, YB:YAG, Hybrid)

- 5.2 By Marking Process

- 5.2.1 Annealing

- 5.2.2 Etching

- 5.2.3 Engraving

- 5.2.4 Foaming

- 5.2.5 Carbonisation

- 5.3 By Offering

- 5.3.1 Hardware

- 5.3.1.1 Stand-Alone Systems

- 5.3.1.2 Integrated/In-line Systems

- 5.3.2 Software

- 5.3.3 Services

- 5.3.1 Hardware

- 5.4 By End-User Industry

- 5.4.1 Automotive and Aerospace

- 5.4.2 Electronics and Semiconductors

- 5.4.3 Medical Devices and Healthcare

- 5.4.4 Food and Beverage Packaging

- 5.4.5 Industrial Machinery and Machine Tools

- 5.4.6 Jewellery and Luxury Goods

- 5.4.7 Other Industries (Oil and Gas, Defence, etc.)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Nordics

- 5.5.2.5 Rest of Europe

- 5.5.3 South America

- 5.5.3.1 Brazil

- 5.5.3.2 Rest of South America

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South-East Asia

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Gulf Cooperation Council Countries

- 5.5.5.1.2 Turkey

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Coherent Corp.

- 6.4.2 IPG Photonics Corp.

- 6.4.3 TRUMPF Group

- 6.4.4 Han's Laser Technology Co. Ltd.

- 6.4.5 Keyence Corp.

- 6.4.6 Novanta Inc. (FOBA)

- 6.4.7 Videojet Technologies Inc.

- 6.4.8 Gravotech Group

- 6.4.9 Mecco Partners LLC

- 6.4.10 Epilog Laser Inc.

- 6.4.11 Trotec Laser GmbH

- 6.4.12 LaserStar Technologies Corp.

- 6.4.13 SIC Marking Group

- 6.4.14 Rofin-Sinar UK Ltd.

- 6.4.15 Panasonic Connect Co. Ltd.

- 6.4.16 Omron Corporation

- 6.4.17 Domino Printing Sciences plc

- 6.4.18 SATO Holdings Corp.

- 6.4.19 TYKMA Electrox Inc.

- 6.4.20 Nichia Corp.

- 6.4.21 Control Laser Corp.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

雷射打标市场:2026-2032年全球市场预测(按雷射类型、材料打标、技术、打标类型、产品类型、光学输入、应用和最终用途行业划分)可携式打标机市场:按技术、产品类型、连接方式、应用和最终用户划分,全球预测(2026-2032)

雷射打标市场:2026-2032年全球市场预测(按雷射类型、材料打标、技术、打标类型、产品类型、光学输入、应用和最终用途行业划分)可携式打标机市场:按技术、产品类型、连接方式、应用和最终用户划分,全球预测(2026-2032) 全球雷射打标机市场:依雷射类型、产品系列、打标类型、最终用途产业、国家及地区划分-产业分析、市场规模、份额及预测(2025-2032年)

全球雷射打标机市场:依雷射类型、产品系列、打标类型、最终用途产业、国家及地区划分-产业分析、市场规模、份额及预测(2025-2032年) 全球雷射打标设备市场规模、份额、趋势及成长分析报告(2026-2034年)

全球雷射打标设备市场规模、份额、趋势及成长分析报告(2026-2034年) 2026年全球点阵打标机市场报告2026年全球雷射打标机市场报告雷射打标机市场规模、占有率、成长及全球产业分析:依类型、应用和地区划分的洞察与预测(2026-2034)全球一体化桌上型雷射打标机市场(按雷射类型、终端用户产业、功率输出、功能和应用划分)-2026-2032年预测

2026年全球点阵打标机市场报告2026年全球雷射打标机市场报告雷射打标机市场规模、占有率、成长及全球产业分析:依类型、应用和地区划分的洞察与预测(2026-2034)全球一体化桌上型雷射打标机市场(按雷射类型、终端用户产业、功率输出、功能和应用划分)-2026-2032年预测 雷射打标机市场规模、份额、成长分析(按类型、机器类型、产品类型、材料、应用、最终用途和地区划分)-2026-2033年产业预测

雷射打标机市场规模、份额、成长分析(按类型、机器类型、产品类型、材料、应用、最终用途和地区划分)-2026-2033年产业预测 雷射打标机市场机会、成长动力、产业趋势分析及2025-2034年预测

雷射打标机市场机会、成长动力、产业趋势分析及2025-2034年预测