|

市场调查报告书

商品编码

1911830

欧洲医药塑胶包装:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Europe Pharmaceutical Plastic Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

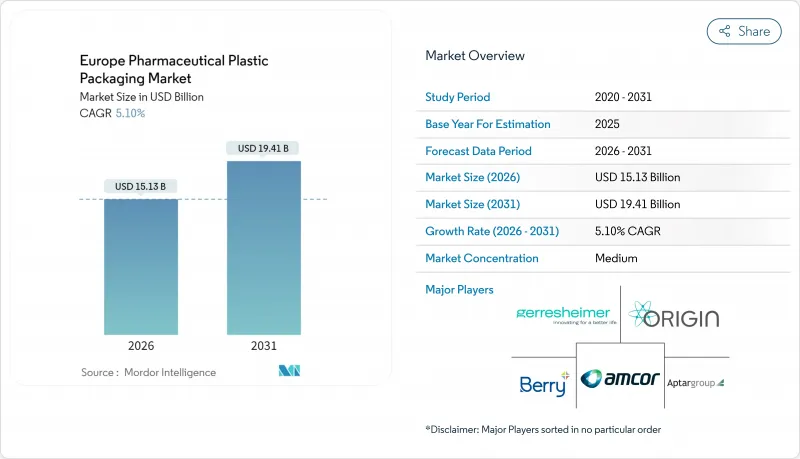

2025年欧洲医药塑胶包装市场价值为144亿美元,预计到2031年将达到194.1亿美元,高于2026年的151.3亿美元。

预计在预测期(2026-2031 年)内,复合年增长率将达到 5.10%。

推动成长的关键因素包括永续性的迫切需求、生物製药的广泛应用以及家庭护理的扩张,这些因素都对阻隔性能、可回收性和以用户为中心的设计提出了更为严格的要求。领先的供应商正在扩大再生材料产品线和RFID技术产品,以满足循环经济目标和医院自动化专案的需求。同时,树脂成本的波动和更严格的萃取物法规正在挤压利润空间,促使企业进行原材料避险、供应商多元化以及选择性併购,以维持规模优势。由于现有企业扩大垂直整合,而专业公司则在智慧和生物基解决方案的细分市场占有一席之地,竞争依然保持适度。这正在重塑欧洲医药塑胶包装市场的定价和合作模式。

欧洲医药塑胶包装市场趋势与洞察

对儿童安全瓶盖和老年人友善包装的需求日益增长

受人口老化和日益严格的儿童安全法规的推动,包装投资正转向兼具触感操作和经认证的儿童安全锁的瓶盖。欧洲加工商为每个符合人体工学的新型瓶盖平台投资200万至400万欧元,这项措施已促使以患者为中心的包装系统在2024年之前采用率提高18%。 Nemera的低扭力瓶盖可将开启力降低30%,同时超越ISO 8317标准,展现了易用性和安全性之间的平衡。欧洲药品管理局(EMA)2024年发布的指南也为监管提供了支持,该指南建议为慢性病药物采用用户友好型包装。早期采用者表示,虽然初始成本增加了15%至20%,特别是对于需要高精度模具来支撑复杂锁定机制的聚丙烯瓶盖而言,但更高的定价和品牌忠诚度的提升弥补了这一成本增加。

需要先进肠外塑胶的生物製药的激增

预计到2024年,欧洲生物製药产量将增加23%,其中德国和瑞士的工厂将扩大单株抗体的生产规模。这些高价值分子需要超低萃取物和无玻璃抗破损性能,加速了对环烯烃共聚物和聚合物的需求。这些材料具有化学惰性和透明度,但成本是聚丙烯的三到四倍。肖特製药计画投资1.5亿欧元扩建管瓶,凸显了供应商对特种聚合物生产能力的重视。生物製药包装的成长率几乎是欧洲整体製药塑胶包装市场的两倍,这正在重塑材料组合、认证时间表和供应商整合格局。

PP和PET树脂价格波动

石化原料供应中断和能源价格波动导致2024年聚丙烯和PET价格上涨15%至20%。BASF等生产商已转向季度定价,将价格波动风险转移给加工商,而加工商通常与製药公司签订多年供应合约。规模较小、避险能力较弱的公司面临压力,引发了一波整合浪潮。同时,大型企业集团正透过多元化供应来源和投资自身回收来减轻价格波动的影响。对于许多中型加工商而言,30%至40%的原材料成本受季度调整条款的约束,这削弱了欧洲医药塑胶包装市场的整体可预测性。

细分市场分析

到2025年,聚丙烯(PP)在欧洲医药塑胶包装市场仍将占据35.20%的份额,这主要得益于其成本效益、耐化学腐蚀性和广泛的监管认可。用于医药领域的PP年消费量将超过18万吨,涵盖瓶盖、泡壳包装、注射器等。然而,欧洲医药塑胶包装市场正逐渐转向高高密度聚苯乙烯(HDPE),其复合年增长率(CAGR)为5.74%。 HDPE优异的防潮和防氧阻隔性满足生物製药的稳定性要求,同时在《塑胶回收再利用条例》(PPWR)下也具有更高的可回收性。

向永续性的转型正在推动对医用级再生PET(rPET)的需求,并促进生物基等级产品的试验。 Gerresheimer已开始商业化生产符合製药纯度标准的再生PET输液瓶。儘管价格溢价高达300-400%,但特种聚合物(COC、COP和PLA混合物)在註射配方中逐渐被接受,因为超低萃取物是此类配方的关键。 Schott Pharma扩大COC生产规模,也印证了市场对这些特殊树脂日益增长的需求。聚丙烯供应商正透过试验使用消费后塑胶原料来应对这一需求,但他们必须克服与气味、颜色和可追溯性相关的技术挑战,以保持主导地位。

欧洲医药塑胶包装市场按原料(聚丙烯、聚对苯二甲酸乙二醇酯、低密度聚乙烯、高密度聚苯乙烯及其他)、产品类型(固态容器、液体和静脉注射瓶、滴鼻剂瓶、口腔清洁用品包、小袋/小袋、管瓶/小瓶及其他)和国家/地区进行细分。市场预测以以金额为准。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 对儿童安全包装和老年人友善包装的需求日益增长

- 需要先进肠外塑胶的生物製药的激增

- 欧盟循环经济规则加速可回收塑胶的开发

- 电子商务药品分销的扩张将推动对二级包装的保护力度加大。

- 家庭注射疗法需要使用小型预填充式注射器。

- 用于医院自动化的机器人辅助RFID泡壳包装

- 市场限制

- PP和PET树脂价格波动

- 更严格的可萃取物和可浸出物监管标准

- 注射剂中玻璃和铝的替代品

- 供不应求

- 供应链分析

- 监管环境

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

- 产业价值链分析

- 宏观经济趋势的影响

第五章 市场规模与成长预测

- 按原料

- 聚丙烯(PP)

- 聚对苯二甲酸乙二醇酯(PET)

- 低密度聚乙烯(LDPE)

- 高密度聚苯乙烯(HDPE)

- 其他(COP、COC、不含PVC的混合物、生物聚合物)

- 依产品类型

- 固态容器

- 液体/滴管瓶

- 鼻腔喷雾瓶

- 口腔清洁用品套装

- 小袋/小袋

- 管瓶和安瓿(聚合物)

- 墨水匣

- 预填充式注射器

- 瓶盖和封口

- 其他(单剂量药片、吸入器药罐)

- 按国家/地区

- 英国

- 德国

- 法国

- 西班牙

- 义大利

- 比利时

- 瑞典

- 其他欧洲地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Gerresheimer AG

- Amcor PLC

- Berry Global Group Inc.

- AptarGroup Inc.

- Origin Pharma Packaging

- Pretium Packaging

- Klckner Pentaplast

- Comar

- Gil Plastic Products Ltd

- Drug Plastics Group

- West Pharmaceutical Services Inc.

- Nemera

- Bormioli Pharma

- Alpla Group

- Sanner GmbH

- Tekni-Plex

- Weener Plastics

- Jabil Healthcare(Nypro)

- Stevanato Group(EZ-fill polymer vials)

- Raumedic AG

第七章 市场机会与未来展望

The Europe pharmaceutical plastic packaging market was valued at USD 14.40 billion in 2025 and estimated to grow from USD 15.13 billion in 2026 to reach USD 19.41 billion by 2031, at a CAGR of 5.10% during the forecast period (2026-2031).

Growth pivots on sustainability mandates, biologics proliferation, and home-based therapy expansion, each tightening performance requirements for barrier properties, recyclability, and user-centric design. Leading suppliers are scaling recycled-content lines and RFID-ready formats to satisfy circular-economy goals and hospital automation programs. Meanwhile resin cost swings and stricter extractables protocols are compressing margins, prompting raw-material hedging, supplier diversification, and selective mergers to preserve scale advantages. Competitive intensity remains moderate as incumbents extend vertical integration while specialists seize niches in smart and bio-based solutions, reshaping pricing and collaboration models across the Europe pharmaceutical plastic packaging market.

Europe Pharmaceutical Plastic Packaging Market Trends and Insights

Rising Demand for Child-Resistant and Senior-Friendly Packs

An ageing population and tighter pediatric-safety mandates are steering packaging investments toward closures that combine tactile ease with certified child resistance. European converters spend EUR 2-4 million on every new ergonomic closure platform, a commitment that lifted patient-centric system launches by 18% in 2024. Nemera's torque-reducing closure lowers opening force 30% while exceeding ISO 8317, illustrating how usability and safety can coexist.Regulatory endorsement came via the European Medicines Agency's 2024 guidelines stressing user-friendly packaging for chronic therapies. Early adopters report premium pricing and brand-loyalty gains that offset the initial 15-20% cost uplift, especially for polypropylene caps whose mold precision supports intricate locking mechanisms.

Surge in Biologics Needing Advanced Parenteral Plastics

Biologic drug output in Europe jumped 23% in 2024, with German and Swiss plants ramping monoclonal antibody runs. These high-value molecules require ultra-low extractables and glass-free break-resistance, accelerating demand for cyclic olefin copolymers and cyclic olefin polymers that cost 3-4 times polypropylene yet deliver chemical inertness and clarity. SCHOTT Pharma's EUR 150 million vial-expansion plan underscores supplier commitment to specialized polymer capacity. Biologics-ready packaging is growing nearly twice as fast as the overall Europe pharmaceutical plastic packaging market, reshaping material mix, qualification timelines, and supplier consolidation patterns.

Volatile PP and PET Resin Prices

Petrochemical feedstock disruptions and energy-price swings pushed polypropylene and PET up 15-20% during 2024. Producers such as BASF now quote quarterly, shifting volatility risk to converters who often lock in multi-year supply deals with drugmakers. Smaller firms lacking hedging capacity face squeezes that have triggered consolidation waves, while larger groups diversify supply and invest in in-house recycling to temper pricing shocks. Quarterly adjustment clauses already cover 30-40% of raw-material spend for many mid-tier converters, eroding predictability across the Europe pharmaceutical plastic packaging market.

Other drivers and restraints analyzed in the detailed report include:

- EU Circular-Economy Rules Accelerating Recyclable Plastics

- E-Commerce Pharma Boosting Protective Secondary Packaging

- Stricter Extractables / Leachables Limits

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polypropylene retained 35.20% Europe pharmaceutical plastic packaging market share in 2025, supported by cost-efficiency, chemical resistance, and widespread regulatory familiarity. Annual pharmaceutical PP consumption exceeds 180,000 tons, covering closures, blisters, and syringes. However, the Europe pharmaceutical plastic packaging market size is tilting toward high-density polyethylene, advancing at a 5.74% CAGR as its superior moisture and oxygen barrier meets biologics stability requirements while presenting stronger recyclability credentials under PPWR.

Sustainability shifts also elevate medical-grade rPET and spur trials of bio-based grades. Gerresheimer has begun commercial runs of recycled PET dropper bottles that satisfy pharma purity thresholds. Niche polymers-COC, COP, PLA blends-command premiums of 300-400% but win specifications for parenterals where ultra-low extractables are mandatory. SCHOTT Pharma's COC expansion underscores rising demand for these specialty resins. Polypropylene suppliers are responding by piloting post-consumer content streams, yet must overcome technical hurdles in odor, color, and traceability to retain leadership within the Europe pharmaceutical plastic packaging market.

Europe Pharmaceutical Plastic Packaging Market is Segmented by Raw Material (Polypropylene, Polyethylene Terephthalate, Low-Density Polyethylene, High-Density Polyethylene, Others), Product Type (Solid Containers, Liquid and Dropper Bottles, Nasal Spray Bottles, Oral-Care Packs, Pouches/Sachets, Vials and Ampoules, and More), and by Country. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Gerresheimer AG

- Amcor PLC

- Berry Global Group Inc.

- AptarGroup Inc.

- Origin Pharma Packaging

- Pretium Packaging

- Klckner Pentaplast

- Comar

- Gil Plastic Products Ltd

- Drug Plastics Group

- West Pharmaceutical Services Inc.

- Nemera

- Bormioli Pharma

- Alpla Group

- Sanner GmbH

- Tekni-Plex

- Weener Plastics

- Jabil Healthcare (Nypro)

- Stevanato Group (EZ-fill polymer vials)

- Raumedic AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for child-resistant and senior-friendly packs

- 4.2.2 Surge in biologics needing advanced parenteral plastics

- 4.2.3 EU circular-economy rules accelerating recyclable plastics

- 4.2.4 E-commerce pharma boosting protective secondary packaging

- 4.2.5 Home-injection therapies driving small PP pre-filled syringes

- 4.2.6 Robotics-ready RFID blister packs for hospital automation

- 4.3 Market Restraints

- 4.3.1 Volatile PP and PET resin prices

- 4.3.2 Stricter extractables / leachables limits

- 4.3.3 Glass and aluminum substitution in injectables

- 4.3.4 Short supply of medical-grade recycled resin

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Degree of Competition

- 4.8 Industry Value-Chain Analysis

- 4.9 Impact of Macroeconomic Trends

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Raw Material

- 5.1.1 Polypropylene (PP)

- 5.1.2 Polyethylene Terephthalate (PET)

- 5.1.3 Low-Density Polyethylene (LDPE)

- 5.1.4 High-Density Polyethylene (HDPE)

- 5.1.5 Others (COP, COC, PVC-free blends, bio-polymers)

- 5.2 By Product Type

- 5.2.1 Solid Containers

- 5.2.2 Liquid and Dropper Bottles

- 5.2.3 Nasal Spray Bottles

- 5.2.4 Oral-care Packs

- 5.2.5 Pouches / Sachets

- 5.2.6 Vials and Ampoules (polymer)

- 5.2.7 Cartridges

- 5.2.8 Prefilled Syringes

- 5.2.9 Caps and Closures

- 5.2.10 Others (unit-dose strips, inhaler canisters)

- 5.3 By Country

- 5.3.1 United Kingdom

- 5.3.2 Germany

- 5.3.3 France

- 5.3.4 Spain

- 5.3.5 Italy

- 5.3.6 Belgium

- 5.3.7 Sweden

- 5.3.8 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Gerresheimer AG

- 6.4.2 Amcor PLC

- 6.4.3 Berry Global Group Inc.

- 6.4.4 AptarGroup Inc.

- 6.4.5 Origin Pharma Packaging

- 6.4.6 Pretium Packaging

- 6.4.7 Klckner Pentaplast

- 6.4.8 Comar

- 6.4.9 Gil Plastic Products Ltd

- 6.4.10 Drug Plastics Group

- 6.4.11 West Pharmaceutical Services Inc.

- 6.4.12 Nemera

- 6.4.13 Bormioli Pharma

- 6.4.14 Alpla Group

- 6.4.15 Sanner GmbH

- 6.4.16 Tekni-Plex

- 6.4.17 Weener Plastics

- 6.4.18 Jabil Healthcare (Nypro)

- 6.4.19 Stevanato Group (EZ-fill polymer vials)

- 6.4.20 Raumedic AG

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment