|

市场调查报告书

商品编码

1934764

东协防水市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031)ASEAN Waterproofing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

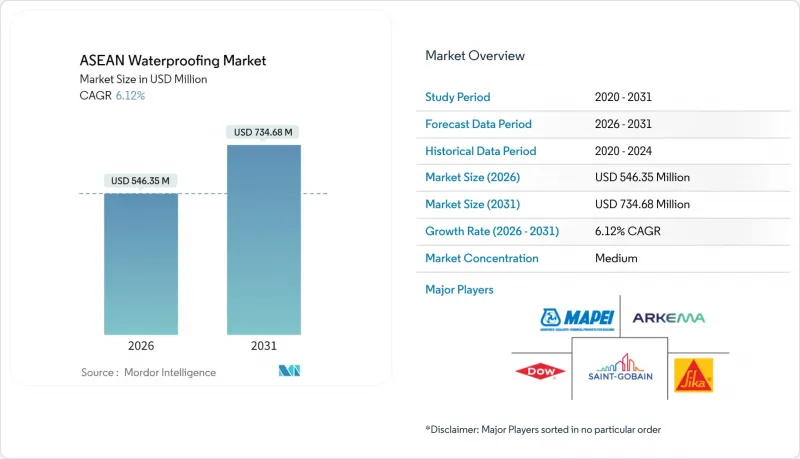

东协防水市场预计将从 2025 年的 5.1486 亿美元成长到 2026 年的 5.4635 亿美元,到 2031 年将达到 7.3468 亿美元,2026 年至 2031 年的复合年增长率为 6.12%。

强而有力的政府资本支出计画、住宅的稳定復苏以及对气候变迁调适的优先重视,正推动东协防水市场保持持续成长动能。印尼、马来西亚、泰国和越南的大型计划与高性能防水卷材、液体防水系统和水泥基涂料的采购直接相关,这些材料用于保护潮湿多雨环境下的钢筋混凝土结构。同时,新加坡和泰国的绿色建筑法规,以及城市层面的绿色屋顶奖励,正在加速采用整合了防潮层、隔热层和防根层等功能的优质防水组件。市场竞争格局仍保持平衡。跨国製造商正日益实现生产在地化以控制运输成本,而本地专业公司则凭藉其成本柔软性和计划经验订单中型专案。儘管原材料价格波动和认证安装人员短缺限制了短期利润率,但也推动了技术创新,朝着更简单、更省力的产品方向发展。

东协防水市场趋势与洞察

政府基础建设支出激增

为交通走廊、机场、供水系统和防洪工程等计划提供的财政奖励策略,带动了结晶质外加剂、隧道防水膜和桥面涂料订单的激增。越南已将2025年公共投资支出上限提高至743.33兆越南盾。这主要得益于《公共投资法》的修订,旨在缩短采购週期,并促进公路、港口和地铁计划采用先进的防水技术。资本计划业主通常将70%的建设成本用于材料,其中防水虽然占比不大,但却是实现热带地区预期使用寿命的关键组成部分。亚洲开发银行估计,2016年至2030年间,东协基础设施缺口将达到2.8兆美元至3.1兆美元,这确保了对包括高性能防潮系统在内的建筑化学品的长期需求。

都市区住宅热潮(东协)

城市人口的快速增长和土地供应的紧张推动了高层公寓大楼和以公共交通为导向的开发项目的兴起,对坚固的外墙保护提出了更高的要求。新加坡的《2040年陆路交通总体规划》拨款225亿瑞士法郎用于铁路网络建设,鼓励在铁路沿线建造住宅。屋顶防水膜必须符合绿地法规。在菲律宾,城镇计划的外商直接投资增加,推动了对兼具成本效益和十年保固的水泥基涂料的需求。在全部区域,开发商正在转向使用液态涂覆型防水膜,这种防水膜能够适应复杂的几何形状,减少接缝缺陷和人工成本。在工期紧张的情况下,这些防水膜是一个极具吸引力的选择。市场需求也转向丙烯酸-聚氨酯混合体系,这种体系的延伸率超过300%,并且能够在两小时内达到防雨性能。这些特质在漫长的季风季节尤其重要。这些住宅市场趋势确保了东协防水市场的持续采购週期,因为每个公寓大楼的建造阶段和维修週期都需要新的防水层。

原物料价格波动

在膜材生产中,石脑油衍生物、基础沥青和聚合物树脂占生产成本的70%之多。根据Polymerupdate报道,2025年4月东南亚苯乙烯单体价格为每吨910-920美元,较上月下降30美元,凸显了受中国需求疲软影响导致的价格快速波动。根据BitumenMag报道,由于SBS和APP改质剂价格下跌导致价差收窄,聚合物改性沥青生产商面临利润压力,而与原油价格挂钩的黏合剂价格则保持坚挺。对于缺乏避险机製或后向整合的东协中小型防水产业参与者而言,原物料成本的波动正在侵蚀其息税折旧摊提前利润(EBITDA),导致週期性停产和配方改善的资本投资放缓。

细分市场分析

预计到2025年,防水卷材将占东协防水市场43.62%的份额,并在2031年之前以6.78%的复合年增长率成长,成为东协防水市场新增收入的主要驱动力。这一成长主要得益于热塑性聚烯(TPO)和三元乙丙橡胶(EPDM)的创新,这些材料具有超过15年的紫外线稳定性、化学惰性和低温焊接性能。大金的含氟聚合物添加剂可提高表面反射率和耐热老化性能,延长热带地区屋顶的使用寿命。

未来的研发重点在于开发自修復膜,这种薄膜集成了微胶囊聚合物,可在穿孔后激活,从而降低业主的全生命週期成本,并在以规格为导向的竞标中使供应商脱颖而出。新兴的混合片材将TPO面层与丁基橡胶背衬相结合,实现机械和化学双重粘合,简化了复杂穿孔的详细设计。投资建设区域先导工厂生产此类复合材料的供应商可以降低运输成本,并符合在地采购要求,从而增强其在公共资助计划竞标的竞争力。

东协防水市场报告按系统类型(水泥基系统、防水卷材、止水带、耐化学腐蚀防水系统)、应用领域(屋顶和墙面、地面和地下室、用水和污水处理、隧道衬砌等)以及地区(马来西亚、印尼、泰国、新加坡、菲律宾、越南、缅甸)进行细分。市场预测以美元以金额为准。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 政府基础建设支出激增

- 东协都市区住宅热潮

- 热带气候中的湿度挑战

- 大城市的绿色屋顶概念

- 根据东协自由贸易协定降低进口关税

- 市场限制

- 原物料价格波动

- 地缘政治贸易紧张局势

- 熟练防水工人短缺

- 价值链分析

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 依系统类型

- 水泥基防水系统

- 膜

- 止水材料

- 耐化学腐蚀防水系统

- 透过使用

- 屋顶和墙壁

- 楼层/地下室

- 用水和污水管理

- 隧道衬砌

- 桥樑和高速公路

- 其他用途

- 按地区

- 马来西亚

- 印尼

- 泰国

- 新加坡

- 菲律宾

- 越南

- 缅甸

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率(%)/排名分析

- 公司简介

- Ardex Group

- Arkema

- Campbridge Paints Inc.

- Dow

- Henkel AG & Co. KGaA(Henkel Polybit Industries)

- MAPEI SpA

- Minerals Technologies Inc.

- Pidilite Industries Ltd.

- PT. SELARAS CIPTA GLOBAL

- Saint-Gobain

- Sika AG

- Solmax

- SOPREMA Group

- SWC Construction

- Xypex Chemical Corporation

第七章 市场机会与未来展望

The ASEAN Waterproofing Market is expected to grow from USD 514.86 million in 2025 to USD 546.35 million in 2026 and is forecast to reach USD 734.68 million by 2031 at 6.12% CAGR over 2026-2031.

Robust government capital-expenditure pipelines, a steady residential construction up-cycle, and climate-adaptation priorities converge to keep the ASEAN waterproofing market on a durable growth path. Infrastructure megaprojects in Indonesia, Malaysia, Thailand, and Vietnam are translating directly into procurement of high-performance membranes, liquid-applied systems, and cementitious coatings that secure reinforced-concrete assets in humid, high-rainfall conditions. At the same time, green-building mandates in Singapore and Thailand, together with city-level incentives for vegetated roofs, are accelerating the specification of premium waterproofing assemblies that combine moisture barriers, insulation, and root-resistance layers. Competitive dynamics remain balanced: multinational manufacturers are localizing production to manage freight costs, while regional specialists leverage cost agility and project relationships to win mid-scale work. Raw-material price swings and the shortage of certified applicators cap short-term margins but also catalyze innovation toward simplified, labor-saving products.

ASEAN Waterproofing Market Trends and Insights

Government Infrastructure Spending Surge

Fiscal stimulus is funneling into transport corridors, airports, water-supply schemes, and flood-control projects, creating immediate order books for concrete-integral crystalline admixtures, tunnel-grade membranes, and bridge-deck coatings. Vietnam has lifted its 2025 public-investment disbursement ceiling to VND 743,330 billion, a move supported by a revised Public Investment Law that speeds procurement timelines and opens doors for advanced waterproofing formulas in expressway, port, and metro packages. Capital-project owners typically allocate 70% of construction outlays to materials, of which waterproofing constitutes a small yet mission-critical fraction to secure service-life targets under tropical conditions. The Asian Development Bank pegs the 2016-2030 ASEAN infrastructure gap at USD 2.8-3.1 trillion, assuring long-run demand for construction chemicals, including high-performance moisture-barrier systems.

Residential-Housing Boom in Urban ASEAN

Surging urban populations and tightening land supplies are spawning high-rise condominiums and transit-oriented developments that require robust envelope protection. In Singapore, the Land Transport Master Plan 2040 commits CHF 22.5 billion to rail connections that stimulate adjacent residential construction, where roof-deck membranes must satisfy green-plot ratio rules. The Philippines is experiencing intensified foreign-direct-investment inflows into township projects, driving volume for cost-optimized cementitious coatings that still deliver 10-year warranties. Across the region, developers are upgrading to liquid-applied membranes that contour complex geometries, reducing joint failures and cutting labor hours-an attractive proposition amid tight construction schedules. Demand is also shifting toward hybrid acrylic-polyurethane systems offering elongation above 300% and rain-resistance in under two hours, features prized during the long monsoon season. These residential dynamics ensure recurring procurement cycles for the ASEAN waterproofing market as each condominium phase and refurbishment cycle specifies fresh layers of protection.

Raw-Material Price Volatility

Naphtha derivatives, base bitumen, and polymer resins account for up to 70% of production cost in membrane manufacturing. Polymerupdate recorded Southeast Asian styrene monomer prices at USD 910-920 per metric ton in April 2025, down USD 30 month-on-month, underscoring price whiplash tied to Chinese demand weakness. BitumenMag notes that polymer-modified bitumen producers saw profit squeezes when crude-linked binder prices held firm while SBS and APP modifiers fell, compressing spread margins. Volatile feedstock costs erode EBITDA for smaller ASEAN waterproofing industry participants lacking hedging tools or backward integration, leading to periodic shutdowns and slowed capex on formulation upgrades.

Other drivers and restraints analyzed in the detailed report include:

- Tropical-Climate Moisture Challenges

- Green-Roof Initiatives in Megacities

- Skilled Waterproofing Labor Gap

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Membranes claimed a 43.62% ASEAN waterproofing market share in 2025, and the segment is forecast to grow at a 6.78% CAGR through 2031, driving the lion's share of incremental revenue within the ASEAN waterproofing market size. Growth stems from thermoplastic polyolefin (TPO) and ethylene propylene diene monomer (EPDM) innovations that deliver UV stability beyond 15 years, chemical inertia, and weldability at lower temperatures. Daikin's fluoro-polymer additives boost surface reflectance and heat-aging performance, giving tropical rooftops an extended life cycle.

Looking ahead, research and development pipelines feature self-healing membranes integrating microencapsulated polymers that activate upon puncture, thus lowering life-cycle costs for owners and differentiating suppliers in specification-heavy tenders. Emerging hybrid sheets combine TPO topsides with butyl-rubber undersides for dual-mode adhesion, mechanical, and chemical, simplifying detailing at complicated penetrations. Suppliers investing in regional pilot plants to produce such composites gain freight savings and qualify under local-content rules, enhancing bid competitiveness across publicly financed projects.

The ASEAN Waterproofing Report is Segmented by System Type (Cementitious Systems, Membranes, Water Stops, and Chemical Resisting Water Proofing System), Application (Roofing and Walls, Floor and Basement, Water and Waste Management, Tunnel Liner, and More), and Geography (Malaysia, Indonesia, Thailand, Singapore, Philippines, Vietnam, and Myanmar). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Ardex Group

- Arkema

- Campbridge Paints Inc.

- Dow

- Henkel AG & Co. KGaA (Henkel Polybit Industries)

- MAPEI S.p.A.

- Minerals Technologies Inc.

- Pidilite Industries Ltd.

- PT. SELARAS CIPTA GLOBAL

- Saint-Gobain

- Sika AG

- Solmax

- SOPREMA Group

- SWC Construction

- Xypex Chemical Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Govt infrastructure spending surge

- 4.2.2 Residential housing boom in urban ASEAN

- 4.2.3 Tropical climate moisture challenges

- 4.2.4 Green-roof initiatives in megacities

- 4.2.5 Lower import tariffs via ASEAN FTAs

- 4.3 Market Restraints

- 4.3.1 Raw-material price volatility

- 4.3.2 Geopolitical trade friction

- 4.3.3 Skilled waterproofing labour gap

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By System Type

- 5.1.1 Cementitious Systems

- 5.1.2 Membranes

- 5.1.3 Water Stops

- 5.1.4 Chemical Resisting Water Proofing System

- 5.2 By Application

- 5.2.1 Roofing and Walls

- 5.2.2 Floor and Basement

- 5.2.3 Water and Waste Management

- 5.2.4 Tunnel Liner

- 5.2.5 Bridge and Highway

- 5.2.6 Other Applications

- 5.3 By Geography

- 5.3.1 Malaysia

- 5.3.2 Indonesia

- 5.3.3 Thailand

- 5.3.4 Singapore

- 5.3.5 Philippines

- 5.3.6 Vietnam

- 5.3.7 Myanmar

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Ardex Group

- 6.4.2 Arkema

- 6.4.3 Campbridge Paints Inc.

- 6.4.4 Dow

- 6.4.5 Henkel AG & Co. KGaA (Henkel Polybit Industries)

- 6.4.6 MAPEI S.p.A.

- 6.4.7 Minerals Technologies Inc.

- 6.4.8 Pidilite Industries Ltd.

- 6.4.9 PT. SELARAS CIPTA GLOBAL

- 6.4.10 Saint-Gobain

- 6.4.11 Sika AG

- 6.4.12 Solmax

- 6.4.13 SOPREMA Group

- 6.4.14 SWC Construction

- 6.4.15 Xypex Chemical Corporation

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

全球浴室防水解决方案市场规模、份额、趋势和成长分析报告(2026-2034年)全球结晶质防水材料市场规模、份额、趋势及成长分析报告(2026-2034年)全球防水系统市场规模、份额、趋势和成长分析报告(2026-2034)

全球浴室防水解决方案市场规模、份额、趋势和成长分析报告(2026-2034年)全球结晶质防水材料市场规模、份额、趋势及成长分析报告(2026-2034年)全球防水系统市场规模、份额、趋势和成长分析报告(2026-2034) 2026年全球聚乙烯防潮层市场报告

2026年全球聚乙烯防潮层市场报告 全球湿房防水解决方案市场-按类型、原料、地区和竞争格局分類的产业规模、份额、趋势、机会和预测(2021-2031年)防潮层市场 - 全球产业规模、份额、趋势、机会及预测(按类型、柔性材料、刚性材料、最终用户、地区和竞争格局划分,2021-2031年)

全球湿房防水解决方案市场-按类型、原料、地区和竞争格局分類的产业规模、份额、趋势、机会和预测(2021-2031年)防潮层市场 - 全球产业规模、份额、趋势、机会及预测(按类型、柔性材料、刚性材料、最终用户、地区和竞争格局划分,2021-2031年) 印度防水解决方案市场:市场份额分析、行业趋势、统计数据和成长预测(2026-2031 年)防水解决方案:市场占有率分析、产业趋势与统计、成长预测(2026-2031)防水外加剂市场-全球产业规模、份额、趋势、机会和预测,按类型、应用、地区和竞争格局划分,2020-2030年预测

印度防水解决方案市场:市场份额分析、行业趋势、统计数据和成长预测(2026-2031 年)防水解决方案:市场占有率分析、产业趋势与统计、成长预测(2026-2031)防水外加剂市场-全球产业规模、份额、趋势、机会和预测,按类型、应用、地区和竞争格局划分,2020-2030年预测 全球防水系统市场

全球防水系统市场