|

市场调查报告书

商品编码

1934795

泰国润滑油:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Thailand Lubricants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

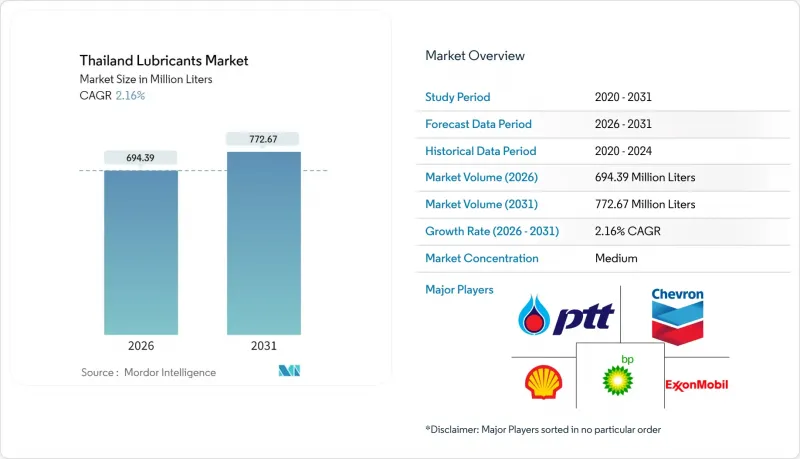

预计泰国润滑油市场将从 2025 年的 6.797 亿公升成长到 2026 年的 6.9439 亿公升,到 2031 年将达到 7.7267 亿公升,2026 年至 2031 年的复合年增长率为 2.16%。

由于电气化导致内燃机油需求下降,但泰国作为东南亚皮卡生产中心以及整车和零件区域配销中心的地位,抵消了这一影响。持续的资料中心建设(投资额超过70亿美元)以及对东部经济走廊(EEC)的稳步投资,正在推动特种冷却液和高性能工业油的消费。宏观因素也在发挥作用,包括商品出口的復苏、物流业对GDP 0.4%的贡献,以及欧5柴油品质标准的实施(该标准提高了产品规格,并促进了向合成油的转型)。来自东协低成本进口产品的竞争压力正在挤压主流矿物油混合油的利润空间,而电动车冷却液、液体冷却解决方案和甲醇相容型船用润滑油的优质化机会正在扩大。

泰国润滑油市场趋势及展望

疫情后製造业及出口復苏

随着供应链中断的缓解,工厂使用率有所提高,使得泰国投资促进委员会 (BOI) 在 2024 年第一季的核准增加了 13%。其中,电子、汽车和机械相关产业尤其受到关注。金属加工活动的活性化和运作的延长推动了精密加工生产线对油压油、切削油和抗磨润滑脂的需求。出口型企业对黏度公差的要求更为严格,更倾向半合成和全合成润滑油。生产计划的稳定也使润滑油采购週期得以恢復,此前由于 2023 年的物流瓶颈而有所延误。泰国润滑油市场受益于国内成熟的供应商网络,这确保了跨国原始设备製造商 (OEM) 的稳定产品供应。

商用车车队扩充与电子商务物流

预计到2024年,线上零售渗透率将超过零售总额的18%,将推动宅配公司和第三方物流公司扩大车队规模。行驶里程的增加导致换油频率增加,尤其是在都市区频繁启动的外送车上。营运商越来越多地采用SAE 10W-30合成机油来降低油耗并延长换油週期,以较低的初始润滑油成本换取更低的营运总成本。虽然泰国政府4,500亿泰铢的财政奖励策略改善了农村道路,缩短了运输时间,但平均车速却有所提高,这给车轴和变速箱带来了更大的热应力。因此,市场对高油膜强度的齿轮油的需求也随之增加。

电动车的快速普及导致内燃机润滑油市场萎缩。

2022年至2024年间,在每辆车5万至10万泰铢的补助推动下,电池式电动车的註册量预计将增加五倍,占所有新轻型车辆的9%。电动车无需使用曲轴箱润滑油,并减少了自动变速箱油的用量,从而缩小了汽车润滑油的主要来源。曼谷的计程车和末端配送货车正在逐步更换为电池式电动车车型,以充分利用充电基础设施补贴。然而,电动桥、电池托盘和温度控管子系统的製造也催生了对组装润滑脂和介电冷却剂的新需求,部分抵消了电动车对泰国润滑油市场的影响。

细分市场分析

预计到2025年,汽车机油将占泰国润滑油市场份额的46.89%,这反映了泰国每年超过200万辆的汽车产量以及超过2,100万辆轿车和皮卡的售后维护需求。与日本製造商签订的工厂灌装协议确保了稳定的基准供应,而出口(主要针对澳洲和中东的皮卡)则推动了年底出货高峰期的需求激增。

预计到2031年,润滑脂将以3.17%的复合年增长率实现最高成长,壳牌公司在泰国的扩张(年产量1.5万吨)将使泰国成为东南亚最大的润滑脂供应中心。东部经济走廊(EEC)包装厂安装的精密机器人和输送机系统有利于锂基复合润滑脂的应用,因为这种润滑脂具有良好的耐水冲刷性能。预计到2031年,润滑脂在泰国润滑油市场的销售量将超过4.62万吨,从而扩大其在特种产品收入中的市场份额。同时,随着都市区乘用车自动变速箱的普及率接近95%,预计变速箱油的需求将保持稳定。

泰国润滑油市场报告按产品类型(汽车引擎油、工业引擎油、变速箱油、齿轮油、煞车油、液压油、润滑脂等)、终端用户产业(汽车、船舶、航太、重型机械等)和基础油类型(矿物油基润滑油、半合成润滑油等)进行细分。市场预测以公升为单位。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 疫情后製造业及出口復苏

- 商用车车队扩充与电子商务物流

- 工业自动化推动了对高性能合成润滑油的需求

- 资料中心扩张推动特种冷冻/发电机润滑油需求成长

- 由于强制使用生质柴油(B20),引擎机油更换频率增加。

- 市场限制

- 由于电动车的加速普及,内燃机润滑油市场正在萎缩。

- 加强对矿物油废弃物的监管

- 来自东协低成本进口商品的利润压力

- 价值链分析

- 法律规范

- 终端用户趋势

- 汽车产业

- 製造业

- 发电业

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章 市场规模与成长预测

- 依产品类型

- 汽车引擎油

- 工业机油

- 变速箱油

- 齿轮油

- 煞车油

- 油压

- 润滑脂

- 加工油(包括橡胶加工油和白油)

- 金属加工油

- 涡轮机油

- 变压器油

- 其他产品类型

- 按最终用户行业划分

- 车

- 搭乘用车

- 商用车辆

- 摩托车

- 船

- 航太

- 重型机械

- 建造

- 矿业

- 农业

- 产业

- 发电

- 冶金/金属加工

- 纺织品

- 石油和天然气

- 其他终端用户产业

- 车

- 依基本类型

- 矿物油性润滑剂

- 合成润滑油

- 半合成润滑油

- 生物性润滑剂

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率**(%)/排名分析

- 公司简介

- Bangchak Corporation Public Company Limited

- BP plc

- Chevron Corporation

- ENEOS Corporation

- ExxonMobil Corporation

- FUCHS

- Idemitsu Kosan Co., Ltd.(Apollo(Thailand)Co., Ltd.)

- MOTUL(Thailand)Co., Ltd.

- PSP Specialties Public Company Limited

- PETRONAS Lubricants International

- PTT PUBLIC COMPANY LIMITED

- Shell Thailand

- Siam Pan Group Public Co., Ltd.

- Total Energies

- Valvoline

第七章 市场机会与未来展望

第八章:执行长面临的关键策略挑战

The Thailand Lubricants Market is expected to grow from 679.70 Million Liters in 2025 to 694.39 Million Liters in 2026 and is forecast to reach 772.67 Million Liters by 2031 at 2.16% CAGR over 2026-2031.

The softer demand for internal-combustion-engine (ICE) oils from electrification is balanced by Thailand's continued role as Southeast Asia's pickup-truck production hub and its position as a regional distribution center for finished vehicles and components. Ongoing data center construction valued at above USD 7 billion, along with steady investment in the Eastern Economic Corridor (EEC), drives the consumption of specialty cooling fluids and high-performance industrial oils. Macro factors, such as a rebound in merchandise exports, a 0.4% GDP contribution from logistics, and the enforcement of Euro 5 diesel quality standards, which tighten product specifications and support the shift toward synthetic formulations. Competitive pressure from lower-cost ASEAN imports keeps margins thin for mainstream mineral oil blends, yet premiumization opportunities in EV fluids, immersion-cooling solutions, and methanol-compatible marine lubricants are expanding.

Thailand Lubricants Market Trends and Insights

Post-pandemic rebound in manufacturing and exports

Factory utilization improved after supply-chain disruptions eased, and Board of Investment approvals rose 13% in value during Q1 2024, with a focus on electronics, automotive, and machinery ventures. Higher metalworking activity and longer operating hours raise demand for hydraulic oils, cutting fluids, and anti-wear greases in precision machining lines. Export-oriented firms specify tighter viscosity tolerances that favor semi-synthetic and full-synthetic blends. Production scheduling stability also restores lubricant procurement cycles that had been delayed during 2023's logistics bottlenecks. The Thailand lubricants market benefits from the country's established supplier network, which provides consistent product availability for multinational OEMs.

Expansion of commercial-vehicle fleet and e-commerce logistics

Online retail penetration exceeded 18% of total retail sales in 2024, prompting fleet additions among parcel carriers and third-party logistics firms. Vehicle-kilometer-traveled growth translates into higher oil drain frequency, particularly for delivery vans operating stop-start urban routes. Operators are increasingly adopting SAE 10W-30 synthetics to reduce fuel consumption and extend drain intervals, trading upfront lubricant costs for lower total operating expenses. Provincial road upgrades under Thailand's THB 450 billion fiscal stimulus reduce transit times but increase average speeds, elevating axle and transmission temperature loads that require high-film-strength gear oils.

Accelerated EV adoption shrinking ICE lubricant pool

Registrations of battery electric cars grew fivefold between 2022 and 2024, reaching 9% of all new light-duty vehicles, supported by subsidies of THB 50,000-100,000 per unit. EVs eliminate demand for crankcase oils and reduce automatic transmission-fluid volumes, shrinking the core automotive lubricant reservoir. Fleets in Bangkok are shifting taxis and last-mile delivery vans to battery electric models to capitalize on charging infrastructure grants. However, manufacturing of e-axles, battery trays, and thermal-management subsystems introduces new requirements for assembly greases and dielectric coolants, providing a partial offset for the Thailand lubricants market.

Other drivers and restraints analyzed in the detailed report include:

- Industrial automation boosting demand for high-performance synthetics

- Data-center buildouts driving specialty cooling and genset lubricants

- Stricter mineral-oil disposal regulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Automotive engine oil captured 46.89% of Thailand lubricants market share in 2025, reflecting annual vehicle output above 2 million units and a robust aftermarket servicing fleet that exceeds 21 million cars and pickups. Factory-fill contracts with Japanese OEMs ensure baseline volume stability, while pickup-centric exports to Australia and the Middle East create incremental demand spikes leading up to year-end shipping windows.

Greases deliver the highest 3.17% CAGR through 2031 as Shell's plant expansion to 15,000 tonnes per year turns Thailand into Southeast Asia's largest grease supply base. Precision robotics and conveyor systems installed in EEC packaging plants prefer lithium-complex greases tolerant to water washout. The Thailand lubricants market size for greases is projected to exceed 46,200 tonnes by 2031, accounting for a growing share of specialty product revenue. Concurrently, transmission-fluid demand holds steady, bolstered by automatic-gearbox penetration approaching 95% in urban passenger cars.

The Thailand Lubricants Market Report is Segmented by Product Type (Automotive Engine Oil, Industrial Engine Oil, Transmission Fluids, Gear Oil, Brake Fluids, Hydraulic Fluids, Greases, and More), End-User Industry (Automotive, Marine, Aerospace, Heavy Equipment, and More), and Base Stock Type (Mineral Oil-Based Lubricants, Semi-Synthetic Lubricants, and More). The Market Forecasts are Provided in Terms of Volume (Liters).

List of Companies Covered in this Report:

- Bangchak Corporation Public Company Limited

- BP p.l.c.

- Chevron Corporation

- ENEOS Corporation

- ExxonMobil Corporation

- FUCHS

- Idemitsu Kosan Co., Ltd. (Apollo (Thailand) Co., Ltd.)

- MOTUL ( Thailand ) Co., Ltd.

- P.S.P. Specialties Public Company Limited

- PETRONAS Lubricants International

- PTT PUBLIC COMPANY LIMITED

- Shell Thailand

- Siam Pan Group Public Co., Ltd.

- Total Energies

- Valvoline

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Post-pandemic Rebound in Manufacturing and Exports

- 4.2.2 Expansion of Commercial-vehicle Fleet and E-commerce Logistics

- 4.2.3 Industrial Automation Boosting Demand for High-performance Synthetics

- 4.2.4 Data-center Buildouts Driving Specialty Cooling/genset Lubricants

- 4.2.5 Biodiesel (B20) Mandate Raising Engine-oil Change Frequency

- 4.3 Market Restraints

- 4.3.1 Accelerated EV Adoption Shrinking ICE Lubricant Pool

- 4.3.2 Stricter Mineral-oil Disposal Regulations

- 4.3.3 Margin Pressure from Low-cost ASEAN Imports

- 4.4 Value Chain Analysis

- 4.5 Regulatory Framework

- 4.6 End-User Trends

- 4.6.1 Automotive Industry

- 4.6.2 Manufacturing Industry

- 4.6.3 Power Generation Industry

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Product Type

- 5.1.1 Automotive Engine Oil

- 5.1.2 Industrial Engine Oil

- 5.1.3 Transmission Fluids

- 5.1.4 Gear Oil

- 5.1.5 Brake Fluids

- 5.1.6 Hydraulic Fluids

- 5.1.7 Greases

- 5.1.8 Process Oil (Including Rubber Process Oil & White Oil)

- 5.1.9 Metalworking Fluids

- 5.1.10 Turbine Oil

- 5.1.11 Transformer Oil

- 5.1.12 Other Product Types

- 5.2 By End-user Industry

- 5.2.1 Automotive

- 5.2.1.1 Passenger Vehicles

- 5.2.1.2 Commercial Vehicles

- 5.2.1.3 Two-Wheelers

- 5.2.2 Marine

- 5.2.3 Aerospace

- 5.2.4 Heavy Equipment

- 5.2.4.1 Construction

- 5.2.4.2 Mining

- 5.2.4.3 Agriculture

- 5.2.5 Industrial

- 5.2.5.1 Power Generation

- 5.2.5.2 Metallurgy & Metalworking

- 5.2.5.3 Textiles

- 5.2.5.4 Oil and Gas

- 5.2.5.5 Other End-Use Industries

- 5.2.1 Automotive

- 5.3 By Base Stock Type

- 5.3.1 Mineral Oil-Based Lubricants

- 5.3.2 Synthetic Lubricants

- 5.3.3 Semi-Synthetic Lubricants

- 5.3.4 Bio-Based Lubricants

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share**(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 Bangchak Corporation Public Company Limited

- 6.4.2 BP p.l.c.

- 6.4.3 Chevron Corporation

- 6.4.4 ENEOS Corporation

- 6.4.5 ExxonMobil Corporation

- 6.4.6 FUCHS

- 6.4.7 Idemitsu Kosan Co., Ltd. (Apollo (Thailand) Co., Ltd.)

- 6.4.8 MOTUL ( Thailand ) Co., Ltd.

- 6.4.9 P.S.P. Specialties Public Company Limited

- 6.4.10 PETRONAS Lubricants International

- 6.4.11 PTT PUBLIC COMPANY LIMITED

- 6.4.12 Shell Thailand

- 6.4.13 Siam Pan Group Public Co., Ltd.

- 6.4.14 Total Energies

- 6.4.15 Valvoline

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

8 Key Strategic Questions for CEOs

纺织润滑剂市场:依产品类型、剂型、应用及最终用途划分-2026年至2032年全球预测金属切削润滑剂市场:依产品类型、金属类型、应用、终端用户产业和通路划分-2026-2032年全球预测

纺织润滑剂市场:依产品类型、剂型、应用及最终用途划分-2026年至2032年全球预测金属切削润滑剂市场:依产品类型、金属类型、应用、终端用户产业和通路划分-2026-2032年全球预测 润滑油过滤器市场规模、份额和成长分析:按过滤器类型、应用、材质、最终用户和地区划分 - 2026-2033 年产业预测

润滑油过滤器市场规模、份额和成长分析:按过滤器类型、应用、材质、最终用户和地区划分 - 2026-2033 年产业预测 2026-2034年全球纱线润滑剂市场规模、份额、趋势和成长分析报告

2026-2034年全球纱线润滑剂市场规模、份额、趋势和成长分析报告 玻璃润滑剂市场规模、份额和成长分析:按润滑剂基础类型、配方类型、应用方法、包装类型、最终用户产业和地区划分-2026-2033年产业预测自行车润滑脂市场按产品类型、通路、浓稠度等级和应用划分-全球预测,2026-2032年

玻璃润滑剂市场规模、份额和成长分析:按润滑剂基础类型、配方类型、应用方法、包装类型、最终用户产业和地区划分-2026-2033年产业预测自行车润滑脂市场按产品类型、通路、浓稠度等级和应用划分-全球预测,2026-2032年 Isododecane润滑剂市场规模、份额和成长分析:按产品类型、应用、最终用户和地区划分-2026-2033年产业预测

Isododecane润滑剂市场规模、份额和成长分析:按产品类型、应用、最终用户和地区划分-2026-2033年产业预测 润滑油市场分析及预测(至2035年):依类型、产品、应用、技术、最终用户、形态、功能、安装类型及解决方案划分

润滑油市场分析及预测(至2035年):依类型、产品、应用、技术、最终用户、形态、功能、安装类型及解决方案划分 南美润滑油:市场占有率分析、产业趋势与统计、成长预测(2026-2031)越南润滑油:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

南美润滑油:市场占有率分析、产业趋势与统计、成长预测(2026-2031)越南润滑油:市场占有率分析、产业趋势与统计、成长预测(2026-2031)