|

市场调查报告书

商品编码

1934885

印度电气外壳市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031)India Electrical Enclosures - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

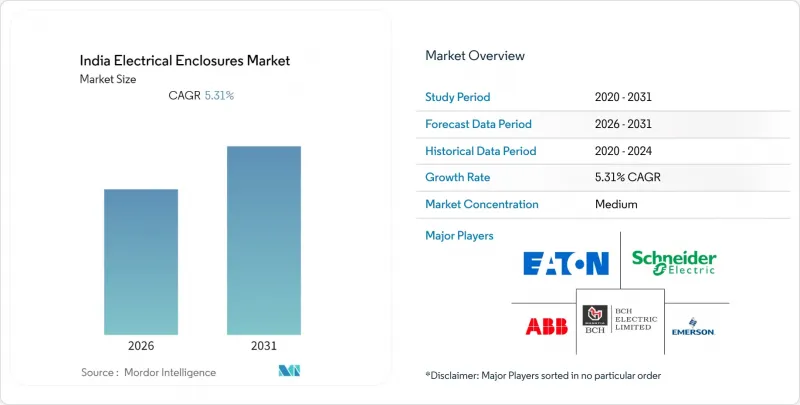

预计在预测期内,印度电气外壳市场将实现 5.31% 的复合年增长率。

快速的电网现代化改造项目、超大规模资料中心的扩张以及日益严格的消防安全法规正在加速对坚固耐用、智慧化且耐候性强的机柜的采购。国有电力公司不断增加的资本支出(CAPEX)超过1万亿印度卢比,尤其是在765千伏输电线路建设方面,推动了机柜销量的增长,而产品构成比向高规格金属设计的转变则支撑了价值的增长。预计超大规模设施的容量将从2024年的1150兆瓦增加到2027年的2100兆瓦,这将带动对IP54+防护等级和温度控管机柜的新需求,尤其是在孟买、清奈和海得拉巴等城市。 2016年国家建筑规范的实施推动了医院、学校和公共机构的维修需求,而印度铁路98%的电网电气化率也支持了持续的维护需求。这些因素,加上适度的竞争和不断增加的在地化奖励,为印度电气机柜市场未来的多年成长奠定了基础。

印度电气柜市场趋势与洞察

国有公用事业公司正在快速投资,以实现电网现代化。

各邦电力公司正大力投资高压输电线路,中央政府仅跨邦输电网路就拨款1兆卢比。古吉拉突邦1500亿卢比的升级计划就是一个典型例子,该计划要求在新765千伏输电线路沿线安装大型IP65防护等级的保护继电器机壳。市场对具备先进温控功能的镀锌钢和铝製机柜的需求不断增长,推动了印度电气外壳市场的销售和平均售价。拥有BIS IS 2147标准认证并具备整合智慧电网感测器能力的供应商有望提高竞标率。随着安装地点从室内变电站转向节省空间的室外场地,耐腐蚀涂层和双层门封正成为关键的差异化因素。中期影响显着,有助于维持与主要原始设备製造商(OEM)的稳定订单。

超大规模资料中心建置的扩展

预计到2027年,全球IT总装置容量将从2024年的1,150兆瓦成长到2,100兆瓦,将使高密度配电单元、母线槽和电池备用配电盘的需求翻倍。超大规模资料中心正在采用具有整合隔热层和线缆管理系统的模组化钢框架,以适应超过10千瓦的机架密度。采购週期正在加快,这有利于那些能够保持本地组装柔软性和库存缓衝的供应商。由于运转率要求超过99.999%,业者强制要求机壳具备IP54或更高的密封等级、双冗余冷却风扇以及预先整合的数位跳脱断路器。虽然主要城市仍然是部署中心,但区域城市的边缘节点正在推动增量需求。随着预先签订合约的超大规模容量过渡到土木工程和电气施工,近期需求成长显而易见。

钢铁和铝价格波动

2024年,受中国进口热轧钢反倾销税和炼焦煤价格波动的影响,热轧钢价格每吨波动幅度达3000印度卢比。铝溢价则与伦敦金属交易所(LME)铝价的飙升密切相关,而LME铝价的飙升又受到能源价格波动的驱动。按季度签订合约的小规模机壳製造商发现避险十分困难,迫使他们重新评估利润率并缩小零件尺寸。一些原始设备製造商(OEM)已将侧板厚度从2毫米减至1.6毫米,但这存在降低大型机柜刚性的风险。原物料价格风险的增加抑制了长期固定价格竞标的积极性,并导致与国有电力公司合作竞标的合约授予延迟。儘管预计从2026年起波动性将有所缓解,但由于短期不利因素,复合年增长率(CAGR)预测已下调80个基点。

细分市场分析

到2025年,金属机壳将占印度电气外壳市场70.85%的份额,其中镀锌钢板在牵引变电站和大电流开关设备中占据主导地位。预计到2025年,金属产品市场规模将达到1.8639亿美元,到2031年将以4.78%的复合年增长率成长。铝材因其重量优势,成为屋顶太阳能汇流箱的首选材料。不断上涨的防腐蚀涂漆营运成本(OPEX)正促使沿海电力公司转向玻璃纤维增强塑胶(FRP)和聚碳酸酯产品,这些产品的复合年增长率将达到7.42%。非金属机柜发热量较低,因此非常适合用于资料中心走廊的封闭。Schneider Electric位于加尔各答的树脂工厂和ABB位于瓦多达拉的FRP生产线表明,供应商正致力于复合材料业务的成长。儘管由于进口树脂的成本和 BIS IS 14772 测试费用,单价仍然高出 15-20%,但总体拥有成本分析仍然显示,一些规范制定者建议在盐碱和化学环境中选择这种聚合物。

第二代工程塑胶现已符合垂直火焰和紫外线老化测试标准,显示已准备好应用于电力设施。聚碳酸酯模具具有符合人体工学的锁扣整合和透明门设计,便于快速目视检查,从而增强了职业安全审核。同时,在存在高故障电流汇流排和敏感SCADA继电器的环境中,金属机柜在电磁屏蔽性能方面仍然无可匹敌。儘管从应用案例来看,金属材料仍将继续占据主导地位,但复合材料在沿海地区和资料基础设施领域逐渐找到新的应用空间。

到2025年,壁挂式产品将占出货量的36.25%,是商业建筑和地铁站配电盘维修的必备之选。其紧凑的面积、铰链门和后部电缆入口简化了租户的室内安装。同时,模组化通道式系统正以6.98%的复合年增长率快速成长,因为超大规模业者会在异地预组装包含塑壳断路器、变压器和监控PLC的异地设备。虽然其价格比同类产品高出25%,但运作时间缩短了35%,这对于寻求满足运转率协定(SLA)的託管营运商而言至关重要。

在变电站、钢铁厂和污水处理厂等设施中,由于重型设备和大截面汇流排需要底部电缆入口和底座安装,自主型落地柜正被广泛采用。屋顶太阳能发电的日益普及,尤其是在拉贾斯坦邦和古吉拉突邦,推动了对接线盒的需求。对于原始设备製造商 (OEM) 而言,多样化的外形规格为交叉销售奠定了基础。Schneider Electric的 Prisma-Plus 在壁挂式接线盒领域处于领先地位,而 SM AirSeT 则占据了落地式接线盒市场。系统整合商越来越多地在框架竞标中捆绑多种外形规格,并对拥有丰富产品目录和标准化内部安装网格的供应商进行评估。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 国营电力企业为实现电网现代化而迅速增加资本支出

- 超大规模资料中心建置的扩展

- 公共建筑强制消防安全标准(NBC-2016)

- 印度铁路快速电气化

- 透过「生产连结奖励计画」(PLI)促进开关设备的本地化生产

- 屋顶光电维生态系的发展

- 市场限制

- 钢铁和铝价格波动

- 假冒知识产权合规产品的氾滥

- 州级认证体系碎片化

- 硅胶垫片供应链中的瓶颈

- 产业价值链分析

- 监管环境

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 依材料类型

- 由金属製成

- 非金属

- 按外形规格

- 壁挂式

- 落地式/自主型

- 接线盒/端子盒

- 模组化/定制

- 按安装类型

- 室内的

- 户外

- 透过使用

- 发电和配电

- 交通运输(铁路、地铁、机场)

- 石油和天然气

- 商业建筑和资料中心

- 加工工业(食品饮料、製药、化学)

- 其他用途

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Schneider Electric SE

- ABB Ltd.

- Siemens AG

- Eaton Corporation plc

- Emerson Electric Co.

- Legrand SA

- Hubbell Incorporated

- Rittal GmbH and Co. KG

- BCH Electric Ltd.

- Larsen and Toubro Limited

- Trinity Touch Pvt. Ltd.

- Fibox India Pvt. Ltd.

- Boxco Industries Ltd.

- Adswitch Limited

- Pentair Technical Solutions India Pvt. Ltd.

- VSM Plast

- GE TandD India Limited

- Panel Builders India Pvt. Ltd.

- Admac Systems

- Ensto India Pvt. Ltd.

第七章 市场机会与未来展望

India electrical enclosures market is expected to register a CAGR of 5.31% during the forecast period.

Rapid grid-modernization programs, hyperscale data-center expansion, and stringent fire-safety regulations are accelerating procurement of robust, smart, and weather-resistant enclosures. Accelerating state-utility CAPEX exceeding INR 1 lakh crore, particularly for 765 kV transmission corridors, is lifting unit volumes, while mix shifts toward higher-spec metallic designs sustains value growth. Hyperscale facilities scaling from 1,150 MW in 2024 to an expected 2,100 MW by 2027 are driving fresh demand for IP54-plus, thermally managed cabinets, especially in Mumbai, Chennai, and Hyderabad. Compliance with the National Building Code 2016 is stimulating retrofit orders across hospitals, schools, and public offices, and Indian Railways' 98% network electrification milestone is underpinning recurring maintenance demand. Together, these vectors create a multi-year runway for the India electrical enclosures market amid moderate competitive intensity and increasing localization incentives.

India Electrical Enclosures Market Trends and Insights

Surging Grid-Modernization CAPEX by State Utilities

State electricity boards are channelling record investments into high-voltage corridors, with the central allocation of INR 1 lakh crore for inter-state transmission alone. Gujarat's INR 15,000 crore upgrade plan typifies the scale, necessitating larger IP65-rated housings for protection relays along new 765 kV lines. Demand rises for galvanized steel and aluminium cabinets with advanced climate controls, propelling both volumes and average selling prices within the India electrical enclosures market. Vendors able to certify products under BIS IS 2147 and integrate smart-grid sensors see heightened tender success. As installations shift from indoor substations to space-saving outdoor yards, corrosion-resistant coatings and dual-door sealing emerge as key differentiators. The medium-term impact is significant, sustaining a solid order pipeline for principal OEMs.

Rising Hyperscale Data-Centre Buildouts

Total installed IT load is projected to grow from 1,150 MW in 2024 to 2,100 MW by 2027, doubling enclosure demand for high-density power distribution units, bus-ducts, and battery-backup switchboards. Hyperscale specifies modular steel frames with integrated thermal barriers and cable management to handle rack densities above 10 kW. Procurement cycles are rapid, favouring suppliers that keep local assembly lines agile and inventory buffered. Because uptime requirements exceed 99.999%, operators insist on IP54-plus sealing, dual-redundant cooling fans, and digital trip breakers pre-fitted into enclosures. Tier-1 cities remain the launch pads, but edge nodes in Tier-2 markets now drive incremental volumes. Short-term uplift is pronounced as pre-committed hyperscale capacity converts to civil works and electrical fitouts.

Steel and Aluminium Price Volatility

HRC steel swung by INR 3,000 per tonne during 2024 as anti-dumping duties on Chinese supply intersected with fluctuating coking-coal costs. Aluminium premiums tracked LME spikes driven by energy-price volatility. Smaller enclosure shops operating on quarterly rate contracts struggle to hedge, forcing margin resets or component downsizing. Some OEMs responded by redesigning side-panels at 1.6 mm thickness versus 2 mm, a trade-off that risks stiffness in larger cabinets. Elevated raw-material risk deters long-duration fixed-price bids, delaying awards on state-utility tenders. Although volatility should moderate past 2026, near-term headwinds shave 80 basis points off CAGR forecasts.

Other drivers and restraints analyzed in the detailed report include:

- Mandatory Fire-Safety Upgrades in Public Buildings (NBC-2016)

- Rapid Electrification of Indian Railways

- Proliferation of Counterfeit IP-Rated Products

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Metallic housings held 70.85% India electrical enclosures market share in 2025, with galvanized steel dominating traction substations and high-current switchboards. The India electrical enclosures market size for metallic products was USD 186.39 million in 2025 and is projected to expand at 4.78% CAGR to 2031. Aluminium earns favour in rooftop solar combiner boxes where weight matters. Rising OPEX on anti-corrosion repainting is nudging coastal utilities toward fiberglass and polycarbonate alternatives that clock a 7.42% CAGR. Non-metallic cabinets also absorb less heat, benefitting data-hall aisle containment. Schneider's Kolkata polymer plant and ABB's Vadodara FRP line illustrate supplier bets on composite growth. Imported resin costs and BIS IS 14772 testing fees keep unit prices at a 15-20% premium, yet total-cost-of-ownership analyses still tilt some specifiers toward polymer choices in saline or chemical environments.

Second-generation engineering plastics are now meeting vertical-flame and UV-aging standards, underscoring their readiness for utility deployments. Polycarbonate molds allow ergonomic latch integration and transparent doors for quick visual inspection, perks that bolster occupational safety audits. Conversely, metallic cabinets remain unrivalled for electromagnetic shielding when sensitive SCADA relays share space with high-fault-current busbars. The balance of use-cases points to sustained metallic dominance but with growing composite niches in coastal and data infrastructure.

Wall-mount products accounted for 36.25% of 2025 shipments and remain indispensable for distribution-panel retrofits in commercial towers and metro stations. Their compact footprint, hinged doors, and rear cable entry simplify tenant fit-outs. Meanwhile, modular aisle-based systems are surging at 6.98% CAGR as hyperscale operators pre-fabricate skids populated with MCCBs, transformers, and monitoring PLCs off-site. Like-for-like price premiums of 25% are offset by 35% faster go-live timelines, a metric valued by colocation providers chasing occupancy SLAs.

Free-standing floor cabinets service substations, steel mills, and wastewater plants where heavy gear and large-cross-section busbars require bottom cable entry and plinth-mount anchoring. Junction-box volumes track rooftop solar rollouts, especially in Rajasthan and Gujarat. For OEMs, form-factor diversification underpins cross-selling: Schneider's Prisma-Plus lends wall-mount segments while the SM AirSeT draws floor-mount demand. System integrators increasingly issue framework bids bundling multiple form factors, rewarding suppliers with broad catalogues and standardized internal mounting grids.

The India Electrical Enclosures Market Report is Segmented by Material Type (Metallic, Non-Metallic), Form Factor (Wall-Mount, Floor-mount/Free-standing, Junction/Terminal Boxes, Modular/Custom), Mounting Type (Indoor, Outdoor), Application (Power Generation and Distribution, Transportation, Oil and Gas, Commercial Buildings and Data Centres, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Schneider Electric SE

- ABB Ltd.

- Siemens AG

- Eaton Corporation plc

- Emerson Electric Co.

- Legrand SA

- Hubbell Incorporated

- Rittal GmbH and Co. KG

- BCH Electric Ltd.

- Larsen and Toubro Limited

- Trinity Touch Pvt. Ltd.

- Fibox India Pvt. Ltd.

- Boxco Industries Ltd.

- Adswitch Limited

- Pentair Technical Solutions India Pvt. Ltd.

- VSM Plast

- GE TandD India Limited

- Panel Builders India Pvt. Ltd.

- Admac Systems

- Ensto India Pvt. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging grid-modernization CAPEX by state utilities

- 4.2.2 Rising hyperscale data-centre build-outs

- 4.2.3 Mandatory fire-safety upgrades in public buildings (NBC-2016)

- 4.2.4 Rapid electrification of Indian Railways

- 4.2.5 'Production-Linked Incentive' (PLI) push for switch-gear localisation

- 4.2.6 Growth of rooftop-solar OandM ecosystem

- 4.3 Market Restraints

- 4.3.1 Steel and aluminium price volatility

- 4.3.2 Proliferation of counterfeit IP-rated products

- 4.3.3 Fragmented state-level certification regimes

- 4.3.4 Supply-chain bottlenecks for silicone gaskets

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Metallic

- 5.1.2 Non-metallic

- 5.2 By Form Factor

- 5.2.1 Wall-mount

- 5.2.2 Floor-mount / Free-standing

- 5.2.3 Junction / Terminal boxes

- 5.2.4 Modular / Custom

- 5.3 By Mounting Type

- 5.3.1 Indoor

- 5.3.2 Outdoor

- 5.4 By Application

- 5.4.1 Power Generation and Distribution

- 5.4.2 Transportation (Rail, Metro, Airports)

- 5.4.3 Oil and Gas

- 5.4.4 Commercial Buildings and Data Centres

- 5.4.5 Process Industries (FandB, Pharma, Chemicals)

- 5.4.6 Others Applications

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Schneider Electric SE

- 6.4.2 ABB Ltd.

- 6.4.3 Siemens AG

- 6.4.4 Eaton Corporation plc

- 6.4.5 Emerson Electric Co.

- 6.4.6 Legrand SA

- 6.4.7 Hubbell Incorporated

- 6.4.8 Rittal GmbH and Co. KG

- 6.4.9 BCH Electric Ltd.

- 6.4.10 Larsen and Toubro Limited

- 6.4.11 Trinity Touch Pvt. Ltd.

- 6.4.12 Fibox India Pvt. Ltd.

- 6.4.13 Boxco Industries Ltd.

- 6.4.14 Adswitch Limited

- 6.4.15 Pentair Technical Solutions India Pvt. Ltd.

- 6.4.16 VSM Plast

- 6.4.17 GE TandD India Limited

- 6.4.18 Panel Builders India Pvt. Ltd.

- 6.4.19 Admac Systems

- 6.4.20 Ensto India Pvt. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

电气外壳市场:按类型、安装配置、材质、最终用途产业和应用划分-2026-2032年全球市场预测电气柜及外壳市场:依材质、防护等级、额定电压、产品类型及最终用户产业划分-2026-2032年全球市场预测全球机柜冷却器市场按类型、冷却能力、机柜类型、安装方式、最终用途产业和分销管道划分,2026-2032年预测

电气外壳市场:按类型、安装配置、材质、最终用途产业和应用划分-2026-2032年全球市场预测电气柜及外壳市场:依材质、防护等级、额定电压、产品类型及最终用户产业划分-2026-2032年全球市场预测全球机柜冷却器市场按类型、冷却能力、机柜类型、安装方式、最终用途产业和分销管道划分,2026-2032年预测 美国电气机壳:市场份额分析、产业趋势与统计、成长预测(2026-2031)

美国电气机壳:市场份额分析、产业趋势与统计、成长预测(2026-2031) 电气外壳市场规模、份额、成长及全球产业分析:按类型、应用和地区划分,并提供 2026-2034 年的洞察和预测

电气外壳市场规模、份额、成长及全球产业分析:按类型、应用和地区划分,并提供 2026-2034 年的洞察和预测 2026年全球电气外壳市场报告不銹钢烘干柜市场按产品类型、材质等级、容量、价格范围、应用、终端用户产业和分销管道划分-2026-2032年全球预测电池外壳及机柜市场(依产品类型、安装类型、材料、电池类型、最终用户和应用划分)-全球预测,2026-2032年电气外壳:市场份额分析、行业趋势和统计数据、成长预测(2026-2031)

2026年全球电气外壳市场报告不銹钢烘干柜市场按产品类型、材质等级、容量、价格范围、应用、终端用户产业和分销管道划分-2026-2032年全球预测电池外壳及机柜市场(依产品类型、安装类型、材料、电池类型、最终用户和应用划分)-全球预测,2026-2032年电气外壳:市场份额分析、行业趋势和统计数据、成长预测(2026-2031) 塑胶外壳市场规模、份额和成长分析(按应用、最终用途产业、材质、配置类型、产业标准和地区划分)-2026-2033年产业预测

塑胶外壳市场规模、份额和成长分析(按应用、最终用途产业、材质、配置类型、产业标准和地区划分)-2026-2033年产业预测