|

市场调查报告书

商品编码

1940742

美国电气机壳:市场份额分析、产业趋势与统计、成长预测(2026-2031)United States Electrical Enclosures - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

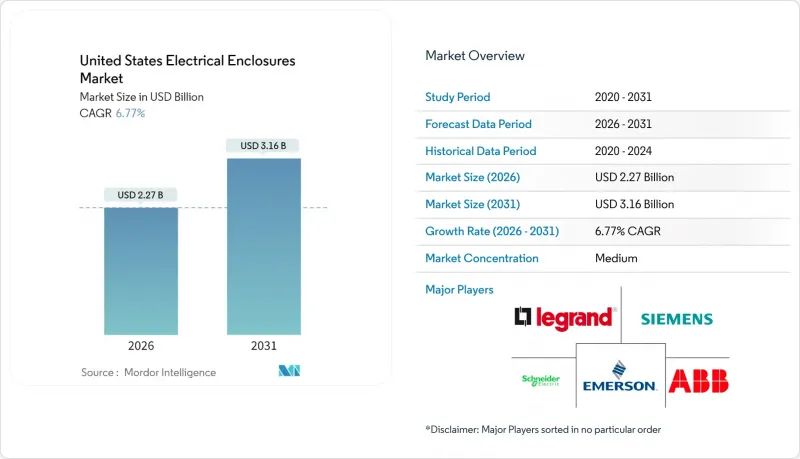

美国电气机壳市场预计将从 2025 年的 21.3 亿美元成长到 2026 年的 22.7 亿美元,预计到 2031 年将达到 31.6 亿美元,2026 年至 2031 年的复合年增长率为 6.77%。

对电网韧性、大型太阳能发电工程和电动卡车充电站的大力资本投资预计将推动两位数以上的持续需求成长。光是公用事业公司就已为输配电设备在2024年前拨款1,790亿美元,其中一部分资金直接用于购买防风雨和网路安全型机柜。每年299.9亿美元的资料中心建设投资正在改变对适用于高密度配电的自主型大容量机柜的需求结构。加州要求在2030年安装15.7万个中大型充电桩,这推动了对兆瓦级新型机壳的需求。这些基础设施发展趋势正在推动美国公共产业、可再生能源、交通运输和数位基础设施等领域的电气机壳市场潜力成长。

美国电气机壳市场趋势与洞察

美国电网加固计划资本投资激增

电力公司正在将五年资本计画增加235亿美元,其中光是PPL一家公司的预算就增加了40%,达到200亿美元。配电变电站的支出将在2023年达到61亿美元,是2003年以来的三倍多。每项维修都指定使用NEMA 4X或IP66防护等级的机柜,这些机柜既能保护智慧继电器,又能抵御风沙和水的侵蚀。增强的温度控管和电磁干扰屏蔽正成为基本要求,推高了平均售价。日益频繁的极端天气事件促使公共产业签订多年期机壳合同,从而为美国电气机壳市场提供了持续的订单。

公用事业规模太阳能发电厂和储能设施的快速扩张

美国国防部指南规范强制要求使用 NEMA 3R 汇流箱和 NEMA 4X 控制柜,额定温度范围为 -25°C 至 +57°C。储能阵列的要求更为严格,包括通风气体管理部分和密封电子设备舱,例如 Solar Electric Supply 的 Class I Div 2 系统。 1 兆瓦以上计划的激增推动了更大面积和模组化、可堆迭机壳的普及。德克萨斯州和佛罗里达州在采购方面处于领先地位,通常每吉瓦太阳能发电容量需要 15,000 至 20,000 个新外壳。这正推动美国电气机壳市场转向更大、预製组件和更高 IP 防护等级的方向。

钢铁和铝商品价格波动

对加拿大和墨西哥进口商品加征25%的新关税,导致钢製导管的平均成本在2025年3月前上涨了14%,而铝材短缺则推高了面板价格22%。中国4,500万吨的产量上限以及受旱灾影响的冶炼厂,导致全球溢价上涨,世界银行预测供应紧张的局面将持续到2025年。美国製造商面临的电价约为加拿大的两倍,并推高了加工成本。製造商正在合约中加入价格上涨条款,并增加原材料库存,这给营运资金带来了压力,预计短期内将限制美国电气机壳市场的成长。

细分市场分析

到2025年,金属机柜将占据美国电气机壳市场70.54%的份额,这主要得益于钢材的机械强度和铝材的电磁屏蔽性能。 316L等不銹钢牌号在船舶和食品加工行业的订单很大,而碳钢主导着大批量需求。非金属产品类别正以7.33%的复合年增长率成长,其中聚碳酸酯和玻璃纤维增强聚合物(GRP)机壳因其轻量化和防腐蚀性能而备受青睐。新兴的无线测量设备采用GRP来维持2.4 GHz讯号的保真度,从而拓展了其在工业物联网(IIoT)部署中的应用。

符合 NEMA 4X 和 IP68 防护等级的聚碳酸酯外壳正被广泛应用于沿海太阳能汇流阵列,其重量仅为钢製外壳的一半,却具备优异的紫外线稳定性和硅胶密封性能。原始设备製造商 (OEM) 非常重视其与 UL 508A 面板结构的兼容性,从而最大限度地减少设计变更过程中的摩擦。随着关税推高金属原料成本,价格竞争力日益增强,可应用领域也不断扩展。复合材料的持续多元化发展有望提高非金属产品的市场渗透率,并改变美国电气机壳市场未来的材料结构。

通用型或全尺寸(超过50公升)系统的出货量占总出货量的33.01%,这反映了分散式PLC和感测器在工厂中的重要角色。模组化或可配置系统的市场预计将以7.55%的复合年增长率成长,主要受变电站维修和资料中心配电盘需求成长的推动。人工智慧工作负载的不断增长将推动机架功率密度接近600kW,从而需要800V高压直流配电,这需要更大、温度控管的机壳。

在电力领域,整合继电器、电池和通讯设备的步入式控制室正被广泛采用,从而缩短了现场布线时间。模组化机柜系统允许随着负载的增加而安装额外的隔间,从而控制了资金预算。这种可扩展性巩固了大型产品的战略价值,推动了其在美国电气机壳市场收入份额的成长。

其他福利:

- Excel格式的市场预测(ME)表

- 分析师支持(3个月)

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 美国电网加固计划资本投资激增

- 公用事业规模太阳能发电厂和储能设施的快速扩张

- 商用车辆停车场的电气化

- 联邦政府对国内面板製造的税收优惠

- 人工智慧驱动的预测性维护机壳

- 具备网路安全功能的工业物联网机壳的需求日益增长

- 市场限制

- 钢铁和铝等大宗商品价格波动

- 2024-2025年非住宅建筑成长放缓

- UL 508A/NEMA 4X智慧型机壳认证成本高昂

- 金属机柜内无线感测器的互通性标准有限

- 产业价值链分析

- 监管环境

- 电气机壳标准

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 竞争对手之间的竞争

- 替代品的威胁

- 投资分析

第五章 市场规模与成长预测

- 依材料类型

- 由金属製成(碳钢、不銹钢、铝)

- 非金属材质(聚碳酸酯、玻璃纤维增强塑胶、聚酯、ABS树脂)

- 按外形规格

- 小型(小于10公升)

- 紧凑型(10-50公升)

- 均码/大尺寸(50公升或以上)

- 模组化/可配置系统

- 按安装类型

- 壁挂式

- 落地式/独立式

- 地下/基础类型

- 桿式安装

- 按最终用户行业划分

- 能源与电力

- 石油和天然气

- 工业製造与机器人

- 金属和采矿

- 交通运输(铁路、公路、航空、电动车充电)

- 资料中心和电信

- 食品、饮料和药品

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Schneider Electric SE

- ABB Ltd

- Eaton Corporation plc

- Hubbell Inc.

- nVent Electric plc

- Rittal GmbH and Co. KG

- Legrand SA

- Siemens AG

- Emerson Electric Co.

- Hammond Manufacturing Ltd.

- AZZ Inc.

- Adalet(Scott Fetzer Co.)

- Austin Electrical Enclosures, LLC

- Bison ProFab, Inc.

- Saginaw Control and Engineering, Inc.

- Stahlin Enclosures(Atkore Inc.)

- Allied Moulded Products, Inc.

- Pentair plc(Schroff)

- Integra Enclosures, LLC

- Fibox USA, LLC

第七章 市场机会与未来展望

The United States Electrical Enclosures Market is expected to grow from USD 2.13 billion in 2025 to USD 2.27 billion in 2026 and is forecast to reach USD 3.16 billion by 2031 at 6.77% CAGR over 2026-2031.

Robust capital outlays for grid resilience, utility-scale solar projects, and electric truck charging depots are converging to sustain double-digit unit demand. Utilities alone budgeted USD 179 billion in 2024 for transmission and distribution hardware, a spending pool that directly specifies weather-sealed, cyber-secure cabinets. Data center construction running at a USD 29.99 billion annual rate is shifting the mix toward free-standing, large-volume housings suited for high-density power distribution. California's mandate for 157,000 medium- and heavy-duty chargers by 2030 underpins a new class of megawatt-rated enclosures. These infrastructure themes collectively expand the addressable market for US electrical enclosures across utilities, renewables, transportation, and digital infrastructure.

United States Electrical Enclosures Market Trends and Insights

Surging CAPEX in U.S. Grid-Hardening Programs

Utility owners are boosting five-year capital plans by USD 23.5 billion, with PPL alone lifting its budget 40% to USD 20 billion. Distribution substation spend hit USD 6.1 billion in 2023, more than tripling 2003 levels. Each retrofit specifies NEMA 4X or IP66 cabinets able to endure wind-borne debris and flood exposure while sheltering smart relays. Enhanced thermal management and EMI shielding now form baseline requirements, pushing average selling prices higher. As extreme-weather events intensify, utilities are locking in multi-year enclosure contracts, giving the US electrical enclosures market durable order visibility.

Rapid Build-Out of Utility-Scale Solar and Storage Farms

Department of Defense guide specs obligate NEMA 3R combiner boxes and NEMA 4X control cabinets that tolerate -25 °C to +57 °C ranges. Storage arrays impose stricter demands, including vented gas management sections and sealed electronics bays, as illustrated by Class I Div 2 systems from Solar Electric Supply. The boom in projects above 1 MW is enlarging physical footprints, spurring uptake of modular, stackable enclosures. Texas and Florida are setting procurement pace, and each gigawatt of solar capacity typically translates to 15,000-20,000 new cabinets. Consequently, the US electrical enclosures market is pivoting toward larger, pre-engineered assemblies with higher ingress-protection ratings.

Commodity Price Volatility for Steel and Aluminum

New 25% tariffs on Canadian and Mexican inputs drove average steel conduit costs up 14% by March 2025, while aluminum shortages pushed panel prices 22% higher. China's output cap at 45 million tonnes and drought-hit smelters lift global premiums, and the World Bank expects tightness to persist through 2025. U.S. producers face power rates almost double those in Canada, inflating conversion costs. Manufacturers are inserting escalation clauses and carrying larger raw-material inventories, which strains working capital and tempers the US electrical enclosures market expansion over the near term.

Other drivers and restraints analyzed in the detailed report include:

- Electrification of Commercial Vehicle Depots

- Federal Tax Incentives for Domestic Panel Manufacturing

- Sluggish Non-Residential Construction in 2024-2025

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Metallic cabinets retained 70.54% command of the US electrical enclosures market in 2025, underpinned by steel's mechanical resilience and aluminum's EMI shielding. Stainless grades such as 316L headline offshore and food-processing orders, whereas carbon steel dominates volume buyers. The non-metallic cohort, expanding at 7.33% CAGR, features polycarbonate and glass-reinforced polymer housings that slash weight and eliminate corrosion. Emerging wireless instrumentation uses GRP to preserve 2.4 GHz signal fidelity, broadening utility in IIoT rollouts.

Polycarbonate boxes rated NEMA 4X and IP68 now serve coastal PV combiner arrays, delivering UV stability and silicone-gasket sealing at half the weight of steel. OEMs appreciate drop-in compatibility with UL 508A panel builds, minimizing redesign friction. As tariffs inflate metal input costs, price parity is approaching, expanding addressable applications. Continued diversification into composites promises to lift non-metallic penetration and reshape future material splits within the US electrical enclosures market.

Free-size or full-size (above 50 L) accounted for 33.01% of the shipments, mirroring distributed PLC and sensor duties in factories. Modular or configurable systems are projected to grow at a 7.55% CAGR, propelled by substation retrofits and data-center switchboards. AI workloads push rack power densities toward 600 kW, obliging 800 V HVDC distribution that demands bigger, thermally managed housings.

Utility segments adopt walk-in control shelters that bundle relays, batteries, and communications inside one structure, cutting field wiring time. Modular cabinet ecosystems let operators bolt incremental bays as loads grow, safeguarding capital budgets. This scalability theme cements the strategic value of large-format offerings and increases their revenue mix inside the US electrical enclosures market.

The United States Electrical Enclosures Market Report is Segmented by Material Type (Metallic, and Non-Metallic), Form Factor (Small, Compact, Free-Size, and Modular), Mounting Type (Wall-Mounted, Floor-Mounted, Underground, and Pole-Mounted), End-User Industry (Energy and Power, Oil and Gas, Industrial Manufacturing and Robotics, Data Centers and Telecom, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Schneider Electric SE

- ABB Ltd

- Eaton Corporation plc

- Hubbell Inc.

- nVent Electric plc

- Rittal GmbH and Co. KG

- Legrand SA

- Siemens AG

- Emerson Electric Co.

- Hammond Manufacturing Ltd.

- AZZ Inc.

- Adalet (Scott Fetzer Co.)

- Austin Electrical Enclosures, LLC

- Bison ProFab, Inc.

- Saginaw Control and Engineering, Inc.

- Stahlin Enclosures (Atkore Inc.)

- Allied Moulded Products, Inc.

- Pentair plc (Schroff)

- Integra Enclosures, LLC

- Fibox USA, LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging CAPEX in U.S. grid-hardening programs

- 4.2.2 Rapid build-out of utility-scale solar and storage farms

- 4.2.3 Electrification of commercial vehicle depots

- 4.2.4 Federal tax incentives for domestic panel manufacturing

- 4.2.5 AI-enabled predictive maintenance enclosures

- 4.2.6 Growing demand for cyber-secure IIoT ready enclosures

- 4.3 Market Restraints

- 4.3.1 Commodity price volatility for steel and aluminum

- 4.3.2 Sluggish non-residential construction in 2024-2025

- 4.3.3 High certification costs for UL 508A/NEMA 4X smart enclosures

- 4.3.4 Limited interoperability standards for wireless sensors inside metal cabinets

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Electrical Enclosure Standards

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Consumers

- 4.8.3 Threat of New Entrants

- 4.8.4 Intensity of Competitive Rivalry

- 4.8.5 Threat of Substitutes

- 4.9 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Metallic (Carbon Steel, Stainless Steel, Aluminum)

- 5.1.2 Non-metallic (Polycarbonate, Fiberglass, Polyester, ABS)

- 5.2 By Form Factor

- 5.2.1 Small (less than or equal to 10 L)

- 5.2.2 Compact (10-50 L)

- 5.2.3 Free-size / Full-size (above 50 L)

- 5.2.4 Modular / Configurable systems

- 5.3 By Mounting Type

- 5.3.1 Wall-mounted

- 5.3.2 Floor-mounted / Free-standing

- 5.3.3 Underground / Pad-mounted

- 5.3.4 Pole-mounted

- 5.4 By End-user Industry

- 5.4.1 Energy and Power

- 5.4.2 Oil and Gas

- 5.4.3 Industrial Manufacturing and Robotics

- 5.4.4 Metals and Mining

- 5.4.5 Transportation (Rail, Road, Air, EV-charging)

- 5.4.6 Data Centres and Telecom

- 5.4.7 Food and Beverage and Pharmaceuticals

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Schneider Electric SE

- 6.4.2 ABB Ltd

- 6.4.3 Eaton Corporation plc

- 6.4.4 Hubbell Inc.

- 6.4.5 nVent Electric plc

- 6.4.6 Rittal GmbH and Co. KG

- 6.4.7 Legrand SA

- 6.4.8 Siemens AG

- 6.4.9 Emerson Electric Co.

- 6.4.10 Hammond Manufacturing Ltd.

- 6.4.11 AZZ Inc.

- 6.4.12 Adalet (Scott Fetzer Co.)

- 6.4.13 Austin Electrical Enclosures, LLC

- 6.4.14 Bison ProFab, Inc.

- 6.4.15 Saginaw Control and Engineering, Inc.

- 6.4.16 Stahlin Enclosures (Atkore Inc.)

- 6.4.17 Allied Moulded Products, Inc.

- 6.4.18 Pentair plc (Schroff)

- 6.4.19 Integra Enclosures, LLC

- 6.4.20 Fibox USA, LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

电气外壳市场:按类型、安装配置、材质、最终用途产业和应用划分-2026-2032年全球市场预测电气柜及外壳市场:依材质、防护等级、额定电压、产品类型及最终用户产业划分-2026-2032年全球市场预测全球机柜冷却器市场按类型、冷却能力、机柜类型、安装方式、最终用途产业和分销管道划分,2026-2032年预测

电气外壳市场:按类型、安装配置、材质、最终用途产业和应用划分-2026-2032年全球市场预测电气柜及外壳市场:依材质、防护等级、额定电压、产品类型及最终用户产业划分-2026-2032年全球市场预测全球机柜冷却器市场按类型、冷却能力、机柜类型、安装方式、最终用途产业和分销管道划分,2026-2032年预测 印度电气外壳市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

印度电气外壳市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 电气外壳市场规模、份额、成长及全球产业分析:按类型、应用和地区划分,并提供 2026-2034 年的洞察和预测

电气外壳市场规模、份额、成长及全球产业分析:按类型、应用和地区划分,并提供 2026-2034 年的洞察和预测 2026年全球电气外壳市场报告不銹钢烘干柜市场按产品类型、材质等级、容量、价格范围、应用、终端用户产业和分销管道划分-2026-2032年全球预测电池外壳及机柜市场(依产品类型、安装类型、材料、电池类型、最终用户和应用划分)-全球预测,2026-2032年电气外壳:市场份额分析、行业趋势和统计数据、成长预测(2026-2031)

2026年全球电气外壳市场报告不銹钢烘干柜市场按产品类型、材质等级、容量、价格范围、应用、终端用户产业和分销管道划分-2026-2032年全球预测电池外壳及机柜市场(依产品类型、安装类型、材料、电池类型、最终用户和应用划分)-全球预测,2026-2032年电气外壳:市场份额分析、行业趋势和统计数据、成长预测(2026-2031) 塑胶外壳市场规模、份额和成长分析(按应用、最终用途产业、材质、配置类型、产业标准和地区划分)-2026-2033年产业预测

塑胶外壳市场规模、份额和成长分析(按应用、最终用途产业、材质、配置类型、产业标准和地区划分)-2026-2033年产业预测