|

市场调查报告书

商品编码

1937306

美国罐车运输:市场份额分析、行业趋势和统计数据、成长预测(2026-2031 年)United States Tank Trucking - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

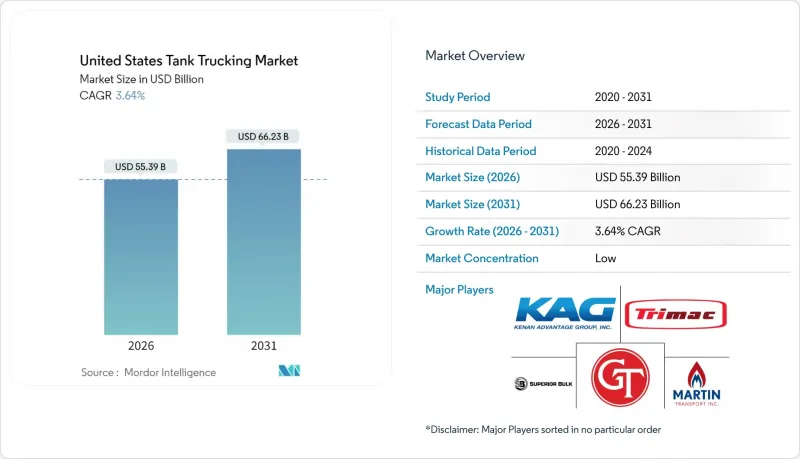

美国油轮运输市场预计到 2026 年将达到 553.9 亿美元,高于 2025 年的 534.5 亿美元。

预计到 2031 年将达到 662.3 亿美元,2026 年至 2031 年的复合年增长率为 3.64%。

这种持续扩张反映了其适应不断变化的能源结构、日益严格的安全法规以及波动的投入成本的能力。可再生柴油、特殊化学品和温控食品配料的运输量增加扩大了货物基础,而数位化调度工具和更轻的罐体配置则提高了资产利用率。同时,司机短缺、危险物品违规处罚以及自动驾驶卡车试验等挑战正在影响营运经济效益,迫使承运商重新评估路线规划、车队配置和资本规划。儘管面临这些挑战,美国罐车运输市场仍持续吸引私募股权资本,目前正在进行收购,以扩大合规基础并获得小众、高收益货物的运输权。

美国罐车运输市场趋势与洞察

对石油和精炼产品的需求不断增长

生质燃料生产的快速发展正在重塑石油物流路线,因为工厂需要可靠的原料「第一公里」运输和成品燃料「最后一公里」配送。预计到2035年,美国生质燃料日产量将达到130万桶,这趋势直接增加了对专用油轮的需求。墨西哥湾沿岸的炼油厂和西海岸的可再生柴油生产商依赖经过认证的油罐来运输高闪点燃料,这推动了船队升级,从而减轻了船舶的空载重量并加快了周转速度。加州修订后的低碳燃料标准要求承运商在2046年前扩大其运输的低碳燃料范围,这进一步推动了对保温专用设备的需求。高价值特种产品的溢价抵消了长途运输成本的增加,并有助于在全国柴油消费量逐步下降的情况下维持获利能力。

美国化学品生产规模扩大

在经历了2024年的短期萎缩之后,预计到2025年底,化学品产量将增加1.9%,这主要得益于工业需求的改善以及乙烷原料供应充足带来的运转率提高。来自美国沿岸地区和中西部工厂的乙烯、丙烯和特殊电池材料的运输正在推动始发地和目的地之间的重新调整,使得油轮运输比铁路运输更受青睐,以便及时将货物装入出口集装箱。石化生产商依靠专用承运商来最大限度地降低污染风险,并在沿海码头获得出口溢价。对半导体级化学品工厂的投资正在推动货物结构的进一步多元化,从而形成稳定的合约量,缓解炼油厂季节性波动的影响。

增加营业时间限制 (HOS) 和危险物质合规成本

美国联邦汽车运输安全管理局 (FMCSA) 的民事罚款大幅飙升,危险物品违规行为的罚款最高可达每次违规 102,348 美元。管道和危险物质安全管理局 (PHMSA) 对小型运输公司的註册费上涨了 50%,货罐检查不合格可能面临 8,000 美元的罚款。使用电子记录设备的数位化审核揭露了以往例行的调度问题,导致运转率下降。为了遵守法规,需要增加人手。无法负责人的小型企业被迫关闭或出售,这加速了行业整合,同时也减少了可用的运输能力。

细分市场分析

到2025年,石油产品将占总营收的46.30%,支撑美国罐车运输市场规模。这主要得益于炼油厂产能的强劲成长以及可再生柴油混合燃料市场的不断扩大。可再生燃料生产商倾向于使用特製不銹钢或铝製油桶来维持产品质量,从而增强了对长期合约的需求。食品饮料产业预计在2026年至2031年间实现4.24%的复合年增长率,成为成长最快的产业,这主要得益于乳製品现代化带来的运输距离延长以及饮料产品种类的增加。化学工业将继续保持其第二大收入驱动力的地位,这主要得益于美国沿岸地区的扩张以及中西部地区化肥产量的增加。化肥运输高峰出现在播种季节,导致现货运费大幅上涨,承运商会利用此机会调整区域间的运输流量。

加强低碳燃料标准 (LCFS) 正在推动对可再生原料物流的投资,并凸显生物基液体燃料的未来成长潜力。儘管从 2027 年起,随着可再生燃料的扩张,石油部分的市场份额可能会下降,但总运输量仍将持续增长,这表明燃料物流在美国罐车运输市场的重要性仍然不容忽视。同时,美国食品药物管理局 (FDA) 的食品安全法规赋予了特种运输公司定价权,使其能够在清洁设施成本不断上涨的情况下保障利润率。这些趋势共同建构了一个多元化的货物基础,从而缓解了单一商品运输线的週期性波动。

到2025年,重型卡车将占总收入的51.85%,装载率的提高将增加单次运输量并分散固定成本。 DOT-412标准的实施进一步扩大了负载容量范围,凸显了重型车辆在长途石化运输路线上的重要性。儘管轻型卡车市场规模较小,但由于都市区规划限制了大型拖车的通行,以及电商加油站对短週期、高频次加油的需求,预计2026年至2031年间,轻型卡车市场将以3.72%的复合年增长率实现最高增长。中型卡车则服务于危险物品运输这一细分市场,在该市场中,绕行有重量限制的桥樑比提高负载容量更为重要。

电气化试点计画主要集中在轻型车辆领域,因为其电池续航里程足以满足日常城市通勤需求,且重量减轻可弥补有效负载容量的减少;而氢燃料和液化天然气(LNG)则对希望在不牺牲负载容量的前提下延长续航里程的大型牵引车极具吸引力。这种技术差异化确保了所有容量等级的车辆都能走上清晰的成长道路,从而惠及设备製造商和车队营运商。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 对石油和精炼产品的需求不断增长

- 美国扩大化学品生产

- 食品级散装和液体运输的成长

- 液化天然气加註通道的开发

- 采用DOT-412标准油箱以提高负载容量

- 扩大可再生柴油和生质燃料的生产将加速特种油轮运输。

- 市场限制

- 遵守营业时间规定 (HOS) 和危险物品运输法规的成本增加

- 燃油价格波动

- 司机和技术人员严重短缺

- 恢復铁路罐车运输能力

- 价值/供应链分析

- 监管环境

- 技术展望

- 波特五力模型

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

- 新冠疫情与地缘政治事件的影响

第五章 市场规模与成长预测

- 按产品类型

- 原油

- 石油产品

- 化学品

- 食品/饮料

- 肥料

- 其他产品类型

- 按产能

- 轻型车辆

- 中型车辆

- 大型车辆

- 目的地

- 国内的

- 国际的

- 按运输距离

- 长途

- 短程交通

- 透过使用

- 住宅

- 商业的

- 工业的

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Kenan Advantage Group

- Trimac Transportation

- Groendyke Transport

- Superior Bulk Logistics

- Martin Transport

- Miller Transporters

- Dupre Logistics

- Eagle Transport

- Tankstar USA

- Florida Rock & Tank Lines

- Mission Petroleum Carriers

- Genox Transportation

- J&M Tank Lines

- CLI Transport

- Tidewater Transit

- Service Transport Company

- Andrews Logistics

- CTL Transportation

- Coastal Transport

- Viessman Trucking

第七章 市场机会与未来展望

United States Tank Trucking Market size in 2026 is estimated at USD 55.39 billion, growing from 2025 value of USD 53.45 billion with 2031 projections showing USD 66.23 billion, growing at 3.64% CAGR over 2026-2031.

The sustained expansion reflects the market's capacity to adapt to shifting energy mixes, stricter safety rules, and volatile input costs. Rising movements of renewable diesel, specialty chemicals, and temperature-controlled food ingredients are expanding the freight base, while digital dispatch tools and lighter tank specifications are pushing asset productivity higher. In parallel, driver shortages, hazmat compliance penalties, and disruptive pilot programs for autonomous trucks are pressuring operating economics and forcing carriers to re-evaluate route design, fleet mix, and capital plans. Despite these challenges, the United States tank trucking market continues to attract private equity capital, with acquisitions aimed at scaling compliance infrastructure and expanding access to niche, higher-margin cargoes.

United States Tank Trucking Market Trends and Insights

Rising Demand for Oil & Refined Products

Biofuel manufacturing momentum is redrawing petroleum logistics corridors as plants require dependable first-mile feedstock deliveries and last-mile finished fuel distribution. United States biofuel output is projected to reach 1.3 million barrels of oil equivalent per day by 2035, a trend that directly increases specialized tank requirements. Gulf Coast refiners and West Coast renewable diesel producers rely on tanks certified for elevated flash-point fuels, driving fleet upgrades that cut tare weight and speed turnarounds. California's updated Low-Carbon Fuel Standard compels carriers to handle a widening slate of low-carbon fuels through 2046, reinforcing demand for insulated, dedicated equipment. Higher-value specialty products pay premiums that offset longer haul distances, securing revenues even as total diesel consumption gradually declines nationwide.

Expansion of U.S. Chemical Production

After the brief 2024 contraction, chemical output is set to advance 1.9% by the end of 2025 as improved industrial demand and a favorable ethane feedstock gap lift utilization rates. Ethylene, propylene, and specialty battery materials moving from Gulf Coast and Midwest plants spur origin-destination realignment that favors tank trucks over rail for just-in-time export container stuffing. Petrochemical producers lean on dedicated carriers to minimize contamination risks and capture higher export premiums at coastal terminals. Investments in semiconductor-grade chemical plants further diversify the freight mix, creating steady contract carriage volumes that smooth seasonal refinery swings.

Tightening HOS & Hazmat Compliance Costs

FMCSA civil penalties have surged, with hazmat violations now costing up to USD 102,348 per count. PHMSA registration fees for small carriers rose 50%, while cargo-tank inspection failures can trigger USD 8,000 fines. Digital audits from electronic logging devices expose once-routine schedule adjustments, cutting utilization and requiring additional headcount to keep fleets legal. Smaller operators lacking compliance personnel are either exiting or selling, accelerating consolidation but trimming available capacity.

Other drivers and restraints analyzed in the detailed report include:

- Growth in Food-Grade Bulk/Liquid Shipping

- LNG Refueling Corridor Build-Out

- Acute Driver & Technician Shortages

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Petroleum products supplied 46.30% of 2025 revenue, underpinning the United States tank trucking market size with resilient refinery throughput and a growing renewable diesel blend pool. Renewable-fuel producers favor dedicated stainless or aluminum barrels to safeguard product integrity, reinforcing long-term contract demand. Food and beverages register the fastest 4.24% CAGR (2026-2031), supported by dairy modernization and beverage SKU proliferation that lengthen haul distances. Chemicals remain the second-largest revenue pillar, lifted by Gulf Coast expansion and Midwest fertilizer output. Fertilizer shipments peak around planting seasons yet drive pronounced spot-rate spikes that carriers exploit to balance regional flows.

Intensifying LCFS requirements steer investment toward renewable feedstock logistics, weighting future growth toward bio-derived liquids. The petroleum segment's share may ease post-2027 as renewable volumes scale, yet absolute barrels shipped continue to rise, underscoring the enduring role of fuels logistics in the United States tank trucking market. Meanwhile, FDA food-safety mandates grant specialized carriers pricing power, securing margins amid climbing wash-bay costs. Together, these trends cement a diverse cargo base that tempers cyclical swings in any single commodity line.

Heavy trucks generated 51.85% of 2025 revenue, benefitting from larger load factors that spread fixed costs over more gallons per trip. DOT-412 retrofits further expand payload windows, reinforcing the heavy-duty fleet's central role in long-haul petrochemical corridors. The light-duty bracket, though smaller, produces the strongest 3.72% CAGR (2026-2031) as urban zoning curbs large trailer access and e-commerce fuel stations demand shorter, more frequent replenishment cycles. Medium-duty assets fill hazmat niches where routing around weight-restricted bridges trumps load size.

Electrification pilots focus on the light-duty class because battery range suffices for daily metro loops, and weight savings offset cargo penalties. Conversely, hydrogen and LNG options appeal to heavy tractors seeking extended range without payload sacrifice. These technology splits assure all capacity classes retain defined growth paths, supporting equipment manufacturers as well as carriers.

The United States Tank Trucking Market Report is Segmented by Product Category (Crude Petroleum, Petroleum Products, Chemicals, Food and Beverages, Fertilizers, and Others), Capacity (Light Duty, Medium Duty, and Heavy Duty), Destination (Domestic and International), Distance (Long Haul and Short Haul), Application (Residential, Commercial, and Industrial). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Kenan Advantage Group

- Trimac Transportation

- Groendyke Transport

- Superior Bulk Logistics

- Martin Transport

- Miller Transporters

- Dupre Logistics

- Eagle Transport

- Tankstar USA

- Florida Rock & Tank Lines

- Mission Petroleum Carriers

- Genox Transportation

- J&M Tank Lines

- CLI Transport

- Tidewater Transit

- Service Transport Company

- Andrews Logistics

- CTL Transportation

- Coastal Transport

- Viessman Trucking

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand for Oil & Refined Products

- 4.2.2 Expansion of U.S. Chemical Production

- 4.2.3 Growth in Food-Grade Bulk/Liquid Shipping

- 4.2.4 LNG Refueling Corridor Build-Out

- 4.2.5 Adoption of Heavier-Payload DOT-412 Spec Tanks

- 4.2.6 Expansion of Renewable Diesel & Biofuel Production Accelerates Specialized Tank Moves

- 4.3 Market Restraints

- 4.3.1 Tightening HOS & Hazmat Compliance Costs

- 4.3.2 Fuel-Price Volatility

- 4.3.3 Acute Driver & Technician Shortages

- 4.3.4 Rail Tank-Car Capacity Rebound

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Impact of COVID-19 & Geo-Political Events

5 Market Size & Growth Forecasts

- 5.1 By Product Category

- 5.1.1 Crude Petroleum

- 5.1.2 Petroleum Products

- 5.1.3 Chemicals

- 5.1.4 Food and Beverages

- 5.1.5 Fertilizers

- 5.1.6 Other Product Categories

- 5.2 By Capacity

- 5.2.1 Light Duty

- 5.2.2 Medium Duty

- 5.2.3 Heavy Duty

- 5.3 Destination

- 5.3.1 Domestic

- 5.3.2 International

- 5.4 By Distance

- 5.4.1 Long Haul

- 5.4.2 Short Haul

- 5.5 By Application

- 5.5.1 Residential

- 5.5.2 Commercial

- 5.5.3 Industrial

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Kenan Advantage Group

- 6.4.2 Trimac Transportation

- 6.4.3 Groendyke Transport

- 6.4.4 Superior Bulk Logistics

- 6.4.5 Martin Transport

- 6.4.6 Miller Transporters

- 6.4.7 Dupre Logistics

- 6.4.8 Eagle Transport

- 6.4.9 Tankstar USA

- 6.4.10 Florida Rock & Tank Lines

- 6.4.11 Mission Petroleum Carriers

- 6.4.12 Genox Transportation

- 6.4.13 J&M Tank Lines

- 6.4.14 CLI Transport

- 6.4.15 Tidewater Transit

- 6.4.16 Service Transport Company

- 6.4.17 Andrews Logistics

- 6.4.18 CTL Transportation

- 6.4.19 Coastal Transport

- 6.4.20 Viessman Trucking

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

2026年全球拖车市场报告2026年全球混合动力卡车市场报告

2026年全球拖车市场报告2026年全球混合动力卡车市场报告 食品油轮市场:依罐体材质、容量范围及终端用户产业划分-2026-2032年全球预测

食品油轮市场:依罐体材质、容量范围及终端用户产业划分-2026-2032年全球预测 日本卡车市场规模、份额、趋势和预测:按车辆类型、负载容量、燃料类型、应用和地区划分,2026-2034年

日本卡车市场规模、份额、趋势和预测:按车辆类型、负载容量、燃料类型、应用和地区划分,2026-2034年 卡车市场-全球产业规模、份额、趋势、机会、预测:按等级、燃料类型、最终用户产业、地区和竞争格局划分,2021-2031年卡车后组合灯市场按技术、车辆类型、最终用途产业和分销管道划分,全球预测(2026-2032年)按重量等级、燃料类型、驱动方式、车队规模、应用领域、车辆类型和销售管道分類的平闆卡车市场-2026年至2032年全球预测

卡车市场-全球产业规模、份额、趋势、机会、预测:按等级、燃料类型、最终用户产业、地区和竞争格局划分,2021-2031年卡车后组合灯市场按技术、车辆类型、最终用途产业和分销管道划分,全球预测(2026-2032年)按重量等级、燃料类型、驱动方式、车队规模、应用领域、车辆类型和销售管道分類的平闆卡车市场-2026年至2032年全球预测 全球刚性水罐车市场:产业分析、规模、份额、成长、趋势与预测(2025-2032)

全球刚性水罐车市场:产业分析、规模、份额、成长、趋势与预测(2025-2032) 全球中型卡车市场

全球中型卡车市场 2025-2029年全球油轮市场

2025-2029年全球油轮市场