|

市场调查报告书

商品编码

1937432

汽车金属衝压:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Automotive Metal Stamping - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

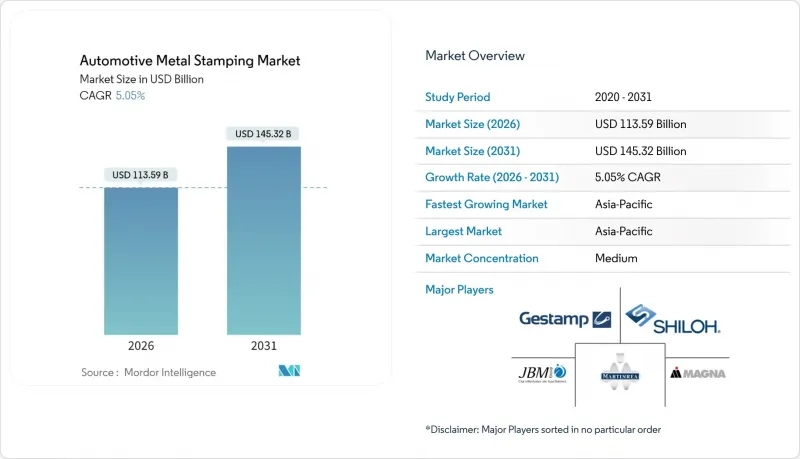

2025年汽车金属衝压市场价值为1,081.3亿美元,预计到2031年将达到1,453.2亿美元,而2026年为1,135.9亿美元。

预计在预测期(2026-2031 年)内,复合年增长率将达到 5.05%。

在车辆电气化程度不断提高、轻量化法规日益严格以及全球汽车产量稳步復苏的推动下,汽车金属衝压市场在乘用车和商用车领域依然保持强劲势头。冲压件是所有现代汽车车身结构、电池机壳和底盘模组的基础,因此,随着汽车製造商并行开发内燃机、混合动力和纯电动车架构,这项技术至关重要。儘管材料向铝和先进高抗拉强度钢 (AHSS) 的过渡仍在继续,但钢材具有成本优势和供应链熟悉度,这使得冲压製造商能够在生产恢復后迅速扩大生产规模。同时,热冲压和伺服压力机的应用使供应商能够在不牺牲尺寸精度的前提下,实现更薄的板材和更高的强度。随着汽车製造商要求数位双胞胎交货和可追溯性以支援空中下载 ( 在线连续) 车辆软体更新,整合数位孪生、线上视觉系统和封闭回路型控制系统正从测试线走向主流生产线。

全球汽车金属衝压市场趋势与洞察

汽车生产加速復苏(2025年及以后)

随着全球汽车组装量恢復到疫情前的峰值水平,冲压机製造商正在运作暂停中的压平机并加快模俱生产。现代钢铁计划在路易斯安那州新建的工厂将于2029年投产,每年供应数百万吨汽车用钢,并透过其电弧炼钢製程将碳排放强度降低五分之三。此次扩建将使区域生产线能够扩大电动车(EV)的产能。产能扩张表明,汽车金属衝压市场正在调整资本支出,以配合整车製造商(OEM)的新车型发布。供应商现在可以在同一台伺服冲压机上灵活生产高抗拉强度钢(AHSS)、传统钢材和铝坯,随着平台多样化,订单增长速度加快。这种柔软性将缩短新车型的前置作业时间是在整车製造商需要为软体定义汽车生产小批量、高频次的试生产批次时。

减轻车身重量以提高燃油效率并延长电动车续航里程

车辆减重每公斤都能提升车辆的整体燃油经济性,并延长电动车的续航里程。为此,冲压製造商目前正在试用一系列高抗拉强度钢(AHSS),其抗拉强度超过 1.2 GPa,同时保持良好的冷成形性能。安赛乐米塔尔和基尔霍夫汽车公司已展示了 Fortiform 系列钢材,其弯曲性能优于双相钢,无需额外的拉延加工即可实现更薄的壁厚。采用这些钢材製造的更薄的盖子、封盖和加强支架,持续为汽车金属衝压市场提供更轻、更强的零件。这项转变要求工厂购买大吨位伺服压力机和雷射切割机,以便对毛坯进行客製化焊接,从而在同一面板中组合不同厚度的部件。随着铝材应用的不断增长,一级供应商需要平衡其用于热处理 6xxx 系列合金的炉线,同时兼顾 AHSS 板材的酸洗和镀锌工序。

钢铁和铝价格波动

原物料价格波动会吞噬原本就微薄的利润,金属成本占冲压成本的五分之三以上。铝坯关税的提高(美国提案暗示将大幅提高关税税率)将对所有坯料供应商产生连锁反应,迫使一级供应商重新谈判年度定价条款。大型企业透过在商品交易所进行避险或与钢厂签订多年期合约锁定采购量来降低波动风险。汽车金属衝压市场的小型製造商则面临营运资金紧张的困境,促使他们透过联合采购池和联盟来增强自身的议价能力。

细分市场分析

到2025年,落料工序将占总收入的26.64%,这巩固了其在下游成型前将板材切割成近净成形坯料的核心地位。这一份额反映了汽车金属衝压市场规模持续依赖高速机械压力机进行平面模压成型。连续卷材生产线和在线连续表面检测确保了外板所需的尺寸精度。压花工序虽然规模较小,但其复合年增长率将达到5.11%,成为成长最快的工序,因为设计工作室需要无需二次装饰工序即可实现的纹理效果。

为了降低噪音、振动和不平顺性 (NVH),原始设备製造商 (OEM) 对阻尼肋和加强轮胎边缘的需求不断增长,推动了压花生产线的订单。高吨位压力机和可程式设计滑块运动装置能够在不减薄基材的情况下製造出深图案,从而满足碰撞安全标准。随着结构件变得越来越薄,压花製程可以提高局部刚度并减少厚度。因此,对伺服驱动压力机的投资使供应商能够在落料、压印和轻压花之间自由切换,从而在保持芯材落料产量的同时扩展其服务范围。这种方法使汽车金属衝压市场保持多元化和韧性。

到2025年,钣金成形将占总收入的42.62%,这表明传统级进模仍然是汽车金属衝压市场(尤其是大批量生产内装板和子组件)的基础。自动捲料送料器和快速晶粒模车最大限度地提高了设备正常运作,使供应商能够适应缩短的车型週期。热冲压的收入成长将相对滞后,但其复合年增长率将达到5.17%,这主要得益于电动车防撞梁应用对马氏体强度要求较高(约1.5 GPa)的驱动。

新型多区淬火控制炉有助于防止氢脆,而机器人真空转移技术则可减少氧化皮的堆积。一级供应商正在提供结合传统冲压机和热压机的平台组合,以满足寻求优化供应商结构的原始设备製造商 (OEM) 采购部门的需求。级进模和传送模系统对于支架和加强筋板的製造仍然至关重要。然而,伺服冲压机的改造正在突破高强度钢 (AHSS) 的成形极限,这表明技术正在逐步转型,从而支持汽车金属衝压市场的发展。

区域分析

预计到2025年,亚太地区将占全球收入的37.89%,并在2031年之前保持5.13%的强劲复合年增长率,这主要得益于中国汽车装配线的重启以及印度政策支持的本地化生产。在上海、广州、浦那和清奈等地的丛集中,伺服冲压机正在安装到位,用于生产国产电动车所需的高抗拉强度钢车顶横樑和热成型侧梁。政府对新能源汽车的激励措施帮助模具厂维持了本世纪末的订单订单,从而巩固了其在亚太地区汽车金属衝压市场的地位。

北美透过投资智慧工厂以及韩国和日本钢铁巨头的近岸外包策略,保持其技术优势。现代钢铁位于路易斯安那州的工厂向南部组装走廊供应卷材,缩短了物流距离,并减少了冲压件的碳排放。美国和墨西哥的一级供应商正在部署基于云端的製造执行系统(MES)平台,以将冲压机运转率与原始设备製造商(OEM)的生产计画同步,从而避免罚款、获得奖金,并提升汽车金属衝压市场的服务水平。

儘管人事费用高昂,欧洲仍保持创新优势。蒂森克虏伯材料加工欧洲公司位于斯图加特的工厂维修计划,将物联网感测器与人工智慧驱动的製程控制系统结合,以减少废弃物并改善预测性维护。欧盟基于车辆排放气体法规的轻量化指令,正在推动多材料连接技术的研发,并增强供应商的专业能力。虽然南美洲和中东及非洲地区的市场份额仍然不足,但CKD组装厂的扩张,特别是待开发区冲压机(用于皮卡和紧凑型SUV)的引入,正在为未来的成长铺平道路。

其他福利:

- Excel格式的市场预测(ME)表

- 分析师支持(3个月)

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 汽车生产復苏的扩大

- 促进减重(以提高燃油效率和电动车续航里程)

- 电动车热冲压电池机壳成长

- 中印汽车供应链快速復苏

- OEM巨型冲压体结构

- 利用闭合迴路数位双胞胎实现零缺陷冲压

- 市场限制

- 钢铁和铝价格波动

- 熟练的模具和工具製造人员短缺

- 伺服和液压压平机需要昂贵的资本投资

- 区域金属供应中断

- 价值/价值链分析

- 监管环境

- 技术展望

- 波特五力模型

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模及成长预测(价值(美元))

- 透过技术

- 空白

- 压花

- 铸币

- 翻边

- 弯曲

- 深画

- 其他的

- 透过流程

- 辊压成型

- 热压印

- 钣金加工

- 渐进式印刷加工

- 转印压机械加工

- 金属加工

- 其他的

- 按车辆类型

- 搭乘用车

- 轻型商用车

- 中型和重型商用车辆

- 材料

- 钢材

- 铝

- 其他的

- 透过使用

- 车身面板

- 传动和结构部件

- 排气系统部件

- 底盘和悬吊部件

- 其他的

- 按地区

- 北美洲

- 我们

- 加拿大

- 北美其他地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲国家

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 亚太其他地区

- 中东和非洲

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 土耳其

- 埃及

- 南非

- 其他中东和非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Magna International

- Gestamp Automocion

- Shiloh Industries

- Martinrea International

- JBM Group

- Aisin Seiki

- G-TEKT

- Tower International

- D&H Industries

- PDQ Tool & Stamping

- Alcoa

- American Industrial Company

- Manor Tool & Manufacturing

- Tempco Manufacturing

- Wisconsin Metal Parts

- Lindy Manufacturing

第七章 市场机会与未来展望

The Automotive Metal Stamping Market was valued at USD 108.13 billion in 2025 and estimated to grow from USD 113.59 billion in 2026 to reach USD 145.32 billion by 2031, at a CAGR of 5.05% during the forecast period (2026-2031).

Rising vehicle electrification, lightweighting mandates, and a steady rebound in global automobile output keep the automotive metal stamping market resilient across passenger and commercial vehicle programs. Stamped parts underpin every modern body structure, battery enclosure, and chassis module, making the technology indispensable as OEMs juggle internal-combustion, hybrid, and battery-electric architectures. Material migration toward aluminum and advanced high-strength steel (AHSS) continues, but steel dominates in cost and supply-chain familiarity, allowing stampers to scale volumes quickly whenever production rebounds. Simultaneously, hot-stamping and servo-press upgrades let suppliers achieve thinner gauges and higher strengths without sacrificing dimensional integrity. Integrated digital twins, inline vision systems, and closed-loop controls are moving from pilot lines to mainstream operations as automakers demand zero-defect delivery and traceability to support over-the-air vehicle software updates.

Global Automotive Metal Stamping Market Trends and Insights

Increasing Automobile Production Rebound (Post-2025)

Global vehicle assemblies are climbing pre-pandemic peaks, prompting stampers to reopen idled presses and accelerate tool builds. Hyundai Steel's planned Louisiana complex will deliver numerous automotive steel annually from 2029, cutting carbon intensity by three-fifths via electric-arc routes and positioning regional lines for higher electric-vehicle (EV) output . Capacity expansions illustrate how the automotive metal stamping market aligns capital spending with renewed OEM model launches. Suppliers can juggle AHSS, conventional grades, and aluminum blanks on the same servo press and win incremental orders as platforms diversify. Their flexibility shortens new-model lead times when OEMs request pilot lots for software-defined vehicles in smaller, more frequent batches.

Lightweighting Push for Better Fuel Economy & EV Range

Each kilogram removed from a vehicle lifts fleet fuel economy targets and lengthens EV range, so stampers now trial AHSS families that exceed 1.2 GPa while remaining cold-formable. ArcelorMittal and KIRCHHOFF Automotive validated Fortiform grades that surpass dual-phase steel bending metrics, enabling thinner gauges without extra draw-bead complexity . Down-gauged lids, closures, and reinforcement brackets created through such grades keep the automotive metal stamping market on course to supply lighter yet stronger parts. The transition forces shops to buy higher-tonnage servo presses and tailor-welded-blank lasers that marry dissimilar thicknesses inside one panel. Aluminum uptake runs parallel, so tier-ones must balance furnace lines for heat-treatable 6xxx alloys alongside pickling and galvanizing for AHSS sheets.

Volatile Steel & Aluminum Prices

Raw material swings can erase thin margins because metal outlays exceed three-fifths of stamping cost. Tariff hikes on aluminum billet-US proposals indicate rates climbing exponentially-would ripple across blank suppliers and push tier-ones to renegotiate annual price clauses. Larger players hedge on commodity exchanges or lock multi-year offtake with mills, cushioning volatility. Smaller shops within the automotive metal stamping market face working-capital strain, prompting joint-procurement pools or consortia to gain leverage.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Recovery of Chinese & Indian Auto Supply Chains

- OEM Adoption of Mega-Stamp Body Structures

- Shortage of Skilled Tool-and-Die Makers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Blanking captured 26.64% of 2025 revenue, underscoring its integral role in cutting sheet stock to net-shape blanks before downstream forming. This share illustrates how the automotive metal stamping market size still relies on high-speed mechanical presses for flat-pattern preparation. Continuous coil lines with inline surface inspection uphold the dimensional accuracy needed for outer panels. Embossing, although smaller, is registering the fastest 5.11% CAGR as design studios request textures that remove secondary decorative steps.

OEM requests for NVH damping ribs and stiffening beads lift embossing line orders. High-tonnage presses with programmable slide motions create deep patterns without thinning the base metal, meeting crashworthiness standards. As structures evolve toward fewer parts, embossing raises local stiffness, allowing gauge reduction. Consequently, capital outlays in servo-driven presses ensure suppliers can toggle among blanking, coining, and light embossing, expanding service menus while retaining core blanking volumes. This approach keeps the automotive metal stamping market diversified but resilient.

Sheet-metal forming contributed 42.62% of 2025 turnover, proving that traditional progressive dies still anchor the automotive metal stamping market share for high-volume inner panels and sub-assemblies. Automated coil feeds and quick-die-change carts maximize uptime, letting suppliers meet compressed model cycles. Hot-stamping trails in revenue but shows the strongest 5.17% CAGR, driven by EV crash-rail applications that require martensitic strengths near 1.5 GPa.

New furnaces with multi-zone quench control help prevent hydrogen embrittlement, and robotic vacuum transfer limits scale build-up. Tier-ones offering conventional and hot-stamping win platform bundles from OEM purchasing teams looking to rationalize supplier counts. Progressive-die and transfer-die systems remain essential for brackets and reinforcement plates. Still, servo-press retrofits lift, forming limits on AHSS sheets and illustrating the incremental technology migration sustaining the automotive metal stamping market.

The Automotive Metal Stamping Market Report is Segmented by Technology (Blanking, Embossing, and More), Process (Roll Forming, Hot Stamping, and More), Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), Material (Steel and More), Application (Body Panels, Transmission & Structural Components, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific commanded 37.89% of global revenue in 2025 and is growing at a robust CAGR of 5.13% through 2031, aided by China's restart of assembly lines and India's policy-backed localization drives. Clusters around Shanghai, Guangzhou, Pune, and Chennai attract servo-press installations, enabling output of AHSS roof rails and hot-stamped side-sills for domestic EV models. Government incentives for new-energy vehicles ensure sustained tool-shop backlogs through the decade-end, bolstering the region's automotive metal stamping market presence.

North America maintains technology leadership through investments in smart-factory upgrades and near-shoring by Korean and Japanese steel majors. Hyundai Steel's Louisiana plant will supply coil stock for southern assembly corridors, shortening logistics and lowering embodied carbon in stamped parts. U.S. and Mexican tier-ones adopt cloud-MES platforms to synchronize press uptime with OEM production sequencing, capturing penalty-avoidance bonuses while elevating service levels within the automotive metal stamping market.

Europe sustains an innovation edge despite high labor costs. Projects like thyssenkrupp Materials Processing Europe's Stuttgart upgrade link IoT sensors to AI-driven process control, slashing scrap and raising predictive maintenance accuracy. Lightweighting directives under EU fleet targets channel R&D toward multi-material joining, reinforcing supplier know-how. South America, the Middle East, and Africa remain smaller contributors. Still, rising CKD assembly hubs usher in greenfield presses, particularly for pickup trucks and compact SUVs, setting the stage for future gains.

- Magna International

- Gestamp Automocion

- Shiloh Industries

- Martinrea International

- JBM Group

- Aisin Seiki

- G-TEKT

- Tower International

- D&H Industries

- PDQ Tool & Stamping

- Alcoa

- American Industrial Company

- Manor Tool & Manufacturing

- Tempco Manufacturing

- Wisconsin Metal Parts

- Lindy Manufacturing

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Automobile Production Rebound

- 4.2.2 Lightweighting Push For Better Fuel Economy & EV Range

- 4.2.3 Growth Of Hot-Stamped Battery Enclosures In EVs

- 4.2.4 Rapid Recovery Of Chinese & Indian Auto Supply Chains

- 4.2.5 OEM Adoption Of Mega-Stamp Body Structures

- 4.2.6 Closed-Loop Digital Twins Enabling Zero-Defect Stamping

- 4.3 Market Restraints

- 4.3.1 Volatile Steel & Aluminum Prices

- 4.3.2 Shortage Of Skilled Tool-And-Die Makers

- 4.3.3 High Cap-Ex For Servo & Hydraulic Presses

- 4.3.4 Regional Metal Supply Disruptions

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD))

- 5.1 By Technology

- 5.1.1 Blanking

- 5.1.2 Embossing

- 5.1.3 Coining

- 5.1.4 Flanging

- 5.1.5 Bending

- 5.1.6 Deep Drawing

- 5.1.7 Others

- 5.2 By Process

- 5.2.1 Roll Forming

- 5.2.2 Hot Stamping

- 5.2.3 Sheet-Metal Forming

- 5.2.4 Progressive-Die Stamping

- 5.2.5 Transfer-Die Stamping

- 5.2.6 Metal Fabrication

- 5.2.7 Others

- 5.3 By Vehicle Type

- 5.3.1 Passenger Cars

- 5.3.2 Light Commercial Vehicles

- 5.3.3 Medium and Heavy Commercial Vehicles

- 5.4 By Material

- 5.4.1 Steel

- 5.4.2 Aluminum

- 5.4.3 Others

- 5.5 By Application

- 5.5.1 Body Panels

- 5.5.2 Transmission and Structural Components

- 5.5.3 Exhaust Components

- 5.5.4 Chassis and Suspension Parts

- 5.5.5 Others

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle-East and Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 Turkey

- 5.6.5.4 Egypt

- 5.6.5.5 South Africa

- 5.6.5.6 Rest of Middle-East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Magna International

- 6.4.2 Gestamp Automocion

- 6.4.3 Shiloh Industries

- 6.4.4 Martinrea International

- 6.4.5 JBM Group

- 6.4.6 Aisin Seiki

- 6.4.7 G-TEKT

- 6.4.8 Tower International

- 6.4.9 D&H Industries

- 6.4.10 PDQ Tool & Stamping

- 6.4.11 Alcoa

- 6.4.12 American Industrial Company

- 6.4.13 Manor Tool & Manufacturing

- 6.4.14 Tempco Manufacturing

- 6.4.15 Wisconsin Metal Parts

- 6.4.16 Lindy Manufacturing

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

汽车底盘冲压件市场按製程类型、材料类型、车辆类型、应用和最终用户划分,全球预测,2026-2032年汽车座椅靠背冲压件市场:按材质、製造流程、车辆类型、应用和最终用户划分 - 全球预测 2026-2032

汽车底盘冲压件市场按製程类型、材料类型、车辆类型、应用和最终用户划分,全球预测,2026-2032年汽车座椅靠背冲压件市场:按材质、製造流程、车辆类型、应用和最终用户划分 - 全球预测 2026-2032 汽车冲压机自动化市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)

汽车冲压机自动化市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年) 汽车金属冲压加工市场评估:车辆类型·技术·流程·各地区的机会及预测 (2018-2032年)

汽车金属冲压加工市场评估:车辆类型·技术·流程·各地区的机会及预测 (2018-2032年) 汽车金属冲压市场 - 全球产业规模、份额、趋势、机会和预测,按车型、技术、工艺、地区和竞争细分,2019-2029F

汽车金属冲压市场 - 全球产业规模、份额、趋势、机会和预测,按车型、技术、工艺、地区和竞争细分,2019-2029F 到 2030 年汽车金属衝压市场预测:按工艺、车型和地区进行全球分析

到 2030 年汽车金属衝压市场预测:按工艺、车型和地区进行全球分析 汽车金属冲压市场,按技术、按工艺、按车型、按国家和地区划分 - 2024-2032 年行业分析、市场规模、市场份额和预测

汽车金属冲压市场,按技术、按工艺、按车型、按国家和地区划分 - 2024-2032 年行业分析、市场规模、市场份额和预测 汽车金属衝压市场规模、份额、趋势分析报告:按製程、按应用、按地区、细分市场预测,2025-2030

汽车金属衝压市场规模、份额、趋势分析报告:按製程、按应用、按地区、细分市场预测,2025-2030