|

市场调查报告书

商品编码

1938995

欧洲纸包装市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031年)Europe Paper Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

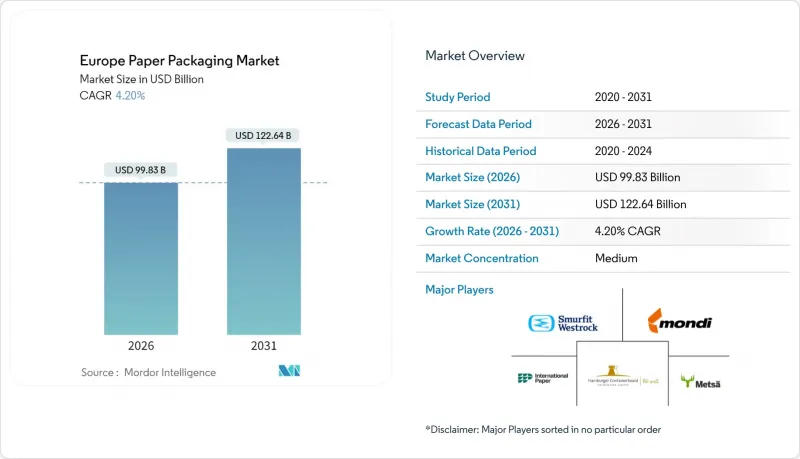

欧洲纸包装市场预计将从 2025 年的 958.1 亿美元成长到 2026 年的 998.3 亿美元,预计到 2031 年将达到 1226.4 亿美元,2026 年至 2031 年的复合年增长率为 4.20%。

该市场的成长主要受以下因素驱动:欧洲大陆监管模式向循环经济模式转变、零售商普遍偏好路边回收方式,以及高强度瓦楞纸板基材技术的持续创新。由于纤维基解决方案碳排放强度低且易于回收(ISO 14040 生命週期评估已证实这一点),它们正日益取代塑料,应用于餐饮服务、电子商务和食材自煮包等领域。对再生纸板产能的上游投资,尤其是在北欧造纸厂的投资,降低了原料风险,同时使供应商能够遵守欧盟碳边境调节机制。积极的併购活动,包括 Smurfit 和 Westrock 于 2024 年的合併,加剧了竞争并加速了垂直整合,使主要企业能够确保原生和再生纤维的供应,优化运输成本,并在欧洲范围内对其基本客群进行标准化的永续采购审核。能源价格波动带来的短期投入成本压力正在挤压利润空间。然而,下游需求仍然强劲,因为线上零售的普及、快速交易的便利性以及对一次性塑胶製品日益严格的禁令共同推动了包装需求的成长。

欧洲纸包装市场趋势与洞察

食品饮料产业对永续和可回收包装的需求不断增长

欧洲食品饮料品牌承诺在2030年实现100%包装可回收的目标,并引入了优先选择纤维材料而非多层塑胶的采购标准。大型零售商正在推行货架即用标准,并优先选用单一材料纤维托盘,例如玛莎百货(Marks & Spencer)于2025年5月推出的纸纤维调理食品托盘。酒厂和啤酒厂也推出了旗舰产品,例如采用90%纸质材料製成的苏格兰威士忌酒瓶,进一步强化了消费者对纸张环境影响低的认知。一项针对巧克力棒包装纸的生命週期研究证实,在所有中间类别中,纸张的温室气体排放量均低于定向聚丙烯(OPP)。包装加工商正加强与涂层技术供应商的合作,以使产品重新设计与品牌所有者的公开永续发展蓝图图保持一致,为即将于2026年8月生效的25 ppb PFAS限值做好准备。随着ISO 14040合规性成为跨境集中采购竞标的强制性要求,拥有检验的生产流程数据(从摇篮到大门)的纸品解决方案供应商将在跨国食品饮料集团中获得优先供应商地位。

电子商务小包裹量快速成长

欧洲线上零售额持续以两位数的速度成长,推动了履约中心纸箱和二次缓衝材料数量的快速成长。随着全通路食品零售商和专卖零售商加强分销网络,英国的纸板消耗量在2010年至2024年间增加了12.6%。亚马逊报告称,自2018年以来,该公司已在其欧洲业务中逐步淘汰了超过10亿个一次性塑胶运输袋,并在2025年1月前全面采用100%可再生纸袋和纸板信封。自动化尺寸最佳化包装设备,例如Mondi和CMC Packaging Automation共同开发的解决方案,可按需产生纸箱尺寸,在提高卡车装载效率的同时,减少高达40%的纸张用量。预计都市区生鲜速递市场将从2021年的250亿欧元快速成长至2025年的720亿欧元,这将需要尺寸优化的二次包装,以确保产品在10分钟内时限并保持完整性。因此,加工商优先考虑高速模切、用于客製化的数位印刷和在线连续品管感测器,以满足电子商务企业对大规模生产和品牌柔软性的要求。

对森林砍伐和原物料供应不稳定的担忧

将于2025年生效的欧盟森林砍伐法规要求对森林地块进行地理位置追溯,由于加工商采用卫星检验和区块链帐本,采购成本将增加3-5%。斯堪的纳维亚半岛的锯木厂正因电价飙升和频繁停工而面临营运运作,原生纸浆供应紧张,迫使买家在现货市场支付溢价。比勒鲁德的生产力提升计画凸显了整个产业应对纸浆价格上涨和原材料短缺造成的利润压力的紧迫性。小麦秸秆和芒草等替代纤维在模塑纤维食品容器中越来越受欢迎,但纤维长度和白度的差异限制了它们在高解析度印刷包装中的应用。向伊比利亚半岛和波罗的海沿岸森林进行地理多元化投资,既降低了集中风险,又延长了物流链,部分抵消了碳足迹的减少。从中长期来看,该工厂正在加快其封闭式水循环和植树造林工作,以向相关人员提供保证,并遵守日益严格的实质审查审核。

细分市场分析

2025年,瓦楞纸箱将占总收入的37.92%,凸显其在履约、工业和食品杂货分销管道的领先地位。由于电子商务小包裹的快速增长、对定製印刷的需求以及在不影响抗压强度的前提下不断推进的轻量化技术,预计欧洲瓦楞纸箱纸包装市场规模将稳步增长。受乳类饮料替代品、常温果汁系列以及品牌主导为减少多层塑胶排放而采取的倡议的推动,液体纸盒的增长率将达到最高,到2031年将达到5.12%的复合年增长率。

折迭纸盒等二次产品在药品泡壳包装和注重精准摺痕和光泽涂层以达到展示效果的高端个人保健产品包装中仍将发挥重要作用。由于全国禁止使用一次性塑胶袋,纸袋和零售袋的需求正在回升。杂货店越来越多地转向使用添加了防潮剂的牛皮纸製品,这些添加剂使其在重复使用时更加耐用。一些专业细分市场(例如防撕裂冷冻袋、模塑纤维托盘和模塑纸浆缓衝材料)正在扩大产能,但瓦楞纸仍然是支撑全部区域加工厂工厂使用率和资本投资合理性的核心产品。

到2025年,再生纸的市占率将达到55.98%,这得益于严格的消费后回收率目标以及为国内造纸厂提供充足原料的完善回收系统。随着碳边境调节机制(CBAM)的实施,原生纸的进口成本高于低碳再生纸,预计再生纸在欧洲纸包装市场的份额将进一步扩大。高品质的白色顶测试衬纸因其表面可印刷,在展示盒中越来越受欢迎,而棕色测试衬纸则在标准运输纸箱中占据主导地位。

对于高端化妆品礼盒、医疗设备手册和折迭纸盒等产品而言,原生纸浆基材仍然至关重要,因为它们需要极高的印刷精准度和优异的挺度。带有分散或挤出隔离层的复合纸板则介于两者之间,满足了水蒸气和油污防护的需求,但由于全氟烷基和多氟烷基物质(PFAS)逐步淘汰的风险,其近期扩张受到限制。采用双原料采购策略,即结合斯堪地那维亚软木牛皮纸和伊比利亚桉木硬木,以平衡强度和光滑度,正逐渐成为供应链的主流。造纸厂正与零售商建立循环伙伴关係,从配销中心回收旧瓦楞纸板(OCC),从而缩短循环时间,并确保食品级再生材料所需的原料纯度。

其他福利:

- Excel格式的市场预测(ME)表

- 分析师支持(3个月)

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 食品饮料产业对永续和可回收包装的需求不断增长

- 电子商务小包裹量快速成长

- 欧盟一次性塑胶指令加速纤维替代

- 轻质高强度瓦楞纸板技术的进步

- 食材自煮包和快速零售的成长推动了对合适尺寸包装的需求。

- 欧盟碳边境调节机制促进了回收工厂的发展

- 市场限制

- 森林砍伐问题与原料供应波动

- 由于可回收性的提高,柔软性塑胶的优势正在减弱。

- 能源价格快速上涨增加了造纸厂的营运成本。

- 阻隔涂布纸中 PFAS 逐步淘汰的不确定性

- 产业价值链分析

- 监管环境

- 技术展望

- 宏观经济因素如何影响市场

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 依产品类型

- 折迭纸箱

- 瓦楞纸箱

- 纸袋和纸袋

- 液体纸盒

- 其他纸包装

- 依材料类型

- 原生纸浆纸

- 再生纸

- 复合纸板

- 按最终用户行业划分

- 食物

- 饮料

- 医疗和药品

- 个人护理及家居用品

- 电子商务与零售

- 烟草

- 其他终端用户产业

- 按包装类型

- 初级包装

- 二级包装

- 三级包装

- 按国家/地区

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 荷兰

- 其他欧洲地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Smurfit WestRock

- Mondi plc

- International Paper Company

- Stora Enso Oyj

- Svenska Cellulosa Aktiebolaget SCA

- Metsa Board Oyj

- Mayr-Melnhof Karton AG

- Prinzhorn Holding GmbH

- Progroup AG

- Schumacher Packaging GmbH

- Klingele Papierwerke GmbH & Co. KG

- Graphic Packaging Holding Company

- RAJA Groupe

- VPK Packaging Group NV

- RDM Group(Reno De Medici SpA)

- Lucart SpA

- Essity AB

- Palm GmbH & Co. KG

第七章 市场机会与未来展望

The Europe paper packaging market is expected to grow from USD 95.81 billion in 2025 to USD 99.83 billion in 2026 and is forecast to reach USD 122.64 billion by 2031 at 4.20% CAGR over 2026-2031.

The market gains momentum from the continent's regulatory shift toward circular economy models, widespread retailer preference for curbside-recyclable formats, and continuous technology upgrades in high-strength corrugated substrates. Fiber-based solutions increasingly displace plastic in food service, e-commerce, and meal-kit applications because they combine ease of recycling with lower carbon intensity confirmed in ISO 14040 life-cycle assessments. Upstream investments in recycled-content board capacity, especially at Nordic mills, mitigate raw-material risk while positioning suppliers for EU Carbon Border Adjustment Mechanism compliance. Heightened merger activity, including the 2024 Smurfit-WestRock combination, tightens competition and accelerates vertical integration, allowing majors to secure virgin and recycled fiber supplies, optimize freight costs, and standardize sustainable sourcing audits across pan-European customer bases. Near-term input-cost headwinds linked to energy volatility squeeze margins; nevertheless, downstream demand remains resilient because online retail penetration, quick-commerce convenience, and increasingly stringent single-use-plastic bans jointly lift packaging volumes.

Europe Paper Packaging Market Trends and Insights

Rising demand for sustainable and recyclable packaging in Food and Beverage

European food and beverage brands publicly commit to 100% recyclable packaging targets for 2030, prompting procurement scorecards that prioritize fiber over multilayer plastics. Leading grocers impose shelf-readiness criteria that reward mono-material fiber trays, as shown by Marks & Spencer's rollout of paper-fiber ready-meal trays in May 2025. Distillers and brewers showcase flagship launches such as a 90% paper bottle for Scotch whisky, reinforcing consumer perception that paper embodies lower environmental impact. Life-cycle studies covering chocolate bar wrappers confirm lower greenhouse-gas footprints for paper against oriented polypropylene in every midpoint category. Packaging converters intensify collaboration with coating-technology suppliers to meet upcoming 25 ppb PFAS limits in August 2026, aligning product reformulations with brand owners' public sustainability roadmaps. As ISO 14040 compliance becomes mandatory for cross-border central procurement tenders, paper solutions with verified cradle-to-gate data sets gain preferred-supplier status across multinational F&B groups.

Rapid surge in e-commerce parcel volumes

European online retail purchases maintain double-digit growth, fueling a steep rise in box counts and ancillary cushioning across fulfillment centers. Corrugated consumption in the United Kingdom increased 12.6% between 2010 and 2024 as omnichannel grocers and specialty retailers upgraded distribution networks. Amazon reports the elimination of more than 1 billion single-use plastic mailers since 2018 by converting its European operations to 100% recyclable paper pouches and board envelopes in January 2025. Automated right-size packaging equipment, such as solutions codeveloped by Mondi and CMC Packaging Automation, generates on-demand box dimensions that cut paper use up to 40% while improving truck-cubic-utilization metrics. Urban grocery quick-commerce, projected to jump from EUR 25 billion in 2021 to EUR 72 billion by 2025, requires dimensionally optimized secondary packs that preserve product integrity in 10-minute delivery windows. Consequently, converters prioritize high-speed die-cutting, digital print customization, and inline quality-control sensors to meet both volume scale and branding agility demanded by e-commerce merchants.

Deforestation concerns and raw-material supply volatility

The EU Deforestation Regulation, effective 2025, mandates traceability back to geolocated forest plots, adding 3-5% to procurement overhead as converters implement satellite verification and blockchain ledgers. Nordic sawmill capacity interruptions, stemming from electricity-cost surges and periodic labor stoppages, and thin virgin-fiber availability, are forcing buyers to tap spot markets at premium prices. Billerud's productivity program underscores industry-wide urgency to offset margin compression arising from pulp price spikes and raw-material scarcity. Alternative fibers such as wheat straw and miscanthus attract attention for molded-fiber food bowls, yet inconsistent fiber length and brightness curtail adoption for high-definition print packs. Geographic diversification toward Iberian and Baltic forests mitigates concentration risk but extends logistics chains, partially reversing carbon-footprint gains. Over the medium term, mills expedite closed-loop water systems and reforestation commitments to reassure stakeholders and comply with tightening due diligence audits.

Other drivers and restraints analyzed in the detailed report include:

- EU Single-Use Plastics Directive accelerating fiber substitution

- Advancements in lightweight, high-strength corrugated technology

- Improving recyclability of flexible plastics narrowing advantage

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Corrugated boxes held 37.92% of 2025 revenue, underscoring their status as the workhorse format across fulfillment, industrial, and grocery distribution channels. Europe's paper packaging market size for corrugated boxes is projected to compound steadily, given e-commerce parcel proliferation, customized print runs, and continuous lightweighting gains that lower freight emissions without forfeiting crush strength. Liquid cartons post the fastest 5.12% CAGR through 2031, propelled by dairy-alternative beverages, shelf-stable juice lines, and brand-led commitments to curb multilayer plastics usage.

Secondary products such as folding cartons maintain relevance for pharmaceutical blister overwraps and high-graphic personal-care packs where precise creasing and glossy varnishes create shelf appeal. Paper sacks and retail bags regain momentum as national bans phase out single-use plastic carriers, with grocers switching to kraft options featuring wet-strength additives for reuse durability. Specialty niches-tear-resistant freezer bags, shaped formed-fiber trays, and molded-pulp void-fill expand addressable volumes, yet corrugated remains the anchor that underpins converter plant utilization rates and capex justification across the region.

Recycled grades captured 55.98% share in 2025, an outcome of stringent post-consumer content targets and robust collection systems that feed domestic mills. Europe paper packaging market share for recycled liner is expected to widen as CBAM makes imports of virgin grades more expensive relative to low-carbon recycled sheet. High-quality white-top testliner gains favor in display-ready cases requiring printable surfaces, while brown testliner dominates standard shipping cartons.

Virgin-fiber substrates remain indispensable for premium cosmetics gift boxes, medical device manuals, and folding cartons demanding pristine print fidelity and superior stiffness. Composite paperboard featuring dispersion or extrusion barriers occupies a middle ground where water-vapor and fat resistance are critical, yet PFAS-phase-out risk tempers near-term expansion. Supply chains gravitate toward dual-sourcing strategies, combining Scandinavian softwood kraft with Iberian eucalyptus hardwood to balance strength and smoothness. Mills engage in circularity partnerships with retailers to backhaul OCC (old corrugated containers) from distribution centers, shortening loop time and securing feedstock purity levels imperative for food-grade recycled content.

The Europe Paper Packaging Market Report is Segmented by Product Type (Folding Cartons, Corrugated Boxes, Paper Bags and Sacks, and More), Material Type (Virgin Fiber Paper, and More), End-User Industry ( Healthcare and Pharmaceutical, Personal Care and Household, and More), Packaging Format (Primary Packaging, Secondary Packaging, and Tertiary Packaging), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Smurfit WestRock

- Mondi plc

- International Paper Company

- Stora Enso Oyj

- Svenska Cellulosa Aktiebolaget SCA

- Metsa Board Oyj

- Mayr-Melnhof Karton AG

- Prinzhorn Holding GmbH

- Progroup AG

- Schumacher Packaging GmbH

- Klingele Papierwerke GmbH & Co. KG

- Graphic Packaging Holding Company

- RAJA Groupe

- VPK Packaging Group NV

- RDM Group (Reno De Medici S.p.A.)

- Lucart S.p.A.

- Essity AB

- Palm GmbH & Co. KG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for sustainable and recyclable packaging in FandB

- 4.2.2 Rapid surge in e-commerce parcel volumes

- 4.2.3 EU Single-Use Plastics Directive accelerating fiber substitution

- 4.2.4 Advancements in lightweight, high-strength corrugated technology

- 4.2.5 Growth of meal-kit and quick-commerce requiring right-sized packs

- 4.2.6 EU Carbon Border Adjustment Mechanism driving recycled mills

- 4.3 Market Restraints

- 4.3.1 Deforestation concerns and raw material supply volatility

- 4.3.2 Improving recyclability of flexible plastics narrowing advantage

- 4.3.3 Energy-price shocks raising mill operating costs

- 4.3.4 PFAS-phase-out uncertainty in barrier-coated papers

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECAST (VALUE)

- 5.1 By Product Type

- 5.1.1 Folding Cartons

- 5.1.2 Corrugated Boxes

- 5.1.3 Paper Bags and Sacks

- 5.1.4 Liquid Cartons

- 5.1.5 Other Paper Packaging

- 5.2 By Material Type

- 5.2.1 Virgin Fiber Paper

- 5.2.2 Recycled Paper

- 5.2.3 Composite Paperboard

- 5.3 By End-user Industry

- 5.3.1 Food

- 5.3.2 Beverage

- 5.3.3 Healthcare and Pharmaceutical

- 5.3.4 Personal Care and Household

- 5.3.5 E-commerce and Retail

- 5.3.6 Tobacco

- 5.3.7 Other End-user Industries

- 5.4 By Packaging Format

- 5.4.1 Primary Packaging

- 5.4.2 Secondary Packaging

- 5.4.3 Tertiary Packaging

- 5.5 By Country

- 5.5.1 Germany

- 5.5.2 United Kingdom

- 5.5.3 France

- 5.5.4 Italy

- 5.5.5 Spain

- 5.5.6 Netherlands

- 5.5.7 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Smurfit WestRock

- 6.4.2 Mondi plc

- 6.4.3 International Paper Company

- 6.4.4 Stora Enso Oyj

- 6.4.5 Svenska Cellulosa Aktiebolaget SCA

- 6.4.6 Metsa Board Oyj

- 6.4.7 Mayr-Melnhof Karton AG

- 6.4.8 Prinzhorn Holding GmbH

- 6.4.9 Progroup AG

- 6.4.10 Schumacher Packaging GmbH

- 6.4.11 Klingele Papierwerke GmbH & Co. KG

- 6.4.12 Graphic Packaging Holding Company

- 6.4.13 RAJA Groupe

- 6.4.14 VPK Packaging Group NV

- 6.4.15 RDM Group (Reno De Medici S.p.A.)

- 6.4.16 Lucart S.p.A.

- 6.4.17 Essity AB

- 6.4.18 Palm GmbH & Co. KG

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

可拉伸纸包装市场:依材料等级、包装形式、应用、终端用户产业及销售管道划分-2026-2032年全球市场预测纸包装材料市场:依产品类型、材料类型、印刷技术和应用划分-2026-2032年全球预测

可拉伸纸包装市场:依材料等级、包装形式、应用、终端用户产业及销售管道划分-2026-2032年全球市场预测纸包装材料市场:依产品类型、材料类型、印刷技术和应用划分-2026-2032年全球预测 纸包装市场规模、份额、趋势和预测:按产品类型、等级、包装等级、最终用途产业和地区划分,2026-2034年

纸包装市场规模、份额、趋势和预测:按产品类型、等级、包装等级、最终用途产业和地区划分,2026-2034年 全球再生纸包装市场规模、份额、趋势和成长分析报告(2026-2034)

全球再生纸包装市场规模、份额、趋势和成长分析报告(2026-2034) 中国纸包装:市场占有率分析、产业趋势与统计、成长预测(2026-2031年)亚太地区纸包装:市场占有率分析、产业趋势与统计、成长预测(2026-2031)越南纸包装:市场占有率分析、产业趋势与统计、成长预测(2026-2031)全球纸包装市场规模、份额、趋势和成长分析报告(2026-2034年)全球纸垫製造机械市场规模、份额、趋势和成长分析报告(2026-2034)全球纸瓶市场规模、份额、趋势和成长分析报告(2026-2034年)

中国纸包装:市场占有率分析、产业趋势与统计、成长预测(2026-2031年)亚太地区纸包装:市场占有率分析、产业趋势与统计、成长预测(2026-2031)越南纸包装:市场占有率分析、产业趋势与统计、成长预测(2026-2031)全球纸包装市场规模、份额、趋势和成长分析报告(2026-2034年)全球纸垫製造机械市场规模、份额、趋势和成长分析报告(2026-2034)全球纸瓶市场规模、份额、趋势和成长分析报告(2026-2034年)