|

市场调查报告书

商品编码

1939617

中国纸包装:市场占有率分析、产业趋势与统计、成长预测(2026-2031年)China Paper Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

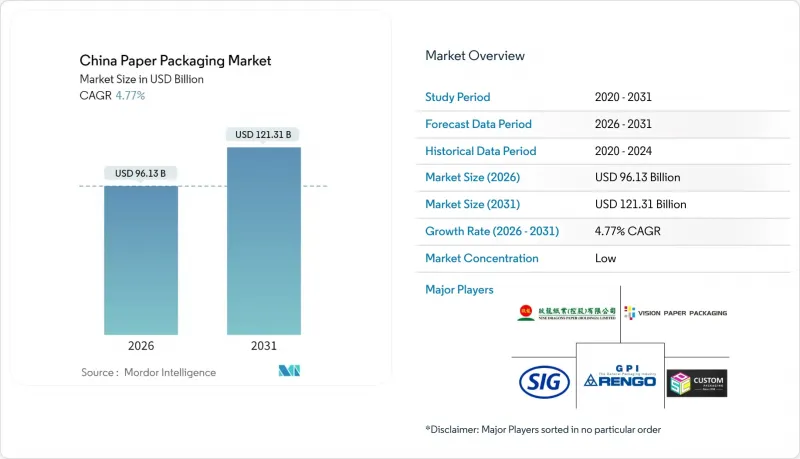

2025年中国纸包装市场价值917.5亿美元,预计到2031年将达到1,213.1亿美元,高于2026年的961.3亿美元。

预计在预测期(2026-2031 年)内,复合年增长率将达到 4.77%。

儘管纸浆价格波动,但市场仍保持成长。这主要得益于电子商务小包裹量的成长、政府的塑胶减量政策以及餐饮服务业的蓬勃发展,这些因素共同推动了对瓦楞纸箱和折迭纸箱的新需求。中国的国家碳信用计画奖励提高回收率的製造商,加速了再生纤维的普及应用。先进的数位印刷技术也使品牌能够进行小批量、客製化的宣传活动,而无需浪费库存。虽然像九龙纸业和太阳纸业集团这样的国内巨头正在透过高速瓦楞纸板机扩大产能,但由于进口木纤维价格波动和电价不稳定,成本压力依然居高不下。各省绿色包装法规的实施也日益复杂,迫使企业进行配方在地化,并投资建置符合GB 43352-2023标准中重金属和限制物质含量规定的品管系统。

中国纸包装市场趋势与分析

电子商务小包裹量成长

预计到2024年,宅配处理量将达到1,745亿件,其中瓦楞纸包装占比高达96.17%,为中国纸质包装市场奠定了坚实的基础。北京和上海等城市物流枢纽正在降低最后一公里配送成本、缩短配送时间,同时也提高了对能够承受多次搬运的二级包装盒的性能要求。阿里巴巴的火箭速递试点服务(目标是实现全球一小时送达)就是一个很好的例子,它展现了极速配送如何迫使包装设计师在保持抗衝击性的同时,优化包装的强度重量比。QR码序列化和RFID标籤植入技术正日益普及于运输纸箱中,实现了库存视觉化和自动退货。这些发展趋势共同巩固了电子商务作为中国纸包装市场结构性基础的地位。

拓展餐饮业及配送生态系统

外带订单在商业中心产生大量废弃物,其中前10%的区域占包装废弃物总量的64%,促使餐饮企业转向轻便的纤维性包装解决方案。由Samcoca等国内供应商开发的甘蔗渣模塑可重复使用托盘在高端加盟商中越来越受欢迎,而能够追踪食品新鲜度的生物感测器标籤则有助于在不影响安全性的前提下扩大配送范围。跨国速食连锁店已开始试用可清洗的店内包装容器,这预示着随着地方政府收紧一次性塑胶製品的监管标准,未来这些容器也将得到遵守。这些因素共同推动了中国纸质包装市场的发展。

废纸进口法规和原料供应的变化

2023年,中国将进口2,800万吨商品浆,比上年增加24%。这使得造纸厂极易受到运输中断和关税波动的影响。禁止进口消费后纤维导致国内回收企业几乎满载运作,推高了废纸价格,迫使加工商降低纸张纸张重量。成品纸关税的降低将加剧与东协造纸厂的竞争,在价格低迷时期挤压国内利润空间。这些趋势导致中国纸包装市场成长预期被下调。

细分市场分析

受宅配对轻便、抗压包装需求的推动,瓦楞纸箱预计到2025年将占据中国纸包装市场35.62%的份额。东莞市黄石金辉的352米/分钟瓦楞纸板生产线便是产能扩张以确保电商枢纽即时供货的典范。然而,随着化妆品奢侈品消费的日益增长,折迭纸盒预计到2031年将保持7.68%的复合年增长率,从而削弱瓦楞纸箱的市场主导地位。多道次数码印刷机无需长时间准备即可实现上光效果和局部烫金工艺,使高阶美妆品牌能够印製限量版产品并获得高利润。液体包装纸盒采用SIG的无铝技术,在保护乳製品保存期限的同时,还能减少61%的碳排放,进而在细分市场中占有一席之地。由于都市区医疗费用支出不断增加,包括防篡改药品包装套在内的特殊药品子产品线正在稳定成长。

到2025年,食品包装将占中国纸包装市场的41.05%,主要都市区外带和饮料消费主导。盒饭需求在主要都市区地区蓬勃发展,促使地方政府试行循环回收系统,为再生纤维工厂提供原料。个人护理和化妆品产业虽然规模较小,但得益于网路美妆部落客的崛起和可支配收入的增加,正以每年8.07%的速度成长。安姆科的可回收包装袋和可重复填充的胶囊正被一线购物中心的洗髮精填充站采用,体现了功能性和永续性的融合。电子品牌对防静电和防潮内衬的需求是一个盈利的交叉领域,瓦楞纸箱製造商正透过在瓦楞纸板上应用奈米黏土涂层来满足这一需求。温度记录智慧标籤正被整合到医疗包装中,以确保药品在整个区域低温运输的品质。

中国纸包装市场报告按产品类型(折迭纸盒、瓦楞纸箱、纸袋、液体包装纸盒等)、终端用户行业(食品、饮料、医疗、个人护理、家居用品、电子产品等)、材料类型(原生纤维、再生纤维)、包装级别(初级包装、二级包装、三级包装)和地区(中国)进行细分。市场预测以美元以金额为准。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 电子商务小包裹量增加

- 拓展餐饮与配送生态系统

- 政府强制减少塑胶製品的使用促进了纸製品的生产。

- 整合先进的数位印刷和智慧包装技术

- 跨境电商一体化提升了对瓦楞纸包装的需求

- 全国排碳权计画加速推广再生材料的使用

- 市场限制

- 废纸进口法规和原料供应的变化

- 与可再生单一材料塑胶的竞争

- 脱碳目标导致能源成本上升

- 纸浆价格波动週期和国内木浆短缺

- 供应链分析

- 监管环境

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 中国纸浆和造纸业:外国投资者的机会

- 环境、社会及公司治理 (ESG) 与永续发展倡议

第五章 市场规模与成长预测

- 依产品类型

- 折迭纸箱

- 瓦楞纸箱

- 纸袋和纸袋

- 液体包装纸箱

- 其他产品类型

- 按最终用户行业划分

- 食物

- 饮料

- 医疗和药品

- 个人护理及化妆品

- 家居用品和清洁剂

- 电子电气产品

- 其他终端用户产业

- 依材料类型

- 基于原生纤维

- 再生纤维基体

- 按包装级别

- 初级包装

- 二级包装

- 三级包装

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Nine Dragons Paper(Holdings)Ltd

- Lee & Man Paper Mfg Ltd

- Shanying International Holdings Co., Ltd

- Dongguan Vision Paper Products Co., Ltd

- Rengo Co., Ltd

- Oji Holdings Corp(China Packaging)

- SIG Combibloc Group

- Shanghai Custom Packaging Co., Ltd

- Xiamen Hexing Packaging & Printing Co., Ltd

- JML Packaging

- Suneco Box Co., Ltd

- Asia Pulp & Paper(APP)Sinar Mas

- Shanghai DE Printed Box

- Mondi Group

- Smurfit WestRock

- International Paper(China)

- Yutong Packaging Technology

- Zhejiang Jingxing Paper

- Guangdong Yizhou Packaging

第七章 市场机会与未来展望

The China paper packaging market was valued at USD 91.75 billion in 2025 and estimated to grow from USD 96.13 billion in 2026 to reach USD 121.31 billion by 2031, at a CAGR of 4.77% during the forecast period (2026-2031).

Expansion continues despite pulp-price cycles because e-commerce parcel volumes, government plastic-reduction mandates, and food-service growth all channel fresh demand into corrugated and folding-carton formats. Recycled fiber adoption accelerates as China's national carbon-credit scheme rewards manufacturers that raise recovered-content ratios, while advanced digital printing lets brands run short, customized campaigns without inventory waste. Domestic leaders such as Nine Dragons Paper and Sun Paper Group extend capacity through high-speed corrugators and board machines, yet volatility in imported wood fiber and dynamic electricity pricing keeps cost pressure high. Provincial variability in green-packaging enforcement adds complexity, prompting firms to localize formulations and invest in quality-control systems that meet GB 43352-2023 limits on heavy metals and restricted substances.

China Paper Packaging Market Trends and Insights

Growth in e-commerce parcel volume

Express delivery handled 174.5 billion items in 2024, with corrugated packaging accounting for 96.17% of box material, ensuring resilient baseline consumption for the China paper packaging market. Metro-based logistics hubs in Beijing and Shanghai compress last-mile costs and shorten delivery times, but they also intensify performance requirements for secondary boxes that must survive multiple handling cycles. Alibaba's pilot rocket-delivery initiative, targeting one-hour global drop-offs, exemplifies how extreme speed pushes packaging designers to optimize weight-to-strength ratios while preserving shock resistance. QR-code serialization and RFID inserts increasingly appear on shipping cartons, enabling inventory visibility and returns automation. Together these developments cement e-commerce as the structural backbone for the China paper packaging market.

Expansion of food-service and delivery ecosystem

Takeaway orders generate high-density waste in core commercial grids where the top 10% of zones account for 64% of packaging discards, driving restaurants to switch to lighter, fiber-based solutions. Reusable, bagasse-molded trays developed by domestic suppliers such as Sumkoka gain traction among premium franchises, while biosensor labels that track freshness support longer delivery radii without safety compromises. Multinational quick-service chains pilot washable dine-in containers, indicating the direction of future compliance as provincial regulators tighten thresholds on single-use plastics. These factors collectively add momentum to the China paper packaging market.

Volatile waste-paper import rules and raw-material supply

China imported 28 million tons of market pulp in 2023, a 24% rise that exposes mills to freight disruptions and tariff shifts. The ban on post-consumer fibre imports keeps domestic recyclers running near full capacity, raising recovered-paper prices and occasionally forcing converters to down-spec grammage. Tariff cuts on finished paper boost competition from ASEAN mills, eroding domestic margins during price troughs. These dynamics trim growth expectations for the China paper packaging market.

Other drivers and restraints analyzed in the detailed report include:

- Government plastic-reduction mandates favouring paper

- Advanced digital printing and smart-packaging integration

- Escalating energy costs amid decarbonisation targets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Corrugated boxes generated 35.62% of China paper packaging market size in 2025 as express freight required light, crush-resistant formats. Dongguan Huangshi Jinhui's 352 m-per-minute corrugator exemplifies capacity build-out that secures just-in-time supply for e-commerce hubs. Yet folding cartons, buoyed by cosmetics premiumisation, are pacing a 7.68% CAGR that will erode corrugated dominance through 2031. Multi-pass digital presses support varnish effects and spot-foil accents without forcing long makeready times, letting boutique beauty labels print limited editions that fetch high margins. Liquid packaging cartons maintain niche relevance by leveraging SIG's alu-layer-free technology, which cuts carbon footprints by 61% while safeguarding dairy shelf life. Speciality sub-lines, including tamper-evident pharma sleeves, grow steadily as healthcare spending rises in urban markets.

Food products held 41.05% of China paper packaging market share in 2025 because takeaway dining dominates urban consumption. Meal-box density spikes in grid hotspots, prompting municipalities to trial closed-loop collection that feeds recycled-fibre mills. Personal-care and cosmetics, though smaller, expand 8.07% yearly on the back of online beauty influencers and rising disposable income. Amcor's recycle-ready pouches and refill pods serve shampoo refill stations in tier-one malls, illustrating how functionality merges with sustainability. Electronics brands demand anti-static, moisture-barrier liners, a lucrative cross-over that corrugated suppliers address by grafting nanoclay coatings onto fluting. Healthcare packaging integrates smart labels for temperature logging, ensuring drug integrity across regional cold chains.

The China Paper Packaging Market Report is Segmented by Product Type (Folding Cartons, Corrugated Boxes, Paper Bags and Sacks, Liquid Packaging Cartons, and More), End-User Industry (Food, Beverage, Healthcare, Personal Care, Household Care, Electronics, and More), Material Type (Virgin Fibre-Based, Recycled Fibre-Based), Packaging Level (Primary, Secondary, Tertiary), and Geography (China). Market Forecasts are in Value (USD).

List of Companies Covered in this Report:

- Nine Dragons Paper (Holdings) Ltd

- Lee & Man Paper Mfg Ltd

- Shanying International Holdings Co., Ltd

- Dongguan Vision Paper Products Co., Ltd

- Rengo Co., Ltd

- Oji Holdings Corp (China Packaging)

- SIG Combibloc Group

- Shanghai Custom Packaging Co., Ltd

- Xiamen Hexing Packaging & Printing Co., Ltd

- JML Packaging

- Suneco Box Co., Ltd

- Asia Pulp & Paper (APP) Sinar Mas

- Shanghai DE Printed Box

- Mondi Group

- Smurfit WestRock

- International Paper (China)

- Yutong Packaging Technology

- Zhejiang Jingxing Paper

- Guangdong Yizhou Packaging

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growth in e-commerce parcel volume

- 4.2.2 Expansion of food-service and delivery ecosystem

- 4.2.3 Government plastic-reduction mandates favouring paper

- 4.2.4 Advanced digital printing and smart-packaging integration

- 4.2.5 Cross-border e-commerce consolidation boosting corrugated demand

- 4.2.6 National carbon-credit scheme accelerating recycled-content uptake

- 4.3 Market Restraints

- 4.3.1 Volatile waste-paper import rules and raw-material supply

- 4.3.2 Competition from recyclable mono-material plastics

- 4.3.3 Escalating energy costs amid decarbonisation targets

- 4.3.4 Pulp price cycles and domestic wood-pulp shortfall

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 China Pulp and Paper: Opportunities for Foreign Investors

- 4.9 ESG and Sustainability Initiatives

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Folding Cartons

- 5.1.2 Corrugated Boxes

- 5.1.3 Paper Bags and Sacks

- 5.1.4 Liquid Packaging Cartons

- 5.1.5 Other Product Types

- 5.2 By End-user Industry

- 5.2.1 Food

- 5.2.2 Beverage

- 5.2.3 Healthcare and Pharmaceuticals

- 5.2.4 Personal Care and Cosmetics

- 5.2.5 Household Care and Detergents

- 5.2.6 Electronics and Electrical Products

- 5.2.7 Other End-user Industries

- 5.3 By Material Type

- 5.3.1 Virgin Fibre-based

- 5.3.2 Recycled Fibre-based

- 5.4 By Packaging Level

- 5.4.1 Primary Packaging

- 5.4.2 Secondary Packaging

- 5.4.3 Tertiary Packaging

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Nine Dragons Paper (Holdings) Ltd

- 6.4.2 Lee & Man Paper Mfg Ltd

- 6.4.3 Shanying International Holdings Co., Ltd

- 6.4.4 Dongguan Vision Paper Products Co., Ltd

- 6.4.5 Rengo Co., Ltd

- 6.4.6 Oji Holdings Corp (China Packaging)

- 6.4.7 SIG Combibloc Group

- 6.4.8 Shanghai Custom Packaging Co., Ltd

- 6.4.9 Xiamen Hexing Packaging & Printing Co., Ltd

- 6.4.10 JML Packaging

- 6.4.11 Suneco Box Co., Ltd

- 6.4.12 Asia Pulp & Paper (APP) Sinar Mas

- 6.4.13 Shanghai DE Printed Box

- 6.4.14 Mondi Group

- 6.4.15 Smurfit WestRock

- 6.4.16 International Paper (China)

- 6.4.17 Yutong Packaging Technology

- 6.4.18 Zhejiang Jingxing Paper

- 6.4.19 Guangdong Yizhou Packaging

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

可拉伸纸包装市场:依材料等级、包装形式、应用、终端用户产业及销售管道划分-2026-2032年全球市场预测纸包装材料市场:依产品类型、材料类型、印刷技术和应用划分-2026-2032年全球预测

可拉伸纸包装市场:依材料等级、包装形式、应用、终端用户产业及销售管道划分-2026-2032年全球市场预测纸包装材料市场:依产品类型、材料类型、印刷技术和应用划分-2026-2032年全球预测 纸包装市场规模、份额、趋势和预测:按产品类型、等级、包装等级、最终用途产业和地区划分,2026-2034年

纸包装市场规模、份额、趋势和预测:按产品类型、等级、包装等级、最终用途产业和地区划分,2026-2034年 全球再生纸包装市场规模、份额、趋势和成长分析报告(2026-2034)

全球再生纸包装市场规模、份额、趋势和成长分析报告(2026-2034) 亚太地区纸包装:市场占有率分析、产业趋势与统计、成长预测(2026-2031)欧洲纸包装市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031年)越南纸包装:市场占有率分析、产业趋势与统计、成长预测(2026-2031)全球纸包装市场规模、份额、趋势和成长分析报告(2026-2034年)全球纸垫製造机械市场规模、份额、趋势和成长分析报告(2026-2034)全球纸瓶市场规模、份额、趋势和成长分析报告(2026-2034年)

亚太地区纸包装:市场占有率分析、产业趋势与统计、成长预测(2026-2031)欧洲纸包装市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031年)越南纸包装:市场占有率分析、产业趋势与统计、成长预测(2026-2031)全球纸包装市场规模、份额、趋势和成长分析报告(2026-2034年)全球纸垫製造机械市场规模、份额、趋势和成长分析报告(2026-2034)全球纸瓶市场规模、份额、趋势和成长分析报告(2026-2034年)