|

市场调查报告书

商品编码

1938998

美国建设化学品:市场占有率分析、产业趋势与统计、成长预测(2026-2031)United States Construction Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

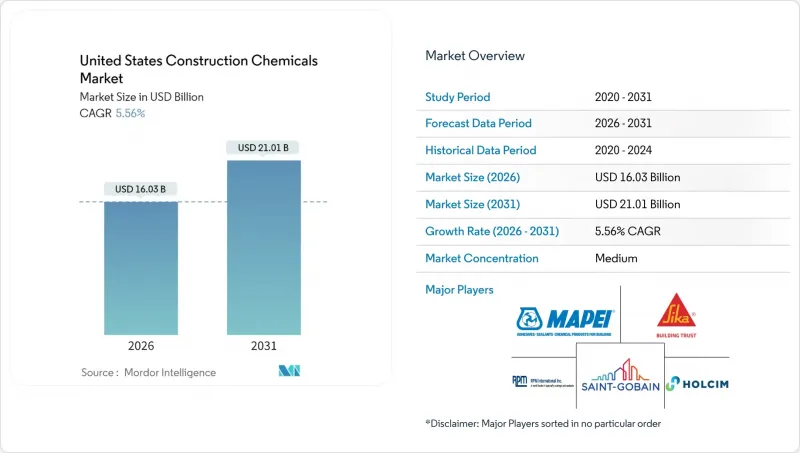

美国建筑化学品市场预计将从 2025 年的 151.9 亿美元成长到 2026 年的 160.3 亿美元,预计到 2031 年将达到 210.1 亿美元,2026 年至 2031 年的复合年增长率为 5.56%。

多项联邦基础设施项目、更严格的建筑规范以及现场工作流程的快速数位化,都在支撑市场需求。同时,石油原料价格波动和劳动力短缺给利润率带来了压力。联邦政府优先采购低碳材料,加速了生物基添加剂和低挥发性有机化合物(VOC)涂料的转型。对资料中心和半导体产业的投资扩大了高性能地板材料系统的潜在市场。气候变迁立法,尤其是在飓风频繁的州,正在推动对防风防水膜材製定更高的规范标准。同时,大型製造商的垂直整合在物流紧张的环境下,为下游建筑公司提供更可预测的供应链,同时也给经销商的利润率带来了压力。

美国建筑化学品市场趋势与洞察

基础设施法案下的主要计划

透过《基础设施投资和就业创造法案》获得的联邦资金正在加速对耐久性外加剂、耐腐蚀涂料和结晶防水系统的需求,这些产品可将桥樑和隧道的使用寿命延长60年或更久。参与铁路改造和港口扩建的承包商越来越多地指定使用低收缩率的高效减水剂,以提高拥挤施工现场的泵送性能。拥有移动式混合料测试实验室的供应商正在赢得多年供应协议,因为许多公共合约现在都规定了连续混合料检验。州际公路沿线的区域丛集使製造商能够缩短前置作业时间、降低运输成本,并提供现场技术培训,从而减少施工错误。

住宅开工量復苏及维修需求不断累积

随着房屋抵押贷款下降,独栋住宅的建筑许可数量正在上升。同时,维修达5,743亿美元的住宅市场正经历持续到2025年的维修需求积压。新建和维修需求的融合有利于多功能防水膜、低VOC密封剂和裂缝修补砂浆的销售,这些产品可以实现持续维修,而无需长时间停工。美国建筑化学品市场持续受益于居住通路,小包装和已调整的着色密封剂鼓励消费者重复购买。由于越来越多的住宅将隔热材料、地板材料和外墙维修合併在一个计划中,捆绑销售防潮层和表面处理的经销商获得了更高的单价。

石油衍生原料价格波动

物流瓶颈和地板材料承包商之间日益扩大的竞标差异导致环氧树脂价格在2025年上涨,迫使固定价格合约中引入价格递增条款。由于付款週期延长,缺乏对冲机制的小规模区域化合物生产商面临更紧张的营运资金,这推动了美国建设化学品市场的整合。一些製造商正在重新配製产品,使用生物基稀释剂和再生PET多元醇来降低利润波动,但供应仍然有限。原物料价格波动也使公共工程预算编制变得复杂,因为许多州在竞标开始前很久就最终确定了年度预算,导致资金筹措和采购成本之间存在差异。

细分市场分析

预计到2025年,防水解决方案将占据美国建设化学品市场34.42%的最大份额,并在2031年之前以6.05%的复合年增长率成长。这一主导地位反映了商业和住宅建筑规范对连续气密层的需求,以及保险业对更高防潮性能的要求。液态涂覆膜正逐渐取代片材,因为其喷涂方式能够无缝覆盖复杂的穿透部位,从而消除潜在的失效点。随着飓风频率的增加,沿海地区的建筑商越来越多地选择弹性体膜,这种薄膜经过测试可承受10,000次疲劳循环。虽然这种特性使其价格高出15%,但可以降低终身维修成本。

无缝防水捲材日益普及,使得单组分、湿固化聚氨酯基产品更受青睐,因为它们可以在潮湿环境下施工。承包商表示,新开发的低气味配方无需负压帐篷即可在室内施工,扩大了其在地下停车场的应用范围。永续性指标也至关重要,目前,含有35%回收成分的水性丙烯酸防水卷材在公共住宅计划中可享有联邦税收优惠。随着美国环保署(EPA)考虑加强溶剂监管,製造商正在投资研发兼具柔软性和超低VOC排放的硅烷封端聚醚主链。预计这些趋势将助力防水系统在预测期内继续保持其在美国建设化学品市场的主导地位。

美国建筑化学品报告按产品类型(黏合剂、锚固剂和水泥浆、混凝土外加剂、混凝土保护涂料、地板树脂、修补和修復化学品、密封剂、表面处理化学品等)和应用类型(商业、工业和公共、基础设施、住宅)进行细分。市场预测以以金额为准。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 基础设施法案下的主要计划

- 住宅开工量及维修需求积压情形的復苏

- 过渡到高性能、环保外加剂

- 根据《建筑标准法》,扩大防水和防护涂料的使用范围。

- 资料中心的快速发展推动了对特种地板材料的需求。

- 市场限制

- 石油衍生原料价格波动

- 加强VOC和危险化学品法规

- 先进系统熟练安装人员短缺

- 价值链分析

- 监管环境

- 波特五力模型

- 竞争对手之间的竞争

- 新进入者的威胁

- 供应商的议价能力

- 买方的议价能力

- 替代品的威胁

第五章 市场规模与成长预测

- 副产品

- 黏合剂

- 热熔胶

- 反应性

- 溶剂型

- 水溶液

- 锚栓和水泥浆

- 水泥基固定剂

- 树脂固定

- 混凝土外加剂

- 加速器

- 空气引射器

- 高效减水剂

- 缓速器

- 收缩抑制剂

- 黏度调节剂

- 增塑剂

- 其他的

- 混凝土保护涂层

- 丙烯酸纤维

- 醇酸树脂

- 环氧树脂

- 聚氨酯

- 其他树脂

- 地板树脂

- 丙烯酸纤维

- 环氧树脂

- 聚天门冬胺酸树脂

- 聚氨酯

- 其他树脂

- 维修和维修化学品

- 纤维缠绕系统

- 压浆

- 微型混凝土砂浆

- 改质砂浆

- 钢筋保护材料

- 密封剂

- 丙烯酸纤维

- 环氧树脂

- 聚氨酯

- 硅酮

- 其他树脂

- 表面处理化学品

- 固化剂

- 释放剂

- 其他的

- 防水解决方案

- 化学品

- 防水膜

- 黏合剂

- 按最终用户类别

- 商业的

- 工业和公共设施

- 基础设施

- 住宅

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率**(%)/排名分析

- 公司简介

- 3M

- Arkema

- Ashland

- Dow

- Kingspan Group

- Henkel AG & Co. KGaA

- HOLCIM

- ARDEX Americas

- MAPEI SpA

- LATICRETE International, Inc

- RPM International Inc.

- Sika AG

- Saint-Gobain

- Xypex USA

第七章 市场机会与未来展望

- 閒置频段与未满足需求评估

第八章:执行长面临的关键策略挑战

The United States Construction Chemicals Market is expected to grow from USD 15.19 billion in 2025 to USD 16.03 billion in 2026 and is forecast to reach USD 21.01 billion by 2031 at 5.56% CAGR over 2026-2031.

Multiple federal infrastructure programs, tightening building codes, and rapid digitalization of job-site workflows are sustaining demand even as volatile petroleum inputs and labor shortages weigh on margins. Federal procurement preferences for low-carbon materials are accelerating the shift toward bio-based admixtures and low-VOC coatings, while investments in data centers and semiconductors are expanding the addressable market for high-performance flooring systems. Climate resilience legislation, particularly in hurricane-prone states, is driving higher specification rates for waterproofing membranes that can withstand wind-driven rain and hydrostatic pressure. At the same time, vertical integration moves by large producers are compressing distributor margins yet providing downstream contractors with more predictable supply in an otherwise strained logistics environment.

United States Construction Chemicals Market Trends and Insights

Infrastructure-Bill Funded Mega-Projects

Federal spending channeled through the Infrastructure Investment and Jobs Act is accelerating demand for high-durability admixtures, corrosion-resistant coatings, and crystalline waterproofing systems that extend bridge and tunnel service life by more than six decades. Contractors undertaking rail realignments and port expansions increasingly specify low-shrinkage superplasticizers that improve pumpability on congested sites. Suppliers with mobile batching laboratories are winning multi-year supply agreements because continuous mix verification is now written into many public contracts. Regional clusters around interstate corridors enable manufacturers to shorten lead times, lower freight costs, and provide onsite technical training that mitigates application errors.

Housing-Start Rebound and Repair Backlog

Single-family permits are rising in tandem with declining mortgage rates, while a USD 574.3 billion home-improvement sector is pushing pent-up repair work into 2025. The dual flow of new builds and retrofits favors multi-purpose waterproofing membranes, low-VOC sealants, and crack-bridging repair mortars that enable occupied-building renovations without lengthy shutdowns. The US construction chemicals market continually benefits from do-it-yourself channels where smaller packaging formats and color-matched sealants produce repeat consumer purchases. Distributors that bundle moisture-barrier products with surface treatments are capturing higher basket values because homeowners frequently tackle insulation, flooring, and facade upgrades in a single project cycle.

Volatile Petroleum-Derived Raw-Material Prices

Epoxy-resin prices rose in 2025 amid logistics bottlenecks, widening bid-price spread for flooring contractors, and forcing escalator clauses into fixed-sum contracts. Smaller regional blenders lacking hedging mechanisms face working-capital pinch points as payment cycles stretch, prompting consolidation within the US construction chemicals market. Some manufacturers are reformulating toward bio-based diluents and reclaimed PET polyols to cushion margin swings, though supply volumes remain limited. Raw-material volatility also complicates public-project budgeting because many states lock annual appropriations well before bid openings, creating a mismatch between funding and procurement costs.

Other drivers and restraints analyzed in the detailed report include:

- Shift Toward High-Performance and Green Admixtures

- Code-Driven Uptake of Waterproofing and Protective Coatings

- Skilled Applicator Shortage for Advanced Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Waterproofing solutions generated the largest share of the United States construction chemicals market at 34.42% in 2025 and are expected to expand at a 6.05% CAGR through 2031. This dominance reflects code-mandated continuous air barriers and insurance-driven moisture control upgrades in both commercial and residential builds. Liquid-applied membranes are outpacing sheet goods because spray application seamlessly wraps complex penetrations, eliminating seams that can become failure points. Rising hurricane frequency encourages builders in coastal ZIP codes to choose elastomeric membranes tested to withstand 10,000 fatigue cycles, a feature that commands a 15% price premium yet lowers lifetime repair expense.

Seamless membrane uptake benefits one-part, moisture-cure polyurethane chemistries that tolerate damp substrates common in fast-track schedules. Contractors report that new low-odor formulations enable interior application without the need for negative-pressure tents, thereby expanding usage to subterranean parking decks. Sustainability metrics matter too, and water-borne acrylic membranes with 35% recycled content now qualify for federal tax incentives on public housing projects. With the EPA exploring stricter solvent cutoffs, producers are investing in silyl-terminated polyether backbones that combine flexibility with ultralow VOC outputs. Together, these dynamics position waterproofing systems to preserve the leading title in the United States construction chemicals market through the forecast horizon.

The United States Construction Chemicals Report is Segmented by Product (Adhesives, Anchors and Grouts, Concrete Admixtures, Concrete Protective Coatings, Flooring Resins, Repair and Rehabilitation Chemicals, Sealants, Surface-Treatment Chemicals, and More), and End-Use Sector (Commercial, Industrial and Institutional, Infrastructure, and Residential). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- 3M

- Arkema

- Ashland

- Dow

- Kingspan Group

- Henkel AG & Co. KGaA

- HOLCIM

- ARDEX Americas

- MAPEI S.p.A.

- LATICRETE International, Inc

- RPM International Inc.

- Sika AG

- Saint-Gobain

- Xypex USA

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Infrastructure-bill funded mega-projects

- 4.2.2 Housing-start rebound and repair backlog

- 4.2.3 Shift toward high-performance and green admixtures

- 4.2.4 Code-driven uptake of waterproofing and protective coatings

- 4.2.5 Data-center boom fueling specialty flooring demand

- 4.3 Market Restraints

- 4.3.1 Volatile petroleum-derived raw material prices

- 4.3.2 Tightening VOC and toxic-chemical regulations

- 4.3.3 Skilled applicator shortage for advanced systems

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces

- 4.6.1 Competitive Rivalry

- 4.6.2 Threat of New Entrants

- 4.6.3 Bargaining Power - Suppliers

- 4.6.4 Bargaining Power - Buyers

- 4.6.5 Threat of Substitutes

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product

- 5.1.1 Adhesives

- 5.1.1.1 Hot-Melt

- 5.1.1.2 Reactive

- 5.1.1.3 Solvent-borne

- 5.1.1.4 Water-borne

- 5.1.2 Anchors and Grouts

- 5.1.2.1 Cementitious Fixing

- 5.1.2.2 Resin Fixing

- 5.1.3 Concrete Admixtures

- 5.1.3.1 Accelerator

- 5.1.3.2 Air-Entraining

- 5.1.3.3 Super-plasticizer

- 5.1.3.4 Retarder

- 5.1.3.5 Shrinkage-Reducer

- 5.1.3.6 Viscosity-Modifier

- 5.1.3.7 Plasticizer

- 5.1.3.8 Other Types

- 5.1.4 Concrete Protective Coatings

- 5.1.4.1 Acrylic

- 5.1.4.2 Alkyd

- 5.1.4.3 Epoxy

- 5.1.4.4 Polyurethane

- 5.1.4.5 Other Resins

- 5.1.5 Flooring Resins

- 5.1.5.1 Acrylic

- 5.1.5.2 Epoxy

- 5.1.5.3 Polyaspartic

- 5.1.5.4 Polyurethane

- 5.1.5.5 Other Resins

- 5.1.6 Repair and Rehabilitation Chemicals

- 5.1.6.1 Fiber-Wrapping Systems

- 5.1.6.2 Injection Grouting

- 5.1.6.3 Micro-concrete Mortars

- 5.1.6.4 Modified Mortars

- 5.1.6.5 Rebar Protectors

- 5.1.7 Sealants

- 5.1.7.1 Acrylic

- 5.1.7.2 Epoxy

- 5.1.7.3 Polyurethane

- 5.1.7.4 Silicone

- 5.1.7.5 Other Resins

- 5.1.8 Surface-Treatment Chemicals

- 5.1.8.1 Curing Compounds

- 5.1.8.2 Mold-Release Agents

- 5.1.8.3 Other Types

- 5.1.9 Waterproofing Solutions

- 5.1.9.1 Chemicals

- 5.1.9.2 Membranes

- 5.1.1 Adhesives

- 5.2 By End-User Sector

- 5.2.1 Commercial

- 5.2.2 Industrial and Institutional

- 5.2.3 Infrastructure

- 5.2.4 Residential

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share**(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 Ashland

- 6.4.4 Dow

- 6.4.5 Kingspan Group

- 6.4.6 Henkel AG & Co. KGaA

- 6.4.7 HOLCIM

- 6.4.8 ARDEX Americas

- 6.4.9 MAPEI S.p.A.

- 6.4.10 LATICRETE International, Inc

- 6.4.11 RPM International Inc.

- 6.4.12 Sika AG

- 6.4.13 Saint-Gobain

- 6.4.14 Xypex USA

7 Market Opportunities Future Outlook

- 7.1 White-space and Unmet-need Assessment

8 Key Strategic Questions for CEOs

建筑化学品市场:2026-2032年全球市场预测(依产品类型、技术、剂型、建筑类型、应用、最终用户和通路划分)固定式机械锚栓市场:依产品类型、材料、应用、终端用户产业及通路划分,全球预测,2026-2032年

建筑化学品市场:2026-2032年全球市场预测(依产品类型、技术、剂型、建筑类型、应用、最终用户和通路划分)固定式机械锚栓市场:依产品类型、材料、应用、终端用户产业及通路划分,全球预测,2026-2032年 建筑化学品市场分析及预测(至2035年):类型、产品、应用、形态、材质类型、技术、最终用户、功能、安装类型、解决方案

建筑化学品市场分析及预测(至2035年):类型、产品、应用、形态、材质类型、技术、最终用户、功能、安装类型、解决方案 建筑化学品:市场占有率分析、产业趋势与统计、成长预测(2026-2031)欧洲建设化学品:市场占有率分析、产业趋势与统计、成长预测(2026-2031)越南建设化学品:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

建筑化学品:市场占有率分析、产业趋势与统计、成长预测(2026-2031)欧洲建设化学品:市场占有率分析、产业趋势与统计、成长预测(2026-2031)越南建设化学品:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 全球建筑化学品市场规模、份额、趋势和成长分析报告(2026-2034年)

全球建筑化学品市场规模、份额、趋势和成长分析报告(2026-2034年) 建筑化学品市场规模、份额、趋势及预测(按类型、应用和地区划分)(2026-2034 年)

建筑化学品市场规模、份额、趋势及预测(按类型、应用和地区划分)(2026-2034 年) 2026年全球建筑化学品市场报告

2026年全球建筑化学品市场报告 建筑化学品市场-全球产业规模、份额、趋势、机会及预测(2021-2031 年)(依产品类型、应用、地区及竞争格局划分)

建筑化学品市场-全球产业规模、份额、趋势、机会及预测(2021-2031 年)(依产品类型、应用、地区及竞争格局划分)