|

市场调查报告书

商品编码

1939039

亚太地区燃气涡轮机维护、修理和大修 (MRO):市场份额分析、行业趋势和统计数据、成长预测 (2026-2031)Asia-Pacific Gas Turbine MRO - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

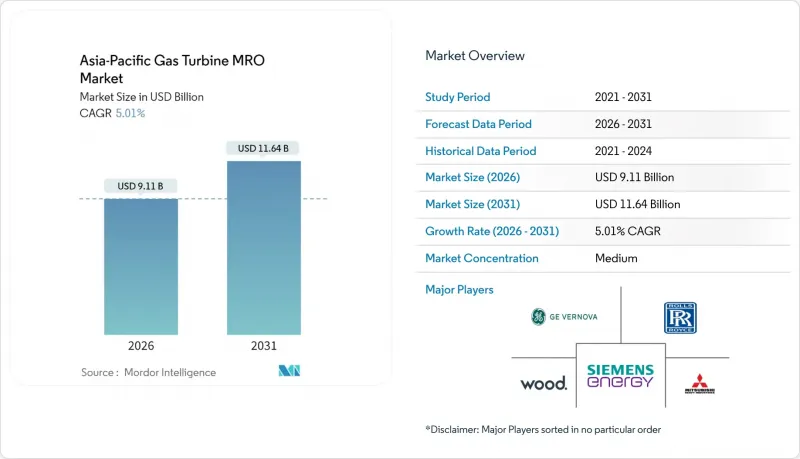

2025年亚太地区燃气涡轮机维护、修理和大修(MRO)市场价值为86.8亿美元,预计到2031年将达到116.4亿美元,高于2026年的91.1亿美元。

预计在预测期(2026-2031 年)内,复合年增长率将达到 5.01%。

飞机老化导致的维修需求不断增长、氢动力升级套件的快速普及以及大规模数位双胞胎技术的部署,都支撑了近期的市场需求。独立服务供应商正在扩大其零件製造商核准(PMA)范围,从而降低面临资金限制的营运商的维修成本。热端铸件供应链的瓶颈迫使电力公司寻求多个关键零件来源,推动了对区域铸造产能的投资。同时,中国和印度的煤改气政策促进了长期服务协议(LTSA)的签订,确保了多年的维护收入。最后,资料中心电力需求的激增显着增加了航空衍生引擎的维修次数,并扩大了高可用性、快速启动机组的服务覆盖范围。

亚太地区燃气涡轮机MRO市场趋势及展望

亚太地区老旧汽轮机机组达10万小时大修里程碑

在2000年代业界繁荣时期安装的数千台机组如今已达到10万运作小时(EOH)里程碑,这是一个关键阶段,需要对热气通道进行全面维修。中国和印度的业者面临相当于新建设成本19%至33%的维修成本,这导致许多业者延后资本更换,并透过实施逆向工程和剩余寿命延长技术来降低支出。随着资产所有者寻求比原厂(OEM)方案更具成本效益的替代方案,专注于转子寿命延长的独立服务公司正在赢得新的订单。

中国和印度的煤改气推动了新的长期服务协议(LTSA)的签订。

儘管到2024年天然气发电量仅占中国总发电量的3%,但北京已签署每年2700万吨液化天然气(LNG)的合同,以支持其能源转型战略。作为回应,电力生产商正在签署6至12年的长期维护协议(LTSA),以稳定维护现金流,并确保电网日益增长的运转率指标。印度也出现了类似的趋势,随着市场自由化,国有和私营电力公司都在转向签订包含绩效保证的综合服务合约。

可再生能源的间歇性会减少基本负载运作时间

随着太阳能和风能发电装置容量的成长,联合循环燃气涡轮机正越来越多地从主要动力源转向循环运作。频繁的启动停止会增加热应力,加速零件疲劳。这导致燃烧室和密封件的更换需求相对高于使用寿命较长的旋转设备。

细分市场分析

目前,120兆瓦以上的燃气涡轮机占亚太地区MRO(维护、维修和大修)支出的51.78%,并以每年5.52%的最快速度成长。业者看重这些大型机组的规模经济和高热效率,即使燃料价格波动,也能维持较低的单位电力成本。泰国的5,300兆瓦联合循环发电厂(由8台M701JAC机组组成)是这一趋势的例证,该电厂在运行10万小时后仍保持着约64%的效率。 120兆瓦以下的燃气涡轮机仍然很重要,尤其是在快速工业化的东南亚国协,它们在汽电共生、分散式发电和尖峰负载响应方面发挥重要作用,但其成长速度较慢。大型机组的检修週期为每2.4万至3万小时,通常成本相当于新机价格的19%至33%。然而,营运商越来越多地透过订购氢能升级改造来抵消这部分成本,这些改造既能保持效率,又能减少排放。

联合循环电厂占该地区维护、维修和大修 (MRO) 收入的 68.42%,预计到 2031 年将以每年 5.88% 的速度成长。其优点显而易见:将燃气涡轮机与蒸气底循环结合,可将热效率提升至 64% 以上,远优于单循环设备。近期的一些建设案例,例如中国的光明计划,表明这些电厂无需进行重大设计变更即可实现氢气混烧,从而在支持脱碳计划的同时,保持电网的柔软性。单循环电厂仍然占据着一定的市场地位,其快速启动和低资本成本的优势超过了燃料消耗,但长期业务收益有限。联合循环电厂营运商主要依赖 6 至 12 年的服务合同,这些合约涵盖零件、人事费用和性能保证,简化了预算编制,并有助于实现运转率目标。

亚太地区燃气涡轮机MRO市场报告按容量(小于30兆瓦、31-120兆瓦和大于120兆瓦)、涡轮循环(联合循环和开式/简单迴圈)、服务类型(维护、修理和大修)、最终用户行业(发电、石油和天然气、工业和其他)以及地区(中国、印度、日本、韩国、东南亚国协、澳大利亚和其他地区进行其他细分国家)。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 亚太地区老旧汽轮机机组接近10万小时大修阈值

- 中国和印度的煤改气推动了新的长期服务协议的签订。

- OEM的数位双胞胎技术可将非计划性停机时间减少15%以上

- 资料中心高峰需求激增导致航空衍生引擎维修车间访问量增加

- 氢燃料相容升级套件便于进行中期检查

- 市场限制

- 可再生能源的间歇性限制了基本负载运作时间

- 全球热型材铸件短缺导致备件前置作业时间延长

- 东协地区熟练工程师短缺问题日益严峻。

- PMA零件会损害OEM保固的经济效益。

- 供应链分析

- 技术展望

- 监管环境

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 按产能

- 小于30兆瓦

- 31~120MW

- 超过120兆瓦

- 通过涡轮循环

- 复合循环

- 开式循环/简单循环

- 按服务类型

- 维护

- 维修

- 大修

- 按最终用户行业划分

- 发电

- 石油和天然气(上游/中游/下游)

- 工业及其他

- 按地区

- 中国

- 日本

- 印度

- 韩国

- 东南亚国协

- 澳洲和纽西兰

- 亚太其他地区

第六章 竞争情势

- 市场集中度

- 策略性倡议(併购、伙伴关係、购电协议)

- 市场占有率分析(主要企业的市场排名和份额)

- 公司简介

- General Electric(GE Vernova)

- Siemens Energy

- Mitsubishi Heavy Industries

- Rolls-Royce

- MTU Aero Engines

- John Wood Group

- EthosEnergy

- Ansaldo Energia

- Sulzer

- Doosan Enerbility

- Kawasaki Heavy Industries

- Harbin Electric

- Shanghai Electric

- Toshiba Energy Systems

- Bharat Heavy Electricals(BHEL)

- Power Machines

- Fluor

- Bechtel

- MAN Energy Solutions

- Wartsila

第七章 市场机会与未来展望

The Asia-Pacific Gas Turbine MRO Market was valued at USD 8.68 billion in 2025 and estimated to grow from USD 9.11 billion in 2026 to reach USD 11.64 billion by 2031, at a CAGR of 5.01% during the forecast period (2026-2031).

Heightened overhaul activity as fleets age, rapid adoption of hydrogen-ready upgrade kits, and large-scale digital twin roll-outs anchor near-term demand. Independent service providers are expanding parts-manufacturer-approval (PMA) portfolios, lowering overhaul costs for operators that face capital constraints. Supply-chain bottlenecks in hot-section castings are prompting utilities to dual-source critical components, spurring regional investments in foundry capacity. Meanwhile, switch-overs from coal to gas in China and India underpin long-term service-agreement (LTSA) signings, locking in multi-year maintenance revenues. Finally, exponential data-center electricity demand pushes aeroderivative shop visits sharply higher, widening the addressable service pool for high-availability, quick-start units.

Asia-Pacific Gas Turbine MRO Market Trends and Insights

Aging APAC turbine fleet approaching 100 k EOH overhaul threshold

Thousands of units installed during the 2000s industrial boom are now hitting the 100,000 EOH mark, a milestone that compels full hot-gas-path refurbishment. Operators in China and India face overhaul bills ranging between 19% and 33% of new-build cost, an outlay many curb by deploying reverse-engineering and remaining-life-extension techniques that postpone capital replacement. Independent service firms specialising in rotor life rebuilds secure new work as asset owners pursue cost-effective alternatives to OEM programs.

Coal-to-gas shift in China & India drives new LTSA signings

Although gas produced just 3% of China's 2024 power, Beijing inked 27 million t per year LNG contracts to underpin its transition strategy. Generators respond by locking in 6- to 12-year LTSAs that stabilise maintenance cash flows and guarantee availability metrics that grids increasingly demand. A parallel pattern emerges in India as market liberalisation pushes state-run and private utilities toward bundled service deals featuring performance guarantees.

Renewable intermittency curtails baseload run-hours

As solar and wind capacity climbs, combined-cycle gas turbines increasingly swing from baseload to cycling duty. Frequent start-stops elevate thermal stresses, amplifying component fatigue and reshaping spares demand profiles toward more combustor and seal replacements relative to long-life rotors.

Other drivers and restraints analyzed in the detailed report include:

- OEM digital twins slash unplanned outages by >15%

- Data-center peaker demand spikes aeroderivative shop visits

- Global hot-section casting shortage inflates spare-part lead times

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Gas turbines rated above 120 MW now account for 51.78 % of Asia-Pacific's MRO spend and are expanding fastest at 5.52 % a year. Operators value these big machines for their scale economies and high thermal efficiency, which keeps unit-cost electricity low even as fuel prices fluctuate. Thailand's 5,300 MW complex, built around eight M701JAC units, illustrates the trend; those machines have already logged 100,000 operating hours while holding efficiency near 64 %. Below-120 MW turbines still matter, especially for cogeneration, distributed generation, and peaking duty in rapidly industrializing ASEAN nations, but their growth pace lags. Overhauls on large units fall every 24,000-30,000 hours and typically cost 19 %-33 % of a new machine, yet operators increasingly offset that expense by ordering hydrogen-ready upgrades that preserve efficiency while cutting emissions.

Combined-cycle plants generate 68.42 % of regional MRO revenue and should rise 5.88 % annually through 2031. The draw is simple: pairing a gas turbine with a steam bottoming cycle pushes thermal efficiency beyond 64 %, far better than a simple-cycle setup. Recent builds, China's Guangming project among them, show how these plants can co-fire hydrogen without major design changes, supporting decarbonization plans while preserving grid flexibility. Simple-cycle units still fill niche roles where fast starts and lower capital cost outweigh fuel burn, but they attract less long-term service revenue. Combined-cycle operators lean heavily on six- to twelve-year service agreements that bundle parts, labor, and performance guarantees-arrangements that simplify budgeting and sharpen availability targets.

The Asia-Pacific Gas Turbine MRO Market Report is Segmented by Capacity (Below 30 MW, 31 To 120 MW, and Above 120 MW), Turbine Cycle (Combined Cycle and Open/Simple Cycle), Service Type (Maintenance, Repair, and Overhaul), End-User Industry (Power Generation, Oil and Gas, and Industrial and Other), and Geography (China, India, Japan, South Korea, ASEAN Countries, Australia and New Zealand, and Rest of Asia-Pacific).

List of Companies Covered in this Report:

- General Electric (GE Vernova)

- Siemens Energy

- Mitsubishi Heavy Industries

- Rolls-Royce

- MTU Aero Engines

- John Wood Group

- EthosEnergy

- Ansaldo Energia

- Sulzer

- Doosan Enerbility

- Kawasaki Heavy Industries

- Harbin Electric

- Shanghai Electric

- Toshiba Energy Systems

- Bharat Heavy Electricals (BHEL)

- Power Machines

- Fluor

- Bechtel

- MAN Energy Solutions

- Wartsila

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Aging APAC turbine fleet approaching 100k EOH overhaul threshold

- 4.2.2 Coal-to-gas shift in China & India drives new LTSA signings

- 4.2.3 OEM digital twins slash unplanned outages by >15 %

- 4.2.4 Data-center peaker demand spikes aeroderivative shop visits

- 4.2.5 Hydrogen-ready upgrade kits trigger mid-life inspections

- 4.3 Market Restraints

- 4.3.1 Renewable intermittency curtails baseload run-hours

- 4.3.2 Global hot-section casting shortage inflates spare-part lead times

- 4.3.3 Skilled?technician gap widens in ASEAN

- 4.3.4 PMA parts disrupt OEM warranty economics

- 4.4 Supply-Chain Analysis

- 4.5 Technological Outlook

- 4.6 Regulatory Landscape

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Capacity

- 5.1.1 Below 30 MW

- 5.1.2 31 to 120 MW

- 5.1.3 Above 120 MW

- 5.2 By Turbine Cycle

- 5.2.1 Combined Cycle

- 5.2.2 Open/Simple Cycle

- 5.3 By Service Type

- 5.3.1 Maintenance

- 5.3.2 Repair

- 5.3.3 Overhaul

- 5.4 By End-user Industry

- 5.4.1 Power Generation

- 5.4.2 Oil and Gas (Up-/Mid-/Down-stream)

- 5.4.3 Industrial and Other

- 5.5 By Geography

- 5.5.1 China

- 5.5.2 Japan

- 5.5.3 India

- 5.5.4 South Korea

- 5.5.5 ASEAN Countries

- 5.5.6 Australia and New Zealand

- 5.5.7 Rest of Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 General Electric (GE Vernova)

- 6.4.2 Siemens Energy

- 6.4.3 Mitsubishi Heavy Industries

- 6.4.4 Rolls-Royce

- 6.4.5 MTU Aero Engines

- 6.4.6 John Wood Group

- 6.4.7 EthosEnergy

- 6.4.8 Ansaldo Energia

- 6.4.9 Sulzer

- 6.4.10 Doosan Enerbility

- 6.4.11 Kawasaki Heavy Industries

- 6.4.12 Harbin Electric

- 6.4.13 Shanghai Electric

- 6.4.14 Toshiba Energy Systems

- 6.4.15 Bharat Heavy Electricals (BHEL)

- 6.4.16 Power Machines

- 6.4.17 Fluor

- 6.4.18 Bechtel

- 6.4.19 MAN Energy Solutions

- 6.4.20 Wartsila

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment

全球燃气涡轮机MRO市场:市场规模、占有率、成长率、产业分析、依类型、应用和地区划分的分析、未来预测(2026-2034)

全球燃气涡轮机MRO市场:市场规模、占有率、成长率、产业分析、依类型、应用和地区划分的分析、未来预测(2026-2034) 燃气涡轮机MRO市场-全球产业规模、份额、趋势、机会及预测(依技术、最终用户、地区及竞争格局划分,2021-2031年预测)

燃气涡轮机MRO市场-全球产业规模、份额、趋势、机会及预测(依技术、最终用户、地区及竞争格局划分,2021-2031年预测) 燃气涡轮机MRO市场规模、份额和成长分析(按产能、类型、技术、终端用户产业和地区划分)-产业预测(2026-2033年)

燃气涡轮机MRO市场规模、份额和成长分析(按产能、类型、技术、终端用户产业和地区划分)-产业预测(2026-2033年) 电力产业燃气涡轮机MRO的全球市场

电力产业燃气涡轮机MRO的全球市场 2032 年燃气涡轮机MRO 市场预测:按供应商类型、服务类型、产能、技术、最终用户和地区进行的全球分析全球燃气涡轮机MRO市场

2032 年燃气涡轮机MRO 市场预测:按供应商类型、服务类型、产能、技术、最终用户和地区进行的全球分析全球燃气涡轮机MRO市场 电力产业的燃气涡轮机MRO:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)中东电力产业的燃气涡轮机MRO:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)

电力产业的燃气涡轮机MRO:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)中东电力产业的燃气涡轮机MRO:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)