|

市场调查报告书

商品编码

1939049

施工机械:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Construction Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

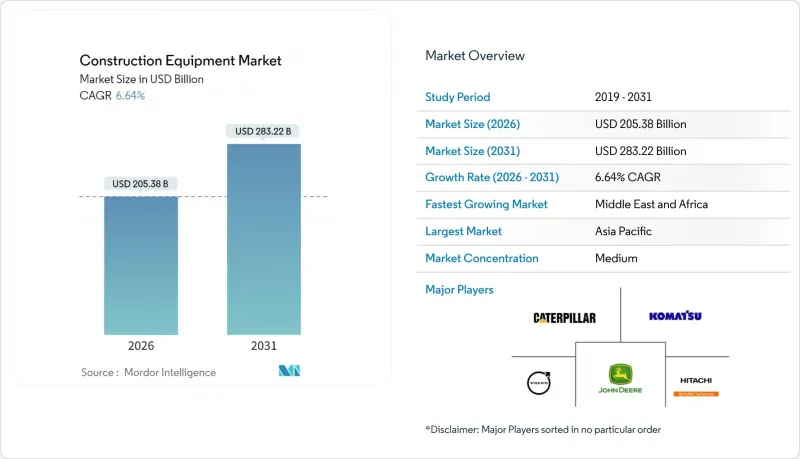

预计到 2026 年,施工机械市场规模将达到 2,053.8 亿美元,到 2031 年将成长至 2,832.2 亿美元。

在此期间,复合年增长率为 6.64%,显示市场规模和利润基础稳步扩大。

政府在道路、铁路、电网和半导体製造厂的大力投入,支撑了对土木机械、物料输送和混凝土机械的需求。亚洲的大型专案计划、欧洲和北美电气化进程的加快,以及整个产业向租赁车队的转型,都为强劲的成长前景做出了贡献。随着中国製造商在海外市场份额的不断扩大,以及西方主要製造商将重心转向以服务为中心的提案和自动驾驶技术,竞争日益激烈。此外,由于第五阶段排放标准和美国环保署第三阶段排放标准的实施,工程机械设备的更新换代週期加快,导致产品和数位化服务的发布週期缩短,这也对施工机械市场产生了影响。

全球施工机械市场趋势与洞察

亚洲各地的巨型基础设施项目每年推动超过2兆美元的资本需求。

随着超过3.7兆美元已承诺的计划改变资源分配优先顺序,大型推土机、45吨液压挖土机和大容量混凝土泵等设备正优先涌入亚洲的仓库,领先其他地区。光是沙乌地阿拉伯一国,到2024年的计划订单就高达550亿美元(比前一年成长57%),而阿联酋的订单量更是成长了200%,达到340亿美元。原始设备製造商(OEM)正在优化其销售组合,以推广高功率、长臂作业机型,并透过高价值合约和售后市场协议来巩固其收入基础。

美国《IRA法案》和《CHIPS法案》加快了为海岸重建计划购买土木机械的步伐

联邦政府对半导体製造厂、电动车工厂和电网升级的激励措施,正在推动美国阳光地带全部区域250至500马力推土机和挖土机的结构性需求。美国土木工程师协会预测,到2035年,基础设施缺口将达到3.7兆美元,因此,原始设备製造商(OEM)的订单累积订单似乎能够持续。由于面临劳动力短缺,建筑公司越来越多地选择功率更大的设备,以缩短计划并降低每小时的营运成本。

液压元件短缺导致OEM厂商前置作业时间大幅延长(超过42週)

关键液压阀和泵浦的交货週期超过 42 週,迫使建筑公司调整计划进度。市场领导正在加速垂直整合以确保供应,例如卡特彼勒公司扩大其内部零件加工能力。如果供应瓶颈持续存在,施工机械市场将在库存恢復正常之前经历短期放缓,这可能会推迟设备更新週期。

细分市场分析

预计到2025年,挖土机将占据施工机械市场51.24%的份额,并在2031年之前以7.15%的复合年增长率成长。液压效率、快换工具和远端资讯处理技术的集成,正推动道路建设、公共产业和拆除工程领域对挖土机的持续需求。装载机销量位居第二,其中轮式装载机更适合铺路作业,而履带式装载机则更适合鬆软地面作业。起重机的需求与高层建筑和桥樑的施工进度密切相关,而平土机和压路机则以毫米级的精度维护路面。

推土机用于矿山台阶作业,这类作业需要高牵引力来保持边坡稳定性;而自动卸货卡车则用于运输500米以上的物料。混凝土泵浦和挖沟机等专用机械在施工机械市场中占据相当大的份额。日本小松公司的氢动力原型机预示着未来燃料多样化的发展方向,但要实现广泛应用,还需要扩大加氢基础设施。

到2025年,内燃机设备将占出货量的90.12%,但由于更严格的法规,混合动力和纯电动马达型的复合年增长率将达到22.16%。混合动力系统将小型柴油引擎与电池结合,可降低25%至35%的油耗,并在怠速或室内作业时实现安静、零排放运行。卡特彼勒323电动挖土机在併网改造工地运作成本低,并已获得大量订单,预计到2025年底交付。

在全球范围内,氢燃料电池挖土机的运作有限,主要集中在日本、德国和韩国的试验计画。 JCB的目标是规避燃料电池的相关成本,并在2027年实现氢燃料电池的商业化。零排放施工机械市场高度依赖电网容量和充电基础设施,因此,在可靠的能源供应广泛普及之前,一些买家更倾向于选择配备柴油引擎备用电源的混合动力机械。

区域分析

预计到2025年,亚太地区将以45.80%的市场份额引领施工机械市场,这主要得益于中国的「一带一路」倡议和印度的国家基础设施发展计画。预计到2027年,中国履带挖土机的产量将超过15万台,是2023年产量的两倍多,这将进一步增强供应商的规模经济效益。製造商正向东南亚和海湾合作委员会(GCC)地区的工地供应高功率柴油机械,同时向日本和韩国的城市出口小型电动装载机。

预计到2031年,中东和非洲地区将以9.12%的复合年增长率实现最高增长,沙乌地阿拉伯的「2030愿景」和阿联酋的「杜拜城市总体规划」将向住宅、旅游和物流行业注入数十亿美元资金。 2024年计划订单的大幅成长导致该地区设备供应紧张,促使原始设备製造商在杰贝阿里港设立临时进口堆场。沿岸地区施工机械市场的差异化优势在于耐热电池技术和密封驾驶室的过滤系统。

由于工业復兴法案(IRA)和城市基础设施保护与创新法案(CHIPS Acts)支持的再工业化和基础设施更新,北美市场依然强劲。美国环保署(EPA)第三阶段标准将于2027年车型年生效,这将推动小型城市公共设施设备朝向混合动力和电动化方向发展。租赁巨头们正透过数十亿美元的收购来扩大规模,导致经销商网路萎缩,进入费用上升。

其他福利:

- Excel格式的市场预测(ME)表

- 分析师支持(3个月)

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 亚洲各地的巨型基础设施项目每年推动超过2兆美元的资本需求。

- 美国《IRA法案》和《CHIPS法案》加快了为海岸重建计划购买土木机械的步伐

- 二级承包商转向优先租赁采购方式,提高了运转率。

- 欧盟第五阶段排放标准迫使车队快速更新换代,采用混合动力/电动设备

- 非洲矿产资源丰富地区关键原料开采的EPC计划数量迅速增加

- 人工智慧驱动的现场自动化有助于提高自动平土机和推土机的投资收益(ROI)。

- 市场限制

- 液压元件短缺导致OEM前置作业时间突然延长(超过42週)

- 锂离子电池供不应求推高了电动重型设备的总拥有成本 (TCO)。

- 拉丁美洲持续存在的技能差距限制了车载资讯服务设备的普及应用。

- 由于地方噪音管制条例,柴油钻机夜间运作受到限制

- 价值/价值链分析

- 监理展望

- 技术展望

- 波特五力分析

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模及成长预测(价值(美元)及销售量(单位))

- 透过装置

- 挖土机

- 装载机

- 移动式起重机

- 平土机机

- 推土机

- 压路机

- 自动卸货卡车

- 其他的

- 依推进类型

- 内燃机

- 混合动力汽车车和纯电动车

- 氢燃料电池

- 按设施规模

- 重型(超过11吨)

- 中型(6至11吨)

- 小型/迷你型(小于6吨)

- 透过输出

- 最高可达250马力

- 250-500马力

- 超过500马力

- 透过使用

- 基础设施

- 住宅及商业建筑

- 采矿和采石

- 石油和天然气/管道

- 工业和製造业

- 其他的

- 按地区

- 北美洲

- 我们

- 加拿大

- 北美其他地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 瑞典

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 印尼

- 亚太其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 南非

- 奈及利亚

- 埃及

- 其他中东和非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Caterpillar Inc.

- Komatsu Ltd.

- Deere & Company

- Hitachi Construction Machinery Co., Ltd.

- Volvo Construction Equipment

- CNH Industrial(CASE, New Holland)

- Liebherr-International AG

- Bobcat Company

- Kobelco Construction Machinery Co., Ltd.

- SANY Group

- Xuzhou Construction Machinery Group Co., Ltd.

- Zoomlion Heavy Industry Science & Technology Co., Ltd.

- JCB Limited

- HD Hyundai Infracore Co., Ltd.

- Terex Corporation

- Astec Industries, Inc.

- Kubota Corporation

- Sumitomo(HSC Cranes)

第七章 市场机会与未来展望

The construction equipment market stands at USD 205.38 billion in 2026 and is forecast to climb to USD 283.22 billion by 2031, registering a 6.64% CAGR during the period, underscoring steady gains in market size and profit pools.

Robust government spending on roads, rail, power transmission, and semiconductor fabs underpins demand across earthmoving, material-handling, and concrete machinery. Asia's mega-project pipeline, the electrification push in Europe and North America, and the industry-wide tilt toward rental fleets jointly reinforce a resilient growth outlook. Competitive intensity is sharpening as Chinese OEMs capture share abroad while Western leaders pivot to service-centric offerings and autonomous technologies. The construction equipment market is also shaped by quicker fleet renewal cycles driven by Stage V and EPA Phase 3 regulations, tightening the gap between product and digital service launches.

Global Construction Equipment Market Trends and Insights

Mega-infrastructure Pipelines Across Asia driving Over USD 2 tn Annual Equipment Demand

A committed project pipeline exceeding USD 3.7 trillion is transforming allocation priorities, pulling large dozers, 45-ton excavators, and high-capacity concrete pumps into Asian depots ahead of other regions. Saudi Arabia alone awarded USD 55 billion in projects in 2024, a 57% jump year-on-year, while the UAE lifted awards by 200% to USD 34 billion. OEMs are tailoring sales mixes toward higher horsepower and longer-reach booms, anchoring revenue in the construction equipment market through larger ticket sizes and aftermarket contracts.

U.S. IRA and CHIPS Acts Accelerating Earth-Moving Purchases for On-shoring Projects

Federal incentives for semiconductor fabs, EV plants, and grid upgrades have created a structural pull for 250-500 HP dozers and excavators across the Sun Belt. The American Society of Civil Engineers identifies a USD 3.7 trillion infrastructure gap by 2035, ensuring sustained visibility for OEM order books. Contractors, faced with labor constraints, are leaning toward larger units that compress project schedules and ease per-hour operating budgets.

OEM Lead-time Spikes (Beyond 42 Weeks) Due to Hydraulic Component Shortages

Delivery windows stretch beyond 42 weeks for critical hydraulic valves and pumps, forcing contractors to adjust project phasing. Market leaders increasingly vertically integrate to secure supply, echoing Caterpillar's expanded in-house component machining. Persistent bottlenecks threaten to defer replacement cycles and dampen near-term construction equipment market momentum until inventories normalize.

Other drivers and restraints analyzed in the detailed report include:

- Rental-first Procurement Shift Among Tier-2 Contractors Expanding Utilization Rates

- EU Stage V Emission Caps forcing Rapid Fleet Renewal Toward Hybrid/E-equipment

- Lithium-ion Cell Scarcity Inflating TCO of Electric Heavy Machinery

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Excavators commanded 51.24% construction equipment market share in 2025 and are projected to register a 7.15% CAGR to 2031. Hydraulic efficiency, quick-attach tooling, and telematics integration sustain demand across road-building, utilities, and demolition. Loaders remain second in volume, with wheel loaders favored for paved operations and track loaders for soft terrain. Crane demand follows high-rise and bridge timelines, while graders and rollers maintain road surfaces to millimeter tolerances.

Bulldozers thrive in mining benches where slope stability requires significant drawbar pull, and dump trucks handle hauls beyond 500 meters. Specialty machines, including concrete pumps and trenchers, together hold a significant share of construction equipment market size. Komatsu's hydrogen-powered prototype signals future fuel diversification, though widespread adoption awaits refueling infrastructure expansion .

Internal combustion units accounted for 90.12% of 2025 shipments, yet hybrids battery electric models will rise at 22.16% CAGR as regulations tighten. Hybrid systems pair smaller diesel engines with batteries, cutting fuel by 25-35% and enabling quiet, zero-tailpipe operation for idling and indoor work. Caterpillar's 323 electric excavator delivered lower operating costs on grid-connected redevelopment jobs and logged significant orders by end-2025 .

Globally, hydrogen fuel-cell rigs are operational in limited numbers, primarily in pilot programs across Japan, Germany, and South Korea. JCB is sidestepping the costs associated with fuel cells, aiming to commercialize its hydrogen combustion engine by 2027. The market for zero-emission construction equipment is closely tied to grid capacity and charging infrastructure. As a result, some buyers are leaning towards hybrids, which offer a diesel fallback until a reliable power source is widely available.

The Construction Equipment Market Report is Segmented by Equipment Type (Excavator, Loader, and More), Propulsion Type (Internal Combustion, Hybrid Battery Electric, and More), Equipment Size (Heavy (Above 11 Tons), Medium (6-11 Tons), and More), Power Output (Up To 250 HP, 250 - 500 HP, and More), Application, and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Geography Analysis

Asia Pacific led with 45.80% of the construction equipment market in 2025, underpinned by China's Belt and Road Initiative and India's National Infrastructure Pipeline. Chinese crawler excavator volumes are set to exceed 150,000 units by 2027, more than doubling 2023 output and reinforcing supplier economies of scale. Manufacturers route high-power diesel inventory to Southeast Asia and GCC job sites while shipping compact electric loaders to Japanese and Korean cities.

The Middle East and Africa posts the fastest trajectory at 9.12% CAGR through 2031 as Saudi Arabia's Vision 2030 and the UAE's Dubai Urban Master Plan funnel billions into housing, tourism, and logistics. Project awards jumped significantly in 2024, tightening regional equipment supply and prompting OEMs to stage temporary import yards at Jebel Ali Port. Heat-tolerant battery chemistries and sealed cabin filtration systems are differentiators in the Gulf slice of the construction equipment market.

North America maintains a solid outlook propelled by industrial reshoring and infrastructure revamps backed by the IRA and CHIPS legislation. EPA Phase 3 standards, effective model year 2027, are nudging fleets toward hybrid and electric compact equipment for urban utility work. Rental giants consolidate to secure scale, evidenced by multi-billion-dollar acquisitions that compress dealer networks and elevate access fees.

- Caterpillar Inc.

- Komatsu Ltd.

- Deere & Company

- Hitachi Construction Machinery Co., Ltd.

- Volvo Construction Equipment

- CNH Industrial (CASE, New Holland)

- Liebherr-International AG

- Bobcat Company

- Kobelco Construction Machinery Co., Ltd.

- SANY Group

- Xuzhou Construction Machinery Group Co., Ltd.

- Zoomlion Heavy Industry Science & Technology Co., Ltd.

- JCB Limited

- HD Hyundai Infracore Co., Ltd.

- Terex Corporation

- Astec Industries, Inc.

- Kubota Corporation

- Sumitomo (HSC Cranes)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mega-infrastructure Pipelines Across Asia driving Over USD 2 tn Annual Equipment Demand

- 4.2.2 U.S. IRA and CHIPS Acts Accelerating Earth-Moving Purchases for On-shoring Projects

- 4.2.3 Rental-first Procurement Shift Among Tier-2 Contractors Expanding Utilization Rates

- 4.2.4 EU Stage V Emission Caps forcing Rapid Fleet Renewal Toward Hybrid/E-equipment

- 4.2.5 Mineral-rich Africa's EPC Surge for Critical Raw-material Extraction

- 4.2.6 AI-enabled Job-site Automation Boosting ROI of Autonomous Graders and Dozers

- 4.3 Market Restraints

- 4.3.1 OEM Lead-time Spikes (Beyond 42 Weeks) Due to Hydraulic Component Shortages

- 4.3.2 Lithium-ion Cell Scarcity Inflating TCO of Electric Heavy Machinery

- 4.3.3 Persistent Skills Gap Limiting Adoption of Telematics-rich Equipment in LATAM

- 4.3.4 Municipal Noise-abatement Bylaws Restricting Night-time Operation of Diesel Rigs

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value (USD) and Volume (Units))

- 5.1 By Equipment Type

- 5.1.1 Excavator

- 5.1.2 Loader

- 5.1.3 Mobile Cranes

- 5.1.4 Motor Graders

- 5.1.5 Bulldozers

- 5.1.6 Road Rollers

- 5.1.7 Dump Trucks

- 5.1.8 Others

- 5.2 By Propulsion Type

- 5.2.1 Internal Combustion

- 5.2.2 Hybrid Battery Electric

- 5.2.3 Hydrogen Fuel-Cell

- 5.3 By Equipment Size

- 5.3.1 Heavy ( Above 11 tons)

- 5.3.2 Medium (6-11 tons)

- 5.3.3 Compact/Mini (less than 6 tons)

- 5.4 By Power Output

- 5.4.1 Up to 250 HP

- 5.4.2 250 - 500 HP

- 5.4.3 Above 500 HP

- 5.5 By Application

- 5.5.1 Infrastructure

- 5.5.2 Residential and Commercial Construction

- 5.5.3 Mining and Quarrying

- 5.5.4 Oil and Gas/Pipelines

- 5.5.5 Industrial and Manufacturing

- 5.5.6 Others

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Sweden

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 Indonesia

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Turkey

- 5.6.5.4 South Africa

- 5.6.5.5 Nigeria

- 5.6.5.6 Egypt

- 5.6.5.7 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Caterpillar Inc.

- 6.4.2 Komatsu Ltd.

- 6.4.3 Deere & Company

- 6.4.4 Hitachi Construction Machinery Co., Ltd.

- 6.4.5 Volvo Construction Equipment

- 6.4.6 CNH Industrial (CASE, New Holland)

- 6.4.7 Liebherr-International AG

- 6.4.8 Bobcat Company

- 6.4.9 Kobelco Construction Machinery Co., Ltd.

- 6.4.10 SANY Group

- 6.4.11 Xuzhou Construction Machinery Group Co., Ltd.

- 6.4.12 Zoomlion Heavy Industry Science & Technology Co., Ltd.

- 6.4.13 JCB Limited

- 6.4.14 HD Hyundai Infracore Co., Ltd.

- 6.4.15 Terex Corporation

- 6.4.16 Astec Industries, Inc.

- 6.4.17 Kubota Corporation

- 6.4.18 Sumitomo (HSC Cranes)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

橡胶压机市场:依橡胶类型、压机类型、操作模式、产能、应用及通路划分-全球预测,2026-2032年电动施工机械市场:依设备类型、推进系统和应用划分-全球预测,2026-2032年自动液压机市场:按压机类型、控制类型、操作模式和终端用户产业划分,全球预测,2026-2032年

橡胶压机市场:依橡胶类型、压机类型、操作模式、产能、应用及通路划分-全球预测,2026-2032年电动施工机械市场:依设备类型、推进系统和应用划分-全球预测,2026-2032年自动液压机市场:按压机类型、控制类型、操作模式和终端用户产业划分,全球预测,2026-2032年 2026 年至 2035 年施工机械轮胎市场的商业机会、成长要素、产业趋势分析与预测。

2026 年至 2035 年施工机械轮胎市场的商业机会、成长要素、产业趋势分析与预测。 东协施工机械:市场占有率分析、产业趋势与统计、成长预测(2026-2031)中国施工机械:市场占有率分析、产业趋势与统计、成长预测(2026-2031)泰国施工机械市场占有率分析、产业趋势及统计、成长预测(2026-2031)

东协施工机械:市场占有率分析、产业趋势与统计、成长预测(2026-2031)中国施工机械:市场占有率分析、产业趋势与统计、成长预测(2026-2031)泰国施工机械市场占有率分析、产业趋势及统计、成长预测(2026-2031) 2026年全球建筑及道路施工机械市场报告2026年全球施工机械市场报告2026年全球液压搭乘用电梯市场报告

2026年全球建筑及道路施工机械市场报告2026年全球施工机械市场报告2026年全球液压搭乘用电梯市场报告