|

市场调查报告书

商品编码

1939065

印刷标籤:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Print Label - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

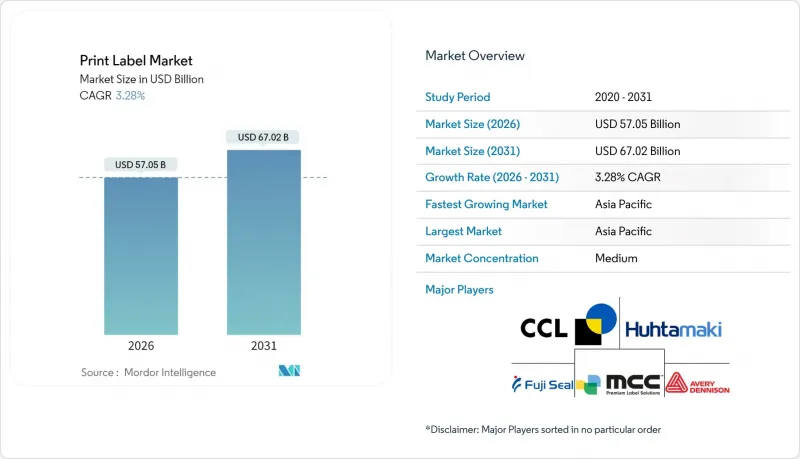

预计到 2026 年,印刷标籤市场价值将达到 570.5 亿美元,高于 2025 年的 552.4 亿美元。

预计到 2031 年将达到 670.2 亿美元,2026 年至 2031 年的复合年增长率为 3.28%。

这项稳定扩张反映了印刷业从纯粹的类比工艺向以永续性发展为导向、利用数位技术的生产模式的转变,后者能够降低最低订购量、缩短前置作业时间并减少材料废弃物。儘管柔版印刷仍占据最大的设备容量份额,但随着加工商寻求满足快速成长的SKU和电商标籤需求,喷墨系统正在迅速扩张。品牌所有者对无底纸印刷格式和智慧识别码的偏好,以及药品序列化和食品可追溯性的要求,正在重塑加工商的投资重点。儘管基材和黏合剂价格波动带来的成本压力将持续存在,但稳健的利润率将取决于混合数位-柔版工作流程、供应链整合以及符合循环经济原则的材料。

全球印刷标籤市场趋势与洞察

加速引进高速数位印刷机进行小批量生产

数位喷墨平台正为消费品品牌带来全新的SKU策略,因为低至500张的印量即可获利,而传统的柔版印刷则需要1万张的起印阈值。例如,R.R. Donnelley公司斥资2500万美元对其位于乔治亚的工厂进行升级改造,就体现了加工商为提高产能和可变数据柔软性而投入的巨额资本。混合喷墨和柔版印刷塔式生产线简化了换版流程,但也造成了操作人员技能方面的差距,柔版印刷技术协会等行业组织正透过其FIRST 5.0课程来解决这个问题。随着高速数位生产效率和类比经济效益的融合,印刷标籤市场将朝着混合技术生产单元的方向发展,从而缩短前置作业时间和减少库存。

品牌所有者转向无底纸标籤以减少废弃物

取消离型纸可减少高达 30% 的标籤废弃物,并提高捲筒密度,从而降低物流成本,并有助于提升永续发展指标。市场领导报告称,无离型纸标籤的销售额实现了两位数的成长,其中生产者延伸责任制 (EPR) 的成本推动了其普及,尤其是在食品零售业。转型面临的障碍包括专用应用设备和能够在湿度波动条件下保持良好性能的黏合剂配方,但供应商正在扩大产能。 UPM Raflatac 报告称,2025 年第一季环比成长 13%,部分原因是欧洲对无离型纸标籤的需求。加工商的竞争优势取决于掌握与传统压敏黏着剂工作流程不同的新型涂布和分切技术。

原物料价格波动对加工企业的利润率带来压力。

预计从2024年起,纸浆和造纸、PET以及丙烯酸黏合剂的价格指数将继续出现两位数的波动,这将使加工商极易受到原材料成本的影响,而原材料成本占销货成本的比例高达75%。全球性企业正在利用避险策略和规模经济效应,而艾利丹尼森公司虽然销售额下降了0.1%,但透过成本控制维持了息税前利润。规模较小的加工商难以将年度合约中的附加费转嫁给品牌所有者。像索诺科这样的综合性公司正在投资3,000万美元扩大黏合剂产能,以确保供应并减轻原物料价格波动的影响。在基材市场稳定之前,利润率的下降可能会抑制小型公司在印刷标籤市场的投资。

细分市场分析

喷墨技术5.3%的复合年增长率凸显了其在重塑印刷标籤市场中的重要角色。儘管柔印凭藉其成熟的製版生态系统仍然占据大批量SKU的大部分份额,但喷墨技术对承印物的适应性以及一键式换版功能,使加工商能够获得高利润的小批量订单,用于促销宣传活动。随着设备成本的下降和白色油墨不透明度接近丝网印刷质量,与喷墨印刷相关的印刷标籤市场规模预计将稳定成长。在加工商中,混合配置——将喷墨印刷机添加到柔印生产线——正成为资本投资计划的主流,它既能支持可变数据,又能保持成熟的模拟模切工作流程。

Astronova 的 Trojan 标籤平台(在 2024 年德鲁巴印刷展上发布)面向中等宽度标籤市场,旨在为精酿饮料和化妆品加工商提供媲美胶印的套准精度和极简的设置。凹版印刷在超长标籤生产领域仍占据优势,尤其受到大型饮料代工企业的青睐,但随着 UV 喷墨印刷能够达到与 Pantone 色卡相媲美的覆盖率,胶印的市场份额正在萎缩。丝网印刷技术在对薄膜厚度要求严格的耐用电子产品应用中仍将继续存在,但其在印刷标籤市场的份额将持续下降。

区域分析

亚太地区在2025年以35.86%的市占率主导印刷标籤市场,预计到2031年将以4.63%的复合年增长率维持最高成长。中国庞大的製造业基础和印度不断扩张的包装市场(2025年市场规模达2,048.1亿美元)是推动该地区成长的主要动力。当地加工商正投资中幅数位印刷机,以满足快速成长的消费品牌需求。同时,日本和韩国政府的回收政策推动了可再生基材和可水洗油墨的应用。东南亚国家正在转型为电商履约中心,刺激了对热转印运输标籤和QR码退货标籤的需求。

北美是技术领域的标竿地区,大型零售商的强制要求推动了云端连接RFID标籤的快速普及。 2024年,树脂价格下跌带来的利润压力影响了营收,但加工商透过自动化和高价值应用抵消了这些不利因素。 2024年11月药品序列化截止日期正在加速美国工厂的硬体更新换代,从而提升智慧标籤在印刷标籤市场的渗透率。

欧洲正经历成熟的需求与严格的循环经济法规并存的局面。在法国和德国,生产者延伸责任制(EPR)促进了无衬纸和单一材料结构的推广。英国的强制性法规指导着薄壁和可回收性的发展,并刺激了无溶剂黏合剂的研发。东欧的加工商正吸引来自欧盟各地品牌的委託製造,这些品牌希望在不牺牲合规性的前提下提高成本效益。

拉丁美洲和中东及非洲的贡献规模虽小,但成长迅速。巴西和墨西哥正在扩大饮料收缩膜套标的生产能力,波湾合作理事会(GCC)国家正将业务多元化拓展至包装食品领域,进口技术诀窍和资本设备。儘管非洲市场面临贸易壁垒和基础设施限制,但行动商务的成长表明可变数据标籤解决方案具有长期潜力。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 加速引进能够处理短交货时间和SKU多样化的高速数位(喷墨)印表机

- 品牌所有者正在转向使用背衬压敏标籤,以减少废弃物和物流成本。

- 电子商务的快速成长推动了对可变数据运输和退货标籤的需求

- 监管机构推动使用智慧/条码标籤,以实现端到端的可追溯性(例如,欧盟药品防伪指令、美国药品安全追踪法)

- 精酿饮品和高端食品市场的成长,对高端、精美标籤的需求也随之成长。

- 低温运输物流中用于食品安全的新型抗菌标籤涂层

- 市场限制

- 纸张、薄膜和黏合剂的价格波动正在给加工商的利润率带来压力。

- 中小加工企业缺乏操作混合式数位柔版印刷机的技能

- 品牌所有者越来越倾向于直接在包装上进行数位印刷(无需标籤)。

- 循环经济市场中多层收缩标籤与套模标籤回收的难题

- 产业价值链分析

- 监管环境

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 透过印刷工艺

- 胶印

- 凹版印刷

- 柔版印刷

- 萤幕

- 凸版印刷

- 静电照相术

- 喷墨

- 按标籤格式

- 湿胶标籤

- 感压标籤

- 无底纸标籤

- 多份追踪标籤

- 套模标籤

- 缩水/拉伸套

- 按最终用户行业划分

- 食物

- 饮料

- 医疗和药品

- 化妆品和个人护理

- 家用清洁用品

- 工业和汽车

- 物流与电子商务

- 电子设备/家用电器

- 按地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 澳洲

- 亚太其他地区

- 中东和非洲

- 中东

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 其他非洲地区

- 中东

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- CCL Industries Inc.

- Avery Dennison Corporation

- Multi-Color Corporation

- Fuji Seal International, Inc.

- Mondi plc

- Huhtamaki Oyj

- 3M Company

- Brady Corporation

- Ahlstrom-Munksjo Oyj

- Autajon Group

- Taghleef Industries LLC

- Ravenwood Packaging Ltd.

- SATO Holdings Corporation

- Taylor Corporation

- Weber Packaging Solutions, Inc.

- Resource Label Group, LLC

- Advanced Labelworx, Inc.

- Alliance Prints USA, Inc.

- Clarion Safety Systems, LLC

第七章 市场机会与未来展望

Print label market size in 2026 is estimated at USD 57.05 billion, growing from 2025 value of USD 55.24 billion with 2031 projections showing USD 67.02 billion, growing at 3.28% CAGR over 2026-2031.

Steady expansion reflects the sector's shift from purely analog processes to digitally enabled, sustainability-focused production frameworks that lower minimum order quantities, compress lead times, and cut material waste. Flexography still controls the largest share of installed capacity, yet inkjet systems are scaling rapidly as converters look to satisfy proliferating SKUs and e-commerce labeling needs. Brand owners' preference for linerless formats and intelligent identifiers, plus mandated pharmaceutical serialization and food traceability, is reshaping converter investment priorities. Cost pressure from substrate and adhesive volatility continues, but margin resilience hinges on hybrid digital-flexo workflows, supply-chain integration, and circular-economy compliant materials.

Global Print Label Market Trends and Insights

Accelerated Adoption of High-Speed Digital Presses for Short-Run Production

Digital inkjet platforms enable profitable runs as low as 500 pieces, contrasting with flexography's historical 10,000-unit threshold, thereby unlocking new SKU strategies for consumer brands. Capital outlays, such as R.R. Donnelley's USD 25 million Georgia upgrade, illustrate the scale converters commit to gain throughput and variable-data flexibility. Hybrid lines integrating inkjet and flexo towers streamline changeovers yet create operator-skill gaps that industry groups like the Flexographic Technical Association address through FIRST 5.0 curricula. As high-speed digital productivity converges with analog economics, the print label market will migrate toward mixed-technology production cells that compress lead times and inventory.

Brand-Owner Shift Toward Linerless Labels for Waste Reduction

Eliminating release liners cuts label waste up to 30% and boosts roll density, generating logistics savings that resonate with sustainability scorecards. Market leaders report double-digit linerless revenue growth, especially within food retail, where Extended Producer Responsibility fees spur adoption. Transition barriers include specialized applicators and adhesive formulations that must perform across humidity swings, but suppliers are scaling capacity. UPM Raflatac reported 13% quarter-on-quarter growth in Q1 2025, partly on European linerless demand. Converter competitiveness hinges on mastering new coating and slitting techniques that diverge from conventional pressure-sensitive workflows.

Raw Material Price Volatility Pressuring Converter Margins

Paper pulp, PET, and acrylic adhesive indices have swung by double digits since 2024, leaving converters exposed because materials account for up to 75% of cost of sales. While global players leverage hedging and scale, Avery Dennison reported a 0.1% sales dip yet preserved EBIT via cost controls, SME converters struggle to pass surcharges to brand owners under annual contracts. Consolidators such as Sonoco channel USD 30 million into adhesive capacity expansions to secure supply and dilute input swings. Until substrate markets stabilize, margin compression will temper investment appetite among smaller firms in the print label market.

Other drivers and restraints analyzed in the detailed report include:

- E-Commerce Expansion Driving Variable-Data Printing Demand

- Regulatory Traceability Requirements Accelerating Smart-Label Adoption

- Technical Skill Gaps in Hybrid Digital-Flexo Operations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Inkjet technology's 5.3% CAGR underscores its role in reshaping the print label market. Flexography still produces the bulk of long-run SKUs thanks to mature platemaking ecosystems, but inkjet's substrate versatility and 1-click changeovers let converters secure high-margin micro-runs for promotional campaigns. The print label market size associated with inkjet presses is forecast to grow steadily as equipment costs fall and white ink opacity rivals screen-print quality. Across converters, hybrid architectures that bolt inkjet bars onto flexo lines dominate capex roadmaps, enabling variable data without abandoning proven analog die-cutting workflows.

AstroNova's TrojanLabel platform, launched at Drupa 2024, typifies the mid-web category aimed at craft beverage and cosmetics converters seeking near-offset registration with minimal setup. Gravure's niche in ultra-long runs remains secure for large beverage co-packers, yet offset lithography's footprint narrows as UV-inkjet delivers comparable Pantone coverage. Screen technology survives in electronics durables where film thickness is critical, but its share within the print label market will continue to erode.

The Print Label Market Report is Segmented by Print Process (Offset Lithography, Gravure, Flexography, Screen, Letterpress, Electrophotography, and Inkjet), Label Format (Wet-Glue, Pressure-Sensitive, Linerless, Multi-Part Tracking, In-Mold, and Shrink and Stretch Sleeves), End-User Industry (Food, Beverage, Healthcare and Pharmaceuticals, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific dominated the print label market in 2025 with a 35.86% share and is projected to post the highest 4.63% CAGR to 2031. China's extensive manufacturing base and India's packaging expansion valued at USD 204.81 billion for 2025 underpin regional momentum. Local converters invest in mid-web digital presses to handle proliferating consumer brands, while government recycling mandates in Japan and South Korea encourage adoption of recyclable facestock and wash-off inks. Southeast Asian nations pivot toward e-commerce fulfillment hubs, stimulating demand for thermal shipping labels and QR-based return tags.

North America remains a technology bellwether, with rapid uptake of cloud-connected RFID labels driven by big-box retail mandates. Margin pressures from resin deflation challenged revenue in 2024, yet converters offset headwinds via automation and high-value applications. The region's pharma serialization deadline of November 2024 spurred hardware upgrades across U.S. plants, reinforcing smart-label penetration within the print label market.

Europe combines mature demand with stringent circular-economy rules. Extended Producer Responsibility fees in France and Germany favor linerless and mono-material constructions. The UK's Essential Requirements Regulations guide downgauging and recyclability, stimulating R&D into solvent-free adhesives. Eastern European converters attract contract manufacturing for pan-EU brands seeking cost efficiency without sacrificing regulatory compliance.

Latin America, the Middle East, and Africa account for smaller but rising contributions. Brazil and Mexico scale capacity for beverage shrink sleeves, while Gulf Cooperation Council members diversify into packaged foods, importing technical know-how alongside capital equipment. African markets grapple with trade barriers and infrastructure constraints, yet mobile commerce growth signals long-term potential for variable-data label solutions.

- CCL Industries Inc.

- Avery Dennison Corporation

- Multi-Color Corporation

- Fuji Seal International, Inc.

- Mondi plc

- Huhtamaki Oyj

- 3M Company

- Brady Corporation

- Ahlstrom-Munksjo Oyj

- Autajon Group

- Taghleef Industries LLC

- Ravenwood Packaging Ltd.

- SATO Holdings Corporation

- Taylor Corporation

- Weber Packaging Solutions, Inc.

- Resource Label Group, LLC

- Advanced Labelworx, Inc.

- Alliance Prints USA, Inc.

- Clarion Safety Systems, LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated adoption of high-speed digital (inkjet) presses for short-run, SKU-proliferated label jobs

- 4.2.2 Brand-owner shift toward linerless pressure-sensitive labels to cut waste and logistics costs

- 4.2.3 E-commerce boom driving demand for variable-data shipping and return labels

- 4.2.4 Regulatory push for smart/barcode labels enabling end-to-end traceability (e.g., EU FMD, U.S. DSCSA)

- 4.2.5 Growth of craft beverage and gourmet foods requiring premium, embellishment-rich labels

- 4.2.6 Emerging antimicrobial label coatings for food safety in cold-chain logistics

- 4.3 Market Restraints

- 4.3.1 Volatile paper, film and adhesive prices squeezing converter margins

- 4.3.2 Skill-gap in operating hybrid digital-flexo presses among SME converters

- 4.3.3 Rising brand-owner preference for direct-to-package digital printing (no label)

- 4.3.4 Difficult recycling of multi-layer shrink and in-mold labels in circular-economy markets

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Print Process

- 5.1.1 Offset Lithography

- 5.1.2 Gravure

- 5.1.3 Flexography

- 5.1.4 Screen

- 5.1.5 Letterpress

- 5.1.6 Electrophotography

- 5.1.7 Inkjet

- 5.2 By Label Format

- 5.2.1 Wet-Glue Labels

- 5.2.2 Pressure-Sensitive Labels

- 5.2.3 Linerless Labels

- 5.2.4 Multi-Part Tracking Labels

- 5.2.5 In-Mold Labels

- 5.2.6 Shrink and Stretch Sleeves

- 5.3 By End-User Industry

- 5.3.1 Food

- 5.3.2 Beverage

- 5.3.3 Healthcare and Pharmaceuticals

- 5.3.4 Cosmetics and Personal Care

- 5.3.5 Household Cleaning

- 5.3.6 Industrial and Automotive

- 5.3.7 Logistics and E-commerce

- 5.3.8 Electronics and Appliances

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 United Kingdom

- 5.4.3.2 Germany

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 Asia Pacific

- 5.4.4.1 China

- 5.4.4.2 Japan

- 5.4.4.3 India

- 5.4.4.4 South Korea

- 5.4.4.5 Australia

- 5.4.4.6 Rest of Asia Pacific

- 5.4.5 Middle East and Africa

- 5.4.5.1 Middle East

- 5.4.5.1.1 United Arab Emirates

- 5.4.5.1.2 Saudi Arabia

- 5.4.5.1.3 Turkey

- 5.4.5.1.4 Rest of Middle East

- 5.4.5.2 Africa

- 5.4.5.2.1 South Africa

- 5.4.5.2.2 Nigeria

- 5.4.5.2.3 Rest of Africa

- 5.4.5.1 Middle East

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 CCL Industries Inc.

- 6.4.2 Avery Dennison Corporation

- 6.4.3 Multi-Color Corporation

- 6.4.4 Fuji Seal International, Inc.

- 6.4.5 Mondi plc

- 6.4.6 Huhtamaki Oyj

- 6.4.7 3M Company

- 6.4.8 Brady Corporation

- 6.4.9 Ahlstrom-Munksjo Oyj

- 6.4.10 Autajon Group

- 6.4.11 Taghleef Industries LLC

- 6.4.12 Ravenwood Packaging Ltd.

- 6.4.13 SATO Holdings Corporation

- 6.4.14 Taylor Corporation

- 6.4.15 Weber Packaging Solutions, Inc.

- 6.4.16 Resource Label Group, LLC

- 6.4.17 Advanced Labelworx, Inc.

- 6.4.18 Alliance Prints USA, Inc.

- 6.4.19 Clarion Safety Systems, LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

美国印刷标籤:市场占有率分析、产业趋势与统计、成长预测(2026-2031 年)

美国印刷标籤:市场占有率分析、产业趋势与统计、成长预测(2026-2031 年) 印刷标籤市场报告:按原料、印刷工艺、标籤格式、最终用途行业和地区划分(2026-2034年)

印刷标籤市场报告:按原料、印刷工艺、标籤格式、最终用途行业和地区划分(2026-2034年) 2026年全球印刷标籤市场报告北美印刷标籤市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

2026年全球印刷标籤市场报告北美印刷标籤市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 印刷组件和标籤(热转印、数位印刷、网版印刷):全球市场份额和排名、总收入和需求预测(2025-2031 年)日本印刷标籤市场规模、份额、趋势及预测(按原材料、印刷工艺、标籤格式、最终用途行业和地区),2025 年至 2033 年

印刷组件和标籤(热转印、数位印刷、网版印刷):全球市场份额和排名、总收入和需求预测(2025-2031 年)日本印刷标籤市场规模、份额、趋势及预测(按原材料、印刷工艺、标籤格式、最终用途行业和地区),2025 年至 2033 年 印刷标籤市场规模、份额及成长分析(依印刷製程、标籤格式、原料、最终用途产业、地区及细分市场预测),2025 年至 2032 年

印刷标籤市场规模、份额及成长分析(依印刷製程、标籤格式、原料、最终用途产业、地区及细分市场预测),2025 年至 2032 年 2025-2029年全球印刷标籤市场

2025-2029年全球印刷标籤市场 印刷标籤市场:按标籤格式、印刷工艺、最终用户产业和地区划分标籤印刷和贴标设备:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)

印刷标籤市场:按标籤格式、印刷工艺、最终用户产业和地区划分标籤印刷和贴标设备:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)